AESC - Avista: Holding Up Pretty Well But Still Has Attractive Valuation Vs. Peers

2023-10-27 18:35:21 ET

Summary

- Avista Corporation is a regulated electric and natural gas utility operating in the Pacific Northwest and Alaska.

- The company has stable cash flows and a high dividend yield of 5.72%.

- Despite a decline in stock price, Avista Corporation has outperformed the U.S. Utilities Index and may be undervalued.

- The company has been negatively impacted by rising interest rates, as it is costing it considerably more money to carry its debt than it did only a year ago.

- The worst may be behind Avista now, but rates could increase further and continue to apply pressure to the company.

Avista Corporation ( AVA ) is a regulated electric and natural gas utility that operates in the Pacific Northwest and Alaska. This is one of the largest utilities in the area, but much of the company's service territory is not particularly populated, so Avista Corporation's customer base is not especially large. This does not prevent the company from enjoying many of the characteristics that we usually associate with utilities, however, such as stable cash flows and a relatively high dividend yield. Indeed, Avista Corporation's current yield is 5.72%, which is pretty impressive to anyone who has been actively investing for more than two years or so. After all, it was not very long ago that it was nearly impossible to find anything with such a high yield.

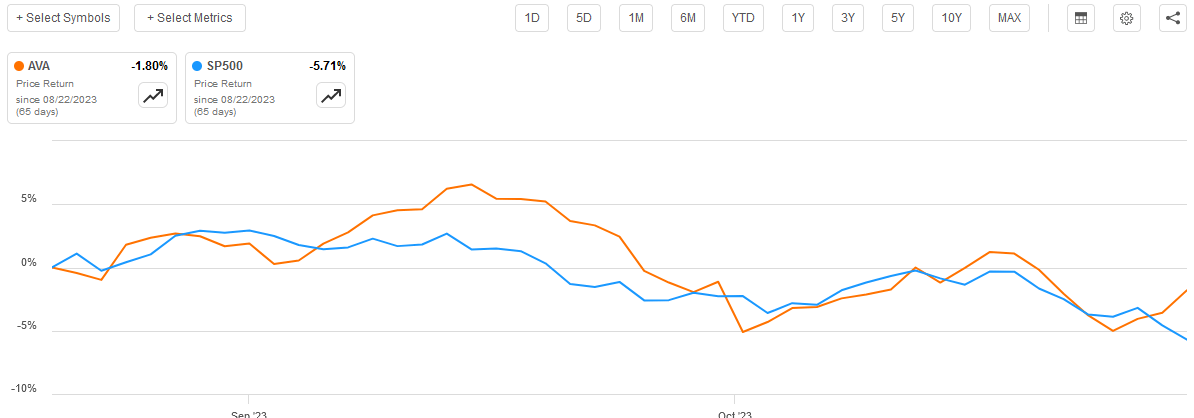

As regular readers can likely recall, we last discussed Avista Corporation around the end of August. The stock's performance since that time has not been too bad, as it is only down 1.80%, which is quite a bit better than the S&P 500 Index ( SP500 ):

{kind=link}

Avista Corporation has also significantly outperformed the iShares U.S. Utilities ETF ( IDU ), which is down 4.89% since the last time that we discussed this company. While the fact that the stock is down over the past two months certainly will not be sending any potential investor jumping for joy, the fact that Avista has delivered a strong performance relative to some of the other things that could be invested in is cause for optimism. Despite this relative outperformance, though, Avista Corporation does not appear to be overvalued, and in fact, the company is currently trading with a reasonably attractive valuation. Thus, a case could still be made for purchasing it even though the stock price has not been going up.

About Avista Corporation

As mentioned in the introduction, Avista Corporation is a regulated electric and natural gas utility that operates in the Pacific Northwest states of Washington, Oregon, and Idaho. The company also has a presence in the state of Alaska as the provider of electricity to the state's capital, Juneau.

{kind=link}

With the possible exception of a handful of small cities in eastern Washington, most of the company's service territory is sparsely populated. Thus, its customer base is somewhat less than might be expected. In the Pacific Northwest, the company serves 411,000 electric and 377,000 natural gas customers. There is a significant amount of overlap though, so many of the company's customers actually purchase both utility services from it. Add to that the 17,000 customers that the company has in Alaska, and we can still see that the company serves far less than one million people despite being a large utility in multiple states.

Utilities in general have been popularly called widows and orphans' stocks. This comes from the fact that they enjoy remarkable stability over time, so retirees and other people who are looking for safety will frequently buy them because they continue to perform regardless of macroeconomic events. I explained the reason for this in my previous article on the company:

The reason why the company's financial performance seems to be highly resistant to economic fluctuations should be fairly obvious. The products provided by Avista Corporation are generally considered to be necessities for our modern way of life. After all, there are not many people in the United States who do not have electric service in their homes or businesses. Indeed, most people take it for granted that any place they go will have working electricity so that they can charge their smartphones and other devices. The same is generally true for natural gas, as people tend to simply assume that the furnace will begin heating up their home as soon as they use the thermostat to turn on the heat. As such, most people will prioritize paying their utility bills ahead of making discretionary expenses during periods in which money gets tight.

In the previous article, I showed that Avista Corporation's revenues and cash flows have been quite stable over the past two years. The same is generally true when we look at these figures over a much longer period. For example, here are the company's annual revenues over the past decade:

{kind=link}

While we do see a pretty significant jump in 2022, overall, there is not a great deal of variation here. The company's cash flows exhibit a bit more variation, but the same general thesis holds true:

{kind=link}

Events such as the COVID-19 lockdowns, the incredibly high inflation of 2021 and 2022, and the fact that energy prices varied significantly over this entire period had absolutely no impact on the company's revenues or operating cash flow. This is a very positive sign, and it is something that we very much like to see with a company that we are invested in. This is especially true when we consider that there is a not insignificant probability that the economy will enter into a recession in the near future. Indeed, there are an increasing number of signs that the "soft landing" scenario that the market still expects is quite unlikely to actually occur. Indeed, as Jamie Dimon of JPMorgan Chase ( JPM ) recently stated ,

Fiscal spending is more than it's ever been in peacetime and there's this omnipotent feeling that central banks and governments can manage through all this. I am cautious about what will happen next year.

Mr. Dimon has put his money where his mouth is, as he sold one million shares of JP Morgan's stock for the first time in his career. While this hardly represents his whole position in the bank, Mr. Dimon has been recently expressing a great deal of doubt over the capabilities of the Federal Reserve to actually achieve a soft-landing scenario in the face of holding interest rates far too low for too long. Thus, there is reason to believe that an economic downturn may be rapidly approaching.

Even if the American economy manages to avoid such a downturn, it would still probably be a good idea to be prepared and fortunately, the overall stability of Avista Corporation's finances over the past decade could position it much better to handle such a scenario than many other things that could be invested in.

Recent Performance

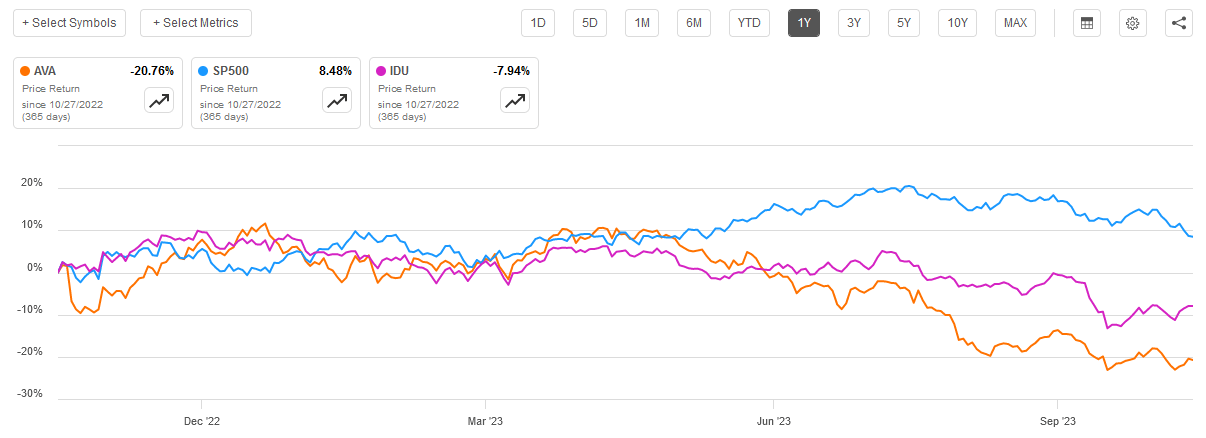

Unfortunately, the company's stock price has not been exhibiting the same stability as the company's finances. Over the past year, shares of Avista Corporation are down 20.76%. This is far worse than the 7.94% decline of the U.S. Utilities Index over the same period. It is also quite a bit worse than the S&P 500 Index, which is actually up over the past twelve months:

{kind=link}

This certainly does not inspire much confidence about the company's ability to serve as a safe haven through potential economic turbulence. However, as we saw in the introduction to this article, Avista Corporation has actually been doing much better than both of the above indices over the past two months. This could indicate that the worst of the stock price decline is behind us. At least, unless interest rates go significantly higher from here.

This comes from the fact that utility stocks like Avista are generally thought of as bond proxies. After all, the basic proposition of a bond is that investors receive relatively stable performance over an extended period of time. This is exactly what Avista Corporation aims to deliver. As we discussed in the last article regarding this company, Avista Corporation is positioned to grow its earnings per share at a slow but steady 4% to 5% rate over the next five years. When we combine this with the company's current 5.72% yield, this means that the company should be able to deliver a total average annual return of around 10% over the period. This is true regardless of the economic conditions that are present over the period. That is basically a pretty similar return profile to a bond.

As such, if interest rates go higher, we can probably expect that Avista's share price will come under pressure. As I pointed out in a few recent articles, such as this one , rates may be higher than expected due to the fiscal policy of the U.S. Federal government. This is exactly what Mr. Dimon is warning about as well.

However, Avista may hold up better than some other utility stocks in such a scenario. This is because this stock has already fallen at a much more rapid rate than the rest of the utility industry. Thus, the company's stock may hold up better than the rest of the industry going forward. We will get further confirmation about this in just a few minutes when we compare its current valuation to the rest of the industry.

Financial Considerations

As I pointed out in my last article on Avista Corporation:

It is always important that we investigate the way that a company is financing its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. That is usually accomplished by issuing new debt and using the proceeds to repay the existing debt. After all, very few companies have sufficient cash on hand to repay their debt as it matures. This process can cause a company's interest expenses to go up following the debt rollover, depending on the conditions in the market.

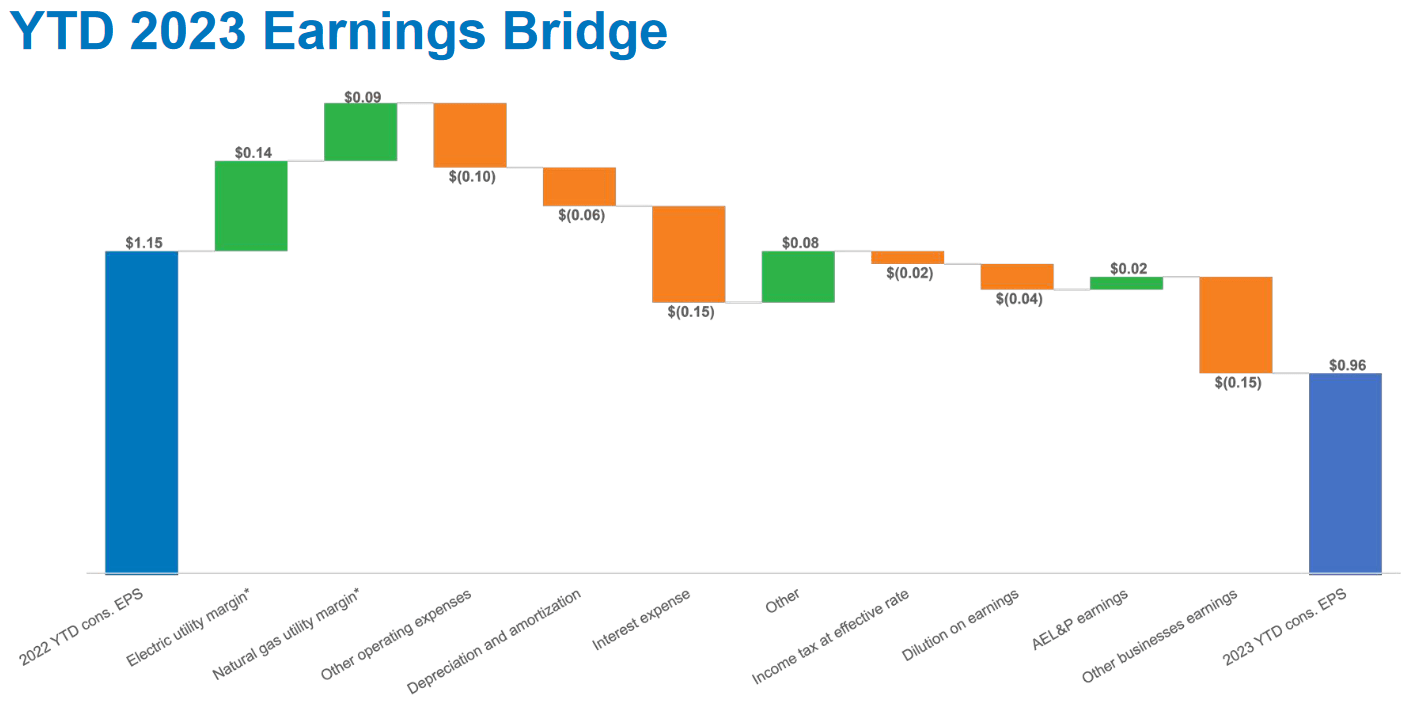

This could be a very important consideration today. This is due to the fact that interest rates are currently very close to the highest level that we have seen in the 21st century. As such, just about any debt rollover today is likely to cause a company's interest expenses to increase as the newly issued debt will probably have a higher interest rate than the maturing debt. Avista is certainly not immune to this, as one of the biggest reasons why the company's year-to-date 2023 earnings per share came in below the same period of last year is that the company's interest expenses were higher. As we can see here, interest expenses alone reduced the company's earnings per share by $0.15 year-over-year:

{kind=link}

This is partly due to a significant increase in the company's debt load. On June 30, 2023, Avista Corporation had a net debt of $2.9066 billion compared with $2.6146 billion on June 30, 2022. The higher level of debt obviously makes it much more expensive for the company to service its debt. This is due to the higher interest rates that exist today. Over most of the past twenty years, interest rates were sufficiently low that increases in a company's debt load were not a big deal because the incremental interest payments were negligible. That is no longer the case, as we can clearly see here:

{kind=link}

We can clearly see that the company's debt-servicing expenses started to increase fairly quickly over the past twelve months or so. This will, unfortunately, serve as a drag on the company's earnings per share growth. After all, Avista Corporation is planning capital expenditures of $475 million during each of the next three years and it will need to finance this somehow.

With that said Avista Corporation still remains conservatively financed relative to its peers. We can see this quite clearly by looking at its net debt-to-equity ratio. As already mentioned, Avista Corporation has a net debt of $2.9066 billion compared to a shareholders' equity of $2.4004 billion. That gives the company a net debt-to-equity ratio of 1.21 as of June 30, 2023. Here is how that compares to its peers as of the same date:

| Company |

| Net Debt-to-Equity |

| Avista Corporation |

| 1.21 |

| DTE Energy Company ( DTE ) |

| 1.89 |

| NorthWestern Energy Group, Inc. ( NWE ) |

| 0.99 |

| The AES Corporation ( AES ) |

| 4.05 |

| American Electric Power Company, Inc. ( AEP ) |

| 1.83 |

As we can see, Avista Corporation is less reliant on debt than many of its peers. This is not to imply that Avista Corporation can cavalierly ignore the consequences of its financial structure in a high-interest rate environment. However, it does mean that the company does not appear to be too aggressive with respect to its financial structure and may be less affected by rising rates than its peers. Overall, this is an acceptable, if not necessarily desirable situation.

Valuation

According to Zacks Investment Research , Avista Corporation will grow its earnings per share at a 6.35% rate over the next three to five years. This is actually higher than management's guidance of 4% to 5% but it is certainly not out of line for a utility. At the current share price, this growth rate gives Avista Corporation a price-to-earnings growth ratio of 2.19. That is a fairly big discount from the 2.29 ratio that the company had back at the end of August. Here is how it compares to its peers:

| Company |

| PEG Ratio |

| Avista Corporation |

| 2.19 |

| DTE Energy |

| 2.65 |

| NorthWestern Energy Group |

| 2.70 |

| The AES Corporation |

| 1.38 |

| American Electric Power |

| 2.98 |

Here we can certainly see how the company's fairly significant twelve-month underperformance relative to the rest of the index has provided an interesting opportunity. Avista Corporation looks remarkably cheap relative to most of its peers. Yes, there may be some who point out that The AES Corporation appears cheaper, but that company has substantially higher debt and that is not what you want in a high-interest rate environment. Thus, there may be an opportunity here.

Conclusion

In conclusion, Avista Corporation has been proving much more stable in terms of its stock price than many of its peers over the past few months. This could be a sign that the worst is behind it, as the company is looking quite cheap right now and a 5.72% dividend yield is rather difficult to pass up. While it has been impacted negatively by the rising interest rate environment, Avista Corporation boasts a stronger balance sheet than much of the sector along with a lower reliance on debt. When we combine this with an attractive valuation, it could be worth picking up some shares as a "safe haven" play in the face of a potential economic calamity.

For further details see:

Avista: Holding Up Pretty Well, But Still Has Attractive Valuation Vs. Peers