CMSD - Avista: Buy This High-Yielding Utility On Dips

Summary

- Avista is a regulated electric and natural gas utility that services rural areas of the Pacific Northwest as well as Alaska.

- The company's natural gas utility business accounts for about half of its business and a significant portion of its cash flow.

- The natural gas operation is very unlikely to become obsolete in the near future as electrification appears to be a pipe dream.

- The company's leverage has been increasing over the past few quarters but it is still reasonable compared to its peers.

- The valuation is rather stretched right now but the company could be a good buy on dips.

Avista Corporation ( AVA ) is a regulated electric and natural gas company that operates in the Pacific Northwest and Alaska. Utilities in general have long been favorite investments among more conservative investors such as retirees due to their relative stability and high yields. Avista Corporation certainly satisfies these criteria, which we can see by looking at the company’s third-quarter 2022 earnings results. Over the past few years, electric utilities have been somewhat more popular investments than natural gas ones in the market, which is evident in the fact that electric utilities tend to have somewhat higher valuations right now. Despite being both an electric and natural gas utility, Avista Corporation is clearly valued as an electric utility as it has a fairly high valuation. In fact, the company has a pretty high valuation even for an electric utility, which is fairly consistent with what we saw the last time that we looked at this company. The thesis for investing in Avista has generally not changed since the last time that we looked at it a few months ago but the company has posted more current results along with some additional developments so it is still a good idea to do our quarterly review of the company. This article will do exactly that and allow us to re-evaluate our thesis.

About Avista Corporation

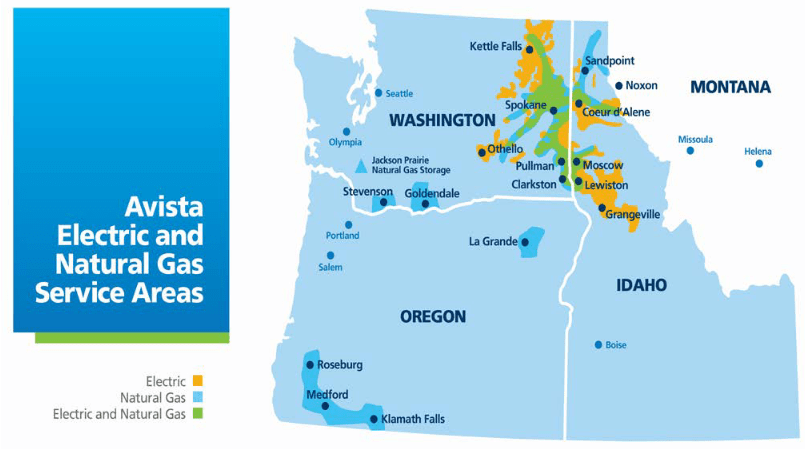

As stated in the introduction, Avista Corporation is a regulated electric and natural gas utility that operates in the Pacific Northwest states of Washington, Oregon, and Idaho. The company also has significant operations in Alaska.

{kind=link}

Despite the large geographic footprint, the company does not have a particularly high customer count. It only serves about 402,000 electric and 368,000 natural gas customers in the Pacific Northwest. The company’s customer count is only 17,000 in Alaska so that is a much smaller operation in terms of customers served. The biggest reason for the fairly small customer counts despite its substantial reach is that most of the areas that it serves are rural. This is particularly true in Idaho and eastern Washington. The company’s service area does not include the Seattle metropolitan area, which is by far the most populated area in these states. The fact that the company serves a rural area does not prevent it from enjoying many of the characteristics that we have come to appreciate across the utility sector. The most important of these characteristics is that the company enjoys remarkably stable cash flow over time regardless of economic conditions. We can see this by looking at the company’s quarterly operating cash flow. Here it is over the past eleven quarters:

{kind=link}

At this point, some readers may point out that the company’s operating cash flow tends to be significantly higher in the first quarter of the year than at other times. This does not disprove my point about stability over time, however. It is in fact expected because roughly half of the company’s business is the natural gas distribution to homes and businesses. The primary use of natural gas is space heating so we can expect consumption to be substantially higher during the winter months than at other times of the year. This is particularly true in the Pacific Northwest, which tends to get fairly cold during the first quarter of the year. We do see that its cash flow is generally pretty similar when we look at the same quarter in different years. The only exception was the third quarter of this year but that is only one occurrence that does not fit the rule out of many that do so it is not a big deal and does not disprove the overall statement.

The reason for this overall stability should be fairly obvious. A utility provides a service that most people would consider to be a necessity for modern life. After all, how many of us do not have electricity or heat in our homes? Thus, most people will prioritize paying their utility bills ahead of discretionary expenses during times when money gets tight. This is something that could be very important today considering that the high inflation rate has caused 63% of American households to live paycheck-to-paycheck. We are also seeing numerous predictions that the United States will enter into a recession during 2023 and many households experience declines in their discretionary income during recessions. Thus, we will want to be in recession-resistant investments today to minimize damage to our portfolios. Avista Corporation fits this bill quite well as just shown.

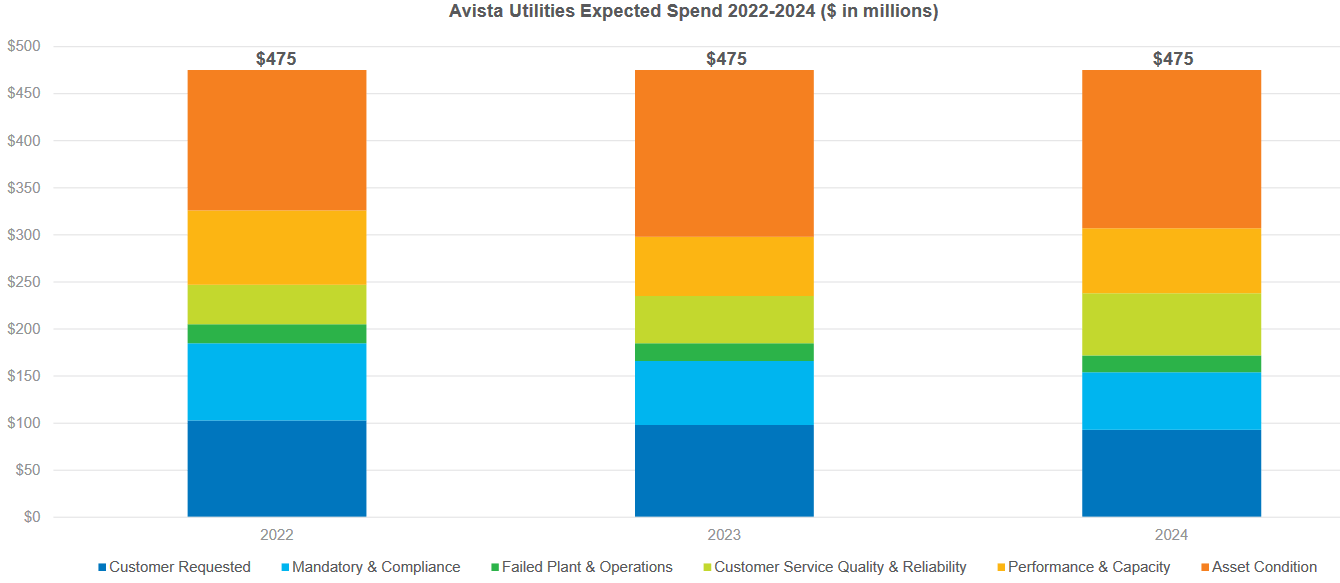

Naturally, as investors, we are not satisfied solely with stability as we also desire to see growth. Avista Corporation is well-positioned to deliver this growth. The primary way that the company will be doing that is by increasing its rate base. The rate base is the value of the company’s assets upon which regulators allow it to earn a specified rate of return. As this rate of return is a percentage, any increase in the rate base allows the company to increase the prices that it charges its customers to earn that allowed rate of return. The usual way that a utility company will increase its rate base is by investing money into upgrading, modernizing, and possibly even expanding its rate base. Avista Corporation is planning to do exactly this as the company has unveiled a plan to spend $475 million during each of the years 2022, 2023, and 2024 for the purpose of upgrading its infrastructure:

{kind=link}

I will admit that I would like the company to provide a bit more visibility into its capital expenditure plans than this. After all, 2022 is almost over so its spending during that year is somewhat irrelevant. Thus, the only thing that is really important to us as forward-looking investors is the $950 million in planned spending over the 2023 to 2024 period. That is not nearly as much visibility as the company’s peers provide, most of which have now provided investors with their capital expenditure plans going out to 2027. If Avista has not yet determined its plans for years beyond 2024 then it does not speak well of the company’s management. If the company has updated its five-year plan, then I am curious about why it has not been provided to investors. Our lack of this information makes it difficult for us to determine our future returns from an investment in the company. The company should be able to grow its rate base at a 5% rate during 2023 and 2024, which should result in 4% to 6% earnings per share growth during each year. That is a bit low for a utility but it still gives us an 8% to 10% total average annual return, which is decent. I just wish we had much more than just two years of projections to use for our analysis.

Fundamentals Of Avista’s Natural Gas Business

In previous articles, we have focused on Avista’s environmental, social, and governance credentials. In particular, its focuses on renewable energy. Indeed, the company does have much stronger credentials than many of its peers as approximately 60% of the company’s electricity comes from renewable sources. This may cause some to believe that the firm’s natural gas business is something of an afterthought despite accounting for nearly half of its operations. This is a belief that is promoted by politicians and activists that have been pushing for electrification across the economy. At its core, electrification refers to the conversion of things that are historically powered by fossil fuels to the use of electricity instead. One of the things that these groups are trying to do is to get everyone to switch away from natural gas in favor of natural gas for space heating. Despite the fact that Avista Corporation is one of the most environmentally-conscious utilities in the United States, this would still hurt the company in the short- to medium-term as it plays out due to the sheer size of its natural gas business which would be rendered obsolete by electrification.

Fortunately, it is highly unlikely that America will convert from natural gas to electricity for space heating purposes in the next few decades. This is a view that is supported by analysts at the Energy Information Administration, who have projected that the national demand for electricity will grow at a 1% to 2% rate over the next thirty years:

U.S. Energy Information Administration

This is nowhere close to the growth rate that would result if the country were to convert from natural gas to electricity for space heating purposes. Not coincidentally, it is also nowhere close to the growth rate that would result from the widespread adoption of electric cars. Thus, the agency does not appear to believe that either of these things is particularly likely for quite some time. It is likely that it is correct, particularly when it comes to space heating. One of the biggest reasons for this is that electricity is far less efficient at heating a building than natural gas so it ends up being considerably more expensive to use electricity for heat. In fact, even with the surge in natural gas prices that occurred over the past eighteen months, it is still nearly four times as expensive to heat a home with electricity as opposed to natural gas:

New Jersey Resources/Data from US EIA

In this light, it seems highly unlikely that very many people will convert their homes to electric heat sources anytime soon. This is especially true among people of limited means or those that live in colder climates, such as those living in the territory that Avista Corporation serves. After all, who would willingly want to see their heating bill go up by this much even assuming that such an increase is affordable? Thus, we can conclude that Avista Corporation’s natural gas business is not likely to be rendered obsolete for many years. It should continue to be a steady source of income for the company and by extension its investors going forward. This is nice to see for obvious reasons.

Financial Considerations

It is always important to look at the way that a company finances its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. This is usually accomplished by issuing new debt to repay the existing debt because very few companies have sufficient cash to completely pay off their debt as it matures. As a result of this, a company might see its interest expenses increase following a rollover depending on the conditions in the market. In addition to this, a company must make regular payments on its debt if it is to remain solvent. Thus, any event that causes a company’s cash flow to decline might push it into financial distress if it has too much debt. Although utilities like Avista Corporation tend to enjoy remarkably stable cash flows over time, bankruptcies have occurred in the sector so we should remain cognizant of this risk.

One metric that we can use to evaluate a company’s financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations as opposed to wholly-owned funds. It also tells us how well the company’s equity will cover its debt obligations in the event of a bankruptcy or liquidation event. This second thing is arguably more important.

As of September 30, 2022, Avista Corporation had a net debt of $2.734 billion compared to a total shareholders’ equity of $2.2348 billion. This gives the company a net debt-to-equity ratio of 1.22. This is somewhat worse than the company’s ratio at the end of the second quarter of 2022, which is disappointing. The company’s ratio has been getting progressively worse over the course of this year:

| Q3 2022 |

| Q2 2022 |

| Q1 2022 |

| Net Debt-to-Equity Ratio |

| 1.22 |

| 1.17 |

| 1.13 |

This is rather disappointing because it illustrates that the company is using ever-growing amounts of debt in its financial structure in a rising rate environment. Thus, the risks posed to investors by the company’s leverage have been increasing over the past month. This is rather disappointing but fortunately, Avista still does not have an especially high amount of debt relative to its peers:

| Company |

| Net Debt-to-Equity Ratio |

| Avista Corporation |

| 1.22 |

| DTE Energy ( DTE ) |

| 2.22 |

| Eversource Energy ( ES ) |

| 1.43 |

| Portland General Electric ( POR ) |

| 1.31 |

| CMS Energy ( CMS ) |

| 1.81 |

This is quite nice to see, especially in light of Avista’s worsening leverage position. The fact that it still remains lightly levered is a sign that the company is not employing too much debt in its financial structure. As such, it should still not present too much risk to investors despite the fact that it is becoming more levered in a rising rate environment.

Dividend Analysis

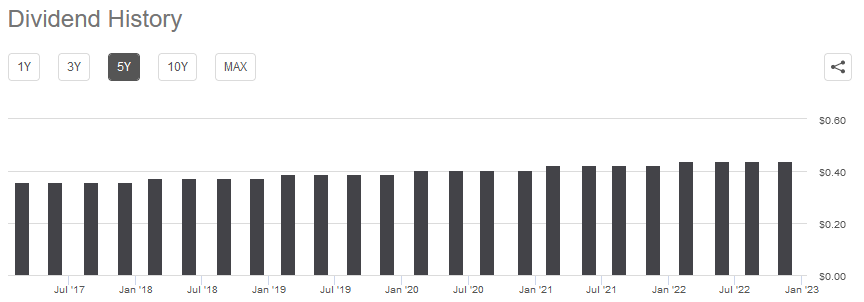

One of the reasons why investors purchase shares of utility companies is because of the fairly high yields that these companies typically possess. The reason for these high yields is largely because of slow growth. As we saw earlier, Avista Corporation is only likely to grow its earnings per share at a 4% to 6% rate, which is considerably less than we see in many other sectors. As a result of this, the company aims to deliver a significant part of its total return to its investors via direct payments. When we combine this with the fact that the stock will not generally trade at high multiples to earnings due to its slow growth, yields tend to be rather high. Avista Corporation yields 4.01% at the current stock price, which is quite a bit above the 1.65% yield of the S&P 500 Index ( SPY ). Avista Corporation also has a long history of raising its dividend annually, as shown here:

{kind=link}

The fact that the company increases its dividends on an annual basis is quite nice to see during inflationary periods like the one that we are in today. This is because inflation is constantly reducing the number of goods and services that we can purchase with the dividend that we receive from the company. The fact that Avista gives us a larger amount of money each year helps to offset this effect and maintains the purchasing power of the dividend. As is always the case though, we want to ensure that the company can actually afford the dividend that it pays out. After all, we do not want it to be forced to reverse course and cut the dividend since that would reduce our incomes and likely cause the stock price to decline.

The usual way that we judge a company’s ability to pay its dividend is by looking at its free cash flow. A company’s free cash flow is the amount of money that is generated by its ordinary operations that is left over after the company pays all of its bills and makes all necessary capital expenditures. This is the money that is available to do things that reward the shareholders such as buying back stock, reducing debt, or paying a dividend. In the third quarter of 2022, Avista Corporation had a negative levered free cash flow of $101.0 million. This is obviously not nearly enough to pay any dividend, let alone the $32.2 million dividend that the company actually paid out.

However, it is not atypical for a utility company to finance its capital expenditures through the issuance of debt and equity while using its operating cash flow to finance its dividend. This is because of the incredibly high costs involved with constructing and maintaining utility-grade infrastructure over a wide geographic area. During the third quarter of 2022, Avista had an operating cash flow of $4.5 million, which is likewise not enough to cover the $32.2 million dividend that was paid out. However, as pointed out earlier, the third quarter had exceptionally low operating cash flow. The company reported an operating cash flow of $38.9 million in the third quarter of 2021 and $82.6 million in the third quarter of 2020. Thus, the company would normally generate enough cash in the third quarter to cover its dividend. In addition, the company’s operating cash flow tends to be higher in the winter months because of the demand for natural gas from that operation so it may be better to look at the company’s trailing twelve-month operating cash flow for our analysis. During the twelve-month period that ended September 30, 2022, Avista Corporation reported an operating cash flow of $248.8 million. This was more than enough to cover the $126.3 million that was paid in dividends over the same period with a great deal of money left over. Thus, we can clearly see that the company should have no trouble maintaining its dividend. There appears to be no real threat here and we will likely see a dividend increase following the company’s fourth-quarter 2022 earnings results as usual.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of an electric utility like Avista Corporation, one metric that we can use to value it is the price-to-earnings growth ratio. This ratio is a modified version of the familiar price-to-earnings ratio that takes a company’s forward earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 is a sign that the stock may be undervalued relative to its forward earnings per share growth and vice versa. However, it is extremely uncommon to find a stock with a ratio of less than 1.0 in today’s overheated market. This is particularly true in the low-growth utility sector. As such, it is best to compare a stock’s price-to-earnings growth ratio to its peers in order to determine which offers the best relative valuation.

According to Zacks Investment Research , Avista Corporation will grow its earnings per share at a 5.18% rate over the next three to five years. This is in line with the 4% to 6% rate that we have been using over the course of this analysis so I see little reason not to use this figure. This gives Avista a price-to-earnings growth ratio of 4.44 at the current stock price, which is pretty high for a utility. We can verify that by comparing it to some of its peers:

| Company |

| PEG Ratio |

| Avista Corporation |

| 4.44 |

| DTE Energy |

| 3.28 |

| Eversource Energy |

| 3.16 |

| Portland General Electric |

| 3.22 |

| CMS Energy |

| 2.69 |

This essentially confirms it. Avista Corporation is quite expensive relative to several other electric and natural gas utilities. We also saw this high relative valuation the last time that we looked at the company, although it was considerably cheaper a few months ago. This is likely because of the market strength that we saw on December 23 and the low liquidity that we will probably see between now and 2023. It may, therefore, be best to wait for a dip in the stock price before picking up some shares as it seems likely that a patient investor should be able to get a somewhat better deal in the near future.

Conclusion

In conclusion, there are certainly a few things to like about Avista Corporation today. In particular, the company’s general stability regardless of economic conditions could prove to be a boon today as the high inflation rate is straining the finances of numerous households and the Federal Reserve is determined to push the nation into a recession. The fact that the company has a fairly high 4.01% dividend yield is nice too since we can collect a high level of income while waiting out the challenging conditions. However, we have to pay through the nose for all of these good things as the valuation looks rather stretched today. The company could certainly be a nice buy on dips, though.

For further details see:

Avista: Buy This High-Yielding Utility On Dips