AVNW - Aviat Networks: Looks Like It Will Continue To Trade Flat

Summary

- There is no significant near-term catalyst that could break AVNW out of the trading flat.

- Redline appears to be contributing to the top and bottom line quicker than management thought it would, so could be a longer term tailwind for the company.

- After the economy recovers I think the company is positioned well for incremental, long-term growth.

After hitting a 2-year high of approximately $44.00 per share, Aviat Networks, Inc. ( AVNW ), which provides microwave networking solutions to various markets around the world, has struggled to break out. After hitting a quadruple top from June 7, 2022, to August 9, 2021, the company has traded sideways after dropping to about $28.50 per share on November 11, 2021, and has since traded in a range of around $24.00 to $34.00.

{kind=link}

Since its last earnings report there were no observable catalysts that would be the type of tailwind that could sustainably break the company out of trading flat for so long.

The acquisition of Redline Communications is a potential long-term tailwind for the company, which over time, should allow for incremental growth. The other interesting win in the quarter was concerning its 5G win with Bharti Airtel in India.

It also reported a win with a "very large county government." Along with its microwave offering, the deal also included routers and hosted software. It'll be interesting to see how this adds to the performance of AVNW, and what the company meant by "very large county government." What I mean by that is whether or not a large county government translates into large country spending.

With a strong balance sheet and recent acquisition (its first in over a decade), AVNW is positioned to withstand economic softness, and if it chooses, to look for another acquisition, which will probably have to be the growth catalyst for the company if it wants to break out of its flat trading range.

In this article we'll look at some of its recent numbers, which were fairly solid, and what the probable blueprint will be to help the company regain growth momentum.

Some of the numbers

Revenue from the first fiscal quarter of 2023 was $81.3 million, up 11.1 percent or $8.1 million from the $73.2 million in revenue generated in the first fiscal quarter of 2022.

{kind=link}

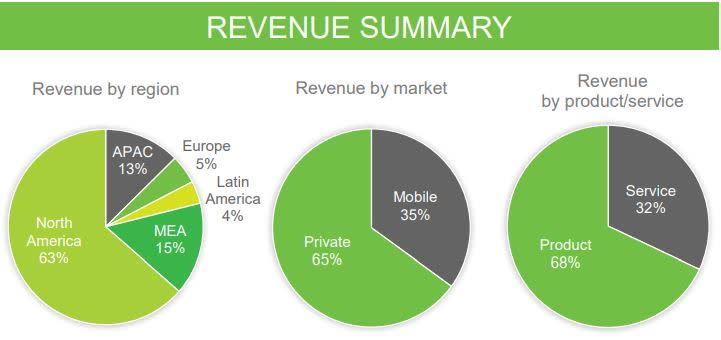

Product sales accounted for $55.1 million in revenue, while Services accounted for $26.2 million. Measured by market, Private represented 65 percent of sales and Mobile 35 percent.

{kind=link}

Gross margin on a GAAP basis was 36.3 percent in the reporting period, up from 35.7 percent year-over-year. Raising prices were the reason for the improvement in gross margin in the quarter, along with an immediate contribution from the Redline acquisition.

Operating expenses in the first fiscal quarter of 2023 were $25.5 million, up $6.2 million year-over-year, primarily from the acquisition costs associated with Redline.

Adjusted EBITDA in the quarter was $10.7 million, compared to adjusted EBITDA of $9.6 million in the first fiscal quarter of 2022. Adjusted EBITDA margin in the quarter was $13.2 percent, slightly up from 13.1 percent year-over-year.

Net loss in the reporting period was $(2.75) million, or $(0.25) per diluted share, compared to net income of $4.7 million, or $0.39 per diluted share in the first fiscal quarter of 2022.

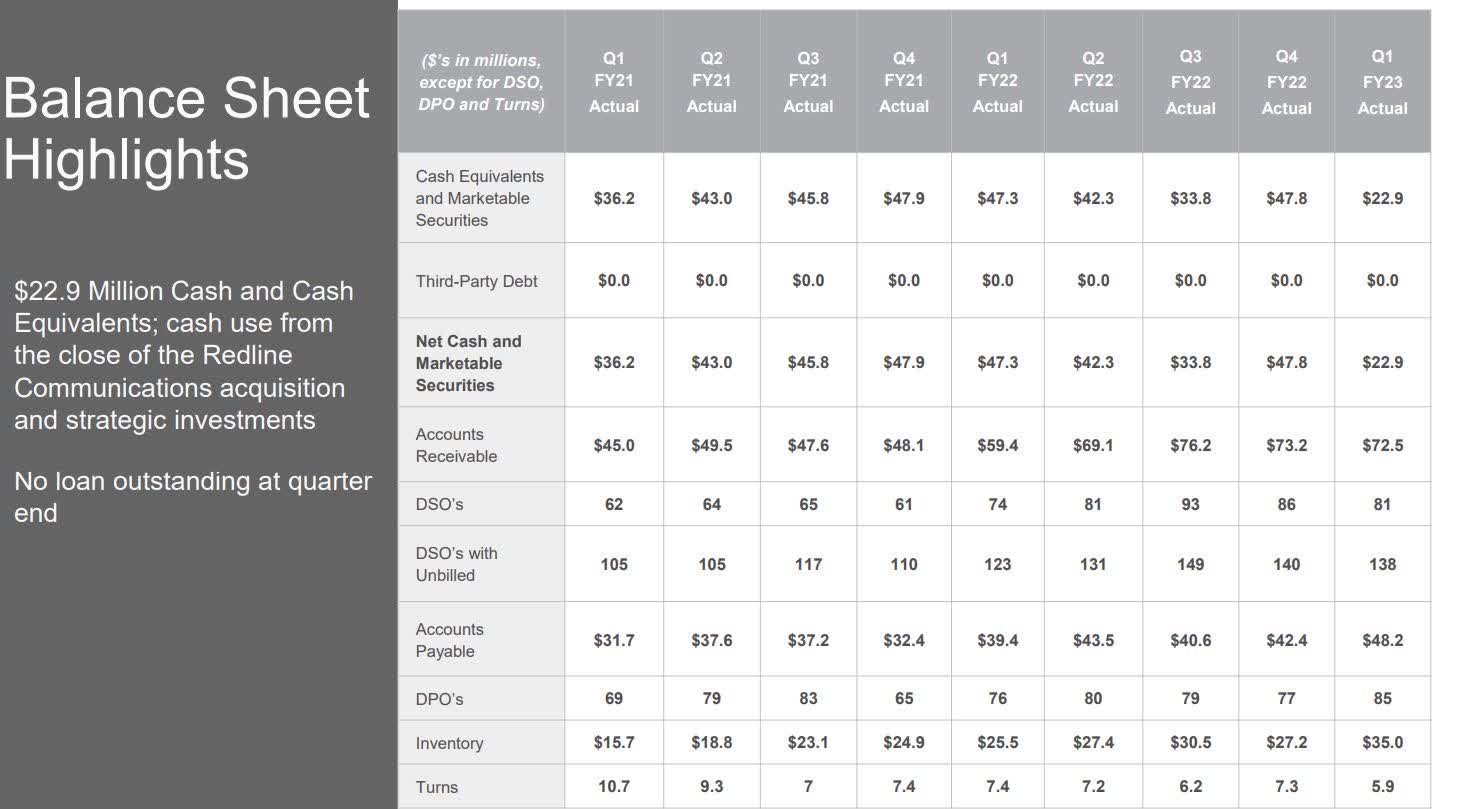

Cash and cash equivalents at the end of the fiscal first quarter of 2023 were $21.6 million, compared to cash and cash equivalents of $36.9 million at the end of the first fiscal quarter of 2022. The decline in cash came from the Redline acquisition, accelerated spend in inventory to offset supply chain risks, and customer cash collections in some emerging markets.

Although the company sees its 5G Tier 1 business growing in the North American and international markets, as companies build out their 5G networks, it's going to grow at the expense of average gross margin for a unspecified period of time. With the additional volume, over time the company says it expects to improve gross margins in 5G.

At the end of the first fiscal quarter of 2023 the company held no debt.

Importance of its balance sheet

Obviously, the balance sheet of any company is important, but with AVNW it's vital to the performance of the company going forward. The major reasons why are the ability of the firm to mitigate some of the risks associated with its supply chain by investing available cash in increasing its inventory without taking on debt. As a result of that competitive advantage, it has allowed AVNW to gain market share.

{kind=link}

Just as important, it empowered the company to acquire Redline, which as mentioned above, was its first acquisition in over a decade.

I think it's extremely important to maintain a healthy balance sheet as the company continues to navigate the supply chain waters while finding ways to grow via acquisition.

Even though the company could likely grow incrementally over time, I don't think it would move the needle. It needs some key acquisitions to help break it out of its trading range in my opinion.

They don't have to be major moves, just the type that can be quickly accretive to the performance of the company. Those types of acquisitions would add up over time, if together, they boost revenue and earnings, building up an even more impressive balance sheet which it could then leverage for more growth opportunities and operational efficiencies.

I don't believe it can organically grow itself out of its flat performance.

Conclusion

AVNW faces many of the similar challenges other companies face in the current macro-economic environment, including supply chain challenges and the lack of organic growth tailwinds to drive the performance of the company higher.

Under the specific circumstances it faces in the industry it competes in, I think management has allocated capital well, taking care of two of the more important challenges: securing more inventory in order to mitigate supply chain shortages, and making the type of acquisition that will have an immediate impact on the growth of the company.

Taking into consideration its geographic footprint, various products and services, and disciplined cash management, I think AVNW has positioned itself for incremental long-term growth, even though it's likely it could suffer some more share price erosion in the near term because of lack of any significant catalyst that would move the needle.

My thesis is that it's going to have to continue to on with its strategy, patiently building up its balance sheet while finding ways to improve its supply chain challenges, while at the same time looking for the types of acquisitions that would add to the long-term growth trajectory of the company.

If it maintains its modest growth plans and doesn't attempt to make any undisciplined moves for the sake of growth alone, I think it could be a solid holding that will return to a consistent growth trajectory once the economy recovers, assuming it finds ways to grow organically and inorganically going forward.

Until then, I think it's going to continue to trade flat, and any meaningful correction in its share price could be considered a buying opportunity for those that believe it has potential for long-term growth if it successfully executes on its strategy.

For further details see:

Aviat Networks: Looks Like It Will Continue To Trade Flat