AXAHY - AXA: Lower Volatility And Higher Earning Growth

2023-05-17 06:59:16 ET

Summary

- Driving Progress 2023 plan is almost completed.

- Solid Solvency II ratio evolution supported by core capital generation.

- Earnings target above €7.5 billion in 2023, so we confirm our buy rating.

After our deep dive into EU insurance and following the recent company's release of the Q1 numbers, today we are back to comment on AXA SA ([[AXAHY]], [[AXAHF]]). As a reminder, the French insurer has ' Immaterial Exposure To AT1 Bonds ' and on a bottom-down approach, in a recession environment, insurance players are protected with a 10% upside . For the above reason, we recently increased our buy rating target from €29 per share to €31 per share ($32 in ADR). This was supported by the new plan called "Driving Progress 2023" in which the company is positioned to achieve an earnings per share growth from 3% to 7% as well as there was a positive confirmation of AXA's tasty dividend per share. In detail, including also Assicurazioni Generali ( recently covered by our team ), AXA is currently offering the highest DPS in the EU insurance top-tiers companies and this was also confirmed by the recent DPS hike of 10% versus the 2022 dividend payment. Zurich, Generali, and Allianz increased their dividend by 9%, 8.4%, and 5.6% respectively.

Why are we bullish on the insurance sector? Here below is a snap from our recent Allianz's Q1 analysis :

In a world with negative interests, insurance companies have always gotten better at managing costs to sustain more operating profit. In the past, insurer players were outperforming thanks to investment activities (reinvestment yield) and not the core operating activities. This is why one of our key metrics to check was the combined ratio ((CR)) quarterly evolution. This metric divides the incurred losses and expenses by the earned premium. A CR lower than 100% means a profitable company. Currently, here at the Lab, we are long in the insurance sector due to a double profit generation 1) higher reinvestment yield and 2) better CR evolution.

This evolution is well-documented (and supported) thanks to Mare Evidence Lab's AXA's 10-year performance analysis.

Aside from the above, here at the Lab, we are confident that AXA has now finalized one of the most ambitious plans in the industry, following its disposal of AXA Equitable in 2017 and XL acquisition in 201 8. The business integration was longer than anticipated; however, in 2022, AXA XL ' Is Benefitting From Lower Risks ' . Today, the company is more resilient and has simplified its structure with a leading position in Japan and Western EU.

Q1 update

As usual in the Q1 release, the French insurance player does not disclose the company's operating profit; however, AXA confirmed the group underlying earnings target above €7.5 billion for the current year. This also includes a negative €0.1 billion FX impact.

{kind=link}

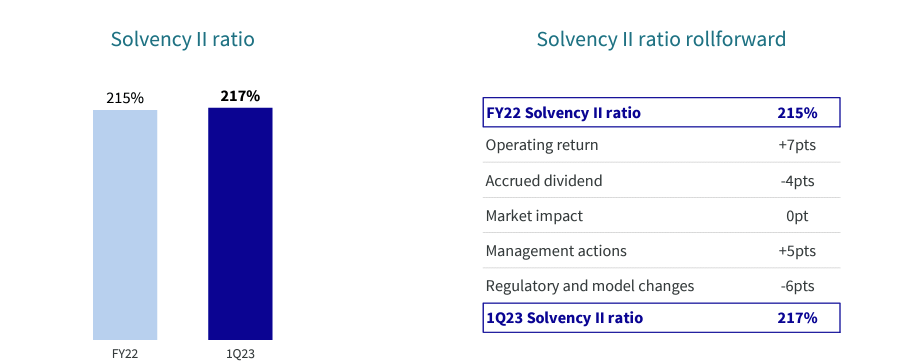

The company delivered a good set of numbers with total gross written premiums up by 1% on a yearly basis. AXA recorded solid growth in the P&C division thanks to price increases. A similar performance was achieved also in the Health division, while the Asset Management top-line sales were down by 4% due to lower AuM management fees from unfavorable market conditions. With no volume impact, and a higher price, the company is continuing to generate capital. Therefore, we are not surprised to see that the Solvency II ratio reached 217% from 215% at year-end. The ratio is also net of accrued dividends. More important to note is the fact that AXA now expects a Solvency II ratio of 25 to 30 basis points higher in 2023, thanks to the solid earnings growth and " the impact of lower required capital ".

{kind=link}

Conclusion and Valuation

2023 is the last year of the company's ' Driving Progress ' strategic plan. In February 2024, the French insurer should disclose a new business cycle plan, which we think will be focused on revenue growth acceleration and higher cash remittances from its core operations. Here at the Lab, we are confident in higher earnings growth and lower volatility (thanks also to the new FRS17/9 accounting standards implementation). With a disciplined capital allocation, AXA is set to achieve our target price. The company is currently trading at a 7.8 P/E on our 2024 estimates with a 2023 FCF yield of 12.3%. According to our estimates, AXA's next plan could deliver a cumulative cash remittance higher than €20 billion to support €13 billion and €4 billion in dividends and buyback (maintaining a Solvency II ratio higher than 190%). Therefore, we confirm our previous target price of €31 per share. Downside risks also include higher natural catastrophes.

For further details see:

AXA: Lower Volatility And Higher Earning Growth