AVA - Avista Is A Solid Long-Term Buy

2023-12-11 02:34:00 ET

Summary

- Avista is a utility company that operates in the electric and natural gas sector, with a focus on renewable energy.

- The company has shown steady revenue and earnings growth over the past decade, with a 20-year streak of annual dividend increases.

- Avista is attractively valued with a P/E ratio of 15.3 and offers a 5.2% dividend yield, making it a solid investment opportunity.

Introduction

Over the last two weeks, I have been looking at the utilities sector. I lack some exposure to the sector and decided to revisit some companies on my watchlist. The sector offers a relatively high dividend yield together with low volatility and high stability due to the tight regulation of the state. Before interest rates decrease, this might still be an excellent opportunity to increase my exposure.

While I hold giants like Southern Company ( SO ) in this segment, I prefer to seek smaller companies. These companies usually operate under the radar with less coverage. These companies are often undervalued when adding their "boring" sector. In this article, I will look at one of my favorite companies in the sector: Avista ( AVA ).

Seeking Alpha's company overview shows that:

Avista operates as an electric and natural gas utility company. It operates in two segments: Avista Utilities and AEL&P. The Avista Utilities segment provides electric distribution and transmission, and natural gas distribution services in parts of eastern Washington and northern Idaho, and natural gas distribution services in parts of northeastern and southwestern Oregon, as well as generates electricity in Washington, Idaho, Oregon, and Montana. The AEL&P segment offers electric services in the city and borough of Juneau, Alaska. The company generates electricity through hydroelectric, thermal, and wind facilities. It also engages in venture fund investments, real estate investments, and other investments.

Fundamentals

Avista's revenues have grown over the last decade by almost 18%, which equates to less than 2% annually. The company grows its sales as customers increase and the states approve price increases. Moreover, Avista also invests in ventures that are not regulated. The primary source for sales growth is the classic rate hikes and expansion to more clients in more areas. In the future, as seen on Seeking Alpha, the analyst consensus expects Avista to keep growing sales at an annual rate of ~0.5% in the medium term.

Avista's EPS (earnings per share) has increased by 19% when using GAAP earnings. The company invests heavily, and it has to depreciate these investments. It aligns with the company's sales growth despite share issuance as it controls its expenses, supporting margins. As the company grows and more projects go online, the company will decrease costs and increase EPS. In the future, as seen on Seeking Alpha, the analyst consensus expects Avista to keep growing EPS at an annual rate of ~7% in the medium term.

Avista is on its way to becoming a dividend aristocrat with a 20-year streak of annual increases and 23 years without reducing the dividend payment. The company pays 80% of its EPS in the form of dividends. The payout ratio may look high, but this is not unique to companies in the sector. They enjoy the stability that comes with their position as a regulated monopoly. The company offers an attractive 5.2% yield to investors.

Unlike many dividend growth companies, Avista doesn't buy back shares. This is not unique among utilities as they constantly need to raise capital. The company already has high leverage, so it has to issue shares for capital as the free cash flow is negative due to the constant investments. Over the last decade, the number of shares increased by 29%, and the company still managed to grow its EPS.

Valuation

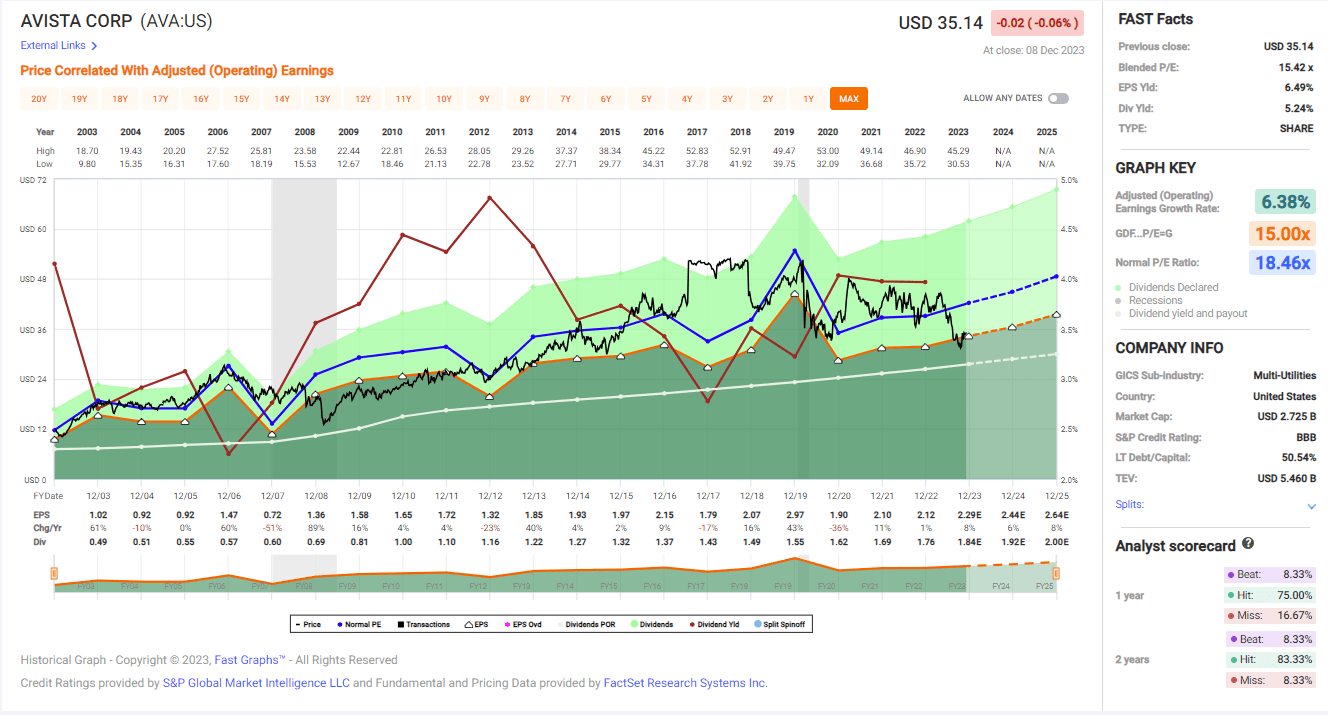

Avista's P/E (price to earnings) ratio stands at 15.3 when using the EPS forecasts for 2023. This is an attractive P/E for a company that is forecasted to show a mid-single-digit growth rate and enjoys being a monopoly in its region. The company's current valuation is almost as low as we have seen over the last twelve months. This valuation seems like a decent entry point for Avista, as investors give some discount to the company, probably due to the higher leverage.

The graph below from FAST Graphs emphasizes that Avista is attractively valued. The company's average P/E ratio over the last two decades is 18.5, and the current is 15.3. The company's growth rate over these two decades was 6.4%, and the current forecasted growth rate is 7%. Therefore, the company offers a decent combination of lower-than-average and higher-than-average valuations.

{kind=link}

Opportunities

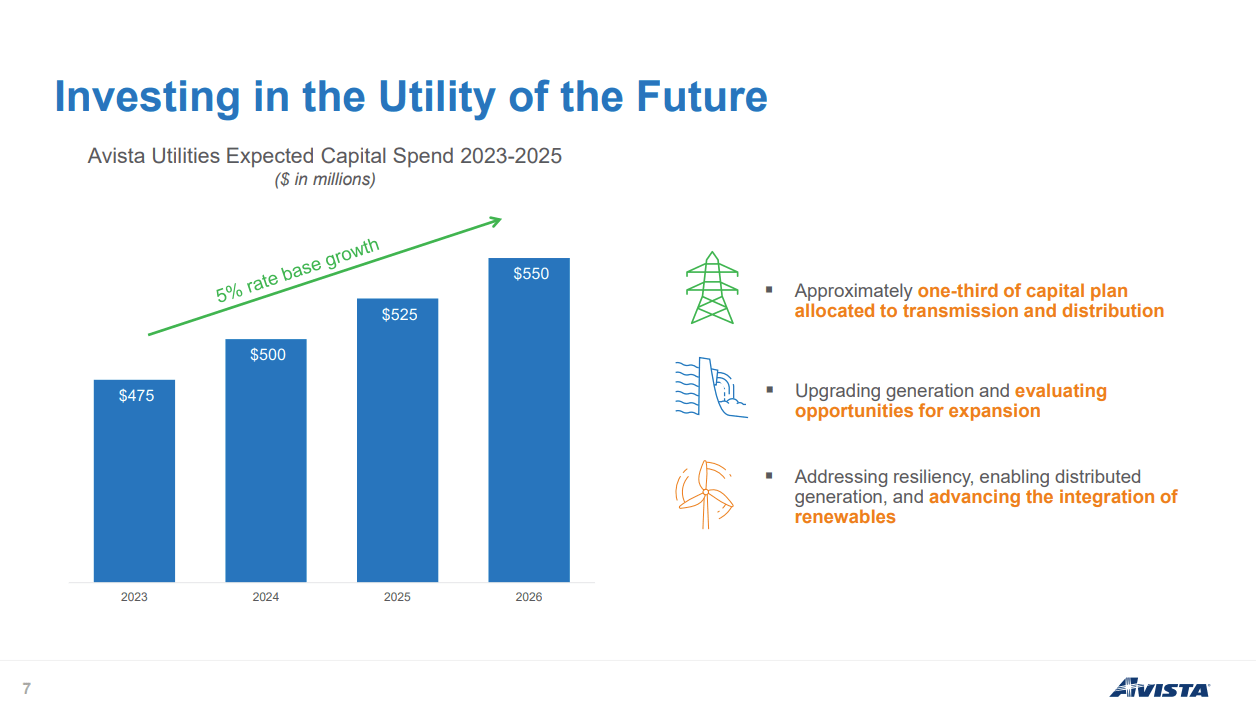

The first growth opportunity is the expansion of the owned generation portfolio. Avista is actively exploring opportunities to expand its owned generation portfolio, aiming to meet the increasing demand for clean energy. This initiative aligns with the company's commitment to achieving its clean energy goals and addressing the challenges of a rapidly changing energy landscape. By strategically investing in generation assets, Avista aims to enhance its capacity for renewable energy production, contributing to a more sustainable future .

" As we explore options, rest assured, we will be prudent and wise with our decisions. How might we possibly expand our owned generation portfolio? Ideas like these tap into the built environment to create a battery of sorts, moving us closer to achieving our clean energy goals and can help make energy more affordable for everyone ."

(Dennis Vermillion - President and CEO, Q3 2023 Conference Call)

Another opportunity is the development of its transmission network. Avista sees potential growth opportunities in the development of transmission assets. With a focus on supporting the integration of renewables, the company aims to play a crucial role in advancing clean energy goals. The strategic evaluation of transmission projects reflects Avista's commitment to enhancing its infrastructure to facilitate efficient and reliable energy transmission, contributing to a more sustainable and resilient energy grid that connects smaller generation units to the grid.

" How might we meet the demand for transmission assets as we move toward our clean energy future? We are evaluating opportunities as they come up to explore the expansion of our generation assets as well as potential transmission projects to support the integration of renewables and to propel us towards our clean energy goals ."

(Kevin Christie - SVP and CFO, Q3 2023 Conference Call)

{kind=link}

Lastly, the company also sees an opportunity in strategic partnerships for energy management in buildings. Avista is exploring partnerships with building owners and operators to manage energy consumption in buildings actively. This innovative approach involves controlling the amount of energy used and optimizing when it is utilized. By leveraging the built environment, Avista aims to create a flexible and efficient energy storage system, contributing to cleaner energy consumption and affordability for consumers .

" How might we partner with building owners and operators to actively manage not only how much energy these buildings use but when they use it. Ideas like these tap into the built environment to create a battery of sorts, moving us closer to achieving our clean energy goals and can help make energy more affordable for everyone ."

(Dennis Vermillion - President and CEO, Q3 2023 Conference Call)

Risks

The first risk is volatility in earnings due to the valuation of investments. Avista faces the risk of earnings volatility driven by the valuation of specific assets. While these investments contribute to learning, economic development, and energy innovation, their valuation can cause fluctuations in quarterly earnings. The company acknowledges losses in other businesses, primarily attributed to these valuation adjustments, leading to potential challenges in maintaining stable financial performance . Higher rates are one leading reason for valuation change as they affect the discount rate of future cash flows.

" Quarterly valuation of certain investments can cause some volatility in our earnings, increasing the transparency of these investments' value. We've recognized net losses in our other businesses, primarily due to valuation adjustments ."

(Kevin Christie - SVP and CFO, Q3 2023 Conference Call)

Another risk is the impact of higher costs on cost management. Avista's cost management efforts have been successful, but the effect of higher resource costs, mainly due to poor hydro performance, poses a challenge. Despite effectively managing costs, the company cannot fully offset the financial impact of increased resource costs. This challenge necessitates narrowing the consolidated earnings guidance range for the year, reflecting the potential limitations of cost management in the face of external factors .

" Due to these higher resource costs, we are narrowing our 2023 consolidated earnings guidance range. We've successfully managed our costs, but we cannot fully offset the impact of higher resource costs due to the year's poor hydro performance ."

(Kevin Christie - SVP and CFO, Q3 2023 Conference Call)

Lastly, the current business environment makes it harder for the company to issue shares or long-term debt. Avista's liquidity management includes planned issuances of common stock and long-term debt, subject to market conditions. The company acknowledges the dependency on favorable market conditions for executing these plans. Changes in market dynamics could impact the success and timing of stock issuances and debt funding, introducing uncertainty and potential challenges in meeting capital expenditure requirements .

" In 2024, we expect to issue approximately $80 million of long-term debt and $60 million of common stock, depending upon market conditions. During the fourth quarter of 2023, depending upon market conditions, we plan to issue $32 million of common stock ."

(Kevin Christie - SVP and CFO, Q3 2023 Conference Call)

Conclusions

To conclude, Avista is an excellent company in the utilities sector. It offers investors solid growth in sales and EPS, which leads to dividend growth. The company offers a 5.3% yield with several growth opportunities that will help the company increase in the medium and long term. The company's risks are present, yet they are mostly short-term. The company does have to deal with its leverage, which makes it harder to raise capital using debt or equity.

Still, when the company trades for 15 times earnings, I believe there is enough margin of safety for investors. Therefore, I rate Avista as a BUY for investors seeking a solid, growing company. They can enjoy a 5% dividend with a mid-single digit growth rate for an above 10% total return with what I believe to be limited risks.

For further details see:

Avista Is A Solid Long-Term Buy