AXAHY - AXA: Why French Insurance Has Outperformed But Is Now A 'Near-Hold'

2023-07-29 04:39:34 ET

Summary

- AXA is expected to report positive earnings in the upcoming quarter, continuing the positive trends seen over the past few quarters.

- The company is undervalued compared to its peers and has strong financials, making it an attractive investment.

- AXA's performance in the insurance sector has been strong, with growth in various segments and stable margins. I consider it a "BUY" but a very weak one.

Dear readers/followers,

In this article, I'm going to provide you with an update on AXA (AXAHY). The company is set to report earnings in about 1 week, but here I expect a continuation of the positive trends we've seen over the past few quarters. AXA hasn't had a bad year or really bad quarter since early 2019-2020 - despite this, the company has traded significantly below a double-digit P/E and currently trades at less than 8.7x, and that's for an A+ rated multi-line insurance business.

Remember, many of our insurance giants here in Europe are multi-line as opposed to specialized/single-line. AXA is one of the best of those, with peers like Allianz (ALIZY) and also ancillary businesses in reinsurance, like Munich Re (MURGY) or Hannover Ruck (HVRRY).

Here is how the company has performed since my initial article, which I published some years back.

Seeking Alpha AXA RoR (Seeking Alpha)

I will say here that the company seems to me very clearly undervalued - both historically, and where it's been trading since. We're up some since that time, but it's nowhere near where I believe the company should justifiably trade given tailwinds from interest rates and other things.

So let's see where I think AXA should be.

AXA - Updating on insurance

In my last article, I said that AXA is actually becoming more expensive at this time - which it is. The valuation since I bought is after all over 30% "worse", given that's the RoR we've seen. But there's still some distance left to go.

I've been bullish on the European insurance sector, and French insurance for years. Not just French, of course. German and British as well, and even Italian insurance has, to my mind, some upside given the valuation we're seeing here.

In fact, Investing in European insurance is one of the reasons my portfolio outperformed vastly in 2022. It was my recognition and investment of significant capital into businesses like Allianz, Munich RE, and others that allowed me to outperform for the financial portion of my investments.

I was surprised by the degree of outperformance offered by the company in a short amount of time - but this is the essence of value investing. Recognizing a "low" or "cheap" share price is key - even if we can't forecast when exactly the company will turn around. Remember that - no one can forecast the market, it's all guesswork. We can see indicators - and we can try to look for signs, but in the end, in the short term, the market is something no one can forecast accurately.

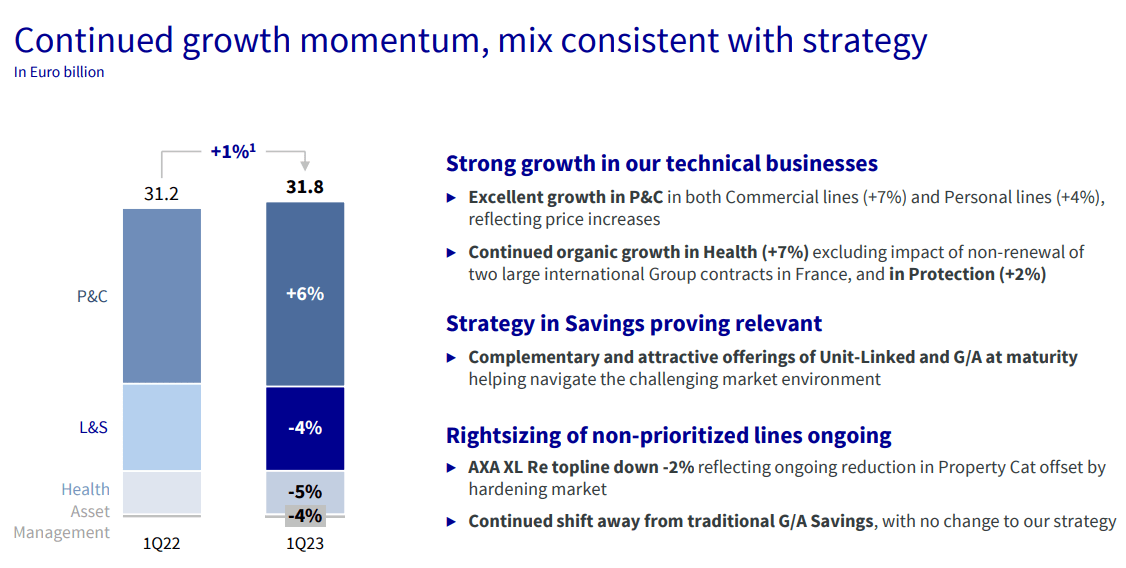

Take 1Q23 for instance for AXA. (Source: Earnings Release )

The company saw 1% topline growth despite pressure, with strong growth in Property & Casualty both for commercial and for personal, with also strong growth in protection. The company's margins are very much intact, underwriting is strong, and the Life/Health segment is working well as well.

Unlike some of its American single-line peers, AXA has no fundamental issues. Its solvency II is at over 215%, and its assets are of extremely high quality.

AXA targets a €7.5B underlying earnings number for the year and this includes €100M FX impact.

{kind=link}

The main advantage or positive result here would be company pricing. Price effects mean that the company is staying well ahead of inflation numbers both in France and on a European-wide basis. AXA XL Re, for instance, is seeing 12.8% increases in 1Q23 alone.

The new business mix is excellent. Company NBV margins are impacted by higher rates in protection and health segments. As mentioned, the target for this year is above €7.5B in underlying earnings. This would represent a €200M increase or more to IFRS4 in 2022, but a more than €1.4B increase to IFRS 17/9 results, which results are to be stated in for 2023 as well. The company's conviction in these targets is solid, due to strong technicals, and predictable CSM releases (CSM in this context being the contractual service margins) but offset somewhat by higher overall expenses at holdings, and lower AM revenues, as you'd expect from this market overall.

Furthermore, the company is expecting better results from the P&C segment going forward, upwards of €300M better for the year due to improved pricing, good releases, and lower losses at a high amount due to the non-repeat from the Ukraine impact.

I've been following the introduction of IFRS 17/9 for some time for EU insurance companies, and I find this to be a vast improvement going forward. The new reporting makes Shareholder equity far less volatile due to changes in OCI related to NIA (net invested assets) as well as liabilities. This was a position that could potentially go in the dozens of billions of Euros under IFRS 4.

Overall, the picture I want to leave you with for the 1Q23 quarter is that AXA continued to deliver very strong sales, showing strong resilience to anything having to do with inflation due to price increases. The company is confident that reaching that single-digit growth in 2023E underlying earnings is very much possible. The major impact for the new reporting is OCI - but overall, we're looking at extremely stable trends from AXA.

That is why I expect no material change going into 2Q23 whatsoever, with the company's guidance at a continued positive. I believe it's going to keep "growing" on a forward basis.

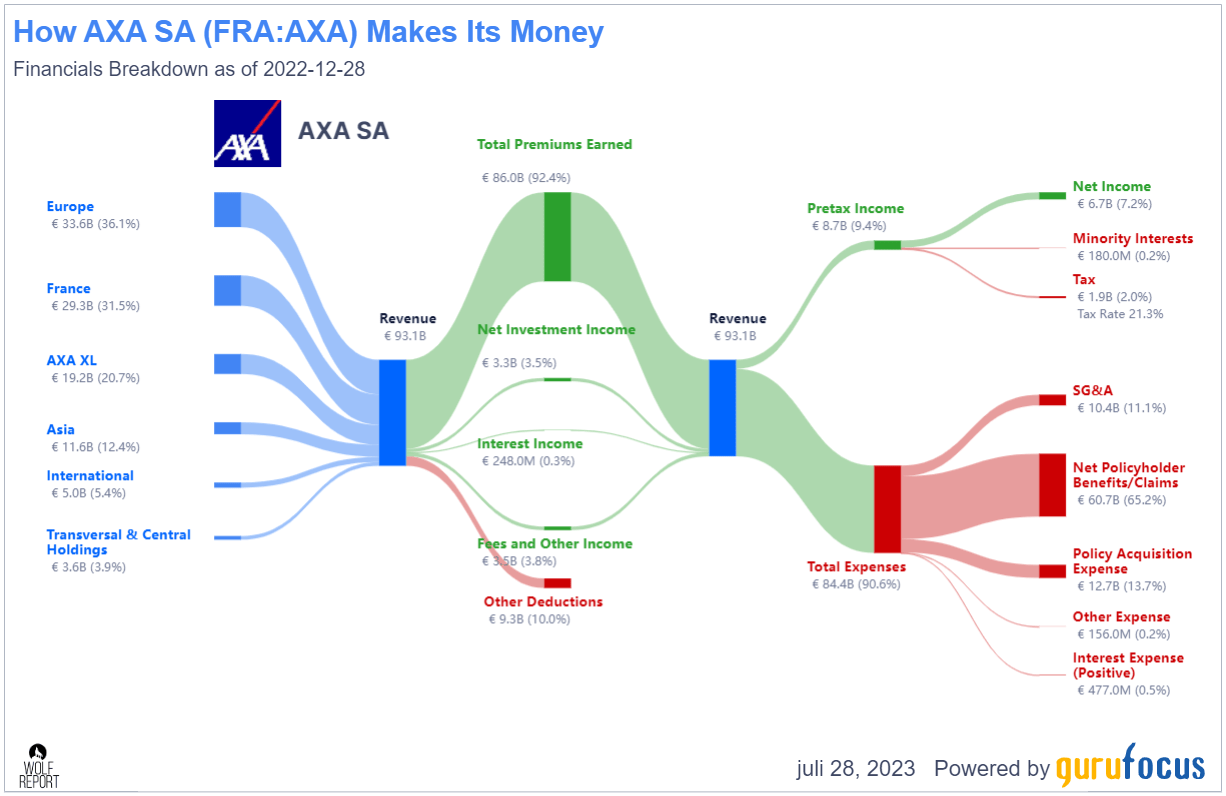

Remember, AXA is a very solid business. Here is a visual representation of its revenue/net.

{kind=link}

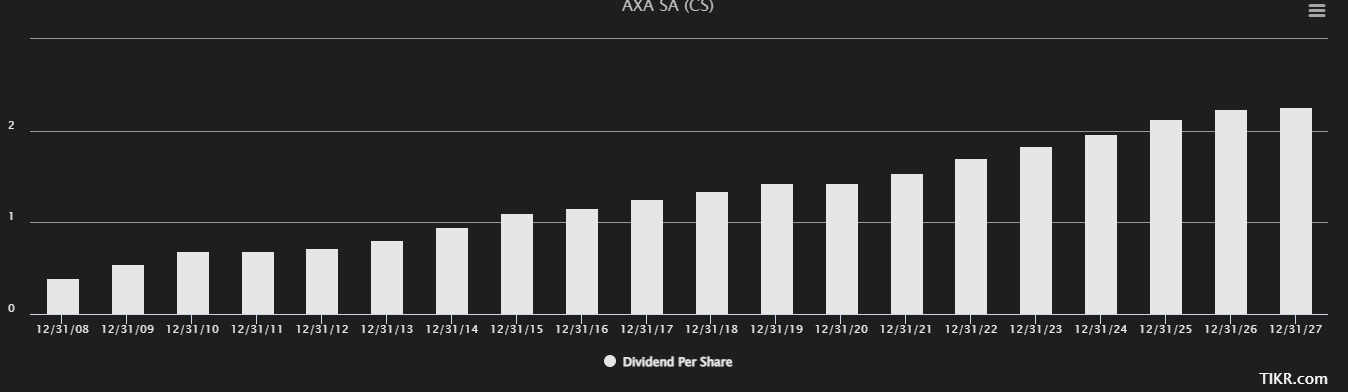

Forecast expectations for AXA are for revenues to keep growing at single-digit rates, and for the company to get above the €110B mark in 2025E, so in 2 years. The company's dividend is expected to remain perfectly stable and growing during all this time - as it has been since the GFC. The company did freeze it during 2019-2020 and COVID-19, but this was really the only impact that there has been for some time. As you can see, the company has been supremely reliable in terms of its payments and payouts and is expected to continue to be so.

AXA dividend (S&P Global/TIKR)

{kind=link}

So for as long as the company doesn't go into overvaluation, I'm very content holding it here, potentially even adding more shares. Remember, AXA still yields above 6% at this time. It's A+ rated, it has less than 30% of its debt/cap, and it averages a 20-year growth rate in earnings of almost 9%. There are few insurance companies in the multi-line subsegment as stable or as profitable over time. The fact that it's a French company should not faze you in the least.

For 2Q23 I don't expect any material changes in the upside or downside. I expect a good result on a YoY basis with some growth, much as we saw in 1Q23. I expect stable margins, and I expect the company to continue to fight off cost increases and other ongoing headwinds. Even in the case of a quarterly surprise downside, which I wouldn't be able to forecast the reason for at this time, I would only add more of this company if the reaction was a further downturn.

What I would keep an eye on is any sudden declines in margins, or if the company can't maintain its price increase to offset inflation and other headwinds. As long as this is the case, anything below a climate catastrophe or another pandemic is unlikely to impair either P&C or L&H lines to the degree that I see it necessary to adjust my price target for the company.

With that, let me update my valuation for you for AXA.

AXA - Continued upside is very clear to me

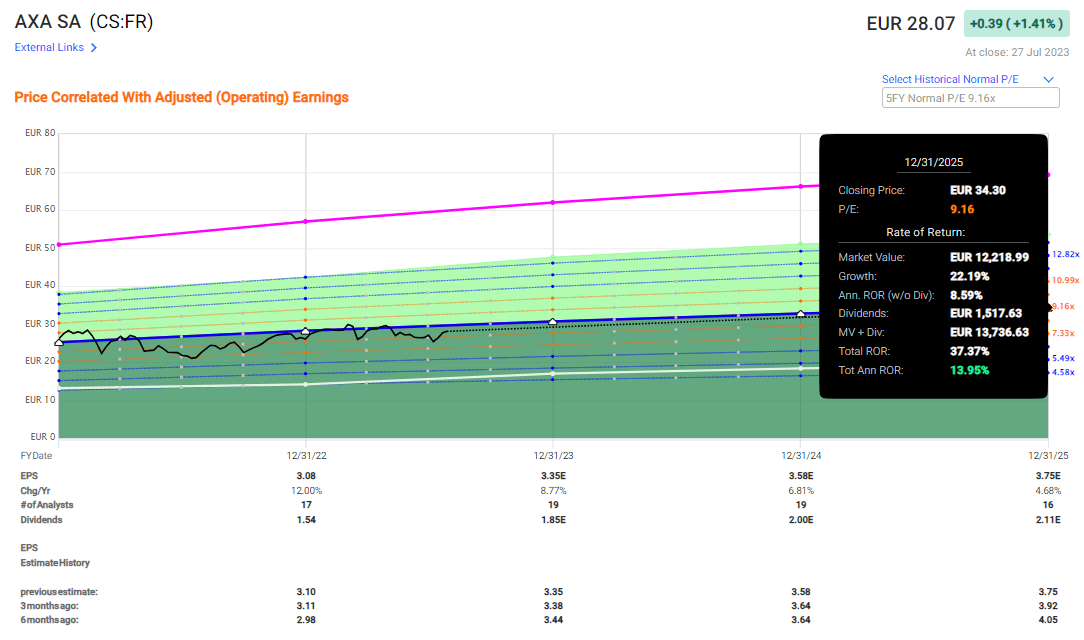

Now, because in my last article, I made it clear that my PT was €28.5/share and the company is now trading at €28.07, I want to be clear that the conservative upside in this investment is almost gone.

It's still there. By conservative upside, I mean 13-14% annualized, and the current 9.15x 2025E P/E forecast gives us a 13.95% annualized RoR, inclusive of the 6% yield. This is still "workable" despite a lower-than-historical earnings growth rate forecast of about 6.7% per year.

F.,A.S.T Graphs AXA upside (F.A.S.T graphs)

{kind=link}

It'll be a long time before I come anywhere close to rotating AXA. The company would have to climb to above €36/share for that to become anything close to valid. But at above €28.5/share, my upside is no longer above 13.5% annualized, and that's where I cap my finance investments for the time being. There's some implied volatility to these investments due to their macro correlation that needs to be accounted for. It's not as stable as some other sectors.

However, if you've followed me here over the past few years and really added to your AXA position during cheap times, you've done extremely well for yourself. It's likely that you're now sitting on a cost basis of below €24 with a yield that's closer to above 7% than below 6.5%. And in this environment, from this company, that is astounding.

S&P Global targets for AXA come in at a range of €28 to €37. You'll note that my PT is far below the average of €34/share they're currently giving the company. I would like to point out though that less than a year ago, that average was below €30/share, with a low of below €23.

Still, 17 analysts follow AXA - out of those, 15 are either at "BUY" or "Outperform"

I agree with the overall sentiment of these ratings and recommendations - I just say that the opportunity here is almost gone.

So, I'm not waiting for 2Q23. I'm adding more shares of AXA at this price to get my position up to my desired portfolio size because I expect that over the next few months, we'll be in a position to regret not investing in the business.

I have proven over many years here on SA that insurance businesses can provide you with substantial returns while also giving you great dividends. Unum (UNM) was my first fully realized such cycle where I covered the company throughout the entire development. I am now doing the same for Lincoln National (LNC). AXA never really fit into that box, because they did not drop as far - but I've shown you over the course of my articles how to beat the market with this sort of investment.

You just can't keep holding these companies when they go into overvaluation - doing so will erode your long-term returns. That's why I also give you my "trim" targets and make articles with clear rating changes when such changes occur.

For now, AXA is a "BUY" - but it's very close to becoming a "HOLD" here.

Here is my thesis for AXA.

Thesis

- This is one of the largest asset managers and insurers in all of Europe and the world. It has rock-solid foundations and a 200-year history. Under the right circumstances and at the right valuation, this company is a definite "BUY".

- I believe that a conservative estimate of the company's abilities calls for at least a target of €28.5/share. This means the upside is now all but gone, and we can look at potentially harvesting profit.

- Based on this, I would consider AXA a "BUY" here, but an extremely weak one.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The company is no longer cheap, and the upside here is less than 1%. Other than that, it's a "BUY", but a very weak one.

For further details see:

AXA: Why French Insurance Has Outperformed But Is Now A 'Near-Hold'