AWF - AWF: Continued Asset Declines Could Force A Distribution Cut

2023-03-06 18:38:04 ET

Summary

- Investors and many others are in desperate need of extra income to defray the rapidly rising cost of living in the United States and around the world.

- AllianceBernstein Global High Income Fund invests in a portfolio of American and foreign bonds to generate a high income for investors.

- The portfolio includes a lot of high-yield bonds but should still be relatively insulated against any risk, except for interest rate risk.

- The AWF closed-end fund is failing to cover its distributions and has seen its assets decline over the past eighteen months. This may force a distribution cut at some point.

- The AllianceBernstein Global High Income Fund valuation is reasonable at the current price.

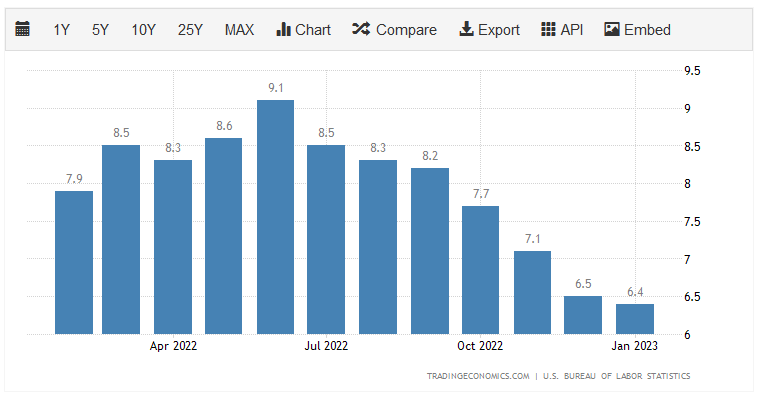

One of the biggest problems that have been plaguing the United States over the past year is the incredibly high inflation rate that has been making it ever more expensive to cover our daily expenses. Indeed, there has not been a single month over the past year in which the consumer price index increased by less than 6.4% year-over-year:

{kind=link}

This has naturally forced a great many people across the country to take on second jobs or perform other tasks in order to obtain the extra money that they need to feed themselves and pay their bills in these conditions. This may, in fact, be one reason why the job numbers continue to come in strong despite the fact that we are seeing large layoffs at many companies.

As investors, we have a better way to earn the extra income that we need to cover the increased cost of living than going out and working extra hours. We can put our money to work for us. One of the best ways to do this is by purchasing a closed-end fund ("CEF") that specializes in the generation of income. These funds are somewhat underfollowed by many investors, but they offer many advantages for income-focused investors. These funds provide easy access to a diversified portfolio of assets that can be purchased with one easy trade. In addition, they can usually boast a higher yield than pretty much anything else in the market.

In this article, we will discuss the AllianceBernstein Global High Income Fund ( AWF ), which is one CEF that investors can use for the purpose of generating extra income. It is reasonably successful at this, as its 7.88% current yield is higher than most things on the market today and it is certainly capable of turning anyone’s head. I have discussed this fund before, but several months have passed since that time, so naturally a few things have changed. In particular, the fund released a new earnings report , which will give us a better idea of how well it handled the turbulence in the market that characterized 2022. This is something that will likely be important for any risk-averse investors.

About The Fund

According to the fund’s webpage , the AllianceBernstein Global High Income Fund has the stated objective of providing its investors with a high level of current income. This is not particularly surprising that this is a fixed-income fund. That should be especially apparent when we consider how heavily weighted the fund is to fixed-income securities:

CEF Connect

There may be some readers that point out that the fund is more than 100% allocated to bonds. This is possible because the fund uses leverage, which we will discuss later in this article. The most important thing for our purposes here is that the fund is a fixed-income fund. This is in line with the investment approach that the fund details on its webpage:

{kind=link}

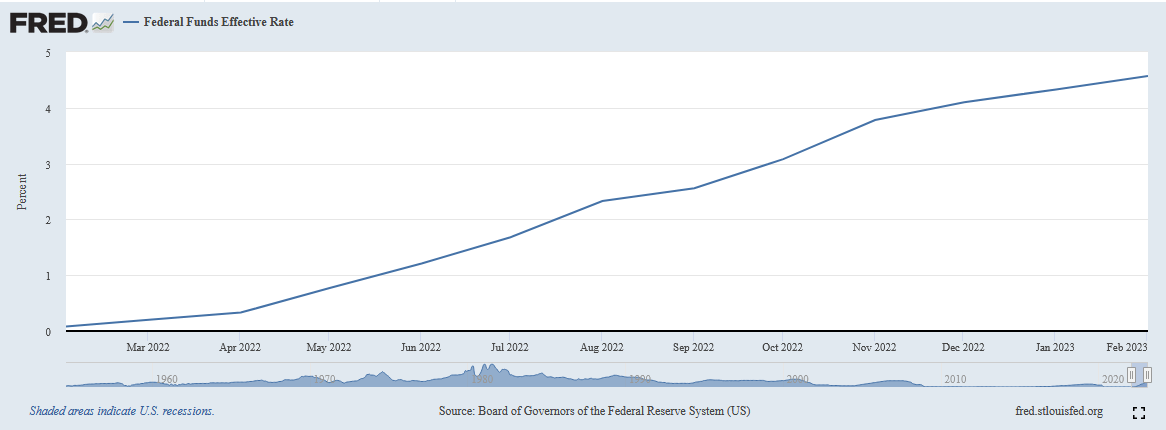

This is important because bonds and other fixed-income securities are incredibly sensitive to interest rates. This is because bonds are loans that investors make to a company. As is usual with debt, the company repays the loan plus interest under the terms specified in the bond agreement. The interest rate on the securities corresponds to the market interest rate at the time of issuance. As everyone reading this is no doubt well aware, the Federal Reserve has been actively raising interest rates over the past year. We can see this by looking at the federal funds rate, which is the rate at which commercial banks lend to each other in the overnight market. In February 2022, the effective federal funds rate was 0.08% but it is at 4.57% today:

Federal Reserve Bank of St. Louis

{kind=link}

This is important because bond prices are inversely correlated to interest rates. In short, when interest rates go up, bond prices go down, and vice versa. This is because newly issued bonds will have a yield that corresponds to the market interest rate at that time. If this yield is higher than what existing bonds are paying, the price of the existing bonds must decline so they offer a similar yield-to-maturity as the brand-new bond.

If this were not the case, it would not be possible to sell existing bonds during rising-rate environments because everyone will only want to buy brand-new bonds. This is relevant for this fund because the bonds that the fund is holding have been falling in price over the past year. Over the past twelve months, the AllianceBernstein Global High Income Fund is down 7.81%:

{kind=link}

This is actually quite a bit better than the 11.32% loss that the Bloomberg U.S. Aggregate Bond Index ( AGG ) has delivered over the same period, but the two assets are not perfectly comparable. As the name of the fund implies, the AllianceBernstein Global High Income Fund invests in bonds issued both domestically and abroad. In fact, only 68.21% of the fund is invested in American bonds:

{kind=link}

The fund states on its webpage that it invests in developing markets, but the only two on this list that could possibly be considered emerging markets are Brazil and Mexico. Then again, the fund sponsor does not specifically state what countries’ bonds are included in that 15.28% allocation to “other.” There could be some emerging markets in that group. The fund’s semi-annual report makes mention of Angola, Argentina, Chile, the Czech Republic, Ecuador, the Dominican Republic, and a number of others.

However, that report is dated September 30, 2022, so it is several months out of date compared to the chart above. As such, we do not know which of those nations still has corporate bonds represented in the fund. It seems likely, though, that no nation accounts for 1.0% of the fund’s portfolio except for the ones above.

One of the reasons why the presence of emerging markets could be important is that many of these nations have far lower debt levels than the developed world. For example, Mexico’s debt-to-GDP ratio is 41.1% and the Czech Republic’s is 36.2%. With that said, the fund does not invest only in sovereign bonds, as it contains a number of corporate bonds. However, many companies tend to operate with lower debt levels in countries with low sovereign debt.

As a general rule, economies with low debt tend to grow more rapidly than those with high debt levels. In addition, those nations with a low debt-to-GDP ratio theoretically have more room to increase their taxes to pay off the debt if need be. Thus, the fact that these countries are represented in the fund could reduce its risk somewhat. In addition, many emerging markets have higher interest rates than developed nations, which should result in higher income for the fund.

One characteristic that we frequently see among closed-end funds is a high exposure to speculative-grade securities. This fund is no exception to this, which we can clearly see by looking at the credit ratings of the securities in the portfolio. Here they are:

{kind=link}

An investment-grade bond is anything rated BBB or higher. As we can see above, that only accounts for 22.02% of the portfolio. The remainder of the fund is invested in what is colloquially called “junk bonds.” This is something that may be concerning to risk-averse investors considering that these securities are frequently considered to be at high risk of default. While it is true that these bonds are more likely to default than investment-grade securities, we still see that 66.58% of the portfolio is invested in securities that are rated either BB or B.

These are the two highest ratings possible for junk bonds and according to the official bond ratings scale , entities whose securities have been assigned one of these ratings have the sufficient financial strength to cover their current debts even in the event of a short-term economic shock. Thus, we should be reasonably confident that there will probably not be huge losses due to default on these securities. As these plus the investment-grade securities account for well over 80% of the portfolio, there should be a reasonable degree of confidence that we should be fairly protected from large losses due to defaults.

Another way that the fund protects us against any default-related losses is by holding a large number of securities in its portfolio. As of the time of writing, the fund has 1,811 unique positions. This should ensure that the proportion of the portfolio occupied by any individual issuer is quite small and thus even if an individual issuer defaults, it should have a negligible impact on the fund as a whole. Thus, the fund’s high weighting toward speculative-grade securities does not appear to be anything to worry about.

Leverage

In the introduction to this article, I stated that closed-end funds like the AllianceBernstein Global High Income Fund have the ability to deliver higher yields than the underlying assets actually possess. One way that this is accomplished is through the use of leverage. In short, the fund borrows money and then uses those borrowed funds to purchase fixed-income securities. As long as the purchased securities have a higher yield than the interest rate that the fund must pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. This fund is able to borrow money at institutional rates, which are considerably lower than retail rates. As such, this will usually be the case.

However, the use of debt is a double-edged sword because leverage increases both gains and losses. As such, we want to ensure that the fund is not employing too much leverage since that would expose us to too much risk. I generally do not like to see a fund’s leverage exceed a third as a percentage of assets since that would expose us to too much risk. Perhaps surprisingly, the AllianceBernstein Global High Income Fund only has levered assets comprising 3.09% of its assets as of the time of writing. Thus, it easily satisfies this requirement. In fact, the fund could probably take on more debt in order to boost its yield higher than it currently is. Overall, though, there is little need to worry with regard to the fund’s leverage.

Distribution Analysis

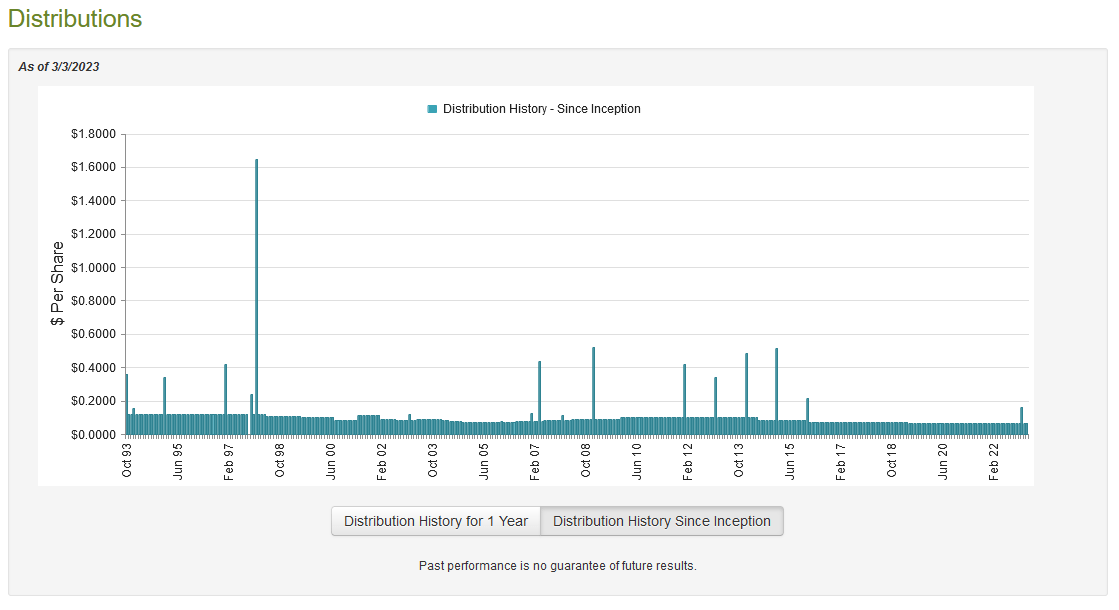

As stated earlier in this article, the primary objective of the AllianceBernstein Global High Income Fund is to provide its investors with a high level of current income. In pursuit of this goal, it invests primarily in junk bonds and other high-yielding fixed-income assets and then applies leverage to effectively boost their yield. As such, we might expect that the fund would boast a fairly high yield itself. This is indeed the case as the fund currently pays out a monthly distribution of $0.0655 per share ($0.7860 per share annually), which gives it a 7.88% yield at the current price. The fund has been pretty consistent about this distribution over the past few years, but its long-term history is much more volatile:

{kind=link}

The fact that the fund’s distribution has varied quite a bit over its lifetime may serve as something of a turn-off for those investors that are seeking a secure and consistent source of income with which to pay their bills and finance their lifestyles. However, the fund has been quite consistent since 2019, which is more than most fixed-income funds can claim. An investor purchasing today does not necessarily have to be concerned about the fund’s past, though. This is because these investors will receive the current distribution at the current yield. As such, the most important thing for them is determining the fund’s ability to maintain its current distribution.

Fortunately, we have a somewhat recent document that we can consult for this purpose. The fund’s most recent financial report (linked earlier) corresponds to the six-month period that ended on September 30, 2022. This is a much newer report than we had available the last time that we looked at the fund. As such, it should give us a pretty good idea of how well the fund handled the first few rounds of interest rate hikes, which can be expected to have had a significant impact on it due to the correlation between bonds and interest rates.

During the six-month period, the AllianceBernstein Global High Income Fund received a total of $32,694,853 in interest and $863,339 in dividends from the investments in its portfolio. This gives it a total income of $33,558,192 during the period. It paid its expenses out of this amount, leaving it with $28,575,139 available for investors. This was unfortunately not enough to cover the $33,888,263 that the fund actually paid out in distributions during the period. This is likely to be concerning at first glance as the fund failed to earn sufficient money to sustain its payout.

However, there are other ways that the fund can obtain the money that it needs to cover the distribution. The most common of these methods is earning capital gains. Unfortunately, the fund failed miserably at this task during the six-month period, which is likely to be expected considering the turbulence in the bond markets that ensued when the central bank started monetary tightening. The fund reported realized net capital losses of $20,720,899 and posted another $138,437,967 net unrealized capital losses during the period.

Overall, the fund’s assets declined by $164,471,990 over the six-month period after we account for all inflows and outflows. This is quite concerning, especially because the fund’s assets also declined during the full-year period that ended on March 30, 2022. This was discussed in my previous article on the fund. Investors should be quite concerned as this fund appears to be bleeding capital and it may be unable to maintain its distribution unless the market turns around quickly. As it is likely that we will see more interest rate increases over the next several months, it appears unlikely that a market turnaround will be forthcoming. Investors may want to be cautious.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the AllianceBernstein Global High Income Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to buy shares of a fund when we can purchase them at a price that is less than the net asset value. This is because such a scenario implies that we are acquiring the fund’s assets for less than they are actually worth. That is fortunately the case with this fund today. As of March 3, 2023 (the most recent date for which data is currently available), the AllianceBernstein Global High Income Fund has a net asset value of $10.60 per share but the shares trade for $9.88 per share. That gives the fund’s shares a discount of 6.79% to the net asset value at the current price. This is quite a bit better than the 4.79% discount that the shares have had on average over the past month. Thus, the current price appears to be reasonable.

Conclusion

In conclusion, there appears to be quite a bit to like about the AllianceBernstein Global High Income Fund. The fund has a fairly strong portfolio of domestic and foreign fixed-income assets that have allowed it to beat the U.S. bond index over the past twelve months. However, AllianceBernstein Global High Income Fund has been seeing its assets under management decline over the past eighteen months, which could be a strong sign that it will need to cut the distribution in the near future. The fund is trading at a reasonable valuation, but the risk here of a distribution cut may mean that it is best to stay away until things improve for AllianceBernstein Global High Income Fund.

For further details see:

AWF: Continued Asset Declines Could Force A Distribution Cut