AVPT - AvePoint: Operating Leverage Doesn't Excite Me Just Yet

2023-08-18 07:06:22 ET

Summary

- AvePoint offers SaaS platform solutions for cloud architecture and data organization.

- The company has achieved significant growth in revenues.

- Although AVPT operates at a loss, further growth could have significant operating leverage raising AvePoint's margins significantly.

- Although the growth story is interesting, high dilution, my DCF model estimates and insider sales point me toward a hold rating.

AvePoint ( AVPT ) offers SaaS platform solutions around cloud architecture and data organization. I believe the company is currently priced for a reasonable amount of growth. As the company's bottom line remains negative for the time being, I have a hold-rating for the stock after the stock has had a massive rally in 2023.

The Company

AvePoint, the SaaS and platform solution provider, has a list of offerings that they provide:

AvePoint's Offering (avepoint.com)

Most of the company's offering revolves around data management with third-party cloud vendors such as AWS, and Microsoft Azure.

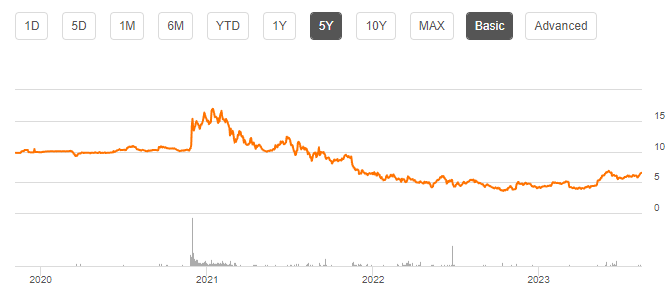

AvePoint became a listed company in late 2020, as the company merged with a SPAC:

{kind=link}

The stock price took a quick jump, which ultimately slowed down with a selloff in 2021 and 2022. The stock has taken off again, as its price has jumped 55% year-to-date.

Financials

AvePoint has achieved a good amount of growth in its history, as the company's revenues have grown by a compounded annual rate of 21.3% from 2018 to 2022:

AvePoint's Revenues (Seeking Alpha)

The growth seems to continue, as AvePoint's recently reported Q2 results had a growth of 16.5%, with trailing revenues currently being at around $251 million.

AvePoint achieved growth is both critical and valuable for the company - for the time being, AvePoint has a negative operating profit of -$27.39 million in trailing numbers. The company's bottom line is improving with growth, though - operating losses have shrunk from 2021's -$53 million into the current figure. AvePoint has a good gross margin of 71.2% in typical SaaS manner, and as the company scales its revenues, it realizes significant operating leverage. With the company's current growth rate, I believe AvePoint could achieve a positive margin in 2024.

As AvePoint currently doesn't have strong cash flows, the company has opted to finance its operations through equity - the company has no outstanding interest-bearing debt . The company also has a strong cash balance of $223 million. I believe this could change in the future, as AvePoint reaches good profitability and is able to pay off debt better.

A worrying sign for investors is the company's rapid dilution; in 2020, the company had 89.6 million outstanding shares, whereas today the outstanding amount stands at 185.4 million. I believe this is mainly caused by the company's excessive stock-based compensation - AvePoint's SBC is currently at a trailing figure of $36.2 million , below 2021 highs of $59.5 million but still at an unhealthy level in my opinion. The dilution is also partly due to the company's need to raise capital because of its negative cash flows - as AvePoint reaches profitability, I believe the dilution should slow down.

Valuation

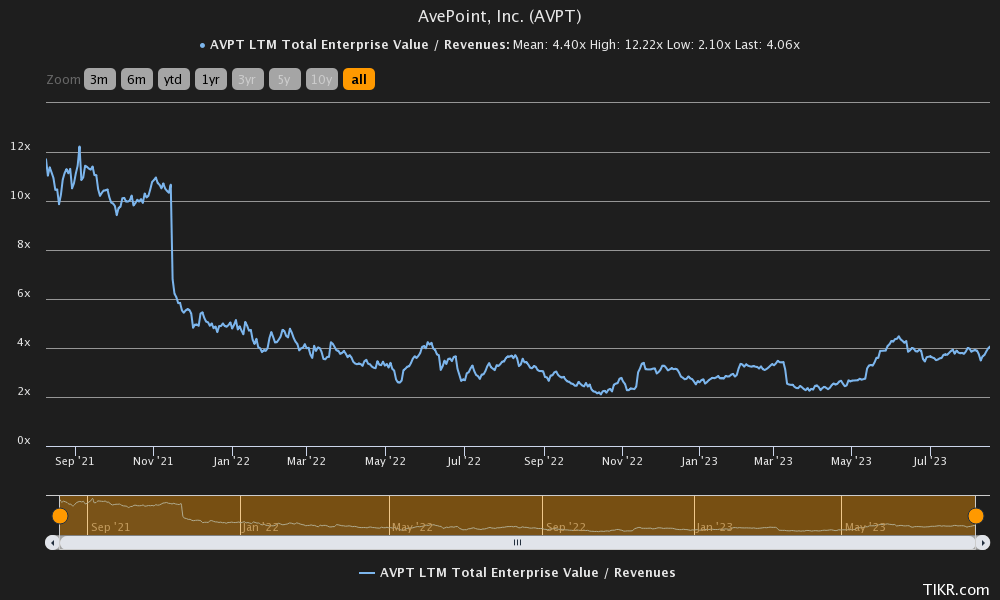

AvePoint's valuation has swung widely. The company reached an all-time high valuation of EV/S 12.22 in 2021 and a low of 2.10 in 2022, with the EV/S figure currently standing at 4.06:

{kind=link}

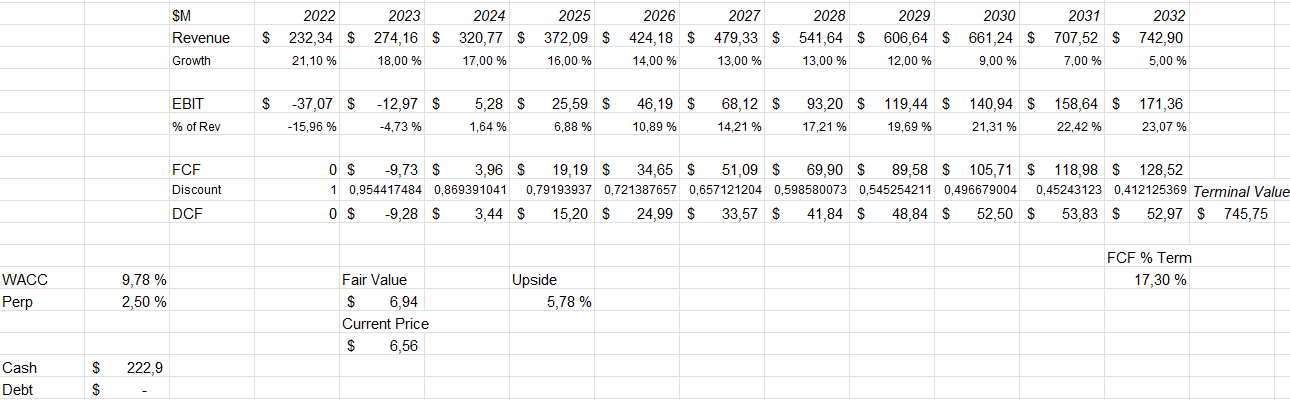

More importantly than revenues though, the company needs to be able to generate free cash flow to be a worthy investment. In my usual manner I modelled a discounted cash flow model to demonstrate the company's fair value estimate with moderate assumptions.

In the model I approximate AvePoint's growth to slow down very slowly, from a growth of 18% in 2023 to 5% in 2032 with small incremental steps. Beyond 2032 I have AvePoint's perpetual growth at 2.5% - slightly above my usual estimate of 2% as the company could still have operating leverage and growth beyond the year.

I believe AvePoint should achieve significant operating leverage - in the model I estimate the company's margin to grow towards a level of 23% in 2032. As the company doesn't seem to capitalize lots of investments, AvePoint's earnings should be well converted into free cash flow. These assumptions shape the following DCF model scenario with a fair value estimate of $6.94, six percent above the current level:

{kind=link}

The used weighed average cost of capital of 9.78% is derived using a capital asset pricing model with the following assumptions:

CAPM of AvePoint (Author's Calculation)

AvePoint currently has no interest-bearing debt, so I assumed an interest rate of six percent for the future - with the United States' 10-year bond yield standing at 4.31% at the time of writing, I believe this leaves a margin for error. As the company achieves positive cash flows, I believe the company could very well take a debt position that would amount to a debt-to-equity ratio of 10%.

As mentioned, the United States' 10-year bond yield is 4.31%, which I use as the risk-free rate on the cost of equity side. The used equity risk premium is Professor Aswath Damodaran's estimate made in July. TIKR estimates AvePoint's beta to be 0.94 , which I use in the model. These estimates craft a cost of equity of 10.37% and a WACC of 9.78%, used in the DCF model.

Insider Sales

The company doesn't come without warning signs - insiders have sold off a good amount of the stock in 2023:

Insider Sales in 2023 (Tikr)

Always a worrying sign, I believe the sales don't signal a good time to buy the stock; investors should be cautious about the company.

Takeaway

At $6.56 a share, I believe AvePoint is fairly priced considering the company's growth prospects. Although AvePoint is a good growth story with a good-quality offering, I believe investors should be wary of the stock as the company has seen large amounts of dilution, with insider sales increasing worries. With a DCF model scenario painting the estimated fair value around the stock's current price, I have a hold-rating for the stock.

For further details see:

AvePoint: Operating Leverage Doesn't Excite Me Just Yet