AXAHY - AXA: Good Performance Looking At 2024E And Potential Overvaluation (Rating Downgrade)

2023-12-31 09:07:52 ET

Summary

- AXA has delivered solid results and is expected to continue performing well in the future.

- The company's half-year results show a 5% increase in underlying earnings and strong solvency ratios.

- AXA's business model and market leadership make it an attractive long-term investment, but its valuation is becoming a concern.

Dear readers/followers,

My position in AXA (AXAHY) has performed well. This is due to the company delivering quite solid results. Looking forward, I see very few scenarios where AXA does not continue to perform well, so in this article, I'm going to look at these possibilities and see what the company could do for your portfolio. We have in fact, new data to consider for the company. Both the half-year results are out, and even if we need to wait until the end of February next year before we get the full-year results, we have the 9M results, albeit a small set of indicators compared to a full quarterly result.

I will say at this point, that there are indicators that AXA S.A. is slowly starting to get fully or even overvalued. In fact, for the first time since covering this company, I have found a realistic assumption where this company at €30/share could be considered to be fully valued in this environment.

To remind you, AXA remains a core investment in the financial portion of my portfolio. I can show you the outperformance that I have been able to record on this investment using this simple picture, from one of my first articles from over 1.5 years ago.

Seeking Alpha AXA (Seeking Alpha article)

So, you may understand why I'm not just "holding" here, with an average YoC of over 8%, but why I am starting to look at a rotation here if the valuation goes "too high".

My last article for AXA can be found here.

Some significant changes in the company's valuation, and therefore the relative upside to the company, call for me to change my rating and my outlook for AXA here. The quality of the company has not changed - but when pricing and upside does, so does my thesis and expectations.

Let me show you how.

AXA - Updating for 9M23 and for 2024E.

As mentioned before, the company has in fact done very well so far this year. The underlying earnings for the group are up 5% YoY according to IFRS4, and 18% on the basis of the previous IFRS17/9, seeing over €4B worth of underlying earnings for the company.

The company also goes on to boast some of the best solvency ratios in the industry - 235% for solvency II, with a Group UEPS of 8% YoY. This implies a solid half-year performance, and indeed AXA had no markets that performed poorly during this period. While it can be argued that Asia and Europe saw a decline, given the larger trends that are and were ongoing during this time, I will still not consider ta single-digit IFRS4 decline anything to be concerned about.

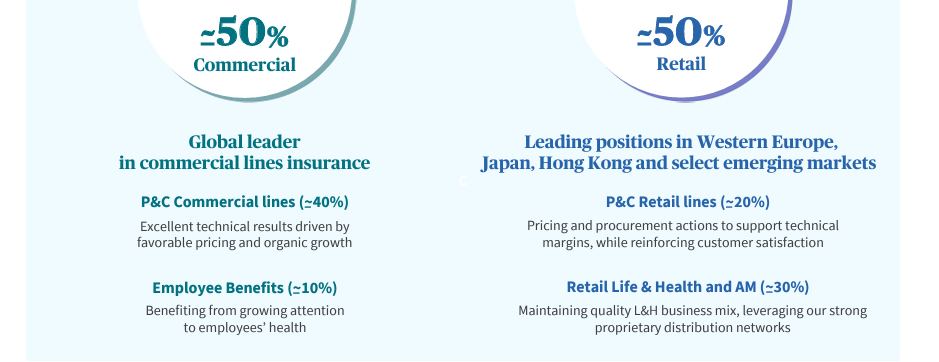

These results were solid - and they reflect AXA's superior business model, with a 50/50 commercial and retail split. This split is one of the core reasons why I am and remain an investor in AXA.

AXA remains a global leader in commercial lines, and a leader in Western Europe and certain Asian markets in the retail market.

{kind=link}

This, as far as I am concerned, makes the company an absolutely superb player to invest in for the long term, at the right sort of price. AXA is also no stranger to reinforcing this market leadership with key M&A's of attractive players, even if sometimes those players come in at sub-€1B prices. Laya Healthcare is a very good example of this, and a very recent one. AXA acquired 600,000 clients with a 28% market share in core areas, mostly in France, UK, and Germany but growing in Italy, Spain, and other areas as well, paying premiums of over €800M per year. This is in accordance with the company's strategy of accelerating its growth in the healthcare sector in Europe.

The company is very confident in terms of delivering its full-year targets, meaning UEPS growth of 3-7% p.A, and a solvency ratio that's 40% over the targeted minimum 190% level. The company has a RoE that's well above the stated 13-15% target, managing over 16.5% for the 2023 half-year period.

A quick glance at the business lines AXA is in. Property and Casualty, or P&C saw good growth at 7%, with 9% in commercial lines due to strong demand. The company does not manage combined ratios close to the sub-87% here in Sweden, but an IFRS17 combined 90.9% ratio is still very good , with claims frequency down and risk managed, while still delivering very solid results.

Life & Health saw good net flows, volatile market conditions sending results down about 1%, but a solid continued NBV margin of 0.1% up from the previous period, with excellent growth among other things in protection and health, and a significant decline in Traditional G&A, which the company is looking to scale down anyway.

The company saw increased claims in the UK for the period, which also impacted results here. As for the company's asset management, or AM arm, the company saw robust flows, but the market impact from underlying market conditions sent earnings down.

These companies move in cycles. AXA has been undervalued for a long time. I mean several years, when I say this. However, in the past 18 months and since I have been covering it, the company has been steadily increasing. That is why my position is now up over 75% including FX and dividends, and why I am doing this review - to see if the time has come to change my price targets for AXA.

The company hasn't materially changed its operations and appeal since I started writing about it. A share price of €30/share was always in what I considered to be the normal operations for this company, and that is why I am not surprised.

Successful investing is more about patience and valuation than it is about anything else, as I see it. AXA is a good example of what can happen when patience and valuation go hand in hand to deliver solid outperformance.

The latest trends we have from the company are the 9M23 trading results and activity indicators. We use these to get, as the name suggests, an implication for the longer-term results for the company, in this case, the 2023 fiscal.

Overall, AXA reported very good results in November as well. Gross written premiums were up 2%, and the P&C commercial lines, one of the company's focal areas, continue to grow at near double-digit rates. The P&C personal lines are up 5%, with protection premiums reversed and up 3%. The Solvency ratio is down 5%, which means it's now a full 40% over target, but not 45% as during 1H23.

In short, AXA is fully on track to achieve its operational targets for the 2023E period, which should be the next step in delivering a solid valuation and seeing this company climb over €30/share.

The company's business model is not in question as I see it, and I give you what risks and upsides to the company that I see below.

Risks & Upside to AXA

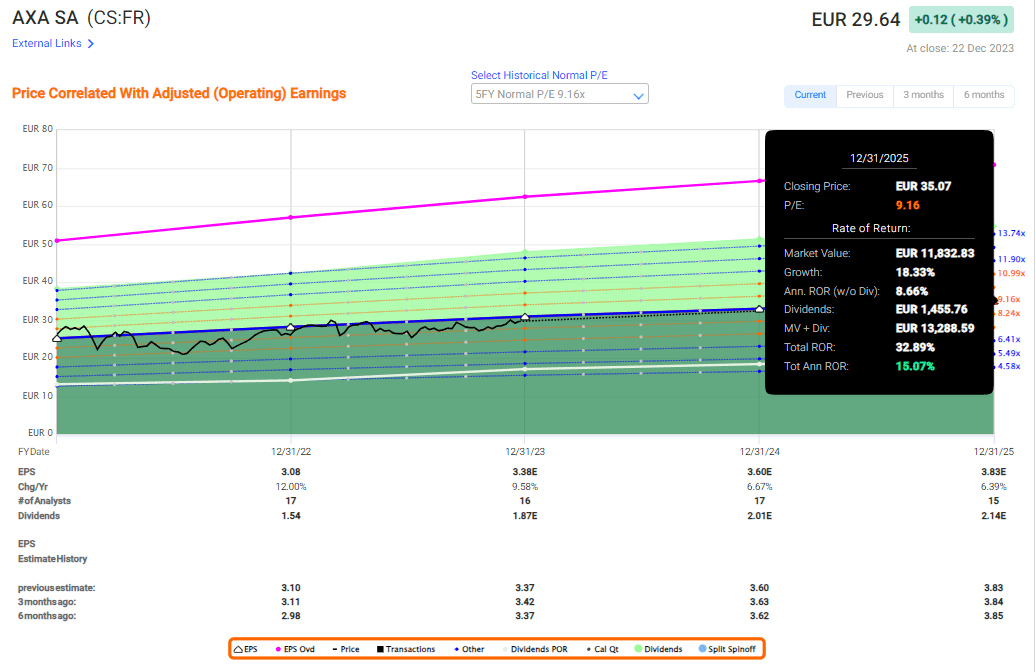

The risk to AXA here becomes one actually of valuation. The company was a no-nonsense buy at any valuation close to or below €20/share. It was cheap, and a great holding for your portfolio with a very solid yield. Even today, the native yield for the French CS ticker here is over 7%. But we're starting to see problems here in terms of pricing. We'll go into more about this in the valuation section, but in essence, the company at anything approaching above €30/share is no longer as great a "BUY" as it once was. Dependable valuation models show this company scoring in a €27-€31/range, which means that over €31, we're starting to push that.

Aside from this, I also have to mention that AXA has a history against it. It's a company that over time generally has not outperformed the market, and its performance when it comes to large M&As like XL is in question.

As with any insurance company in the P&C sector with exposure to central Europe, which AXA has, it's also heavily exposed to natural catastrophes. Any such instance would deeply affect profitability upsides.

On the flip side, we have the fact that AXA has done extremely well in carving out a niche for itself in some of the commercial lines, and while I can question XL, the appeal of XL expands the commercial lines and portfolio to NA, which can deliver the company solid growth if AXA can underwrite (which we know it can). The sale of the AXA equitable segment in conjunction with the XL M&A is also a good move because it means solid portfolio balancing - again, a significant positive here.

So, to conclude, the main risk here is valuation.

Valuation for AXA - It's no longer a top-tier "BUY".

Despite all the positives I said in the rest of the article, you also have to remember that my price target here is €28.5 - at least that was my last one. I am willing here, based on good results, to increase it to €29.5, but that still leaves us 14 euro cents overvalued to the current native share price.

The fact is here, that while you could buy the company here and get an adjusted 15%+ annualized RoR, I argue that the rate of error makes it so that you might consider other investments.

{kind=link}

You may argue here that I am changing my rating too early, and I am being a bit trigger-happy. But know that I am not yet selling my stake. I'm just not buying more, and I believe that in today's market where you can easily score prefs with over 7.5% yield at good upside, this is no longer as attractive as it was a year ago or more.

Whenever this company inches toward 9-10x P/E, it's historically been a good time to pay, and when it actually moves above, the right choice has been to rotate and sell this to other companies.

So I am watching AXA now. Not "BUY" ing more, and not selling yet either.

Thesis

- This is one of the largest asset managers and insurers in all of Europe and the world. It has rock-solid foundations and a 200-year history. Under the right circumstances and at the right valuation, this company is a definite "BUY".

- I believe that a conservative estimate of the company's abilities calls for at least a target of €29.5/share, up from €28.5 in my last article. This means the upside is now gone, and we can look at potentially harvesting profit, if the company moves up more.

- Based on this, I would consider AXA a "HOLD" here, and a firm one, and this represents a very long-term rating change for me, given how long I have been positive on AXA.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The company is no longer cheap, and the upside here is less than ~1%. Other than that, it's a "BUY", but a very weak one.

For further details see:

AXA: Good Performance, Looking At 2024E And Potential Overvaluation (Rating Downgrade)