ASM:CC - Avino Silver & Gold Mines: High-Risk High-Reward

2023-08-16 16:30:51 ET

Summary

- Avino had a softer Q2 report, with lower production and sales and significantly higher costs, with margins impacted by a sharp rise in the Mexican Peso.

- This leaves ASM well behind its annual guidance & while production & costs should improve in Q3, Peso strength has persisted while silver has slid, setting up another mediocre quarter.

- In this update, I'll look at the stock's valuation after this correction, recent developments, and whether the stock looks worthy of a long position at current levels.

It's been a mixed Q2 Earnings Season for the precious metals sector ( GDXJ ) and while there have been a few disappointments to date like Coeur Mining ( CDE ) and First Majestic Silver ( AG ) in the silver space, Avino Silver & Gold Mines ( ASM ) didn't deliver much better results. And while this was partially due to mine sequencing with mining in lower grade areas and lower recoveries, all-in sustaining costs [AISC] soared to $23.06/oz on the back of lower ounces sold and despite relatively modest sustaining capital spend. This resulted in significant margin compression in the period, and with the Mexican Peso's strength continuing into Q3, I would expect another relatively high-cost quarter on deck. Meanwhile, we saw further share dilution in the period from sales under its ATM both during the quarter and post-quarter end. Let's look at the Q2 results below and any recent developments.

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Q2 Production & Sales

Avino Silver & Gold Mines ("Avino") released its Q2 results earlier this month, reporting quarterly production of ~587,300 silver-equivalent ounces [SEOs], a 10% decline from the year-ago period. The lower production was despite higher throughput of ~157,400 tonnes and was related to mine sequencing, with lower silver, gold, and copper grades in the period. Meanwhile, the company also lower recoveries across the board (silver, gold, copper), with Avino calling out supply chain issues for some maintenance parts that affected plant recoveries. This has resulted in year-to-date SEO production tracking well behind the FY2023 guidance mid-point of ~3.0 million SEOs, with just ~1.27 million SEOs produced year-to-date. That said, the company expects a better H2 with improved haulage rates (new scoop added in June and upgrades to the haulage ramp), suggesting a better performance sequentially.

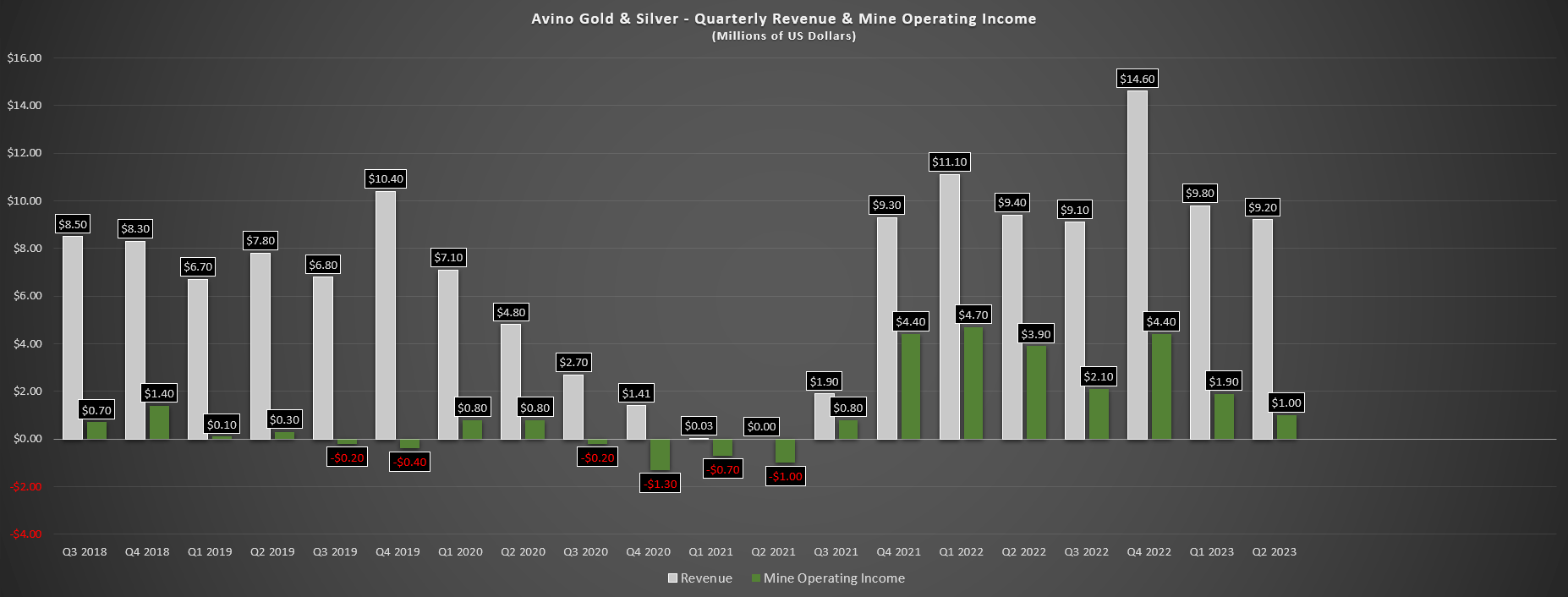

Avino Silver & Gold - Quarterly Revenue & Mine Operating Income (Company Filings, Author's Chart)

{kind=link}

Although the outlook for a better H2 is positive after a slow start to the year, we saw a hit to Q2 and H1 financial performance, with revenue down 2% year-over-year to ~$9.2 million in Q2 despite the benefit of higher metals prices ($1,995/oz gold, $24.50/oz silver, and ~$8,650/tonne copper). Meanwhile, mine operating income sunk 73% to ~$1.04 million. The result was that Avino's cash balance fell to just $1.2 million at quarter-end with barely $4.0 million in working capital. Given the weaker balance sheet despite share sales under its At-The-Market Equity Program [ATM], the company elected to sell additional shares following quarter-end, with ~2.36 million shares sold for proceeds of ~$1.63 million or at a cost of US$0.69/share.

On a positive note, there was some solid news in the quarter, with Avino recording the best drill intercept in its history from below Level 17, which is the deepest working level at the ET Area of its Avino system. The highlight intercept in the release was 57 meters (true width) at 296 grams per tonne silver-equivalent, with this being one of the thickest intercepts drilled and having much higher grades than its average grade closer to ~140 grams per tonne silver-equivalent. And while ET-23-09 was the highlight hole, the other two intercepts also hit solid grades with 11 meters at 230 grams per tonne silver-equivalent and ~10 meters at 188 grams per tonne silver-equivalent. Overall, this is certainly a positive development for the company and points to the potential for further resource growth at depth to build on an already large resource base.

Costs & Margins

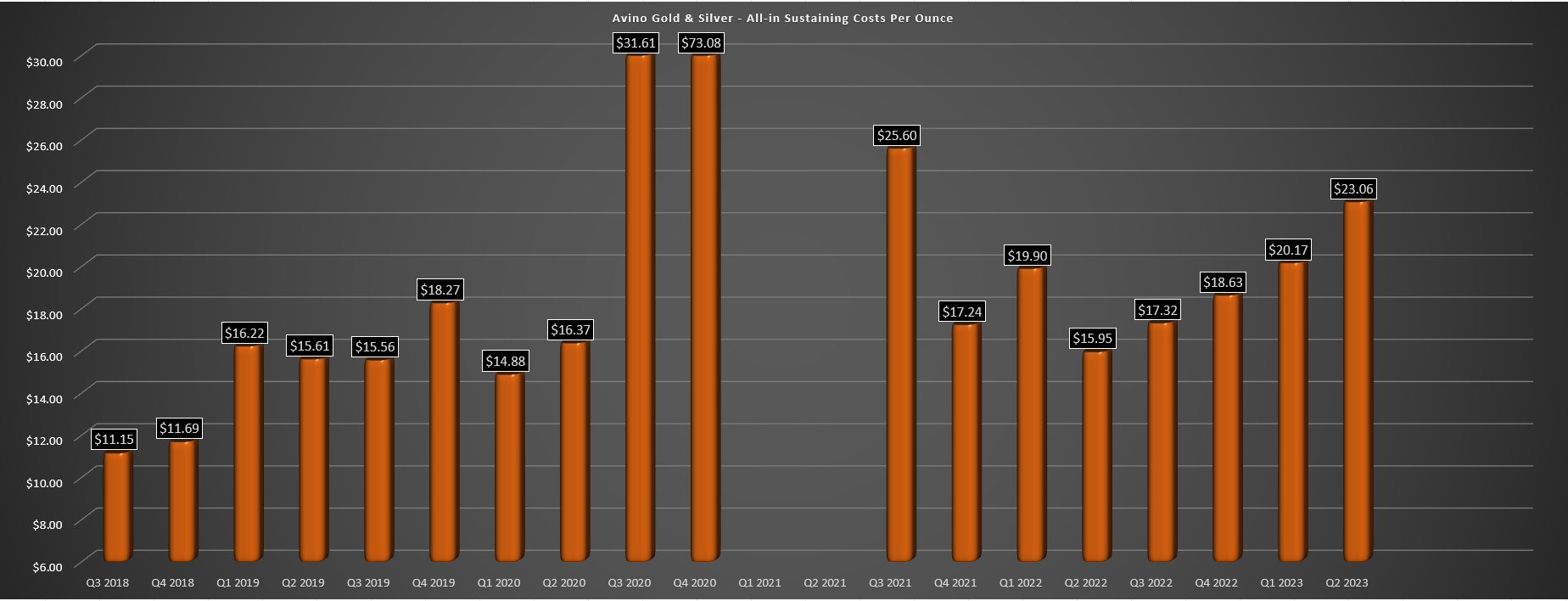

Moving over to costs and margins, Avino reported cash costs of $16.33/oz in Q2 (Q2 2022: $8.39/oz), and all-in sustaining costs of $23.06/oz, with the latter increasing by 44% from the year-ago period. This sharp increase in costs was driven by the persistent strength of the Mexican Peso, which affected several producers in Mexico, fewer ounces sold in the period vs. produced and higher G&A costs. And while I would expect better performance in the upcoming quarter with the benefit of higher ounces produced and sold, the Mexican Peso isn't doing the company any favors, sitting at a rate of ~$17.0 USD/MXN quarter-to-date vs. an average exchange rate closer to ~$18.0 USD/MXN in Q2 2023. In addition, this increase in costs was despite very modest sustaining capital spend in the period (~$0.27 million), as well as exploration expenses of $0.03 million vs. $0.31 million in Q2 2022.

Avino - All-in Sustaining Costs (Company Filings, Author's Chart)

{kind=link}

Given the sharp rise in costs, AISC margins slipped to $1.44/oz, down from $6.80/oz in Q2 2022, and it looks like the silver price might be less of a tailwind than the company hoped in the upcoming quarter, averaging ~$23.10/oz quarter-to-date vs. the $24.50/oz average realized price enjoyed in Q2 2023. So, while I would expect margins to improve sequentially (Q3 2023 vs. Q2 2023) with higher production, we could see some offsets from more normalized sustaining capital spend vs. just ~$0.40 million spent year-to-date, the continued strength in the Mexican Peso, and what could be a ~5% lower silver price if we don't see a recovery in silver soon.

Valuation

Based on ~132 million shares (excluding warrants) and a share price of US$0.68, Avino trades at a market cap of ~$90 million. This makes it one of the lowest market cap silver producers in the precious metals sector. It also remains one of the most undervalued on a resource per ounce basis, with Avino trading at just ~$0.33/oz of silver-equivalent resources across all of its projects/mines, or ~$0.56/oz based on its resource base that excludes its future growth project, La Preciosa. I continue to see this as an attractive valuation, and assuming Avino was based out of a more favorable jurisdiction, I would view the stock as a Speculative Buy on further weakness. However, there are three risks I see to the thesis:

The first is that we continue to see share dilution, with ~838,000 shares sold in the first six months of the year and another ~2.4 million shares sold at $0.69 after quarter-end. And with a working capital position of less than $7 million and the Mexican Peso putting a dent in Avino's margins (along with its Mexican producer peers), it's hard to rule out further share dilution here, especially with the company having ambitious growth plans. For this reason, the share count is a bit of a moving target, up ~5% since the closing of the La Preciosa acquisition, making it more difficult to value the stock.

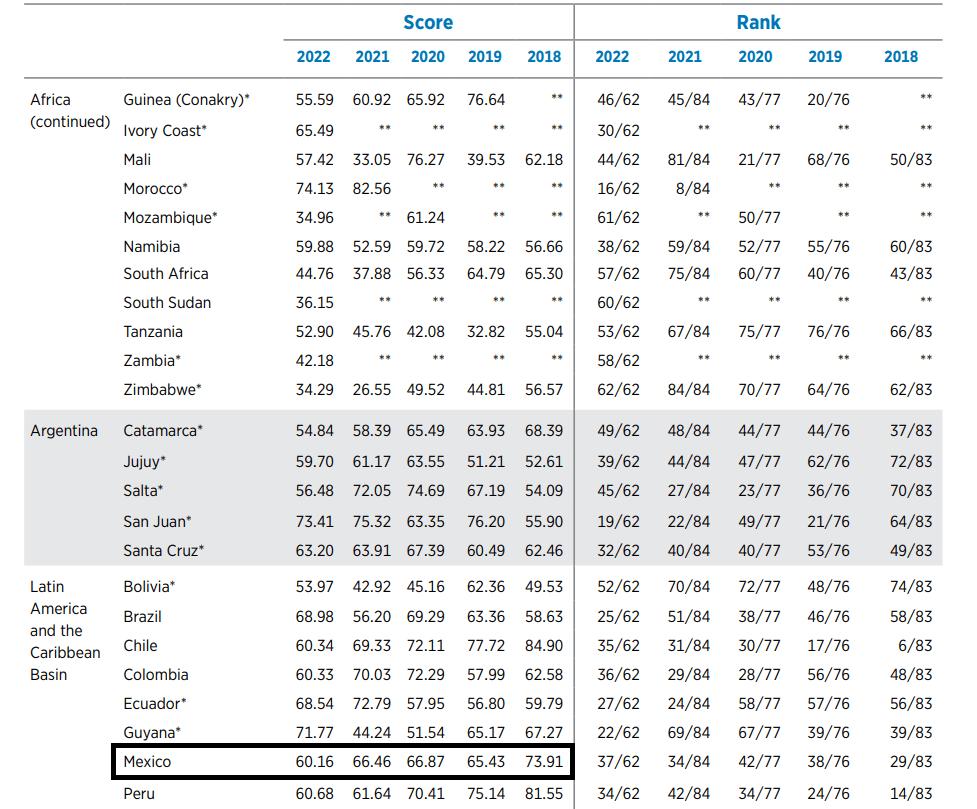

The second issue is that Avino is a single-asset producer operating in a jurisdiction that has lost some of its lustre, evidenced by Mexico continuing to drop in rankings each year on the Fraser Institute's Annual Survey of Mining Companies. And this sharp drop in rankings (2022) was before the recently proposed tougher mining laws , which may not affect existing mines but could affect future projects and could weigh on investment attractiveness further for producers in the country. In addition, there appears to be a risk of an upward pressure on labor costs in Mexico with the massive Penasquito Mine still in a 2-month-long strike and an illegal blockade recently at Fortuna's ( FSM ) San Jose Mine with demands, with both instances looking for higher profit-sharing.

Mexico Investment Attractiveness Rankings - Fraser Institute Annual Survey

{kind=link}

This is not ideal for a single-asset producer in the country like Avino, and certainly not when it has relatively low margins (potentially making it harder it to absorb any rise in labor costs). Aside from this, the Mexican Peso has hit new multi-year highs vs. the US Dollar, and we've already seen the significant impact that has had on other producers, and the MXN/USD rate has strengthened further since its Q2 average. So, with elevated exposure to this unfavorable currency change and 100% exposure to Mexico, I see Avino as high-risk, even if the reward might also be high if it can execute successfully on its growth. And in regards producers in less favorable risk jurisdictions, I prefer to pass entirely unless they have diversification outside of that jurisdiction (multi-asset producer) or have an asset that with such exceptional economics that it is worth taking on some risk, like MAG Silver ( MAG ).

{kind=link}

The final concern is that 14 million shares of Avino were paid to Coeur Mining as consideration for the La Preciosa acquisition, which was in addition to deferred consideration of up to $50 million ($0.25 per silver-equivalent ounce of new mineral reserves outside of current resource area at La Preciosa), royalties, and an additional cash to be paid within 12 months of initial production. This represents ~12% of Avino's share count and given Coeur's weak balance sheet (~$430 million in net debt) with further upwards cost revisions at Rochester POA 11, the company has had no hesitation dumping its share positions in other companies that were acquired for strategic purposes, including selling its position in Integra ( ITRG ) and Victoria Gold ( OTCPK:VITFF ). And while it's not clear if they will dump these shares in the open market, this could create a severe overhang for the stock and Coeur's share price weakness certainly makes selling shares of another company to raise cash a more attractive option than selling its own shares at depressed prices (multi-year lows).

{kind=link}

To summarize, while Avino's valuation may be attractive, it's hard to rule out further equity dilution, potential share sales by a large holder with a weak balance sheet which could further pressure the stock, with Avino using its ATM as recent as last quarter. Meanwhile, this is a micro-cap stock with a weak balance sheet itself, making it more susceptible to share price declines if we see further weakness in the sector. Finally, I prefer low-risk, high-reward investments, and while Avino may be high reward, it's hard to call it low-risk as a single-asset silver producer in a Tier-2 jurisdiction. Hence, I continue to see far more attractive bets elsewhere in the sector where I'm being paid to wait, such as B2Gold ( BTG ) with a near 20% FY2025 free cash flow yield, a ~5.4% dividend yield and greater diversification with a high-margin Tier-1 operation recently added to its portfolio.

Summary

Avino has become more attractively valued after its recent ~35% correction, but with several names on the sale rack sector-wide, I prefer to reach for quality vs. buying micro-cap names with weaker balance sheets that will have a more difficult time to funding their growth without potential equity sales. In addition, I prefer higher margin names that are more insulated from metals price weakness, a quality that Avino lacks, with trailing-twelve month AISC of ~$19.80/oz. So, with relatively slim margins, a growth story that could be difficult to fund without share dilution if metals prices don't cooperate, and better reward/risk bets available, I think there are far better ways to allocate one's capital elsewhere in the sector.

For further details see:

Avino Silver & Gold Mines: High-Risk, High-Reward