AWP - AWP: No Meat On This One

2023-12-26 12:29:09 ET

Summary

- abrdn Global Premier Property has failed to deliver value for investors in its 16-year history, with a drop in price by 81% and total returns of only 5%.

- The fund's high dividend distribution yield of 12% has not kept up with inflation, and its distributions have often come from return of capital rather than taxable income.

- AWP's use of leverage, international holdings, and high expense ratio may be contributing factors to its underperformance, making it a less attractive option compared to other REIT funds.

abrdn Global Premier Property ( AWP ) is a CEF that seeks to generate income for investors but in its 16-year history it failed to deliver any value for investors, and this may not change anytime soon in my view.

Despite having a 12% dividend distribution yield, the fund saw its price drop by 81% and it only generated total returns of 5% in the last 16 years while the market as a whole ( SPY ) was up 338% in total returns during the same period. If a fund has been around for that long and delivered no real returns, it starts resembling an annuity rather than a fund whose job is to generate wealth for investors.

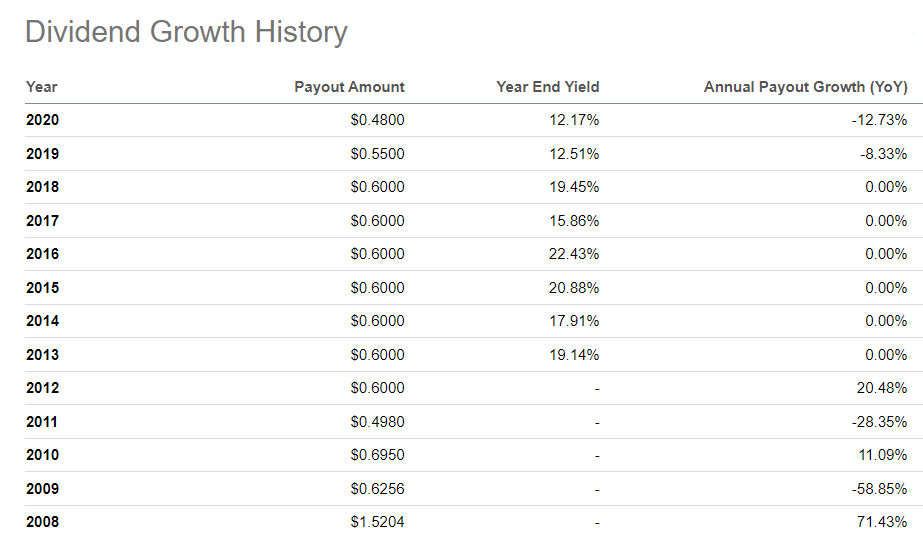

The fund's main premise is that it invests into high quality real estate investments which are backed by real assets so it should generate not only strong sustainable returns but also become a hedge against inflation since "real assets" tend to perform strong during inflationary periods (which we also found out not to be always true especially when interest rates are rising rapidly as a response to said inflationary period) but this fund's dividend distributions didn't even come close to keeping up with the inflation so that premise also seems to be unfulfilled at best. After distributing $1.52 per share in 2008, the fund never came anywhere close to this amount in following years. For most years, the fund's distributions stayed somewhat flat within a range; it got reduced from 60 cents to 55 cents in 2019 and further got reduced to 48 cents in 2022. As of 2023 it continued to distribute 48 cents per share which is the same amount as 2020 despite double-digit inflation we've experienced since then.

{kind=link}

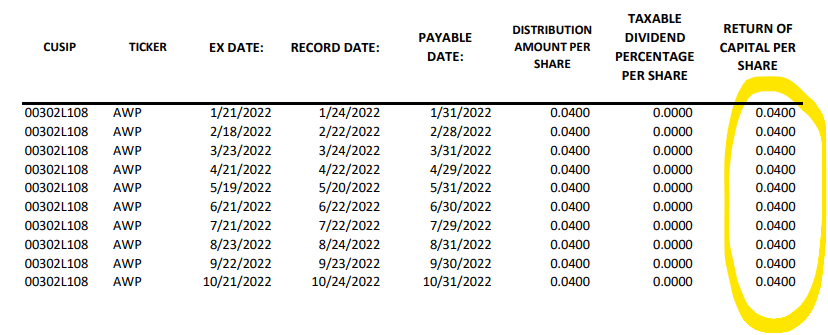

The fund always had trouble covering its distributions. For example, in 2022 all 48 cents distributed by the fund came from return of capital. The fund did not generate a single cent of taxable dividend which is good if you are trying to reduce your tax bill but bad if you want to see a well-covered dividend.

{kind=link}

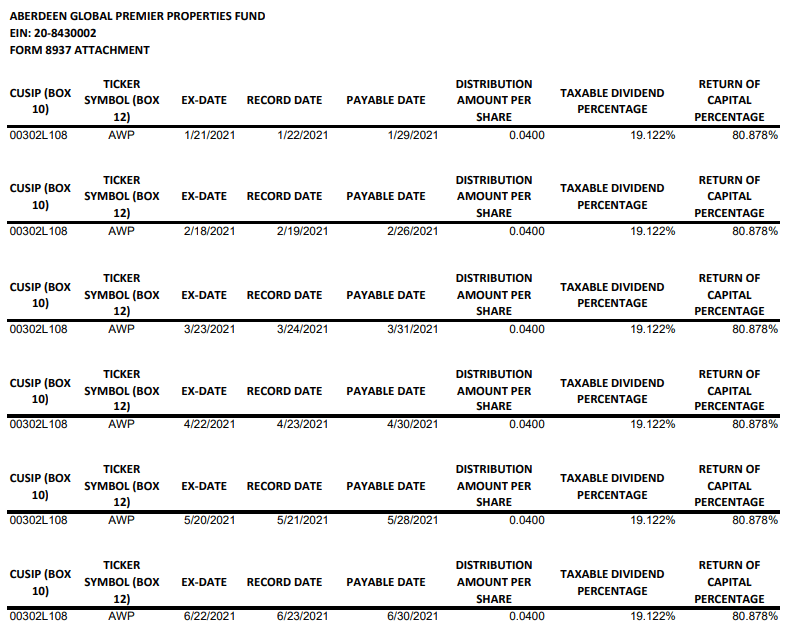

You might think that 2022 was a bear market so it's normal for all returns to come from return on capital. This is not necessarily true because the fund would still book some dividends and it could still sell some shares it held from past years for profit but that's beside the point. The finalized tax report for 2023 didn't come out yet but let us look at the report from 2021 which was a very strong year for the market. Notice how 80% of the distributions came from return of capital every single month during this year even though we weren't exactly in a bear market. I won't be surprised if we see a similar pattern when tax documents come out for the year of 2023.

{kind=link}

When we look at the fund's actual holdings, they don't look too bad. In fact, I personally hold many of them in my personal portfolio. Many of these REITs have a history of outperforming and hiking dividends year after year. But the fund's aggressive distribution policy coupled with its use of leverage might be hurting it. Another thing hurting the stock might be the fact that 40% of its holdings are international REITs which may be subject to different rules, regulations and policies than what American REIT investors are used to.

Top 10 Holdings (Seeking Alpha)

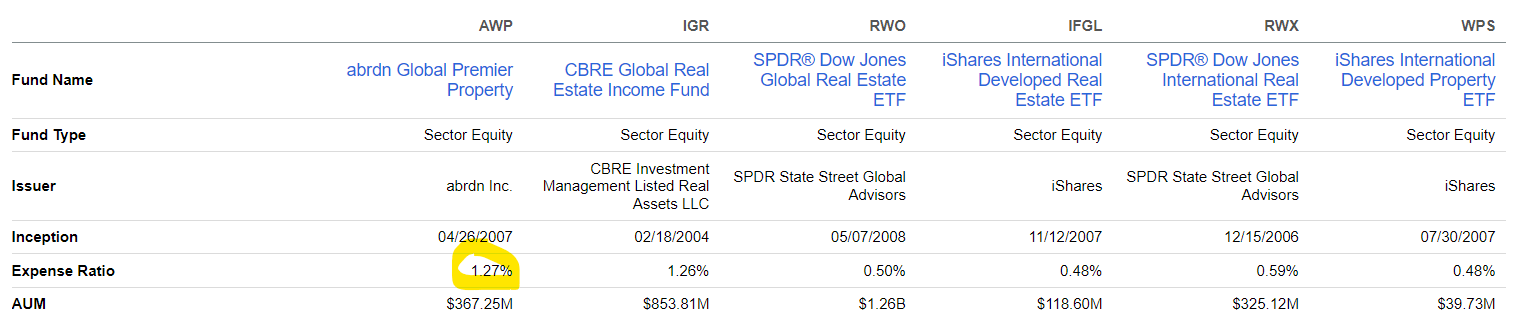

Another factor that might not be helping this fund out is its high expense ratio. The fund charges an expense ratio of 1.27% which is much higher than some of its competitors which have much lower expense ratios. If this fund had a history of outperformance, I wouldn't mind paying this expense, but in its 16-year history the fund did little besides returning investors' money to them in slow motion and I don't think it deserves such a high expense ratio. Paying 1.27% might not seem like much but these things add up. If the average REIT has a yield of 4-5% today, 1.27% is already anywhere from 20 to 25% of that yield so you are giving up a good portion of your income potential with that.

{kind=link}

The fund currently trades at a 10% discount against its NAV which is where it has traded for the most of the last decade even though there were brief periods where it had a bigger or smaller discount. The fund has never traded at a NAV premium in the last decade but there was a brief period last year where it traded almost at the NAV price. There was also a very brief period in March 2020 where it traded at a deep discount of almost -30% but it didn't last since the market had a very quick and sharp recovery during that year. Since this fund seems to settle around a discount of 10% for the most part, short term traders could benefit from buying the stock when its discount approaches and selling it when the discount is closer to 10% but I wouldn't hold this fund for the long term.

If investors still want to be in REITs for income purposes there are much better alternatives. For example they could buy and hold Cohen & Steers REIT & Preferred Income Fund ( RNP ) which has close to a 9% dividend yield and performed about 40 times better than this fund in generating total returns (200% vs 5%). Alternatively you can buy a REIT index fund like VNQ ( VNQ ) which didn't generate great returns by itself but performed much better than AWP.

Whether investors are in it purely for income generation or wealth creation, they should pay attention to a fund's long term NAV history and its total returns. If investors only look at a stock or fund's dividend yield, they risk falling into a trap which we call a yield trap. They find themselves in assets that continue to underperform year after year while the rest of the market performs much better, and they not only leave money on the table, but also potentially lose their hard-earned money in the process. When it comes to investing, your first job is to protect your hard earned money and then to grow it.

For further details see:

AWP: No Meat On This One