AVRO - Avrobio: Net-Net Biotech Pursuing Strategic Alternatives

2023-08-12 04:03:14 ET

Summary

- After monetizing one of its pipeline candidates, Avrobio has cash well in excess of its market cap.

- The company announced its search for strategic alternatives recently. The process could close its valuation gap soon.

- There is potential for significantly more value if Avrobio can also monetize its remaining candidates.

Company Overview

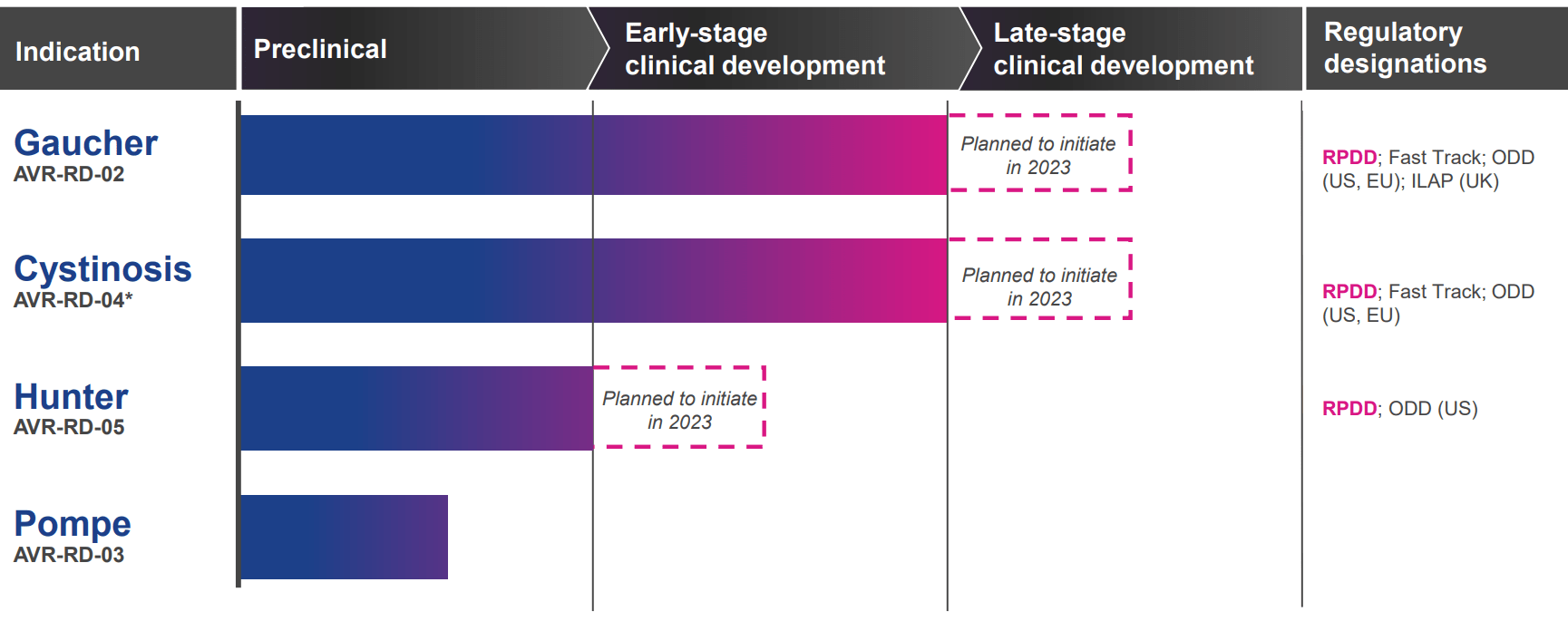

Avrobio ( AVRO ) is a pre-revenue gene therapy biotech firm with four indications in its pipeline. The candidates could treat Gaucher, Pompe, Hunter, and Cystinosis diseases. Each one has its own timeline, risks, and potential for profit.

{kind=link}

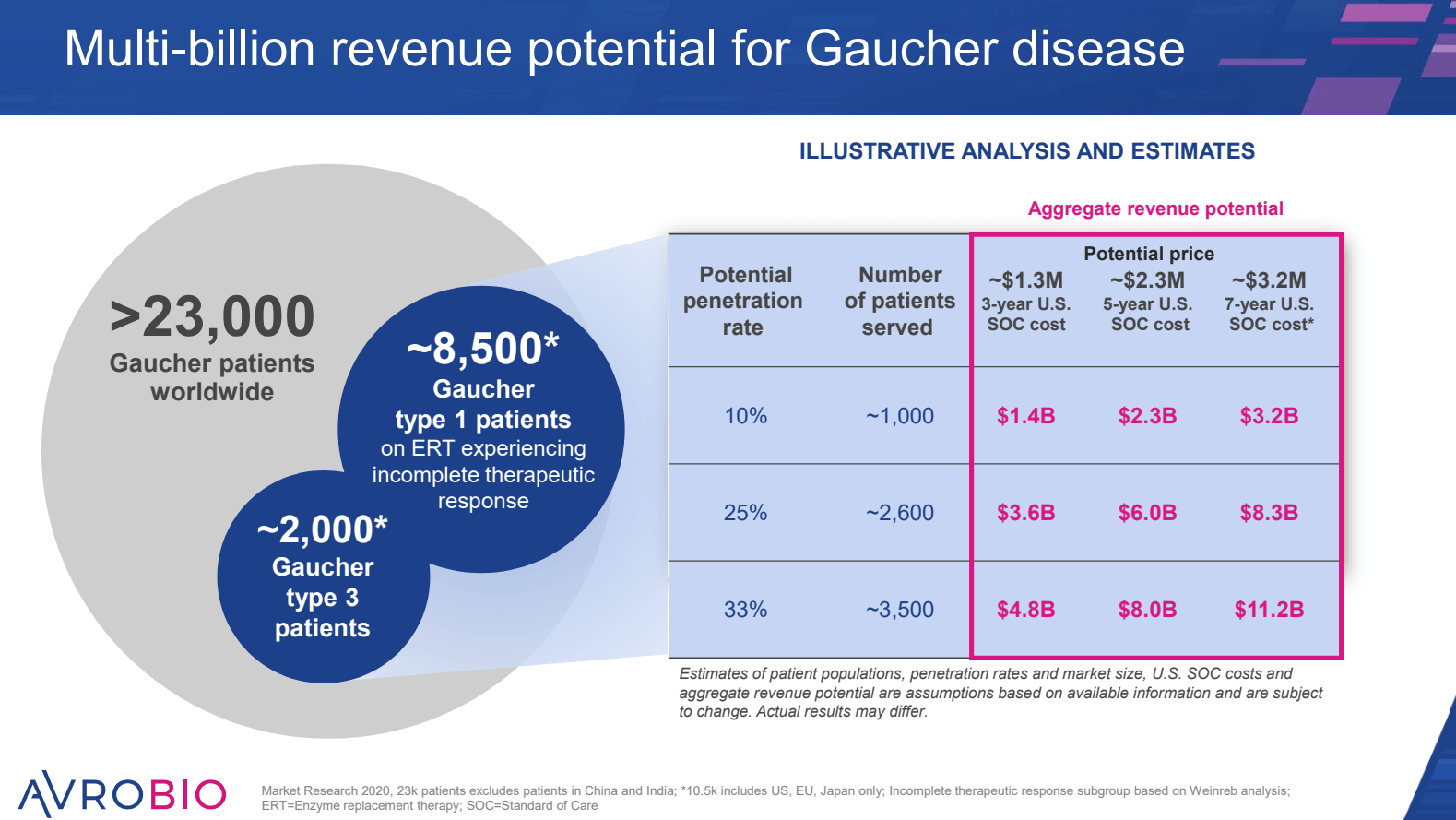

- Gaucher Disease – Planned initiation of Phase 2/3 in late 2023. Positive data from its first in-human evaluation. Avrobio estimates the therapy could be a multi-billion-dollar revenue niche breakthrough if approved.

- Hunter Syndrome – Initiated Phase ½ clinical trial in early 2023. Granted Rare Pediatric Disease and Orphan Drug Designation.

- Pomp Disease – Being evaluated in a pre-clinical research program.

- Cystinosis – See below.

Investment Thesis

In a surprise move, Avrobio sold its Cystinosis assets to Novartis for $84 million in June. The deal may have been struck based on interest from Novartis, Avrobio having difficulty obtaining capital to sustain development or a combination. Either way, the deal injected Avrobio with a significant amount of cash.

The company used the proceeds to pay off its loan from Silicon Valley Bank. The principal and outstanding interest was $16.4 million, leaving about $67.6 million in net proceeds. At that time, the company estimated that the fresh capital would sustain its operations through the fourth quarter of 2024.

In a subsequent decision by its board, Avrobio announced that the company would discontinue developing its remaining assets and explore strategic alternatives. The decision may have been made for similar reasons the company sold its Cystinosis candidate. Regardless, the remaining assets could result in further cash inflows to Avrobio.

Avrobio shares actually bounced higher upon the announcement of strategic alternatives and have seemingly settled to ~$1.50 per share ($66.6 million market cap) as of the timing of this writing. That’s a significant discount to the company’s $125 million in cash and no debt. Perhaps more importantly, the company’s cash burn will be dramatically reduced after the announcement, which gives management a runway to execute the strategic alternatives process while maintaining a compelling margin of safety.

Valuation

Avrobio’s June quarter balance sheet showed a book value of $122 million. After adjusting for non-cash items and accounting estimates, the quarter-end statement shows about $128 million in economic book value.

Company Filings and Cook Capital Management

After some layoffs at the beginning of the year, Avrobio burned about $20 million during the first quarter. That number mainly consisted of the salaries and wages paid to execs and R&D staff but also included development costs. It appears the company halted development costs (save for the Gaucher indication) and had some headcount reductions prior to the announcement of strategic alternatives during the second quarter.

Company Filings Company Filings

{kind=link}

{kind=link}

The cost-cutting reduced second-quarter cash burn to about $14 million. Due to the reduced spending, we’ll use that number as a proxy for the cash burn case in our projections. Because the strategic alternatives process was announced in mid-July, we can assume that July and August (due to severance) will be full months of cash burn, or about $4.9 million. That will leave the company with an estimated $118.4 million in cash at the end of August. From there on, Avrobio should only be burning through salary and wages for the remaining employees after a 50% headcount reduction, or about $2.2 million per month. To be conservative, this number includes continued investment in Gaucher at the same rate as the second quarter.

The chart below demonstrates Avrobio’s estimated cash balance for each period, including a one-time $15 million ($0.33 per share) professional fee to investment bankers and wind-down costs. The last row shows the potential upside from today’s ~$1.50 share price.

Cook Capital Management

The table shows that if management can conclude its strategic alternative process by the end of the year, shares could be worth about $2.11 or a 40% upside. Alternatively, the process could drag on until the end of 2024 before shareholder’s margin of safety vanishes.

This valuation has not considered additional cost-cutting or any value that CEO Erik Ostrowski and his team could extract from the remaining drug candidates. Also, Avrobio is in an advantageous environment to realize value quicker than you might expect.

Catalysts

Funding for biotech and other startups has dried up over the last year or two . Venture Capital wants to conserve cash for its current investments, and the general investment community has soured on startups, leaving the IPO market largely unavailable. A lack of funding and an IPO market has left biotech companies scrambling for cash.

Interestingly, however, life science increased over the same time. Why? Possibly because private biotech companies are now looking at non-traditional sources of capital. For instance, a private biotech company could obtain Avrobio’s cash through a reverse merger. Additionally, Avrobio’s remaining assets could be a viable source of pipeline candidates for big pharma.

The situation leaves companies like Avrobio in an interesting position. Avrobio’s cash will likely draw interest from biotechs strapped for cash and a listing. Avrobio’s financial advisors will be working diligently to get a deal done and earn their fee, and big pharma companies may find Avrobio’s remaining candidates attractive. Given its advanced clinical trials and multi-billion-dollar revenue potential, Avrobio’s Gaucher candidate may be particularly interesting.

{kind=link}

Private biotechs, investment bankers, buyers, and sellers have become hip to the game over the last few years. Our current state of affairs gives me some confidence that a deal could be completed in a reasonable amount of time.

Risks

- Avrobio could burn cash faster than expected. My projections are based only on second-quarter expenses. That proxy could turn out to be inaccurate. The company has been trimming costs for a few quarters. Cost-cutting may have extended into the third quarter. My projections considered no additional cost-cutting. So, I have some confidence that the estimates are on the conservative side.

- Delayed strategic alternative process. The sooner Avrobio concludes its strategic alternatives process, the higher the expected return for shareholders. Ostrowski and CFO Azadeh Golipour were awarded significant retention bonuses in June, which will be paid out at the end of 2023. Their bonuses, stock options, and RSUs will accelerate based on a change in control. I’m not convinced this is a motivating factor to get a deal done quickly because the bulk of their comp will come at the end of the year, regardless of the process. Their comp packages could change in the near future based on the company’s change in strategy. For instance, Ostrowski and Golipour were bonused $150,000 and $100,000, respectively, in connection with the sale of Avrobio’s cystinosis candidate. Another bonus based on a successful strategic alternative process could follow. It’s also important to note that Ostrowski has a decade of experience as an investment banker, which should make the process run smoother than it otherwise would.

Actionable Conclusion

You’ve got a situation that looks hideous on the outside. But when you dig into the balance sheet, there is significant value on a per-share basis compared to the stock price. That provides today’s shareholders with a healthy margin of safety. Yes, that margin will dwindle over time, but the company has a cash runway for over a year before it is entirely eroded.

In a base case, investors will have cash returned in a wind-down and potentially Contingency Value Rights (CVRs) for the remaining candidates. Shareholders could also have their shares invested pro rata in a reverse merger with another company.

The bull case here is that Avrobio can monetize its Gaucher and the other two remaining candidates. In this case, the company could multiply its cash position and retain the potential upside of a reverse merger. In another bull scenario, management completes a deal for the entire company, including value for cash and its pipeline assets.

The bear case here is that the strategic alternatives process extends past our projected cash balance timeline. I think this is an unlikely scenario considering today’s biotech environment. Plus, by the end of next year, Avrobio could return cash to shareholders approximately equal to today’s share price.

I think it is likely that a deal will be done before the end of the year. At that time, investors should be rewarded with a return on their investment. That, of course, comes with the potential for additional return if any of Avrobio’s three remaining assets can be monetized.

For further details see:

Avrobio: Net-Net Biotech Pursuing Strategic Alternatives