AXAHY - AXA: Time For An Update On High-Yielding Quality Insurance/Finance - I Say 'Buy'

2023-10-09 23:07:56 ET

Summary

- AXA has reported 1H23, a set of results that I am going to review in this article.

- AXA remains a core investment in my portfolio, and a very solid insurance and financial investment overall. I would call more to the company if it dropped.

- AXA is still appealing here, and the company trades at a sub-10x P/E, which to me still marks it as a "BUY".

Dear readers/followers,

AXA SA ( AXAHY ) ( AXAHF ) has been a company I've been offering free coverage on for over 1.5 years at this point. It's also one of the largest asset managers and insurance businesses I have been investing in for quite a long time.

My last article came at the onset of August, or the end of July, where I still maintained a solid "BUY" rating, but noted that on the whole, the company is moving closer and closer to its PT and therefore a "HOLD" stance from my side. However, since that article, which you can find here, the company has actually normalized somewhat in terms of pricing and valuation. Not as much as the S&P500, and not even 5% in total - but still some amount.

All things being equal, this should imply a somewhat larger upside to the company here, and a yield that despite the current interest rate environment is very competitive.

So let's see what we have here, and update on AXA S.A.

AXA S.A - One of the French companies you should own.

I've not made a secret of my investing in French companies, which on the whole are relatively undercovered here on Seeking Alpha. The same goes for other countries in the central/southern parts of Europe. I do understand some of the hesitation on the part of income investors given the dividend taxation in France, but I also argue that you can find plenty of attractive businesses here with higher conservative upsides than those found in the US and that those businesses are as or even more qualitative than American businesses that are comparable.

When it comes to AXA, that argument is relatively easy to make.

AXA as a business hasn't had a bad year or really bad quarter since early 2019-2020 - despite this, the company has traded significantly below a double-digit P/E and currently trades at less than 8.7x, and that's for an A+ rated multi-line insurance business. So, the logic in that, or lack of it, really stands out to me. It can be compared to businesses like Allianz (ALIZY) or, despite not being a reinsurer, have similar safety to Munich RE (MURGY). Those two businesses are for some reason much more well-received than AXA - and that's something I want to change.

Education and information are the best tool - so here we go.

Half-year results, which I have yet to formally review, were posted in early August of this year - so we'll go into estimates a bit as well.

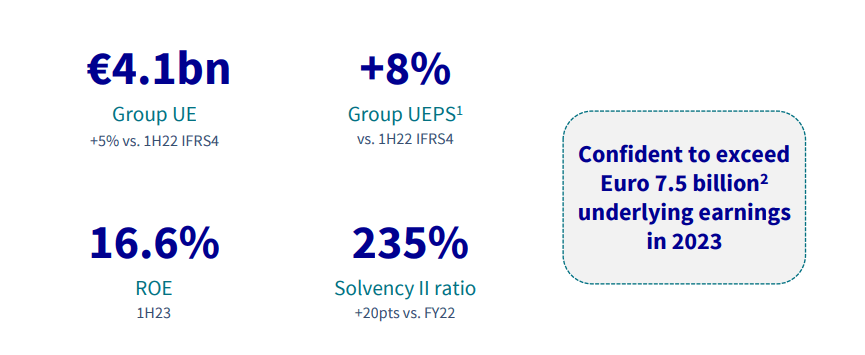

But let's dig down and make it clear that the company went above its expected earnings growth, maintains solid solvency, and an excellent RoE. (Source: 2Q23 AXA )

{kind=link}

This implies a run rate of over €8B or as the company guides for, above €7.5B in annual underlying earnings for this superb business.

What makes AXA such a convincing investment for me?

It's an attractive mix, for one. The company's 50% commercial and 50% retail exposure with only 10% exposure (out of 50%) to employee benefits is beneficial to where I sit. This mix is well-suited for the current interest rate and macro environment - because when one goes up, the other is usually down or flat. This more or less guarantees, or at least strongly implies, a stable performance. (Source: 2Q23 AXA )

Furthermore, AXA is adding to this through the addition of M&As like Laya Healthcare. The M&A is, as of this example, amongst-leading market participator in Ireland with a 28% market share in a fast-growing market, highly digital highly efficient, and extremely capital-light. The company's acquisition will add €800M to AXA's top line - nothing to sneeze at, and AXA bought it at 11x P/E.

Why did AXA do so well in terms of earnings? Like any larger player, the company enjoys a very favorable pricing environment in the Property and casualty sector. The high interest rates are, as you know, in part very beneficial to insurance players, and the company really had no issues in terms of Natural Catastrophes in Europe for the past 6 months (starting January) compared with earlier terms. (Source: 2Q23 AXA)

Instead, AXA can focus on growing organically and managing the ongoing volatility. Fundamentals are a place to drive earnings growth due to an attractive business mix that historically has enjoyed a very attractive margin.

{kind=link}

And, did I mention that AXA has increased its Solvency II by over 2000 bps in less than a year? This was due to strong capital generation, lower capital requirements due to a change in the business mix (the life business above all), and reduced interest rate sensitivity on the receiving side.

It's a trend I've been witnessing for a few years now - insurance companies being less and less willing to hold risk in the life sector, and trying to divest what risk in life-related or life insurance blocks they do have. It does indicate some trends that make me want to look deeper at where that risk is being directed to, and what companies would make for attractive investments in those sectors - but for now, it's a mere observation.

Going forward, what you want to keep an eye on with AXA will be continued profitable underlying earnings growth. Where the company can steer this is in terms of its pricing discipline and margins - so those are the KPIs you want to be looking at.

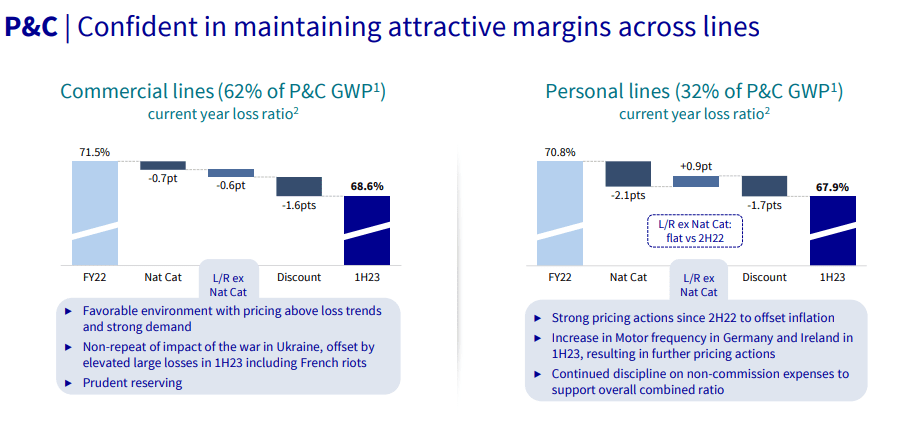

For the 1H23 period, these pricing trends are holding up well above current loss trends, and renewals are being made at 4-7% for AXA XL, which is above the current rate of inflation in many environments, though not in my home environment. (Source: 2Q23 AXA)

The company's year-long move towards commercial line-type insurance is now paying off due to higher technical margins. We're looking at a combined ratio, adjusted for IFRS17, of below 91% here. It's far from as solid as some of the class-leading players in this industry, but it's good enough that I'm raising eyebrows here. Furthermore, the company is confident in retaining this trend thanks to favorable loss ratios.

{kind=link}

The company's sectors that are being viewed with more care on a macro level given the trends in life/health for the past few years have nonetheless performed well. We have good net flow, even if those flows are being impacted by volatile market conditions. It's the sector that on the basis of this report is down in terms of revenues, mostly due to traditional G/A products/services.

However, AXA's NBV margin, that being the new business value margin, a common concept in insurance, is solid and unimpacted by the market. So like with other companies, it's mostly the legacy L/H that's causing some issues here. The new business is actually fueling growth. (Source: 2Q23 AXA)

Still, claims are up and this is at the very least worth noting - especially in the UK.

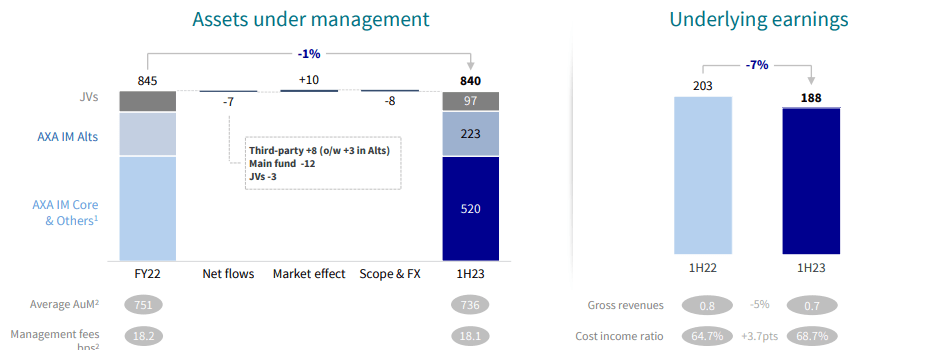

Moving on to Asset management.

{kind=link}

As you can see, some decline here as well, but overall reflective of a very qualitative business despite the troubles the market is currently in as I'm writing this (the overall decline we're seeing right now).

So, wrapping up the first half year for AXA, here is my view.

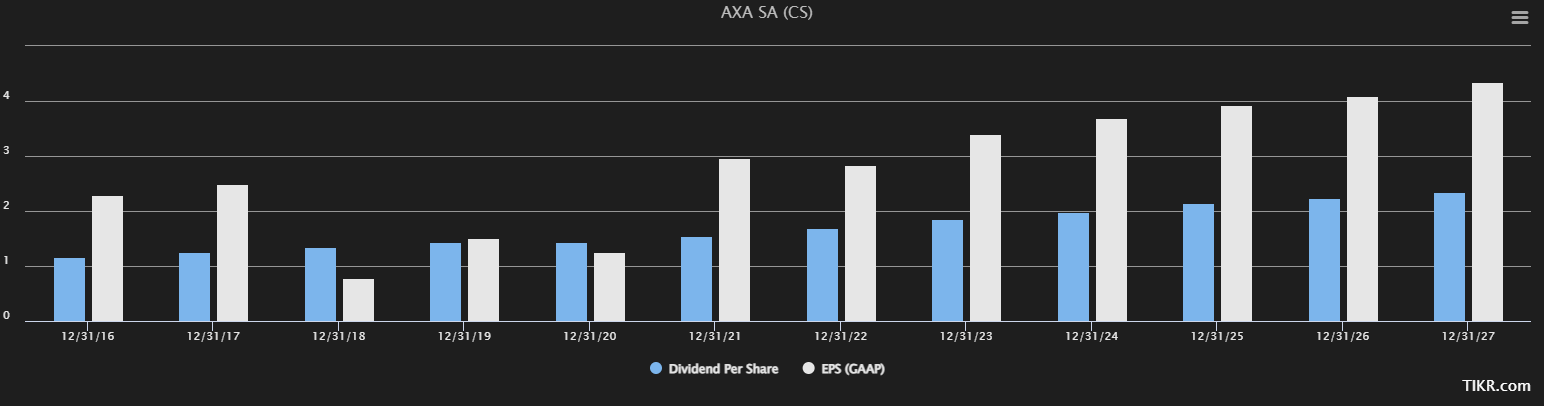

AXA had a very positive 1H23 in the context of this macro. We're talking about a solid increase in UEPS, or underlying earnings, of 8% from capital management and earnings growth combined. The half-year EPS is now almost €1.8, which implies a ~€3.6 run rate for this fiscal. Fundamentals and solvency are extremely high, and the company offers investors a yield based on the 2022A dividend of €1.7/share of around 6%.

This is no longer as great as it once was - plenty of companies offer a high dividend, and there are many options that give you yields above 6% while taking a BBB+ type rated risk.

AXA is not "cheap" much like I said in my last article. But valuation still dictates that the company is attractive here.

AXA - The valuation continues to be attractive.

Why is AXA continually attractive here?

Because earnings, as things stand as well as the dividend, are set to continue to grow.

{kind=link}

At current valuations, the company is around at 9x blended P/E, with a continued upside based on growth to that 9-10x P/E range. In my last article, I made it clear that the upside was around 14% to around 9.1x on a 2025E basis. That upside is now over 15% again, which makes the company easier to "BUY" - even if the difference is actually less than €0.5/share in terms of share price.

It'll be a long time before I come anywhere close to rotating AXA. The company would have to climb to above €36/share for that to become anything close to valid. But at above €28.5/share , my upside is no longer above 13.5% annualized, and that's where I cap my finance investments for the time being - especially now in October of 2023 when rates and upsides in other investments have become comparatively much more attractive.

My "dream" scenario for AXA would be for the company to drop down below €24/share again, and to see yields of 7% and above again for this company. However, the increasing quality and solid set of quarterly performances have made the likelihood of this smaller.

S&P Global targets for AXA come in at a range of €28 to €37. You'll note that my PT is far below the average of €33.8/share they're currently giving the company, but this is the same as with Allianz or Munich RE, where I'm willing to "BUY" up only to a certain point, but where rotation of the holding is actually something I would only consider at significantly higher levels.

Still, 17 analysts follow AXA - out of those, 15 are still either at "BUY" or "Outperform", as of October 2023. So there's no change here from my last article.

The changes since July and since 1H23, now that we have more clarity as to the annual results, are small, but they still push AXA above a 15% potential annualized RoR, and that's what makes it more interesting here and actually causes AXA to fulfill my fundamental requirement for investing in a business in this environment.

There are valuation models where this company is actually overvalued here - but I believe that underestimates AXA's fundamental earnings power and its market position, so I don't give that much credence here.

This is my thesis for AXA in this environment.

Thesis

- This is one of the largest asset managers and insurers in all of Europe and the world. It has rock-solid foundations and a 200-year history. Under the right circumstances and at the right valuation, this company is a definite "BUY".

- I believe that a conservative estimate of the company's abilities calls for at least a target of €28.5/share. This means the upside is now all but gone, and we can look at potentially harvesting profit.

- Based on this, I would consider AXA a "BUY" here, but a weak one still, albeit at a higher upside than in my previous article.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The company is no longer cheap, and the upside here is less than ~1%. Other than that, it's a "BUY", but a very weak one.

For further details see:

AXA: Time For An Update On High-Yielding Quality Insurance/Finance - I Say 'Buy'