CHMI - Avoid These REIT Fireworks At All Costs

2023-07-04 07:00:00 ET

Summary

- I could not wait to light the first bottle rocket.

- I lit the fuse, and I screamed out something like "get ready for the light show folks."

- At that moment, I knew something was terribly wrong.

I’ll never forget my lesson with fireworks.

I must have been around 12-years-old, and I was excited that it was Ju ly 4 th and I was going to Jack’s Quick Shop to buy some fireworks.

I had saved up around $100 from my job as a paperboy, and I decided that I would blow some dough on some firecrackers and bottle rockets.

My two best friends, Andy and Bobby, joined me at the store and they also forked out their life savings to buy some fireworks.

We decided to meet up at Dead Man’s Hill, which was a popular destination famous for sledding (although I don’t think anyone ever died on the hill).

First though, I went home and informed my mother that I would be out late celebrating, and that she could expect me around midnight. Of course, as mothers always do, she told me to be careful with fireworks, and to always point the bottle rockets up in the air.

I could not wait to light the first bottle rocket, and it seemed as if this once-in-a-year celebration was my reward for delivering newspapers for half a summer.

I told Andy and Bobby that I wanted to go first, so we decided to put all of our combined fireworks in a safe place, which was around ten feet away from our launch pad.

I pulled out a Black Cat bottle rocket and I pointed it straight up, just as my mother suggested. I then lit the fuse, and I screamed out something like "Get Ready for the light show folks."

At that moment, I knew something was terribly wrong.

The bottle rocket was sitting in an empty Coke can and just as I looked over at the bottle rocket, it was pointed directly at me.

The Coke can fell over and the bottle rocket was coming my way.

I dove hard on the ground, and the rocket exploded just in front of me, and directly into our treasure chest of fireworks.

Yes, it was a direct hit, and all the fireworks went off in one gigantic explosion.

I thought at the time that I had started World War 3.

I told Andy and Bobby that I was sorry for igniting the flame that caused all the fireworks to go up in smoke. (I had to pay them back too.)

When I got home my mother asked me why I decided to come back early, and I just smiled and said, “Mom, we had so much fun that I was simply blown away. Time flies when you’re having fun.”

Now, watch out for these risky REITs…

Avoid this Net Lease REIT

Global Net Lease ( GNL ) is an externally managed real estate investment trust (“REIT”) with a diverse portfolio of commercial properties that are typically acquired through sale-leaseback transactions and are leased to tenants on a net basis.

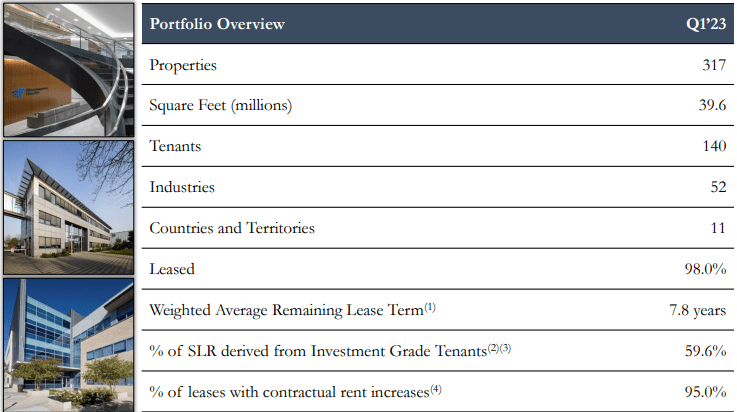

They’re globally diversified with properties in the U.S., Canada, and Europe and are diversified by asset mix with a portfolio of Industrial, distribution, office, and retail properties. In total, their portfolio consists of 317 properties that cover 39.6 million square feet and are leased to 140 tenants operating across 52 industries.

Their properties are 98.0% leased with a weighted average remaining lease term of 7.8 years and almost 60% of their straight-line rent (“SLR”) comes from investment grade tenants.

{kind=link}

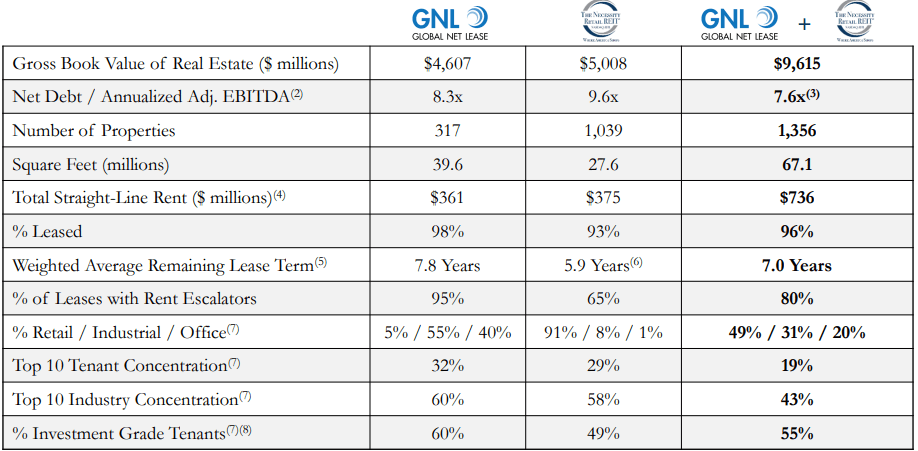

On May 23, GNL announced the merger between the company and The Necessity Retail REIT ( RTL ) which will internalize GNL’s management and is expected to reduce expenses by $75 million through cost synergies and internalization savings.

The merger will further diversify GNL’s property mix, and they expect the transaction to be 9% accretive to their first quarter adjusted funds from operations (“AFFO”) on a per share basis.

Additionally, after the merger GNL will own and manage approximately 1,350 properties that cover 67.1 million square feet. GNL’s post-merger leased rate will drop from 98% to 96%, their weighted average remaining lease term will drop from 7.8 years to 7.0 years, and their percentage of leases with rent escalators will drop from 95% to 80%.

{kind=link}

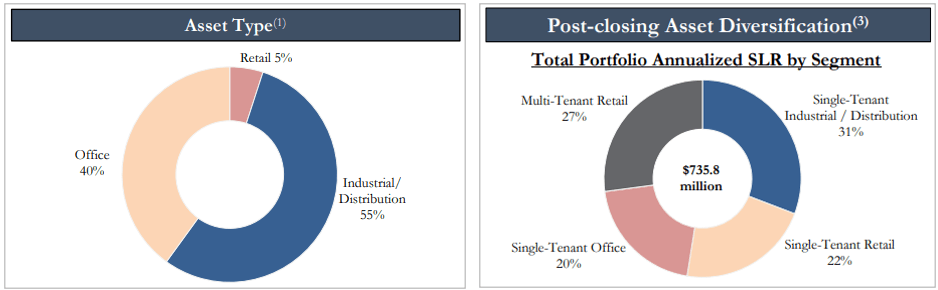

GNL’s asset mix post-merger will reduce their office exposure from 40% to 20%, their industrial / distribution properties will be reduced from 55% to 31%, while the retail properties will increase from 5% to 49%.

Additionally, their top 10 tenant concentration will be reduced from 32% to 19% and their top 10 industry concentration will be reduced from 60% to 43%.

{kind=link}

Global Net Lease has a BB+ credit rating which is one notch below investment-grade. GNL has relatively high levels of debt with an 8.3x net debt to adjusted EBITDA (7.6x expected post-merger), a long-term debt to capital ratio of 58.29%, and an interest coverage ratio of 2.85x.

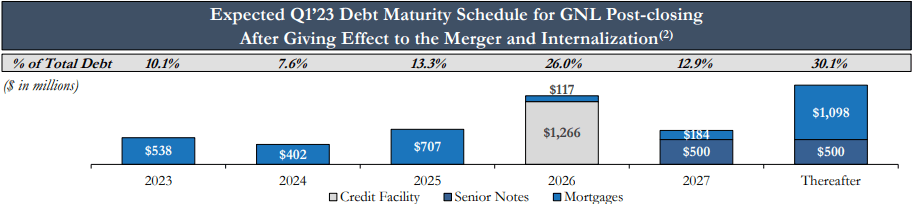

After the merger, GNL’s debt is expected to have a weighted average debt maturity of 3.7 years and a weighted average interest rate of 4.4%. As of the end of the first quarter, GNL had $119 million in cash and cash equivalents and $65 million available to them under their revolving credit facility for a total of $184 million in liquidity.

RTL had approximately $89.7 million in liquidity at the end of the first quarter. While the merger should increase GNL’s total liquidity, the post-merger debt maturity schedule is concerning with $538 million debt maturities in 2023 and $402 million debt maturities in 2024.

{kind=link}

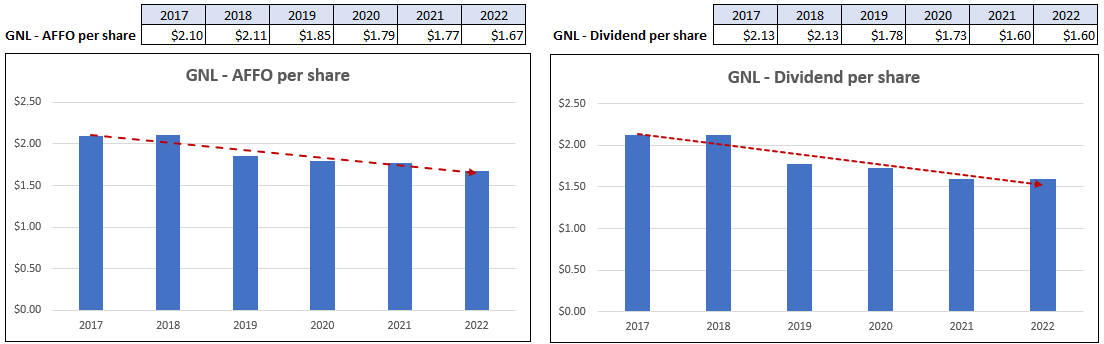

GNL’s earnings and dividend track record has been lacking over the past several years (that’s putting it kindly). AFFO per share has averaged a negative -4.85% growth rate since 2017 and fell by -6% in 2022.

Similarly, their dividend per share has averaged a negative -4.45% growth rate over this same time period.

The dividend was cut by -16.67% in 2019, -2.39% in 2020, and then -7.65% in 2021. In 2022 the dividend was maintained at $1.60 per share, down from dividend paid in 2017 of $2.13 per share.

{kind=link}

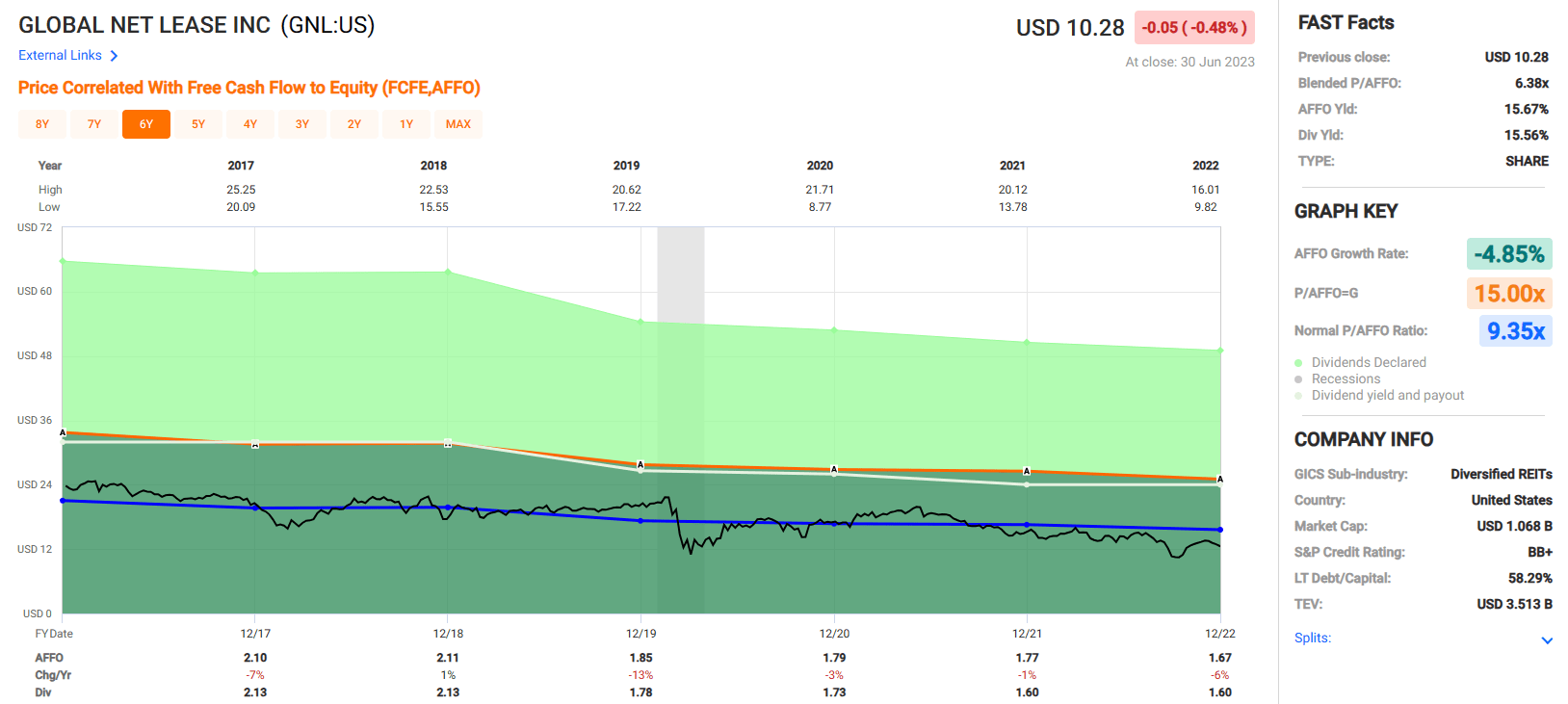

GNL currently pays a 15.56% dividend yield but the 2022 AFFO payout ratio is high at 95.81%. Per their latest presentation, GNL’s post-merger 2023 AFFO payout ratio should improve to 84%, but as it now stands, the payout ratio is concerning, and it remains to be seen how much the metric will improve after the merger closes.

As I pointed out in a recent article, “the merger will cut GNL's dividend and result in the company's credit ratings being put on negative watch by Fitch” while padding the pockets of the external manager, AR Global.

Currently GNL’s stock is trading at a P/AFFO of 6.38x, well below the normal AFFO multiple of 9.35x, but we're advising to avoid this REIT and have a Trim rating assigned to it due to its historical poor performance and high payout ratio.

iREIT© is avoiding GNL and RTL.

{kind=link}

A Chronic Dividend Cutter

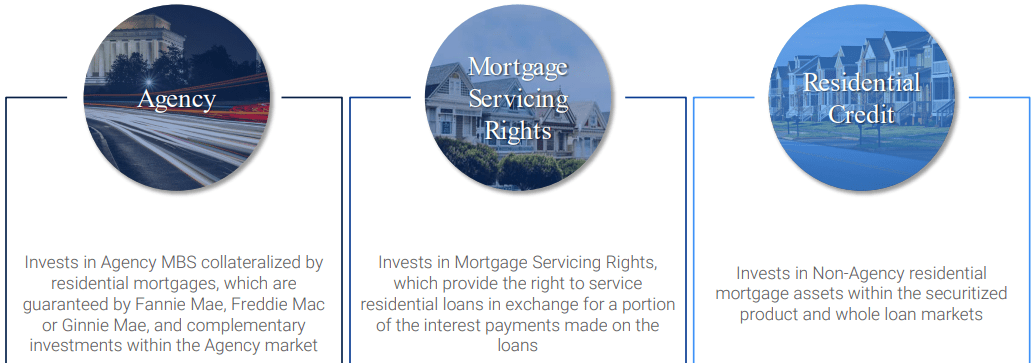

Annaly Capital Management ( NLY ) is an internally managed mortgage REIT (“mREIT”) that invests in multiple debt instruments that are collateralized by residential real estate. NLY conducts its business through these investment segments that include agency mortgage-backed securities, mortgage servicing rights, and residential credit.

Annaly’s agency group is their largest investment segment with $72.9 billion of assets as of the end of 2022. The agency group invests in mortgage-backed securities (“MBS”) that are backed by residential mortgages and are guaranteed by Fannie Mae, Ginnie Mae, or Freddie Mac.

NLY’s second largest segment is their residential credit group with $5.0 billion in assets. Through this segment, NLY invests in non-agency securitized products and whole loan markets that are backed by residential mortgage assets.

NLY’s mortgage servicing rights group makes up their smallest investment segment with $1.8 billion in assets. Through this segment, NLY invests in mortgage servicing rights which entitles them to a portion of the interest payments made by servicing residential mortgage loans.

{kind=link}

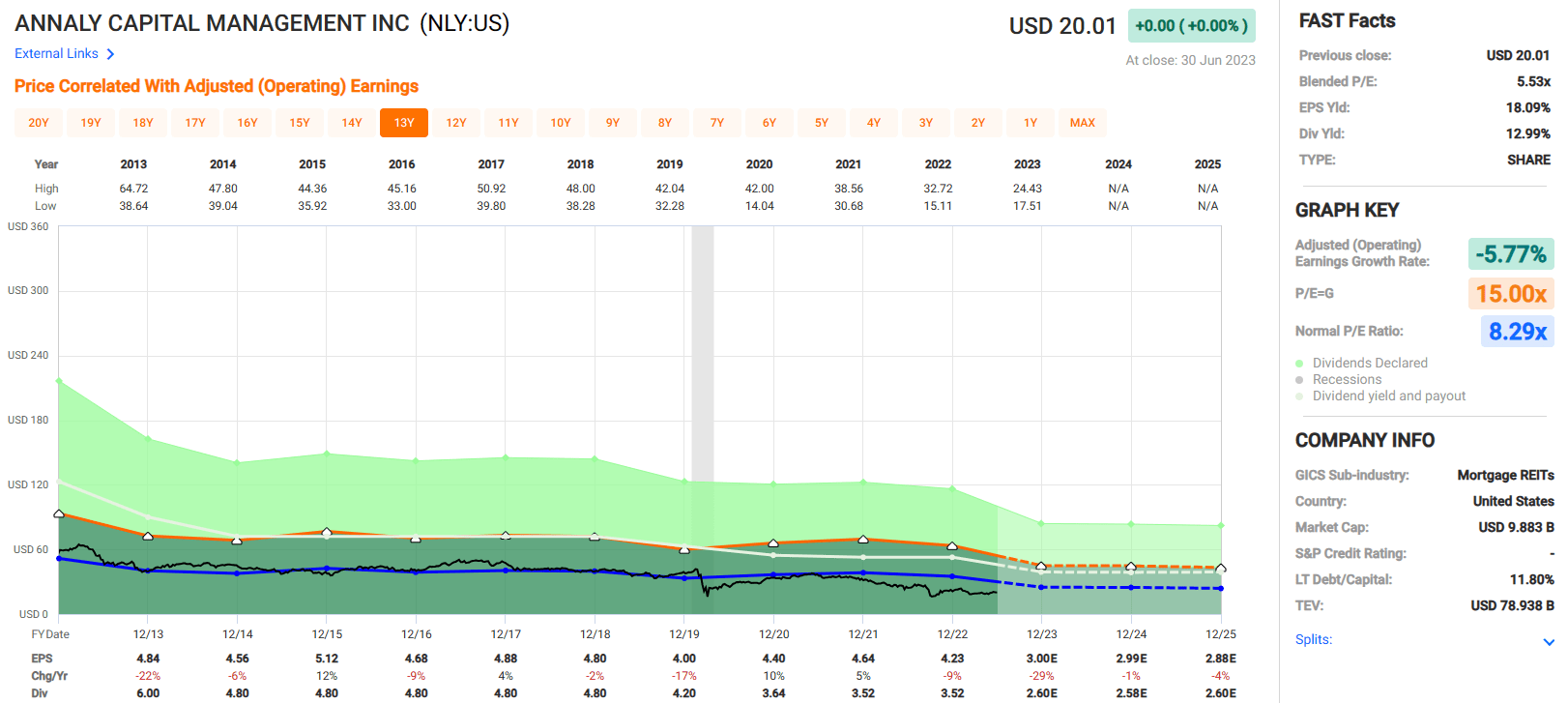

Over the past decade, NLY has done a terrible job of delivering positive returns to shareholders . In terms of its market valuation, the stock has lost 53.02% during the last five years. In July of 2018, NLY stock traded for approximately $42.00 per share but is now currently trading under $20.00 per share.

{kind=link}

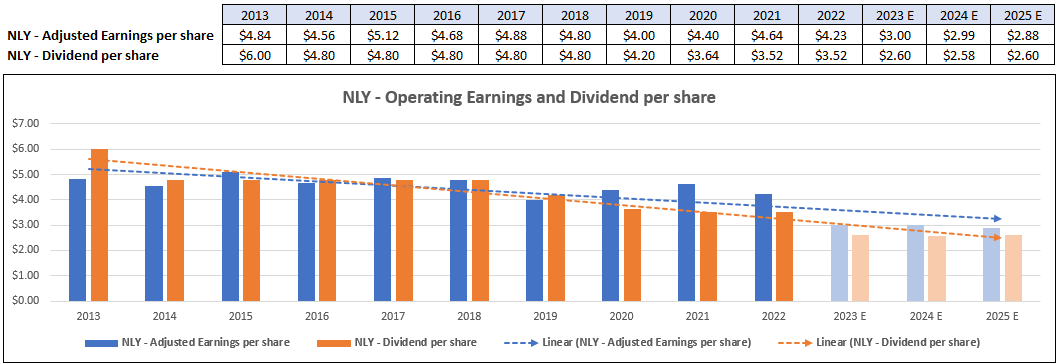

NLY’s stock price has followed the fundamental performance with adjusted operating earnings “growth” rate averaging negative -5.77% since 2013. Earnings declined by -9% in 2022 and analysts expect earnings to significantly decline by -29% in 2023. If analysts’ projections hold up, NLY’s earnings would fall from $4.84 per share in 2013 to $3.00 per share in 2023.

NLY’s dividend track record has been just as bad , with six dividend cuts over the past 10 years. They cut their dividend by 26.83% in 2013, 20% in 2014, 12.5% in 2019, 13.33% in 2020, and 3.30% in 2021. They maintained their dividend in 2022, but as of the first quarter in 2023 the quarterly dividend was cut from $0.88 per share to $0.65 per share for a cut of approximately 26%.

{kind=link}

NLY pays a 12.99% dividend yield, but we view this as a sucker yield . Although the dividend payout ratio was 83.22% as of the end of 2022, NLY has only been able to keep the payout ratio under 100% due to all the dividend cuts they have made over the years.

If analysts’ estimates are on target, the 2023 payout ratio would come to 86.67%, but this is assuming a 26% dividend cut with the dividend going from $3.52 in 2022, to $2.60 in 2023.

Currently NLY is trading at a P/E of 5.53x, which is a significant discount to their normal P/E of 8.29x but given the long-standing poor performance in both earnings and dividend growth I would avoid this residential mortgage REIT.

At iREIT© we rate NLY a SELL.

{kind=link}

Avoid this Cherry Bomb

Cherry Hill Mortgage ( CHMI ) is an externally-managed mREIT that invests in a variety of residential mortgage debt related products and services. CHMI operates through two investment segments including investments in residential mortgage-backed securities (“RMBS”) and investments in servicing related assets.

Through their RMBS segment, they acquire and own primarily Agency RMBS that are whole-pool, pass-through certificates, but also invest in private label non-agency RMBS and collateralized mortgage obligations (“CMOs”).

Through their service related segment, they invest in mortgage servicing rights (“MSRs”) and Excess MSRs. CHMI does not directly service the mortgage loans related to the acquired MSRs, but instead contracts the servicing functions to third party sub-servicers.

CHMI – IR (in millions)

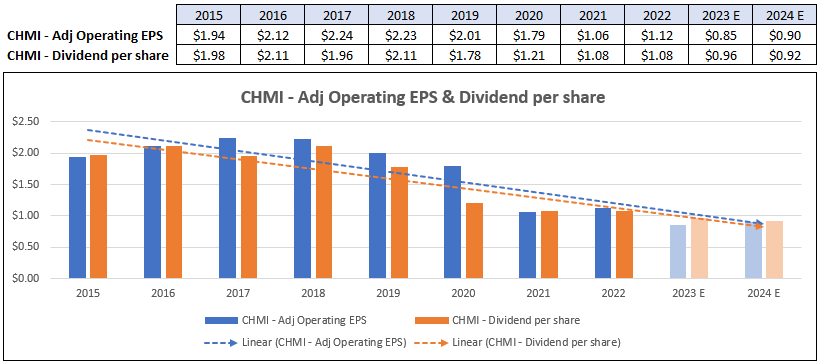

Cherry Hill Mortgage’s fundamental performance has been dismal since 2015 with an average annual earnings growth rate of negative -7.69% and an average annual dividend growth rate of negative -6.72% over that same time period.

CHMI’s adjusted operating earnings fell from $1.94 per share in 2015 to $1.12 per share in 2022. To add on to that, analysts expect earnings to fall by 24% in 2023 to $0.85 per share.

The dividend has followed suit with $1.98 per share paid in 2015 vs $1.08 per share paid in 2022. The dividend has been cut numerous times since 2015 with notable cuts of -15.64%, -32.02%, and -10.74% in the years 2019, 2020, and 2021 respectively.

{kind=link}

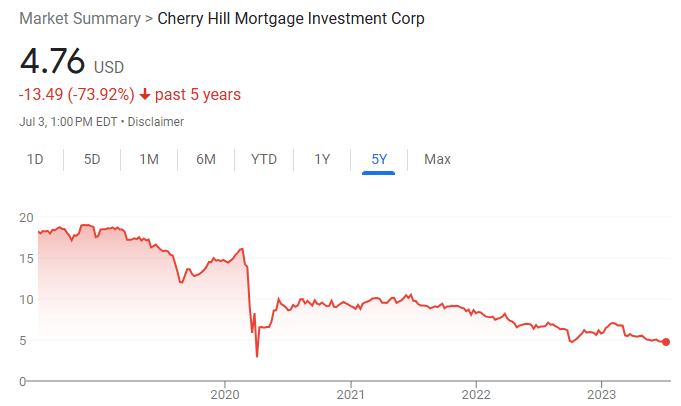

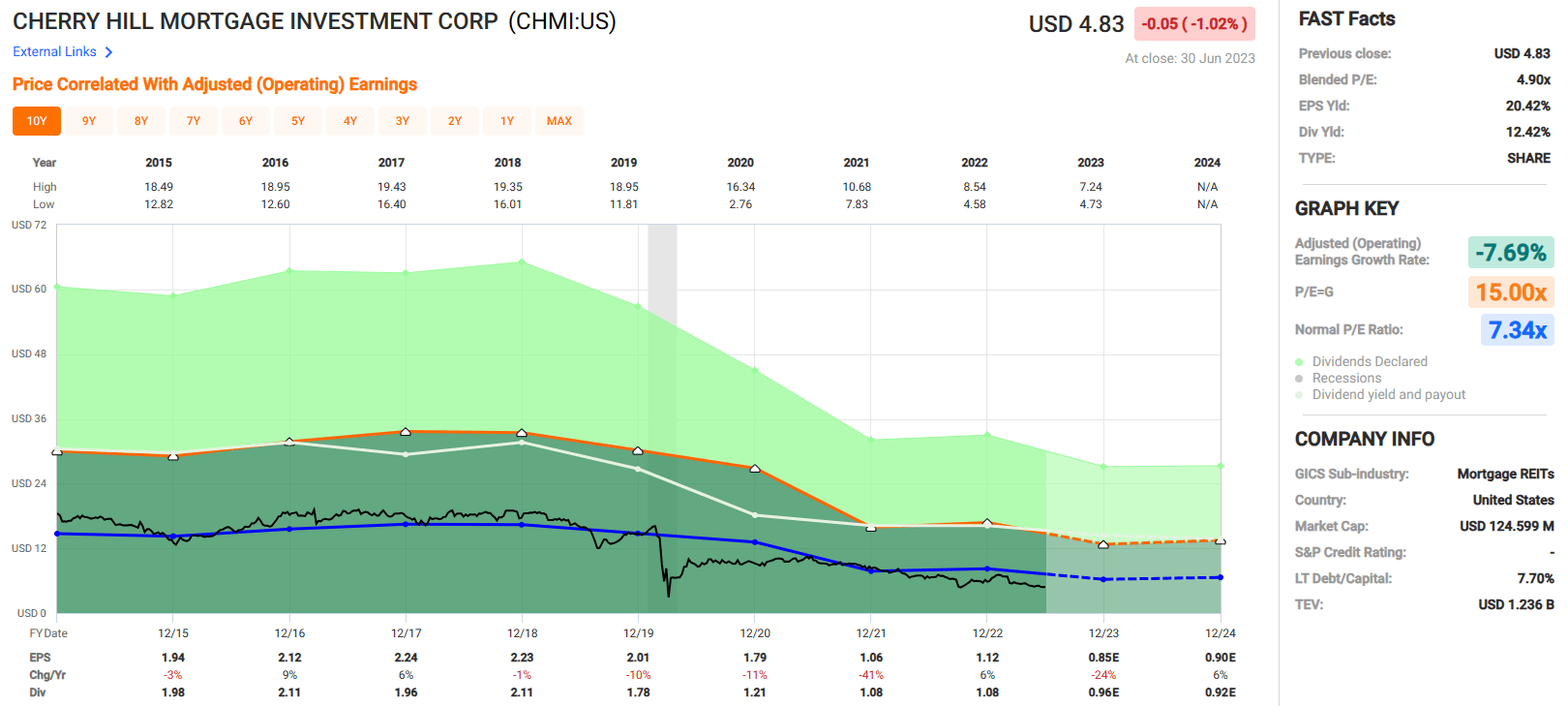

CHMI’s stock price has reflected the fundamental performance with the stock trading at approximately $18.00 per share in 2018 vs its current price of $4.76 per share for a 73.92% decline in market value.

{kind=link}

Cherry Hill Mortgage currently pays a 12.42% dividend yield but has a dividend payout ratio of 96.43%. Between the high payout ratio and the mREITs dividend history I see this as a sucker yield .

Earnings are expected to fall by 24% in 2023 to $0.85 per share which would put the dividend payout ratio at 127% if the current dividend is maintained .

The stock is trading at a 4.90x P/E ratio, which is well below their normal P/E of 7.34x, but given the fundamental performance over the company’s history I would avoid this stock.

At iREIT we’re avoiding this firecracker.

{kind=link}

Lessons Learned

I hope my mom is not reading this article, because I never told her that I blew up all of my fireworks. It was certainly a painful experience which is why I’m ending m y July 4 article with a “lessons learned”…

Had I anchored the Coke can with sand (or something heavy) I could have avoided this catastrophic explosion.

In other words, a solid foundation is critical.

That’s precisely why I’ve anchored my REIT portfolio with quality names like Realty Income ( O ), Agree Realty ( ADC ), W. P. Carey ( WPC ), American Tower ( AMT ), Mid-America ( MAA ), Camden Property ( CPT ), VICI Properties ( VICI ), and others.

On behalf of the iREIT on Alpha team, we wish you a terrif ic July 4 th an d I look forward to your comments below.

Be safe out their folks!

For further details see:

Avoid These REIT Fireworks At All Costs