VNQ - AWP: Distribution Cut Coming Here Are Better Choices

2023-06-20 10:00:00 ET

Summary

- It would be a splendid compliment to call AWP a mediocre fund.

- The underperformance vs benchmark sector ETFs has been gargantuan.

- The yield has not been covered even from day 1 of the last distribution cut.

- Time for another one is upon us.

Aberdeen Global Premier Property Fund ( AWP ) is one we have covered quite a few times. The fund has a legion of fans thanks to a very large distribution. Unfortunately the real returns have been excruciatingly bad and likely to get far worse in the medium term. We go over our thesis to tell you why a big distribution cut now is a matter of time and what are some better choices today.

Fund Basics

There are a few REIT/Real Estate closed end funds around and they have all generally been structured to provide income. AWP is no different and that has been the mantra since the fund's inception more than 1.5 decades back.

CEF Connect

That picture also shows that we got this started right around when the global financial crisis was getting into motion and we started the score keeping at $20.00 per unit.

So above is what the price only chart would look like. To be fair, most real estate funds have not done spectacularly in this time frame. You would get better results if you just blacked out the global financial crisis and started after that. But if you ran from AWP's inception, even other funds like Vanguard Real Estate ETF ( VNQ ) and Cohen & Steers Total Realty Fund Inc. ( RFI ) had really poor price performance.

The allure for AWP and most other closed end funds, comes from their distributions. This next picture gets very instructive. AWP and RFI have huge distributions relative to VNQ, but only one of the two funds has done well.

Even if you love distributions, you would have to escape from an asylum to say you would prefer AWP's total return over RFI's.

The Current Setup

There are three things we want to focus on here, all of which have implications for the distributions going forward.

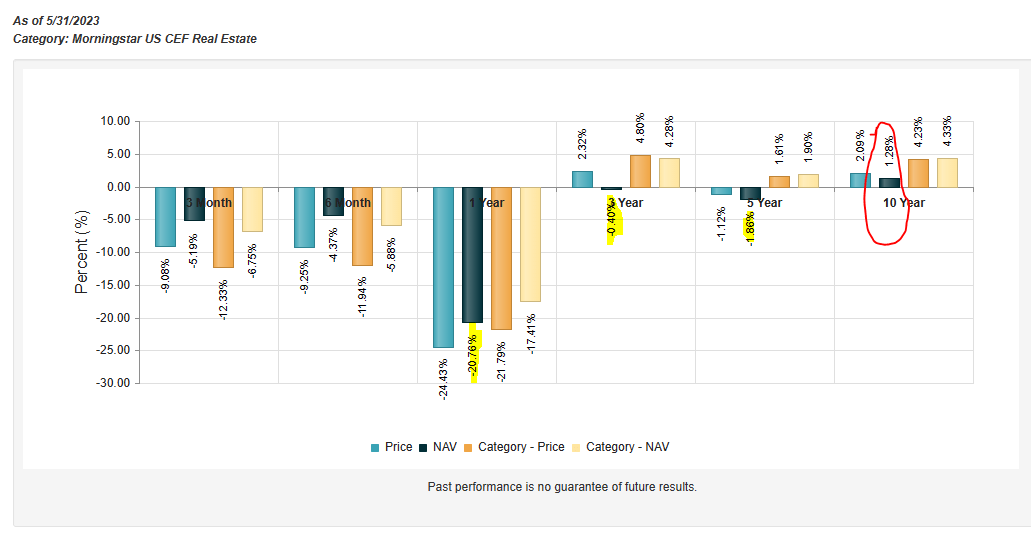

The first is the performance over all relevant timeframes. We had previously shown you the total returns since inception but below we show you annualized performance over 1, 3,5 and 10 years. Those all include distributions reinvested.

{kind=link}

So whichever time frame you choose, you can see that AWP's total return lags the yield by a mile. So if you were looking for a covered distribution, whether via underlying yields or capital gains, you won't find it in this fund.

The REIT's troubles are compounding though as time moves on. It is constantly depleting its NAV to fund its distributions. The last distribution cut happened just as the fund hit a 12% distribution yield on price. Today we are over 12.4%. Yes, the yield went briefly higher during the beginning of the pandemic, but that was an extremely brief period. Here, we have made an entire base near the 11-12% mark and broken higher.

The final problem is that the cost of capital is becoming really high. AWP does use leverage like most other CEFs. To their credit, this is relatively modest.

AWP

Unfortunately, the cost of this now exceeds pretty much the bulk of their underlying holdings, distribution yields. That $65.2 million would cost the risk -free rate plus 0.85% or over 6.0%. None of their top 10 holdings yield that much.

CEF Connect

Outlook

We think REITs will be pressured for the foreseeable future. Analysts assigning ultra-high multiples from the last decade in the name of "growth" are likely to get extremely poor returns. REITs like Prologis, Inc. ( PLD ), Equinix Inc. ( EQIX ), Welltower Inc. ( WELL ) and Digital Realty Trust Inc. ( DLR ) are most vulnerable to substantial multiple contractions. If you take another 20% decline in the REIT index and multiply by the leverage in AWP you get a 23% drop in AWP. Add to that an unfunded 12.4% distribution and you are looking at a sub $3.00 price. The fund will likely cut to 2-3 cents a month at that point. Of course you could fall into the trap by arguing " the yield is still high.". That is a poor argument and if you made that same argument before the last cut when the fund was at $6.20, this would be your fate.

Further, after the next likely cut, the yield on your original cost would to 5.8% assuming a 3 cents a month distribution. So the yield always looks great if you have a short term outlook.

Better Choices

There are pretty much no great choices to generate 12.4% safely. If you think you will make that without your capital going down and eventually your total return losing out to Treasuries, you are deluding yourself. So if you want good real returns, you have to compromise on that yield.

1) Our best choice here among CEFs would be RFI. The fund's biggest strength here is the lack of leverage.

CEF Connect

We think this will be critical to capital preservation over the next 12-24 months. The yield is 8.4%, something we think the fund can maintain, though not really "earn" over the medium term.

2) Option Income On Quality REITs.

If you are looking for safer yields that have far lower beta than the market, then options can help you get there. On one of our most recent REIT trades we are setup to harvest 11.94% annualized to be long the stock only 19% below the market price (at the time of the trade).

CIP Trade 357

Early exercise was possible, but still our yield to worst (earliest exercise) was still near 10%.

Verdict

Circling back to AWP, the fund has had an unsustainable distribution policy for years and it will soon be time to pay the piper. The good thing here is that the fund is at a modest discount to NAV. So we have that going for us, which is nice. It still won't stop poor returns from here in our opinion and we maintain a Sell rating on it, same as last time.

{kind=link}

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

AWP: Distribution Cut Coming, Here Are Better Choices