WRK - Avery Dennison Q4 2022 Earnings Preview: Shares Still Offer Upside From Here

Summary

- The management team at Avery Dennison is expected to report financial results covering the final quarter of the company's 2022 fiscal year.

- Leading up to that point, sales, profits, and cash flows have all been rising nicely.

- Shares of the company also look attractively priced, but investors should continue to keep an eye out for unexpected changes.

Buying companies that are in the packaging space may not seem like the most exciting way to make a profit. But in my opinion, packaging firms offer some of the best prospects at this point in time. One of the players in this space, a company that produces pressure-sensitive materials like papers, plastic films, metal foils, and fabrics, much of which are sold to label printers and converters that turn said products into labels and other offerings, is Avery Dennison ( AVY ). Historically speaking, the company has done well to grow on both its top and bottom lines. Relative to similar firms, the stock is a bit pricey. But on an absolute basis, it is still cheap enough to rate a ‘buy’. But of course, economic conditions are uncertain and volatile. And as a result, the picture for anyone firm or industry can change at a moment's notice. This makes it more important than ever for investors to pay special attention when firms report their financial results each quarter. It just so happens that, for Avery Dennison, the next earnings release will be on February 2nd before the market opens. Leading up to that point, investors should know what to expect and what to look out for.

Great results so far

The last article I wrote regarding Avery Dennison was published in late August of 2022. Leading up to that point, strong sales and profits had been instrumental in pushing shares of the company higher. On top of that, management was offering investors a more favorable view of the 2022 fiscal year than what they had previously. Ultimately, I concluded that shares of the company we're still fundamentally attractive and attractive from a price perspective. At the same time, however, I also recognized that the easy money had been made and that further upside from that point would be more limited. This still did not prevent me from rating the company a soft ‘buy’, a rating that reflects my view that shares should marginally outperform the broader market for the foreseeable future. While shares of the company are still up 14.3% compared to the 3.2% decline experienced by the S&P 500 when I wrote about the firm in March of last year, they have been virtually flat since my August article. By comparison, the S&P 500 has been up only modestly, posting a gain of 0.7%.

{kind=link}

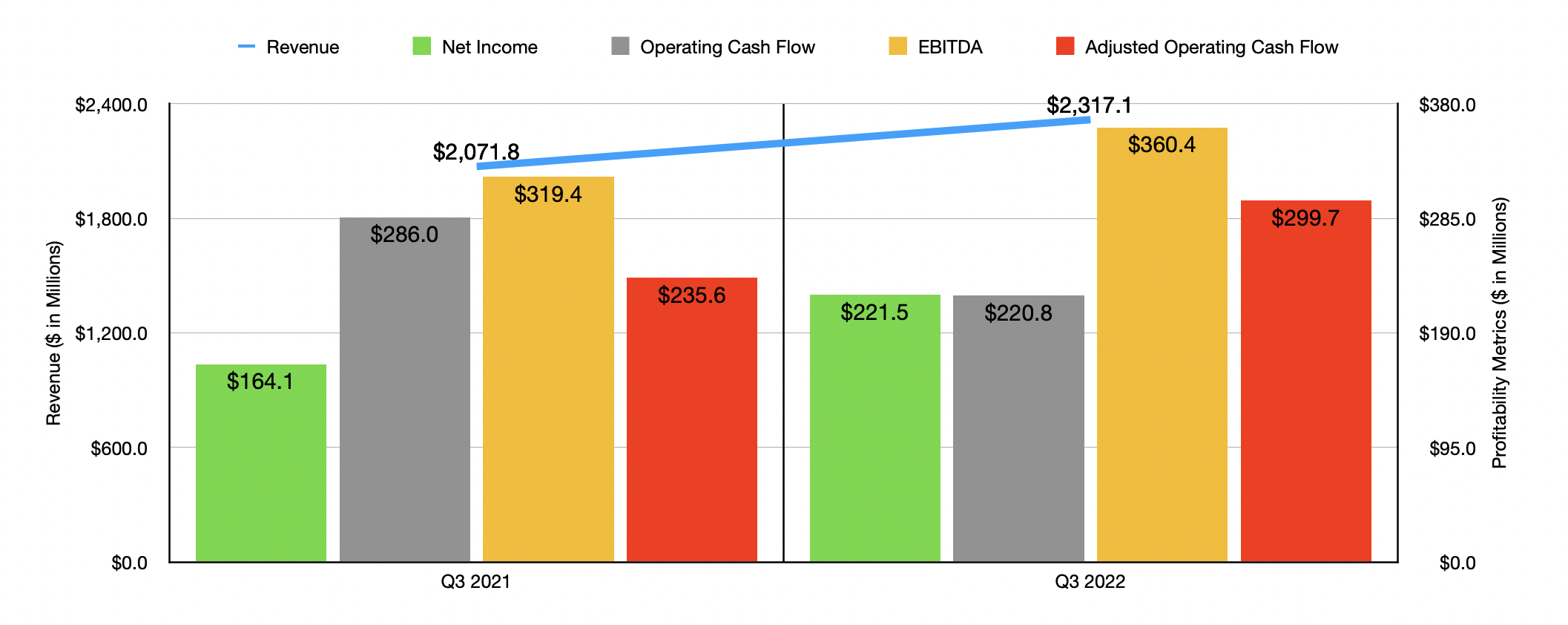

I know I mentioned already that the easy money had already been made. But truth be told, I am a bit surprised and how limited upside has been. Consider how the company performed during the third quarter of its 2022 fiscal year. During that time, sales came in at $2.32 billion. That represents an increase of 11.8% over the $2.07 billion generated one year earlier. This increase, though impressive, was not as impressive as it should have been. Overall sales for the Label and Graphic Materials segment of the company managed to climb roughly 12%, rising from $1.37 billion to $1.54 billion. But had it not been for pain associated with foreign currency translation, growth would have been 20%. The company also saw a 17% rise in sales for the Retail Branding and Information Solutions segment, with revenue jumping from $541.1 million to $633.2 million. Actual organic growth was only 7%. In this case, foreign currency actually added 5% to the segment’s top line, but the big driver was a 14% contribution caused by acquisitions.

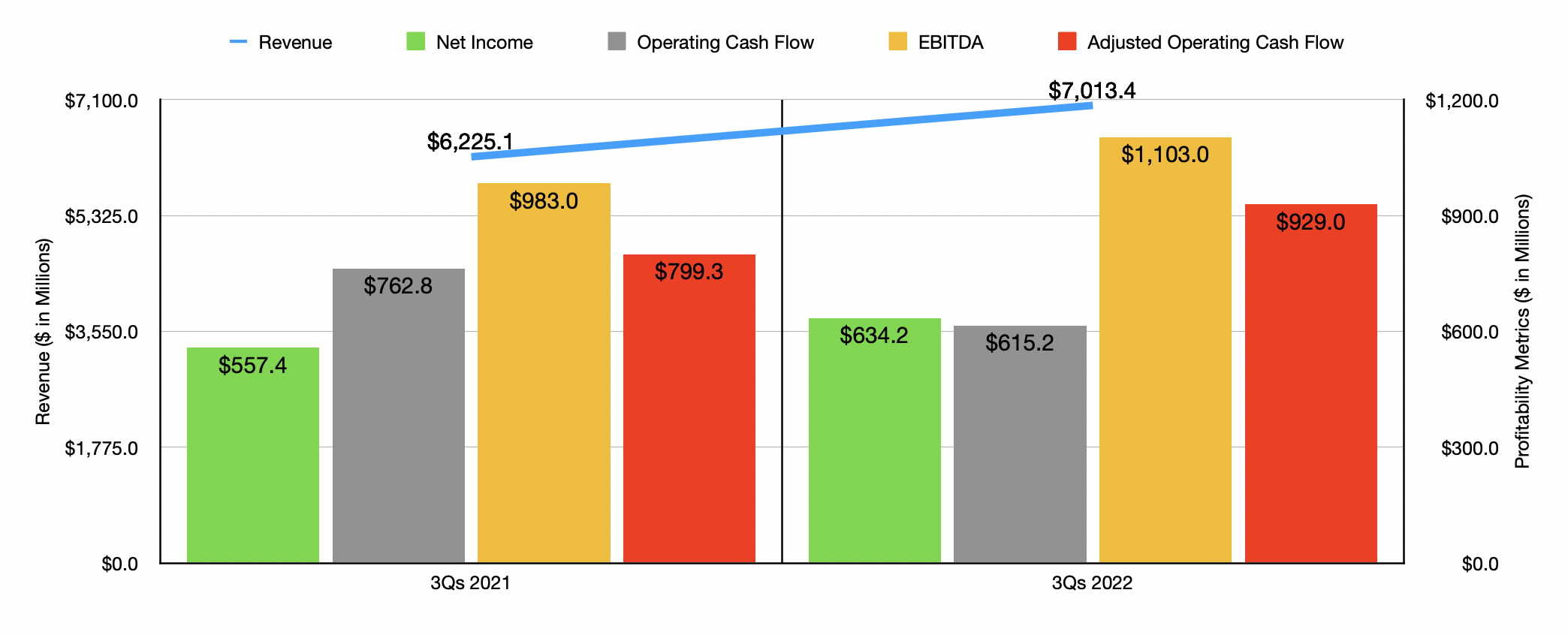

Profits for the company also increased during this window of time. Net income of $221.5 million dwarfed the $164.1 million reported in the third quarter of 2021. It is true that operating cash flow declined, dropping from $286 million to $220.8 million. But if we adjust for changes in working capital, it would have risen from $235.6 million to $299.7 million. Similarly, EBITDA for the company also improved, jumping from $319.4 million to $360.4 million. The third quarter is only a taste of how the company performed for 2022 as a whole. Revenue of $7.01 billion was meaningfully higher than the $6.23 billion reported for the first nine months of 2021. That income increased from $557.4 million to $634.2 million. Once again, operating cash flow took a hit too, dropping from $762.8 million to $615.2 million. But on an adjusted basis, it would have grown from $799.3 million to $929 million. And finally, EBITDA for the company increased from $983 million to $1.10 billion.

{kind=link}

Management has said that adjusted earnings per share for 2022 should be between $9.70 and $9.85. This compares to the prior expected range of between $9.70 and $10. Taking the midpoint, we would end up with a reading of around $800.6 million. If we also assume that the other profitability metrics will rise at the same rate the net income should, then we should anticipate adjusted operating cash flow of $1.24 billion and EBITDA of $1.47 billion. But of course, this kind of performance is contingent on how the company fared during the final quarter of the year. At present, analysts anticipate revenue of $2.17 billion. This would compare to the $2.18 billion the business reported one year earlier. This would actually be rather surprising given how strong the rest of 2022 looked for the company. When it comes to earnings, management gave a forecast for GAAP of $2.025 per share at the midpoint and an adjusted reading of $2.075 per share. Analysts, meanwhile, are estimating that official earnings will be only $1.98, while the adjusted figure would be $2.03. By comparison, at the same time one year earlier, official earnings were $2.19 per share, while adjusted earnings were $2.13.

{kind=link}

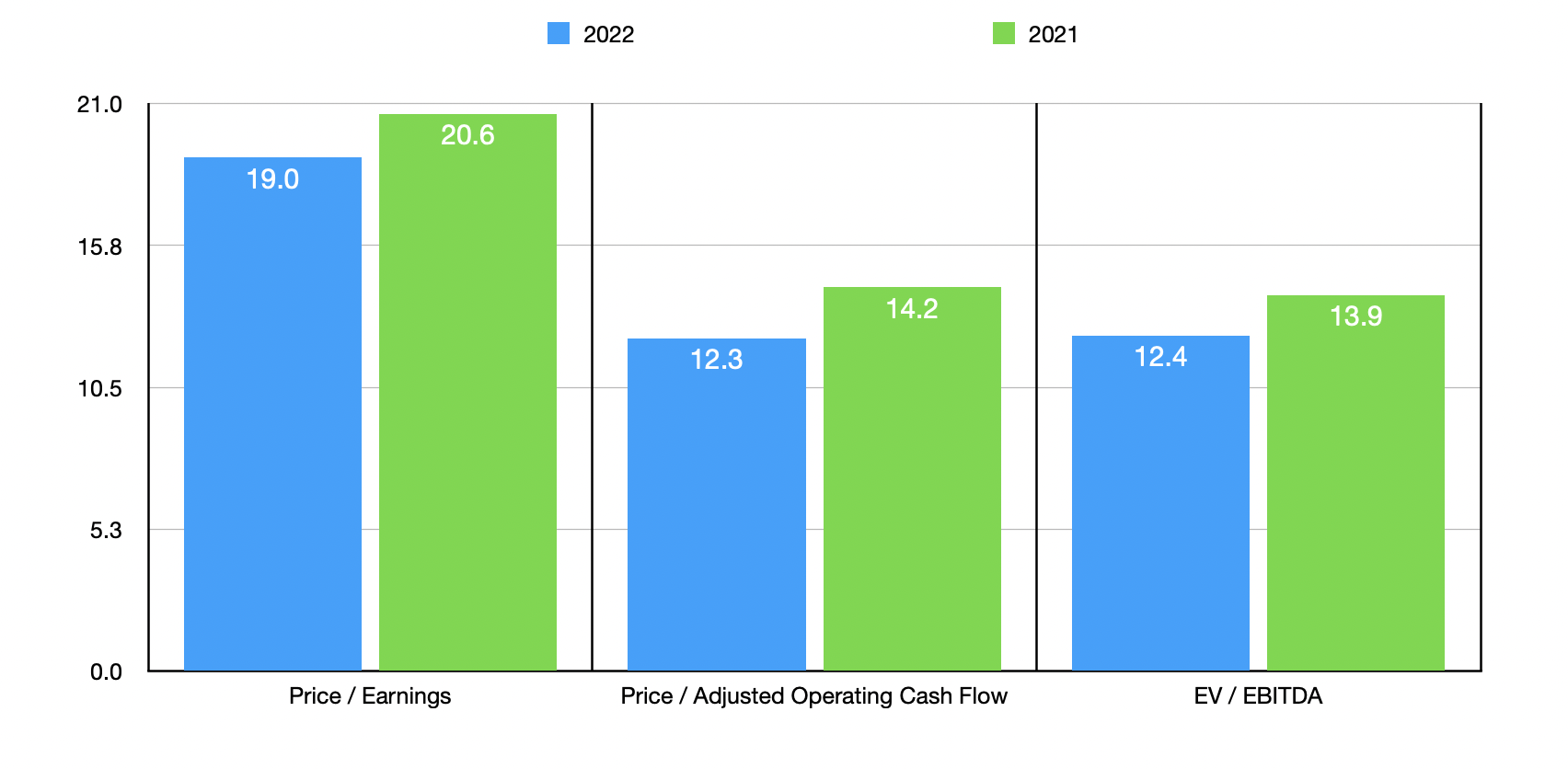

Using the estimates that I already provided, I calculated that the company is trading at a price-to-earnings multiple of 19. The price to adjusted operating cash flow multiple is 12.3, while the EV to EBITDA multiple should come in at 12.4. By comparison, if we were to use the data from the 2021 fiscal year, these numbers would be 20.6, 14.2, and 13.9, respectively. As part of my analysis, I did also compare the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 10.5 to a high of 18. And using the EV to EBITDA approach, the range should be from 5.5 to 9.8. In both of these cases, Avery Dennison was the most expensive of the group. When it comes to the price to operating cash flow approach, the range was from 4.9 to 14.8. In this scenario, four of the five companies were cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Avery Dennison |

| 19.0 |

| 12.3 |

| 12.4 |

| Sonoco Products ( SON ) |

| 13.7 |

| 14.8 |

| 9.5 |

| Packaging Corporation of America ( PKG ) |

| 12.6 |

| 8.8 |

| 7.0 |

| Graphic Packaging Holdings ( GPK ) |

| 18.0 |

| 9.5 |

| 9.8 |

| Sealed Air Corporation ( SEE ) |

| 13.7 |

| 12.1 |

| 9.5 |

| WestRock Company ( WRK ) |

| 10.5 |

| 4.9 |

| 5.5 |

Takeaway

Fundamentally speaking, Avery Dennison has been knocking it out of the park. By almost every measure, the company is doing very well. Unfortunately, this has led the market to assign a rather high price on shares compared to similar businesses. But on an absolute basis, the stock does not look overpriced, even though it might be a bit lofty compared to its competitors. certainly, the easy money has been made, but absent anything horrible happening during the final quarter of the year, I would anticipate that shares should rise a bit higher from where they are today. But of course, this picture could change based on the financial data reported in the next few days.

For further details see:

Avery Dennison Q4 2022 Earnings Preview: Shares Still Offer Upside From Here