RCEL - AVITA Medical Positioned For Stellar 2024 With Skin Repair Innovation Momentum

2023-12-19 20:38:32 ET

Summary

- AVITA Medical's Spray-On Skin Cells device rapidly processes a patient's own skin to treat large dermatological injuries.

- The company's sales growth is expected to accelerate in 2024 due to the supplement of its RECELL System for full-thickness skin defects.

- AVITA's expanded FDA label approval has significantly increased its addressable market, with an opportunity in excess of $2.7 billion in the US alone.

AVITA Medical, Inc. ( RCEL ) is a unique play on regenerative medicine. Its novel device rapidly processes a small sliver of a patient’s own skin to create a mixture of “Spray-On Skin Cells”. This mixture of cells is applied by trauma and burn surgeons to treat large dermatological injuries. 2024 is shaping up to be a year that this microcap rewards shareholders with rapid sales growth, resulting from the June 2023 premarket approval ((PMA)) supplement of its RECELL® System to treat full-thickness skin defects, kicks in.

Background

I last provided an update on AVITA Medical on August 10, 2023 in an analysis titled, AVITA Medical's 'Better Mousetrap' Rapidly Gaining Traction in Skin Repair, soon after full-thickness wound label expansion was approved. The shares have weakened since due primarily to a couple of temporary hiccups in the AVITA story that will be discussed later.

The heart of the company is the RECELL Autologous Cell Harvesting Device. As shown below, the kit includes a small device, an enzyme, and other disposable tools that allow a surgeon to take a stamp-sized sliver of the patient's skin and process it into a cocktail of the patient’s autologous desegregated skin cells that are sprayed onto the patient’s wound.

AVITA Medical, Inc.

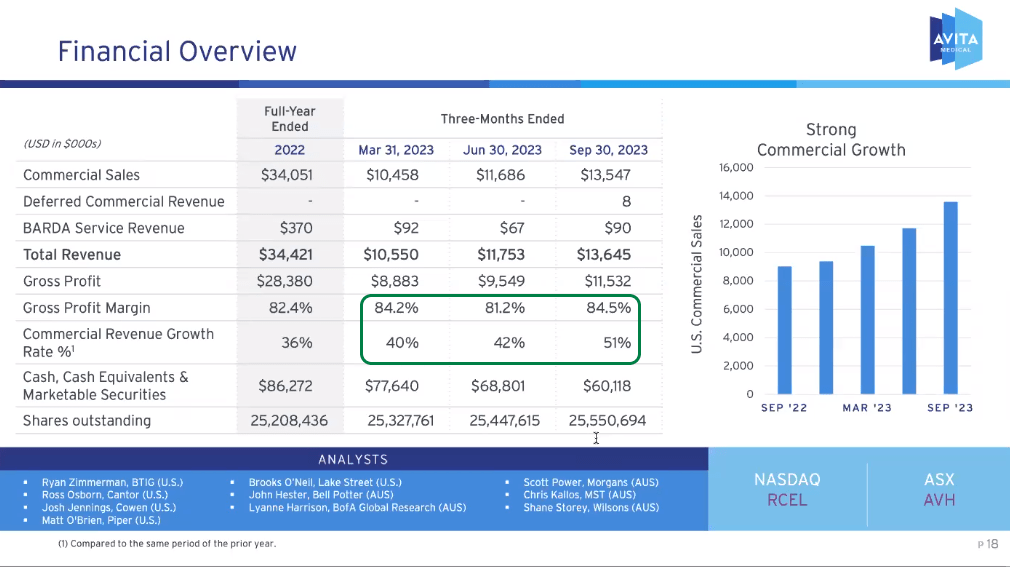

These cells are the seeds that can expeditiously heal a wound as large as 80 times larger than the sample taken . Unlike an untreated wound that can only heal from the wound edges, a RECELL-treated wound heals uniformly across the injury. This intuitively simple procedure is superior to conventional skin grafts as the patient is subject to reduced pain and trauma and also benefits from faster healing. The related savings to the health care system are a significant driver of sales growth as the RECELL procedure has rapidly caught on. In the table below, provided by the company, the accelerating sales growth and very attractive gross margins are highlighted. These are key 2024 factors positioning the company’s move towards profitability and thus creating shareholder value that translates into improved stock price performance.

{kind=link}

AVITA Medical, Inc.

AVITA’s Expanded Market with Recent FDA Label Expansion

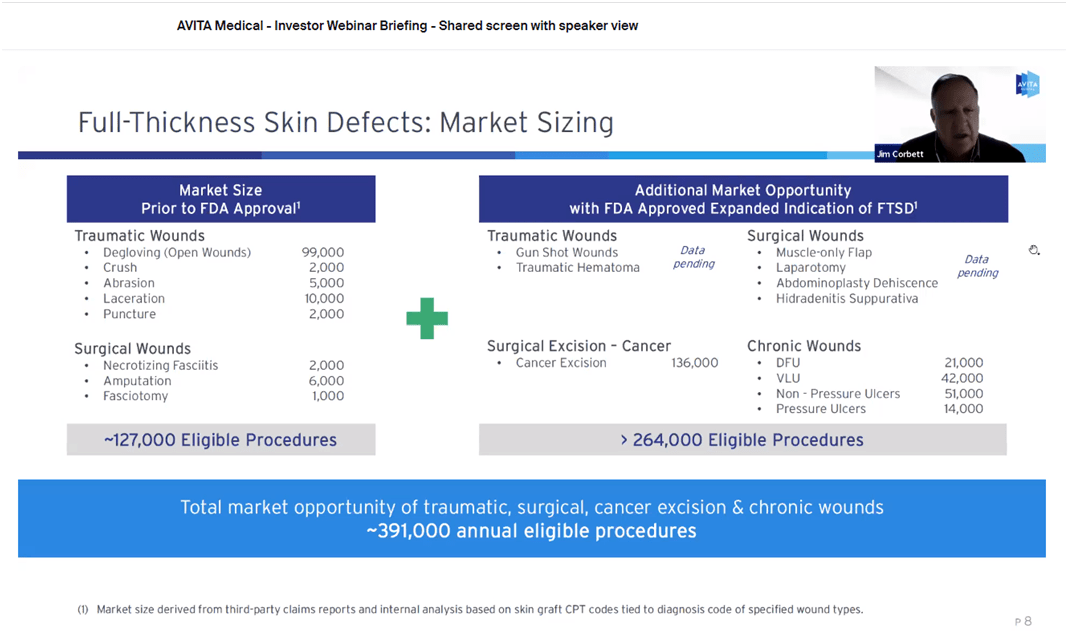

On an investor webinar held in August 2023, the company revealed a significant upside surprise that it hadn’t fully understood when full thickness skin graft approval was initially granted a few months prior. Prior to the June 2023 approval, the addressable U.S. market the company targeted was limited to 25,000 burn cases in about 150 burn centers. The burn market approval alone is reflective of the sales growth for each period shown above, except for the September 2023 quarter when the FDA full-thickness wound approval was in place for the entire quarter. With this expanded approval, the company was anticipating an additional 127,000 eligible procedures. However, the FDA approval included significantly more eligible indications than expected, including chronic and cancer wounds, as the following slide from the company’s second quarter earnings webinar illustrates:

{kind=link}

AVITA Medical, Inc.

AVITA’s annual addressable market in the U.S. had instantly expanded from 25,000 cases to 391,000+ cases with that single FDA label expansion; all concentrated in burn and trauma centers. With a procedure sales price set at about $6,500, that equates to an opportunity in excess of $2.7 billion (35,000 burns + 391,000 full thickness cases) in the U.S. before accounting for the rest of the pipeline that will be discussed later.

Most of these procedures listed above take place in Level I, II & III Trauma Centers. These centers also treat an additional 10,000 burn wounds that the company hadn’t been targeting up until now. Another significant positive to this story is that all these additional procedures use the same Diagnoses-Related Group ( DRG) codes that the company uses for burns. There is no sales ramp wait time necessary to apply for additional coding, an unusual advantage for new indications. On the same company call, CEO James Corbett specifically noted the 136,000 cancer-related surgical excision cases as a large unexpected opportunity given the patient-centric advantages of the RECELL procedure and cost savings to the health care system. This will be one of the initial areas of focus for the expanded sales team that has roughly been doubled in size this year to handle the expanded market.

In the Pipeline - Vitiligo - Another Large Market for Potential Future Growth

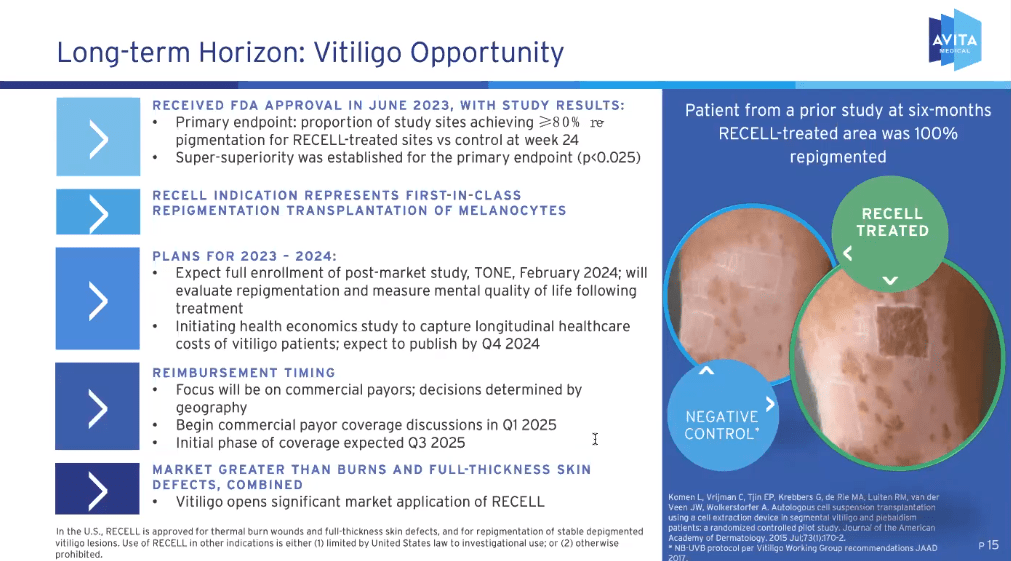

Vitiligo is an autoimmune skin condition where the immune system causes blotches of loss in skin color. AVITA obtained FDA approval of the RECELL treatment for stable vitiligo on June 16th, 2023. This is another large market opportunity that was worth about $1.5 billion in 2022. However, AVITA is guiding toward a measured commercial launch starting in the second half of 2025. The reason for this phased rollout is the time needed to demonstrate healthcare savings to payers. Vitiligo is not a dangerous or contagious condition. However, it can create quality of life and mental health issues for patients. In order to obtain insurance coverage for the procedure and attempt to create a commercial success, the company is running an additional 100 patient study called TONE with the twin goals of once again demonstrating regimentation, but also showing improvement in quality of life and mental health. A further analysis is planned to quantify the savings to the healthcare system that will be used in the goal of obtaining insurance reimbursement. Enrollment is expected to be completed within the next month or two. As discussed, this is a longer-term project that will take time to develop. The company summary of this opportunity is shown below.

{kind=link}

Vitiligo Opportunity ( AVITA Medical, Inc.)

International Growth Prospects

AVITA has chosen partnering as a strategy to expand internationally, which is a smart low capital, lower-risk approach to enter a complicated market. Each international market has its own regulatory, reimbursement framework, and other challenges and it makes sense to look for partners with local expertise and distribution networks already in place.

AVITA Medical's distribution partner in Japan is COSMOTEC, a subsidiary of the M3 Group Company. COSMETIC obtained PMDA approval for the RECELL® System in Japan, initially for the treatment of burns, in February 2022. The M3 group is a healthcare provider with a $10.4 billion market cap. In September 2022, COSMOTEC obtained insurance reimbursement approval for burn wounds and is expected to follow AVITA's path and seek approval for additional indications in Japan.

On November 9 th , 2023 an agreement was signed with PolyMedics Innovations GmbH for exclusive RECELL distribution rights in Germany, Austria, and Switzerland, with an option to expand to additional European markets in the future. AVITA has and will provide training and regulatory assistance in return for a 50% share of revenues in both of these agreements. International growth is currently in early stages but should grow quickly as the advantages of the RECELL system are demonstrated to surgeons. Of the total $35,948,000 in revenues for the 9 months ended September 30, 2023, $2,569,000 came from international sales , up from $849,000 for the prior year.

Recent Developments that have Pressured Shares

AVITA shares have done well in 2023 but are well off their 2023 high of $21.70:

{kind=link}

Seeking Alpha

Aside from the normal market volatility and the relative over/underperformance of different market segments over the year, the shares have been recently pressured by two recent poorly received company updates that will now be discussed:

I. RECELL GO Approval Delay

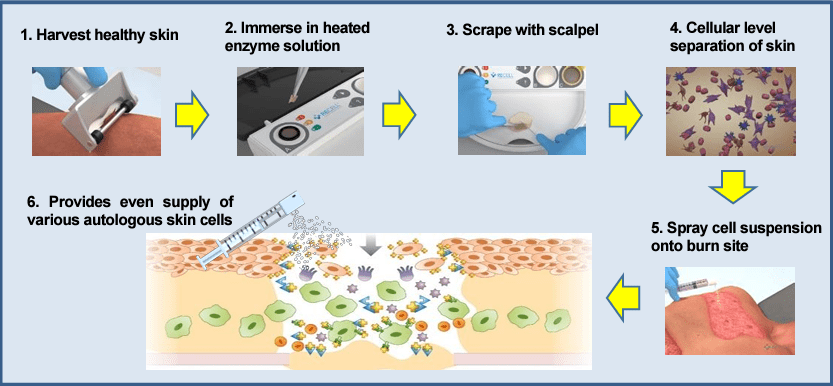

The first bit of bad news came on October 2 nd and is related to a very important upcoming innovation called RECELL GO. RECELL GO is the next generation of the RECELL system that will automate the cell harvesting process. The current RECELL system is a manual system involving multiple steps as shown below:

{kind=link}

Cosmotec Press Release

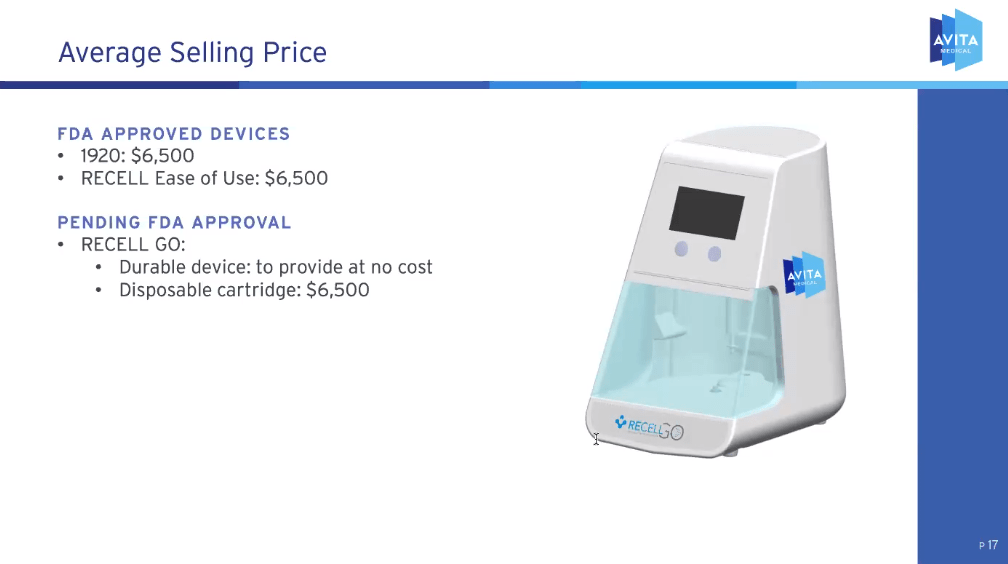

In this current system, the entire kit is disposable and the process requires extensive training from AVITA and the involvement of the surgeon to manually scrape the skin graft after it has been sitting in a heated enzyme solution. The new RECELL GO system (shown below) will completely automate this step to about 30 minutes of processing time. All the trauma surgeon will need to do is obtain the small skin sample and let RECELL GO do the rest, freeing up the surgeon to do other things.

{kind=link}

AVITA Medical, Inc.

The RECELL GO processing unit will be provided at no cost by AVITA and small disposable cartridges will be sold at $6,500 for each procedure. The company now anticipates about 200 cartridge based procedures can be performed with each RECELL GO device. This simplified process will reduce the level of training needed in the sales process, leaving more time to reach new accounts.

The bad news on RECELL GO that rocked shares came on October 2 nd when it was disclosed that the FDA was seeking more data on the RECELL GO device and, as a result, there would be a 4-6 month delay in approval. Shares dropped sharply on the news but it seemed like an overreaction given the current healthy strong sales growth. Nonetheless, the market reacts the way the market reacts.

II. Company Guidance Confusion

The next mishap was an unforced error in company guidance. In the third quarter earnings release of October 18th, the company stated, “Guidance for full year 2023 commercial revenue remains unchanged and is expected to be in the range of $51 to $53 million.” Then, only about a month later, the company revised guidance lower to a range of $49.5 to $50.5 million. The explanation, as provided, was the “result of slower-than-anticipated progression through the customer’s Value Analysis Committee ((VAC)) processes, driven by the expanded label applications of its newest indication, full-thickness skin defects.” To explain further, due to the greater diversity of indications treated in comparison to burn wounds alone, the company underestimated how the many additional individuals involved in the decision-making process would affect the VAC decision timeframe. In the long run, this is not really a big deal. However, a guidance revision over such a short time frame looked really bad and spooked investors, once again damaging shares. Again, the market reacts the way the market reacts.

To recap, these two situations are mentioned because they have been at least partially responsible for the slide in share price. When looking at the big picture, it still comes back to a unique device that has already shown healthy adoption rates in burn injury and now has FDA approval to pursue an opportunity about 16 times larger than their 25,000 burn case universe of just 6 months ago. To reiterate, the AVITA sales force has doubled in size this year to take advantage of this opportunity.

Cash Position Recently Strengthened Through Non-Dilutive Debt

At the end of the September 2023 quarter, the company had cash and marketable securities totaling about $60,000,000. Subsequently, on October 18 th , the company boosted its cash position by $40,000,000 with a new credit agreement. The relevant details can be found in this SEC filing . The agreement was also described in AVITA’s third quarter conference call :

As Jim mentioned, we entered into a credit agreement with OrbiMed on October 18th. The debt facility provides us access up to $90 million, of which $40 million was funded at closing. Two $25 million tranches are available at our option. The first $25 million is available on or before December 31, 2024, but only if our net revenue is $75 million or more for the last 12 months. If and only if we draw the first tranche, then the second tranche of $25 million is available again at our option on or before June 30, 2025, but only if our net revenue is $100 million or more for the trailing 12 months prior to the month of a drawdown of the second tranche. At the current time, we do not have need for either $25 million tranche. And given our revenue growth and expectations of reaching cash flow breakeven, we do not foresee a need to take down either of the $25 million tranches before they expire. With our current cash balance and the $40 million funded at closing, we are confident that we have sufficient cash reserves to achieve our goals and reach profitability in 2025 .

The increased cash position of about $100,000,000 greatly reduces the near-term risk of dilution that is often associated with biotech microcaps. The primary intent of this agreement was to increase the working capital needed to fund sales growth without diluting shares in a secondary equity offering. The cash proceeds were invested in treasury securities to mitigate interest costs.

Risks

With the recent FDA market expansion approvals in full thickness skin grafts and vitiligo, the largest of risks of obtaining FDA approval have been mitigated. While the automated RECELL GO device is still subject to FDA approval, it simply represents a more consistent and efficient methodology over the already approved device and approval seems like a relatively low risk.

At this point in time, the major risk for AVITA is the execution by the sales force of their expanded and exciting opportunity. The company needs to continue to gain market share and maintain its advantages over competing products. In addition, investors should note that the RCEL shares are not very liquid with a daily 10-day average daily volume of only 132,700 shares. So expect volatility that will be painful on the days the market is slumping. Alternatively, when the market in small caps is rallying, don't get overly euphoric! AVITA still needs to execute or the gains will be fleeting.

Conclusion

A better mousetrap for skin repair with a greatly expanded market has set up shares in AVITA Medical for a promising 2024. Momentum should really be built with the introduction of the automated RECELL GO. This will soon be a blade-razor blade technology platform that already has very attractive gross margins. With a recently expanded sales force positioned to seize an expanded opportunity, all the elements for success are in place. Despite all these positives, AVITA’s market cap has declined to about $320,000,000, partially as a result of the unanticipated mishaps mentioned above that are only temporary in the bigger picture. In my view, therein lies today's opportunity for investors.

Editor's Note: This article was submitted as part of Seeking Alpha's Top 2024 Long/Short competition, which runs through December 31 . With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

AVITA Medical Positioned For Stellar 2024 With Skin Repair Innovation Momentum