REET - AWP: Decent Thesis But This CEF Looks Risky

2023-04-04 14:31:10 ET

Summary

- Real estate should increase in value with inflation, resulting in it being a way to protect your wealth against loss of purchasing power.

- abrdn Global Premier Property invests in a portfolio of real estate investment trusts and similar companies from around the world.

- Real estate did not perform very well in 2022 for a few reasons, none of which change the overall thesis of inflation protection.

- The AWP closed-end fund appears to be overdistributing and may have to cut its payout in the near future.

- The fund does have a reasonable valuation, but it is not discounted enough given the risks of a distribution cut.

Without a doubt, one of the biggest problems facing Americans today is the incredibly high level of inflation permeating the economy. Over the past year, there has not been a single month in which the consumer price index was less than 6% higher than in the equivalent month of the prior year:

{kind=link}

This has had a devastating effect on the finances of many American families. In a recent blog post , I discussed how many people have been forced to resort to spending down their savings or running up their credit cards just to maintain their standard of living in the face of such high inflation. However, investors have another problem in that we want to preserve the purchasing power of our wealth. Ideally, we want to both maintain the value of the money that we spent most of our lives earning and even grow it. This is a task that has become much more difficult over the past year as high inflation combined with a falling stock market has had a significant negative impact.

Fortunately, there are still a few ways to achieve both wealth preservation and earn a return. One way through which this can be accomplished is by purchasing shares of a closed-end fund, or CEF, that specializes in real estate. This may seem an odd choice considering that most real estate investment trusts performed especially poorly over the past year, but real estate does possess many of the qualities that other real assets that increase in value due to inflation do. In addition, real estate can be rented out to tenants in order to earn a profit.

In this article, we will discuss the abrdn Global Premier Property Fund ( AWP ), which is one closed-end fund that investors can use in order to gain exposure to real estate, as well as obtain some international exposure. This fund boasts an impressive 11.71% yield at the current price, which is certainly an acceptable yield. However, any fund whose yield enters the double digits is generally the subject of fears that it could be cut, so we will need to place special emphasis on the finances of this fund in our analysis. Fortunately, the price of this fund is fairly reasonable so even if it does cut the distribution somewhat, it could still be a good deal. Let us investigate and see if this fund could be a good addition to our portfolios today.

About The Fund

According to the fund’s webpage, the abrdn Global Premier Property fund has the stated objective of providing capital appreciation and current income to its investors. This is hardly surprising considering that this is an equity fund that invests in real estate securities. This is evident in the fact that 99.24% of the fund is currently invested in common stock:

CEF Connect

As I discussed in a recent article , common stock has much greater potential for capital appreciation than fixed-income securities such as preferred stock or bonds due to the fact that common equity has a direct link to the growth and prosperity of the issuing company. In this case, the common equity should increase as the value of the real estate owned by the issuing company goes up. That is something that will typically occur during inflationary times for reasons that will be discussed later in this article. In addition, we can assume that the rents paid by the tenants of the properties that are owned by a given real estate company should also increase with inflation, which has certainly happened over the past year or two. This should drive up the profits of the companies issuing the common equity, which likewise ultimately leads to rising common stock prices.

With that said, there will undoubtedly be many readers that point out that real estate investment trusts have certainly not seen their stock prices appreciate over the past year. In fact, the iShares Global REIT ETF ( REET ) is down 22.06% over the past twelve months:

{kind=link}

There are a few reasons for that. One of them is that the rising interest rate environment has made the dividend yields paid by most real estate investment trusts much less appealing. After all, right now the Global REIT Index is yielding 2.49%, which is not at all attractive when an investor can simply put the cash into a money market fund and get 4.50%. The raising interest rate environment has greatly reduced the reward for taking on the extra risk of putting your money into real estate, which has reduced the demand for shares of real estate investment trusts.

The second drag on real estate performance has been that the rising interest rate environment over the past year has made mortgages significantly more expensive. As such, a potential buyer with a limited budget cannot spend nearly as much on a real estate purchase as they could two years ago. That has had virtually no impact on a cash buyer and is more representative of the bubble bursting and real estate returning to its intrinsic value than it is an actual real decline in real estate values. This is especially true in the housing market since many home sellers cannot actually reduce their selling price because they need to get a certain amount to pay off their own mortgages. Thus, it is questionable how much the decline in real estate investment trusts is really something that we need to worry about.

There is one final factor that has proven to be a drag on real estate performance. This is because virtual work grew significantly in popularity during the pandemic-related lockdowns. Despite the fact that the concerns about spreading the disease and demands for social distancing have largely subsided, many companies and employees are still opting to work remotely due to the flexibility that it provides. This has caused a rise in commercial office vacancies, as seen here:

{kind=link}

This has caused rents for commercial office space to decline, which is a sharp contrast to the increased rents that we see in the residential market. According to Commercial Edge , the average rent for commercial office space nationwide stood at $38.28 per square foot in February 2023, which represents a 1.6% decline year-over-year. This has put some pressure on the cash flow of those companies that own office buildings, which is particularly concerning considering that they need the money from rents to cover their own expenses, such as property taxes and payments on the mortgage. It is somewhat understandable that their share prices would decline given these fundamentals.

In short, most of the factors that have led to weakness in the share prices of real estate companies over the past year have been due to the fundamentals of the companies and property owners and are not due to characteristics of the real estate itself. In the end, it makes little difference, though.

As the name of the fund implies, the abrdn Global Premier Property Fund purchases equity securities from real estate companies located all over the world. Unsurprisingly, though, the majority of the fund is invested in American companies:

CEF Connect

This is something that is typical of most global funds. Although the United States only represents a little less than 25% of global gross domestic product and economic production, it usually has a 60% to 70% weighting in most global funds. Thus, the funds are substantially overweight to this country based on its actual representation in the global economy. It is not really surprising in the case of this fund though, since the United States does have more publicly-traded real estate companies than any other country. We do still see an acceptable weighting to several other countries in this fund, though. Perhaps the most notable of these is Japan, which is a nation that is not often seen in global real estate funds. Overall, this fund appears to be doing an acceptable job of diversifying its assets internationally. That is something that is nice to see because of the protection that it provides us against regime risk. Regime risk is the risk that some government or other authority will take an action that has an adverse impact on a company in which we are invested. The only real way to protect ourselves against that risk is to ensure that only a relatively small proportion of our assets are invested in any given country, so this fund provides one way to achieve that.

For the most part, the largest positions in this fund will be familiar to most readers that follow the real estate industry. Here they are:

CEF Connect

For a global fund, there are a surprising number of American companies making up the largest positions. In fact, the only company on this list that is not an American firm is Sun Hung Kai Properties ( SUHJY ), which is based on Hong Kong. This is similar to other global real estate funds like the CBRE Global Real Estate Income Fund ( IGR ), which also only has one foreign position on its largest holdings list. This alone is not really that bad though, since it is the weighting to the country’s securities that defines the overall foreign exposure, not simply the presence of foreign companies among the largest positions.

We do see that the abrdn Global Premier Property Fund has some different positions than many other real estate closed-end funds. In particular, we do not see mainstays such as American Tower ( AMT ) or Crown Castle International ( CCI ) in this fund. We do see a great deal of diversification though as we have industrial, healthcare, data center, residential, and most other types of real estate represented in the largest positions. This is nice to see as the fundamentals of these properties are all very different. For example, the trend towards remote work has had a much bigger impact on office building owners than it did on residential properties or data centers. The fact that the fund is providing exposure to all these different types of properties is very nice from a diversification perspective.

As my long-time readers on the topic of closed-end funds are no doubt well aware, I do not generally like to see any individual position in a fund account for more than 5% of the fund’s total assets. This is because that is approximately the level at which a position begins to expose the fund to idiosyncratic risk. Idiosyncratic, or company-specific, risk is that risk that any asset possesses that is independent of the market as a whole. This is the risk that we aim to eliminate through diversification, but if the asset accounts for too much of the portfolio, then this risk will not be completely eliminated. Thus, the concern is that some event may occur that causes the price of a given asset to decline when the market as a whole does not, and if that asset accounts for too much of the portfolio, then it may end up dragging the entire fund down with it. As we can clearly see here, there is one asset, Prologis ( PLD ), that substantially exceeds that 5% weighting restriction. As such, potential investors will want to ensure that they are willing to be exposed to the risks of that asset individually before buying shares of the fund.

Real Estate As Inflation Protection

In the introduction to this article, I stated that real estate can help an investor protect their wealth against the ravages of inflation. Indeed, this forms a major part of our thesis for including real estate in a portfolio. As such, it is important to discuss why this would be the case.

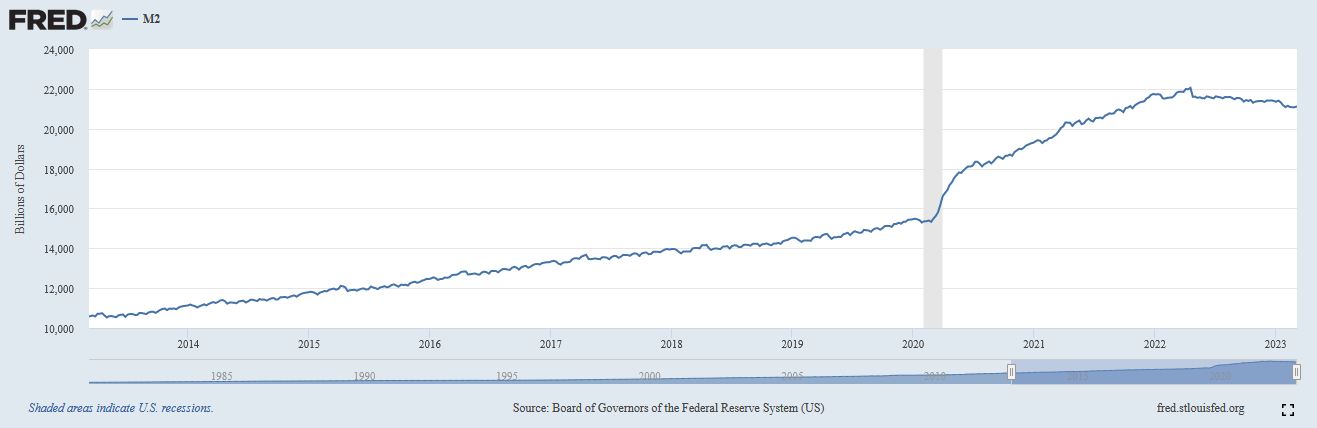

Let us begin by discussing the cause of the inflation that is so prevalent in the American economy today. Economists generally state that inflation is a natural phenomenon that is always present in an economy. That is not correct, as inflation is caused by the money supply growing more rapidly than the productive capacity of the economy. This has been the case in the United States for more than a decade. We can see this by comparing the M2 money supply, which is a measurement of the actual liquid supply of money in an economy, to the gross domestic product.

This chart shows the M2 money supply of the United States over the past ten years:

{kind=link}

As we can see, the M2 money supply went from $10.5993 trillion on March 11, 2013, to $21.1233 trillion on March 6, 2023 (the most recent date for which data is available). This is a 199.29% increase over the ten-year period. In other words, the nation’s money supply almost doubled over the period. It should be fairly obvious that the nation’s economic production did not double over the same period. Here is the gross domestic product over the same period:

{kind=link}

As we can see, the nation’s gross domestic product went from $16.420386 trillion to $26.137992 trillion over the period. That is only a 59.18% increase over the period. Thus, the nation’s money supply grew much faster than the actual production of goods and services in the economy. This is the root cause of the inflation that we are seeing today. After all, there are now more units of currency available to purchase each unit of economic output. The law of supply and demand states that prices will increase to achieve equilibrium in such a situation.

At this point, there may be some people that point out that we did not see inflation over the 2009 to 2019 period despite the fact that the money supply was growing faster than the economy. We actually did, but it showed up in the price of other things. This is why the stock market delivered such strong returns and the reason why housing prices went up over the decade. In 2020 and 2021, the government aimed to deliver the newly printed money into the hands of people that would spend it, which they did, creating inflation that actually shows up in the consumer price index.

Real estate helps to protect owners against the inevitable loss of purchasing power than accompanies inflation. This is because real estate shares many of the qualities possessed by those things that increase in price during inflationary times. For example, real estate is in limited supply, and it can only be created or improved through actual human or mechanical effort. One cannot simply press a button on a computer and cause an entire neighborhood to appear on an island in the middle of the Atlantic Ocean, after all. Fiat currency most certainly can be created out of thin air with just the push of a button. As such, real estate should be able to hold its value as the supply of money increases, which is the case during inflationary periods.

Distribution Analysis

As stated earlier in this article, the primary objective of the abrdn Global Premier Property Fund is to provide its investors with a high level of capital appreciation and current income. In order to accomplish this objective, it invests in a portfolio of securities issued by real estate investment trusts and similar assets. Admittedly, the yields of most real estate investment trusts are nowhere near as impressive as they once were, but they still beat the 1.57% yield of the S&P 500 Index ( SPY ). However, the fund also pays out any capital gains that it manages to achieve, which boosts its yield beyond that of the yields of the companies that actually comprise the portfolio. As such, the abrdn Global Premier Property Fund has a respectable yield. Currently, the fund pays a monthly distribution of $0.04 per share ($0.48 per share annually), which gives it an 11.71% yield at the current price. The fund has been somewhat consistent about its payout over its history, but there have been a few variations:

{kind=link}

This history is admittedly not as good as that of the CBRE Global Real Estate Income Fund, as that fund increased its distribution over the past decade. The abrdn Global Premier Property decreased its distribution with the cutback in 2019. However, this fund did manage to avoid a cut following the events of 2022, which is admirable. Overall, its track record is reasonable and may be appealing to those investors that are looking for a safe and secure source of income to pay their bills or otherwise finance their lifestyles. This is especially true when we consider that anyone purchasing today will receive the current distribution and current yield and will not be directly impacted by a distribution cut that occurred three years ago. As such, the most important thing for any investor today is the fund’s ability to sustain or grow its distribution going forward.

Unfortunately, we do not have an especially current document that we can consult for our analysis. The fund’s most recent financial report corresponds to the full-year period that ended on October 31, 2022. As such, it will not include information regarding the fund’s performance over the past five months. However, the worst aspects of the market for real estate securities occurred in the first few months of 2022 when the Federal Reserve began raising interest rates. The impact of this event will be reflected in this report, so we will be able to get a good idea of how the fund handled this event. During the full-year period, the abrdn Global Premier Property Fund received $18,289,489 in dividends and curiously nothing in interest. Thus, the dividend income accounts for the whole of the fund’s investment income. It paid its expenses out of that amount, which left it with $10,218,633 available for shareholders. As might be expected, that was nowhere close to enough to cover the $40,995,817 that the fund paid out in distributions over the period. At first glance, this will likely be very concerning as the fund failed to cover its distributions out of net investment income.

However, the fund does have other methods that can be employed in order to obtain the money that it needs to cover the distribution. For example, it might have had capital gains. As is likely expected from the poor performance of most real estate securities during 2022 though, the fund failed miserably here. It reported net realized losses of $17,773,918 and had another $173,996,407 net unrealized losses over the course of the year. After accounting for all inflows and outflows, the fund’s assets declined by $222,547,509 over the twelve-month period. This is likely why the market apparently expects a distribution cut as the fund’s assets are currently lower than they were on November 1, 2020. Thus, the fund’s assets are down over the two-year period. It does appear that the fund is currently overdistributing and it may have to cut in the near future if the market does not turn around sufficiently.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a sure-fire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the abrdn Global Premier Property

Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund’s assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of April 3, 2023 (the most recent date for which data is currently available), the fund had a net asset value of $4.26 per share but the shares currently trade for $4.15 per share. This gives the shares a discount of 2.58% to the net asset value at the current price. This is, admittedly, not as attractive as the 4.97% discount that the shares have averaged over the past month, and it is not as big of a discount as we would like given the concerns about the distribution. It is recommended to wait for the shares to decline in price before buying.

Conclusion

In conclusion, real estate can offer investors a way to hedge themselves against the loss of purchasing power that accompanies inflation as well as generate an income. The abrdn Global Premier Property Fund is one way to gain that real estate exposure and its 11.71% yield makes it a very acceptable way to get an income. However, there are some signs that the fund cannot afford to maintain its distribution unless the market improves. That is not a particularly likely scenario as Chairman Powell has outright stated that the Federal Reserve will not pivot in the near term. Thus, it would be nice to see a bigger discount than this fund is providing. It is worth watching, but it is not advisable to buy the abrdn Global Premier Property fund today.

For further details see:

AWP: Decent Thesis, But This CEF Looks Risky