AVES - AVES: Emerging Market Value Equities Outstanding Potential Returns Good Track Record

2023-12-12 23:29:25 ET

Summary

- Avantis Emerging Markets Value ETF is an actively managed emerging markets value ETF with a cheap valuation and above-average dividends.

- The fund focuses on China, Taiwan, India, and South Korea, but overweighting China poses significant risks.

- AVES has a subpar performance track record but is managed by Avantis, a firm with a proven strategy in value investing.

The Avantis Emerging Markets Value ETF ( AVES ) is an actively managed emerging markets value ETF. AVES offers investors an incredibly cheap valuation, above-average dividends, and consistent outperformance relative to emerging market benchmarks. I rate the fund a buy, but it is riskier than most and yields a lot less than funds of comparable risk.

AVES - Overview and Investment Thesis

Holdings and Strategy

AVES is an actively managed emerging market value ETF. The fund holds a diversified portfolio within its equity market niche, with investments in over 1400 emerging market equities. Concentration is quite low too, with the fund's top ten holdings accounting for just 9.2% of its portfolio.

AVES

AVES invests in dozens of countries but focuses quite strongly on China, Taiwan, India, and South Korea.

AVES

I'm wary of overweighting China, due to the country's deteriorating economy , adverse regulatory environment, and crackdown on private enterprise/investors. Overweighting China and Taiwan means significant losses if China invades Taiwan, which is possible . Even though I'm broadly bullish on AVES, these issues make the fund an incredibly risky investment, and broadly unsuitable for more risk-averse investors. Position sizes should be kept small too, in my opinion at least.

AVES provides investors with exposure to the most relevant industry segments, including tech, with a 16.7% allocation.

AVES

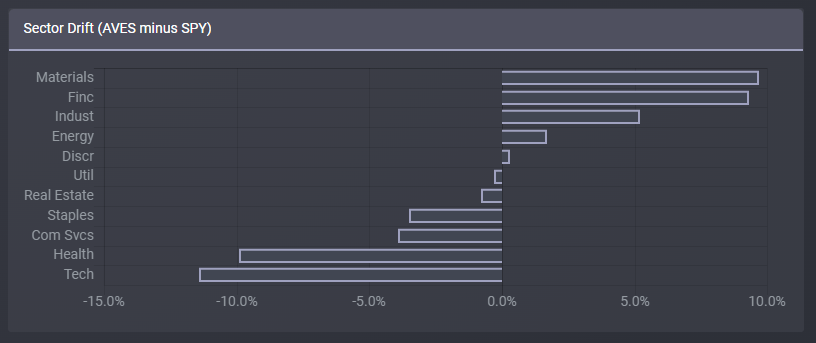

Relative to the S&P 500, AVES is overweight old-economy industries like materials and financials, but underweight growth, tech, and healthcare. These industry tilts are common in international, emerging markets, and value funds.

{kind=link}

AVES's industry tilts have a significant impact on the fund's performance, especially relative to the S&P 500. The fund tends to underperform when materials underperform and tech outperforms, as has been the case YTD.

On the flip side, the fund tends to outperform when materials outperform and tech underperforms, as was the case in 2022 (although barely so):

Data by YCharts

Besides the above, only one thing else stands out about the fund's strategy and holdings: its value focus. Let's have a look.

Cheap Valuation

AVES focuses on emerging market equities with comparatively cheap prices and valuations. As per management, book value and profitability to book are particularly important metrics for the fund. The latter metric is somewhat uncommon, but still reasonable and effective. AVES's valuation is much lower than that of broader emerging market equity indexes, as expected.

Morningstar - Chart by Author

Valuation gaps are much wider compared to U.S. equities, as emerging markets tend to trade with heavily discounted prices due to elevated levels of risk. Emerging markets are cheap, AVES' emerging market equities are doubly so. As per Morningstar, AVES trades with a +50% discount to the S&P 500, a self-evidently significant amount. Discounts to international equities are narrower, but still quite significant.

Morningstar - Chart by Author

Discounts are sometimes the result of weak growth prospects, but that does not seem to be the case for AVES. Expected growth is slightly higher than that of the S&P 500, and historical growth is a tad lower. Differences are small, however. Compare AVES's growth:

Morningstar

With that of the S&P 500:

Morningstar

AVES's cheap valuation could lead to significant capital gains and market-beating returns moving forward, contingent on valuations normalizing. In all honestly, I don't see any short-term catalyst for this, so prospective capital gains are incredibly uncertain, and might fail to materialize for years. Prospective gains are ultimately dependent on market sentiment, which is generally fickle, and not always rational.

AVES's cheap valuation boosts the positive impact / EPS accretion of any share buyback program. I'm sure the fund derives some tangible benefit from this, but the fund does not really target companies with significant buyback programs, nor are emerging market equities known for these.

AVES's cheap price directly boosts the fund's yield, which brings me to my next point.

Above-Average Dividends

AVES currently yields 3.4%. Although it is not a particularly strong yield on an absolute basis, or relative to high-yield fixed-income asset classes, it is higher than the average equity index fund.

Seeking Alpha - Table by Author

Higher dividends are almost always a benefit for investors, and AVES is no exception. AVES's higher dividends are also a reasonably certain benefit, insofar as these are not dependent on the market sentiment or expectations. Do remember that this is not the case for valuations or prospective capital gains.

Investors looking for emerging market equity funds with strong yields could consider an investment in the Cambria Emerging Shareholder Yield ETF ( EYLD ), with a 7.3% dividend yield. The iShares Latin America 40 ETF ( ILF ) is another solid choice, with a 9.1% yield. ILF obviously lacks the diversification offered by AVES and is much more dependent on commodity prices too.

Subpar Performance Track Record

Net, AVES's performance track record seems to be subpar. Although the fund consistently outperforms its benchmark, it matches the performance of broader international equity ETFs, and has significantly underperformed the S&P 500 since inception.

Seeking Alpha - Table by Author

Although AVES's performance is quite poor, I am much more bullish about the future. Remember, AVES is cheaper than the S&P 500, is seeing faster earnings growth, and yields more. Under these conditions, AVES should outperform moving forward, but obviously, the market might disagree.

Proven Strategy

AVES is administered by Avantis, a smaller investment management firm with a strong track record of successful value investing. Specifically, Avantis has several value equity ETFs available to investors, all of which have reasonably good performance track records, and most of which have outperformed their benchmark.

Their international value equity ETF has outperformed its benchmark:

Their U.S. large-cap value equity ETF has outperformed:

Their U.S. small-cap value equity ETF has outperformed:

Their international large-cap value equity ETF has outperformed:

Their global value equity ETF has outperformed:

Their broad-based U.S. value equity ETF has effectively matched, very slightly underperformed, its benchmark:

In my opinion, and considering the above, Avantis is clearly an effective value investor. Consistent outperformance across equity market segments, and during a period in which value has slightly underperformed, is proof enough.

Cheap Enough

As a final point, AVES sports a 0.36% expense ratio. It is a bit lower than average for an actively managed ETF focusing on a relatively small equity market segment. Index funds are generally cheaper, but AVES is cheap enough, in my opinion at least.

Conclusion

AVES offers investors an incredibly cheap valuation, above-average dividends, and consistent benchmark outperformance. The fund is a buy but is incredibly risky, and broadly unsuitable to risk-averse investors.

For further details see:

AVES: Emerging Market Value Equities, Outstanding Potential Returns, Good Track Record