AXAHY - AXA: Record Results Again A Buy

Summary

- AXA delivered a strong set of numbers.

- DPS is up by another 10% and there is also a new buyback program.

- Above guidance. “Driving Progress 2023” strategic plan at full speed. We decided to maintain our buy rating.

In 2022, it was a solid call to move AXA (AXAHY) (AXAHF) from a neutral position to a buying opportunity. Following our publication called After The Recent Drop, It's Time To Buy , AXA is up by more than 30% (including its tasty dividend per share payment) and outperformed the S&P 500 return that signed a plus 1.42% in the same period. Here at the Lab, we often look to the past for future ideas and the French insurer giant investment was another successful capital gain story. Indeed, this idea was supported by our continuous effort to build up our internal models. In AXA (as for Allianz and Zurich ), we have a 10-year analysis of its main financial ratio evolution. In detail, we track the Combined ratio, the Solvency ratio, the Reinvestment Yield, and the company's Cash remittances. Our buy rating was also supported by a bottom-down analysis where we emphasized how AXA was scoring in the highest percentile based on the forecast shareholders' remuneration (including buyback and dividend payments) and in the lowest percentile in terms of valuation. There was also a mismatch between AXA's strong solvency ratio and its market discount.

Mare Evidence Lab's previous publication

{kind=link}

Q4 and FY 2022 results

" AXA delivered a strong performance in 2022 despite a challenging environment, a confirmation of the resilience of our business model " explained AXA's CEO Thomas Buberl. In detail, the company's top-line sales were up by 2% thanks to a strong performance in the P&C segments (driven by price increases) and the L/H division which was up by 16% on a yearly basis. These positive results were partially offset by Life & Savings and Asset Management division results which decreased by 5% and 3% respectively. For the latter, this is not coming as a surprise given the unfavorable market conditions and the consequent lower fee generation. Regarding the L&S segment, as already reported in Allianz, there was a decline in Unit-Linked products, mostly in Italy, France, and Japan. Given the recent upward trend in interest rates, B2B clients are now investing more in fixed-income products & Govies.

Looking at AXA's financial ratio, we are happy to report that:

- All-year combined ratio stood at 94.6% and was only up by 0.1 points (Fig 1). This is a solid result given the COVID-19 new normal (with elevated Motor claims), the Ukraine war, and the Nat Cat charges. AXA was able to lower its expense ratio from 26.6% to 26% thanks to improved profitability and AXA XL's higher pricing evolution. Very much in line with this development, we suggest checking our previous analysis called AXA Is Benefitting From XL Lower Risks;

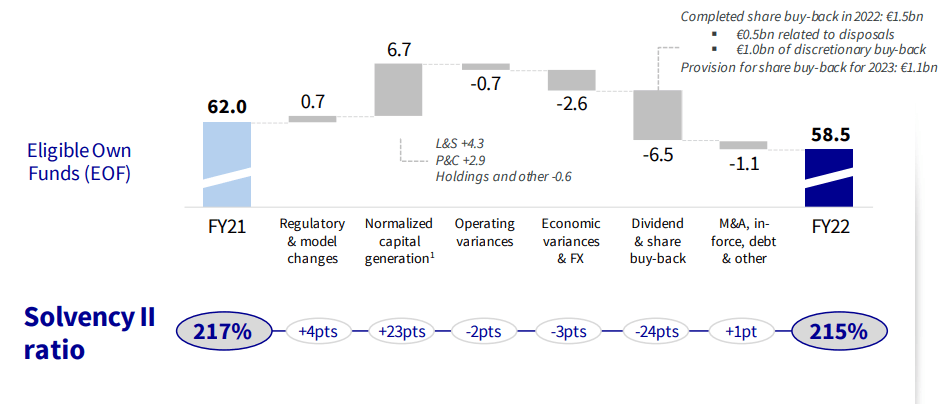

- The Solvency II ratio reached 215% at December end and was down by 1% point compared to last year. However, this was mainly due to the €1.5 billion share repurchase completed in 2022 as well as a provision for the next buyback of €1.1 billion announced today. This provision impacted the AXA ratio by -10 points. Here at the Lab, we are already incorporating lower solvency for Q1 2023. The EIOPA risk-free rates decision on the IBOR coupled with a change in portfolio reference will weigh down the ratio by minus 5 and 4 points respectively. Despite that, AXA is fully in line with EU regulatory requirements.

AXA combined ratio evolution

(Fig 1)

AXA Solvency II ratio evolution

{kind=link}

(Fig 2)

Conclusion and Valuation

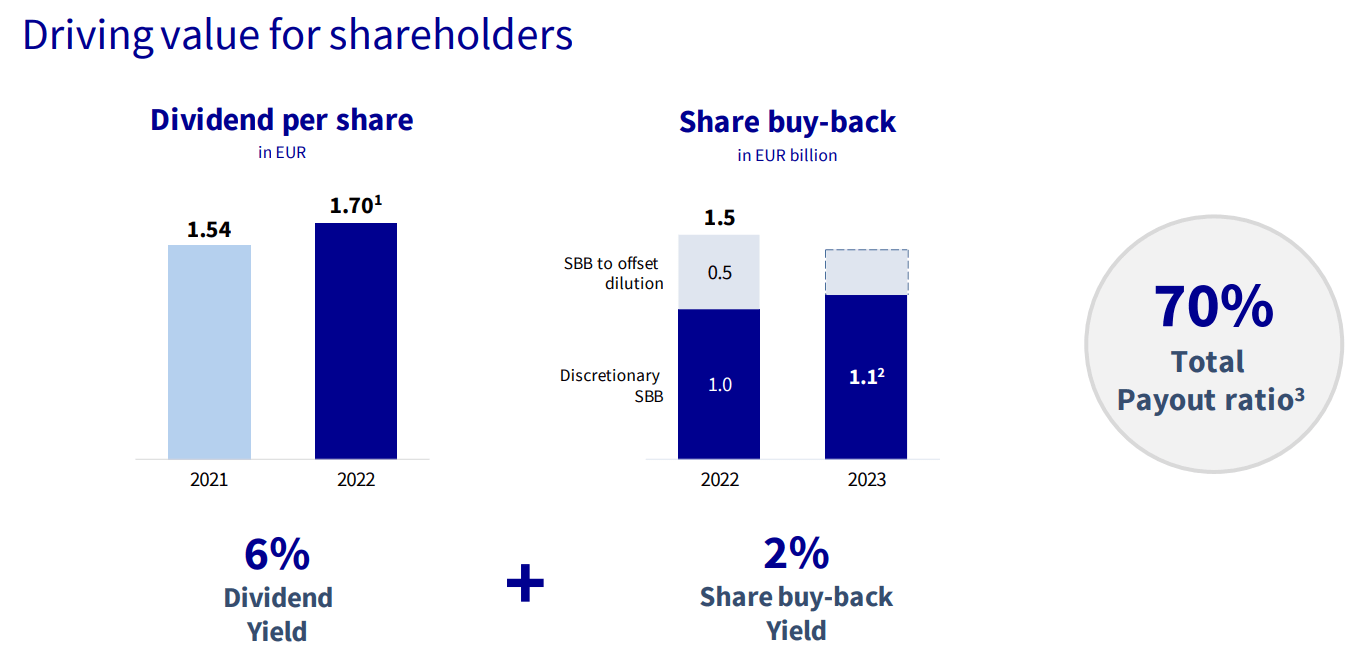

Starting with the shareholder remuneration, if approved, AXA will propose a dividend of €1.7 per share, up by 10% (as a reminder Allianz increased its DPS by 5.6%, while Zurich by 9%). The company once again is yielding higher than its closest peers. In addition, AXA will launch another buyback for a total value of approximately €1.1 billion. Important to report is the €4.5 billion cash at Holding at December end which is well above management targets. Here at the Lab, we positively welcome AXA results which confirmed our view. In detail, our internal team was forecasting a continued surprise in the ROE evolution and above-average EPS and dividend growth. We were estimating a 10% and 13% increase respectively for 2023. AXA's net profits reached €6.7 billion and were down by 11% on an annual basis. This was mainly weighed by a drop in the value of assets and derivatives as well as by the Russian JV write-down. Despite that, the group CEO Thomas Buberl said that AXA " is well positioned to deliver on our "Driving Progress 2023" key targets, and currently expect to exceed our targeted compounded annual growth rate of 3%-7% in underlying earnings per share over the plan period ." Excluding these adjustments, underlying EPS reached €3.08 and was up by 12.3% compared to the Fiscal Year 2021 results. For 2023, we are forecasting an EPS growth of 4% (at midpoints of management guidance) and continuing to value AXA with an 11x P/E, we derive a valuation of €31 per share and $32 in ADR (from our previous buy rating at €29 per share). If you are looking for more capital upside opportunities, we suggest checking our latest Generali publication.

{kind=link}

For further details see:

AXA: Record Results, Again A Buy