AVDX - AvidXchange: Leader In The Middle-Market B2B Automation Space

2023-06-09 09:41:04 ET

Summary

- AvidXchange Holdings is a dominant player in the middle-market B2B payments sector.

- AvidXchange's competitive advantage lies in its extensive network of over 220 integrations with accounting/ERP systems, which has been built over a period of two decades.

- I have a price target of $13 on the stock.

Investment Thesis

I consider AvidXchange Holdings, Inc. (AVDX) to be the dominant AP Automation solution in the middle-market B2B payments sector, which I believe has historically been underserved. Compared to small and medium-sized businesses or large enterprises, the middle market faces greater operational complexity due to the presence of various vertical-specific solutions that lack integration capabilities. While there is competition in the AP segment of B2B commerce from well-funded players, AvidXchange has established a strong competitive advantage through its extensive network of over 220 integrations with accounting/ERP systems. This advantage has been built over two decades, allowing the company to cater to a wide range of middle-market businesses operating within its targeted verticals. I view the stock as a buy and have an end-of-year price target of $13 on the stock.

Q1 Review: Positive Adj. EBITDA Achieved Ahead of Expectations

AVDX exceeded expectations in the first quarter, reporting strong financial results with higher revenue and adjusted EBITDA. Although float income fell short of expectations by approximately $1 million, the transaction yield came as a positive surprise. AVDX raised its full-year guidance, but some believe the increase to be conservative, considering that this quarter's performance surpassed the revised guidance. Long-term prospects for AVDX remain favorable due to positive trends in AP automation. There is potential for further upward movement in guidance if the macroeconomic conditions remain stable.

AVDX revised its outlook for FY23 based on better-than-anticipated results in the current quarter. The company cited ongoing cost-cutting measures by customers and extended sales cycles, which have been prevalent across the industry. While macroeconomic factors continue to pose challenges for AVDX's long-term growth potential (with the FY23 guidance indicating 15% year-on-year organic growth at the midpoint), these headwinds are expected to be temporary. Instead of lost growth, customer volume growth is expected to be delayed. Furthermore, easier year-over-year comparisons and benefits from upcoming elections should contribute to growth rates in 2024.

Leading Player in Middle-Market B2B Automation

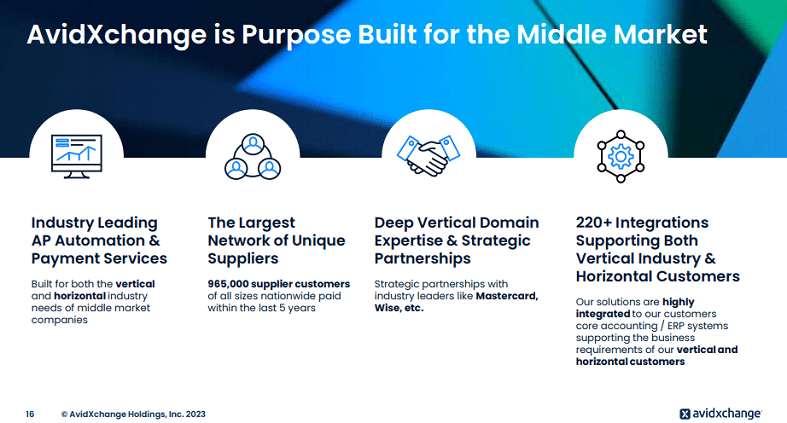

AVDX holds a prominent position in the middle-market B2B automation sector. This particular market segment consists of businesses with annual revenues ranging from $5 million to $1 billion and employing 50 to 1,000 personnel. Most companies within this segment already have established accounts payable ((AP)) processes, but these systems are often outdated and involve manual data input and matching of purchase orders and invoices. The traditional AP process is intricate, time-consuming, and costly.

AVDX offers industry-specific solutions that automate various aspects of the AP process, seamlessly integrating with ERP/Accounting systems. By implementing AVDX's solution, corporate customers can receive invoices from suppliers, view and approve invoices, make payments using various instruments, and seamlessly integrate the data into their buyer's ERP/accounting system. This digital workflow eliminates the need for paper-based processes and manual data entry, enhances visibility into the workflow, and facilitates effective management of supplier relationships and spending.

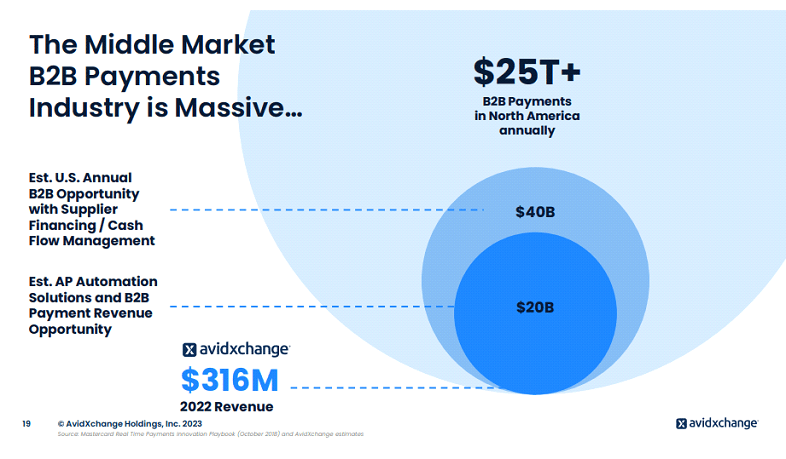

For a long time, investors have been aware of the vast global addressable market in B2B payments, which amounts to trillions of dollars. However, this market has been challenging to penetrate due to the complex web of back-office accounting systems across various industries and the intricacy of the commercial purchasing process itself. Unlike consumer card payments, B2B payments have resisted a standardized approach. However, with the increasing adoption of cloud-based solutions and upgrades to back-office technology by businesses, there has been a significant opportunity for B2B payments to thrive by automating and simplifying the accounts payable and receivable processes.

{kind=link}

Deep Moat with 220+ Integrations Across Multiple Verticals

AVDX boasts an extensive range of over 220 integrations with vertical-specific accounting software packages. The process of integrating each ERP/accounting platform varies in duration, typically taking around 9 months on average due to the complexity involved. This extensive integration capability, combined with the company's ownership of exclusive software obtained through acquisitions, has created a significant competitive advantage or "moat" for AVDX.

These integrations cover a wide range of industry-specific solutions, including real estate, homeowner's associations, construction, financial services, healthcare and social services, education (expanding into new markets), and media. Additionally, AVDX integrates with popular horizontal solutions like Oracle NetSuite, Sage Intacct, Intuit QuickBooks, and Microsoft Dynamics 365. The company has made considerable headway in tapping into the AP automation potential within the middle market. As a result, AVDX now holds a leading position, ranking either first or second, in many of the fragmented vertical markets it competes in.

{kind=link}

Valuation

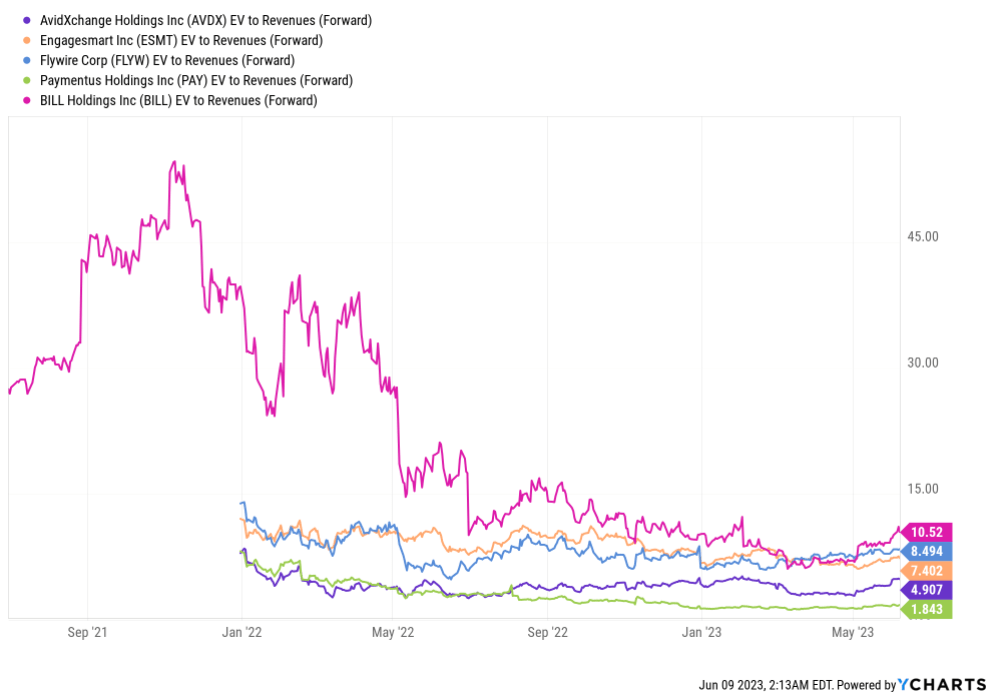

I believe the most relevant comp for AVDX will be BILL Holdings, Inc. ( BILL ). BILL is an AP automation company that trades at a significant premium at 10.5x EV/Sales, given the company's above-market-average growth rate and large earnings revisions on the beat & raise cadence. Moreover, I have also identified a secondary comp group of AR automation companies that includes EngageSmart, Inc. ( ESMT ), Flywire Corporation ( FLYW ) and Paymentus Holdings, Inc. ( PAY ). This group shares the common attribute of focusing on billers, but they focus on the AR side. This group is generally viewed to be 20-30% growers trading at revenue multiples of 2- 9x.

I view BILL as an aspirational comp for AVDX, a high bar in the event the company is able to materially accelerate revenue and expand gross margins. I maintain a buy rating on the stock and have an end-of-year price target of $13 on the stock based on a 6x EV/sales multiple on FY24 estimates, which I think is warranted given AVDX's solid revenue growth profile, significant future TAM opportunities, leadership position in the middle market, strong management team, and expansion opportunities in new verticals and international markets through recent acquisitions and organic investments.

{kind=link}

Risks

AvidXchange operates on a revenue model that is dependent on the usage and volume of its buyer and supplier clients. It should be noted that not all bills paid through the platform are recurring or maintenance-related. The company competes in seven key verticals, some of which are influenced by cyclicality, meaning that the volume of bills paid is positively correlated with business activity. For example, sectors such as real estate, homeowner's associations ((HOA)), and construction are particularly exposed to these cyclicality risks. During the onset of the pandemic, AvidXchange experienced a significant decrease in organic revenue growth as certain businesses, like education, faced closures. While the company can be considered relatively defensive, it is not entirely immune to the effects of cyclicality.

Moreover, before the pandemic, AvidXchange had a strong net transactions processed retention rate, with a rate of 105% (indicating growth) from one year to the next. However, this rate dropped to 102% from 2019 to 2020. Given that AvidXchange has consistently achieved annual revenue growth of over 20%, it suggests that a significant portion of this growth comes from acquiring new buyers and increasing monetized spend on the platform. This places pressure on the company to continually generate new sales to replenish the backlog of transactions and to overcome resistance from suppliers who may be hesitant to pay higher acceptance costs. Consequently, AvidXchange must maintain a relentless focus on promoting the value and efficiency of its platform. Any slowdown in these efforts could potentially result in slower growth for the company.

Conclusion

AVDX specializes in providing AP automation software and payment solutions to middle-market businesses in sectors like real estate, media, education, and financial services. The company's business model focuses on maximizing payment adoption within these industries by leveraging vertical-specific software solutions that have high acceptance rates for electronic payments. I consider AVDX to have a strong competitive advantage, with a deep moat and a greater ability to monetize payments compared to its competitors. I view the stock as a buy and have an end-of-year price target of $13 on the stock.

For further details see:

AvidXchange: Leader In The Middle-Market B2B Automation Space