AVDX - AvidXchange: Excellent Performance Business On Track To 20% Growth

2023-12-05 11:08:19 ET

Summary

- AvidXchange reported 3Q23 revenue growth of 19.7%, exceeding my expectations.

- AVDX's strong performance suggests it is not facing major macro headwinds and has a positive customer mix.

- Catalysts for future growth include the US presidential election, a partnership with AppFolio, and the rollout of Invoice Accelerator 2.0.

Summary

Following my coverage on AvidXchange ( AVDX ) stock, which I upgraded to a buy rating due to my expectation that AVDX can continue to grow near 20% for FY23. The caveat I had last quarter was to size the position small and only size up when AVDX starts to show >20% growth rate. Looking at how the stock price has moved over the past few months (it took a deep dive before reaching a 7% gain based on the share price at the time of writing), I acknowledge that my rating upgrade was too early. However, 3Q23 results proved that AVDX was performing in line with my thesis. This post is to provide an update on my thoughts on the business and stock. I reiterate my buy rating for AVDX as growth tracks well against my expectations and there are several growth catalysts in the near term that I foresee will accelerate growth past 20%. With >20% growth, I expect valuation to re-rate back to the AVDX historical average.

Investment thesis

On 9 th November 2023 , AVDX reported 3Q23 revenue of $98.7 million, representing 19.7% growth (tracking above my expectation for 17% FY23 growth). The revenue growth was primarily driven by payments revenue 21% growth to $68.5 million and the software segment’s $28.9 million revenue. The strong top-line performance, combined with improved adj gross margins of 70%, led to an adj gross profit of $69 million. This marks the 7 th consecutive quarter of sequential adj gross margin expansion. The solid gross margin expansion along with efficient cost management led to adj EBITDA coming in at $11.4 million, representing an 11.6% margin. This was a huge beat against consensus expectation of $2 million in adj EBITDA (or 2.1% margin).

A fair argument led by bearish investors is that the headline growth is not reflective of AVDX organic growth. While AVDX grew 19.7% on a headline basis, float income was a major contributor to payments revenue (growth would have been only 8% vs. the reported 21%). However, I think other positive aspects of AVDX outperformance outweigh this bearish point. Firstly, AVDX saw record levels of software revenue per transaction at $1.51. This was the first time AVDX has ever broken the $1.5 threshold. Secondly, regarding payments, if we strip away the impact of float, AVDX saw 5 bps of sequential improvement in take rate. Thirdly, AVDX's strong top-line performance suggests that they are not facing any major macro headwinds that peers are facing. For instance, if we compare AVDX performance to Bill.com performance, the latter saw major headwinds in the SMB space, seen in customers shifting to cheaper payment alternatives and weak volume performance. These dynamics shine a positive light on AVDX customer mix (skewed towards the mid-market segment with revenue between $5 million and $1 billion) and should ease concerns regarding weak underlying demand.

I believe the success that AVDX found in the mid-market segment was not due to sheer luck. It was all the experience that AVDX has garnered from years of working closely with Mastercard. Through the Mastercard partnership, AVDX has much experience driving monetized payment adoption. One of the highlights was AVDX's ability to offer variable interchange tiers, which, I believe, has a strong value proposition as it reduces the adoption hurdle for businesses that are of smaller scale (the revenue range in the mid-market segment is huge). In other words, rolling out these tiers leads to businesses adopting AVDX as there is the right pricing for them. Fundamentally, it is hard for various service providers to differentiate themselves in payments; hence, pricing is one of the key differentiators, which AVDX has managed to turn to its advantage. Aside from pricing, I think AVDX has also found other ways to differentiate itself. Specifically, through its software services like cash flow management, network management, etc. In short, AVDX has positioned itself as an affordable payment solution with a wide range of software solutions that can make the lives of mid-market businesses easier. As such, I continue to believe AVDX growth is sustainable and that once the macro environment normalises, growth should accelerate back to >20%.

We're already up to maybe 6 different versions of a Virtual Card. As an example, leveraging our partnership with Mastercard, we're able to utilize different interchange structures for different supplier use cases. Goldman Sachs Communacopia & Technology Conference (Sign in required)

Just with that, things that we do is really unique on virtual card is because of our partnership with MasterCard, we're able to really set our own interchange and create our own interchange structures within some guardrails that MasterCard provides us.

And we focus very heavily on providing an overall value proposition to the supplier around software tools, helping with their cash flow management, managing their business rules on the network, all those type of things. Wells Fargo 7th Annual TMT Summit (Sign in required)

In the near term, I see three major catalysts that should drive growth acceleration, hopefully past 20% growth. Firstly, the US 2024 presidential election is a major event catalyst that should drive a surge in political advertising dollars. For reference, in the 2019–2020 election cycle , total political ad spend reached $8.5 billion across TV, radio, and digital media. These huge amounts of dollars are not going to be exchanged via cash between buyers and sellers of ads. A good portion of it will flow through digital payment solutions, and AVDX should benefit. The second catalyst is the new partnership with AppFolio (going live in 1Q24), a real estate solutions software with around 19k customers. This is a huge announcement, as it is AVDX's largest vertically focused partnership. Given the stable nature of payments being processed (i.e., rents) at AppFolio, it should help reduce any volatility in AVDX payment volume. The third catalyst is the Invoice Accelerator 2.0 [IA2.0], which went live in early 4Q23 (October) and is expected to ramp up over the next several quarters. I believe IA2.0 will see strong adoption simply because it addresses the core needs of businesses—to get paid faster. With AVDX already establishing a strong repo with existing customers, it should not be hard for AVDX to upsell them IA2.0.

So, Invoice Accelerator, when we think of the value proposition for the supplier, one of the things that suppliers have told us is, in addition to helping us manage our payment modalities and give us the remittance data, it would be great if we had some tools to help us manage our cash flow and hopefully accelerate the timing of getting paid. 3Q23 earnings results call

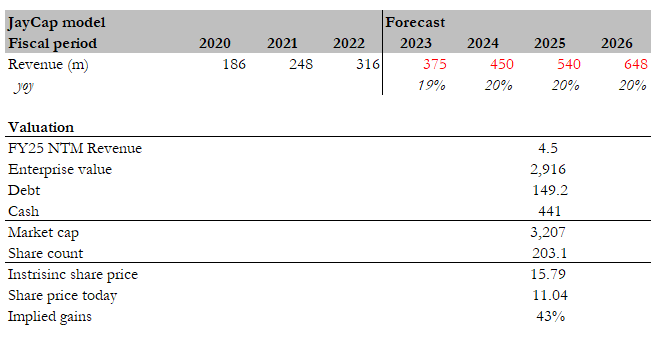

Valuation

{kind=link}

My target price for AVDX is now $15.80 based on my updated model. Two key updates were made here:

- I increased FY23 growth expectation from 17% to 19% as 3Q23 performance was tracking above previous FY23 expectation of 17%, and AVDX is growing at 20.1% on a 9M23 basis. However, I assumed 19% to reflect management guidance.

- I now expect AVDX to trade at 4.5x forward revenue, an increase of 0.5x from my previous model. I think the adjustment is justified as AVDX showed little signs of macro headwinds impacting its growth (in fact, growth accelerated on a sequential basis by 70 bps). At 4.5x, AVDX is simply trading at its historical average, so I am not making a huge assumption here.

Risk

AVDX over-indexing mid-market customers can be a double-edged sword, relative to dealing with SMBs. SMBs typically do not have the time or balance sheet (downtime will hurt cash flow) to keep switching payment providers. This is not the case for mid-market customers. I would expect larger-sized customers to constantly evaluate their cost structure and put pressure on payment solution providers for cheaper pricing. This might hurt AVDX growth.

Conclusion

I maintain my buy rating due to the strong performance which has tracked well against my projections. There are also several growth catalysts ahead such as the 2024 US presidential election, AppFolio partnership, and IA2.0 rollout which should further accelerate growth. As AVDX prints revenue growth of >20%, I expect the market to re-rate multiples back to AVDX historical average.

For further details see:

AvidXchange: Excellent Performance, Business On Track To >20% Growth