XLI - Axalta Coating Systems Not Quite Reassuring

2023-09-10 06:25:00 ET

Summary

- Axalta Coating Systems' stock price fell about 20% from its 52-week high and may continue to decline due to macroeconomic headwinds.

- The stock has potential to increase by 20% this year, but its high volatility and lack of dividend contribute to a risky outlook for retail value investors.

- Factors to consider for the company's future include the performance of the auto and industrial sectors, Wall Street analysts' ratings, and the company's debt and effectiveness in controlling expenses.

Holding-On

Seeking Alpha and industry analysts have maintained a conservative assessment of paint, industrial coatings, and chemical manufacturers’ stocks this past year. In June, we assigned a Sell rating to Axalta Coating Systems Ltd. (AXTA). Shares were approaching their 52-week high and hit it the next month. The share price fell and is down about 20% from +$33 to $27.41 at the close of the first week in September.

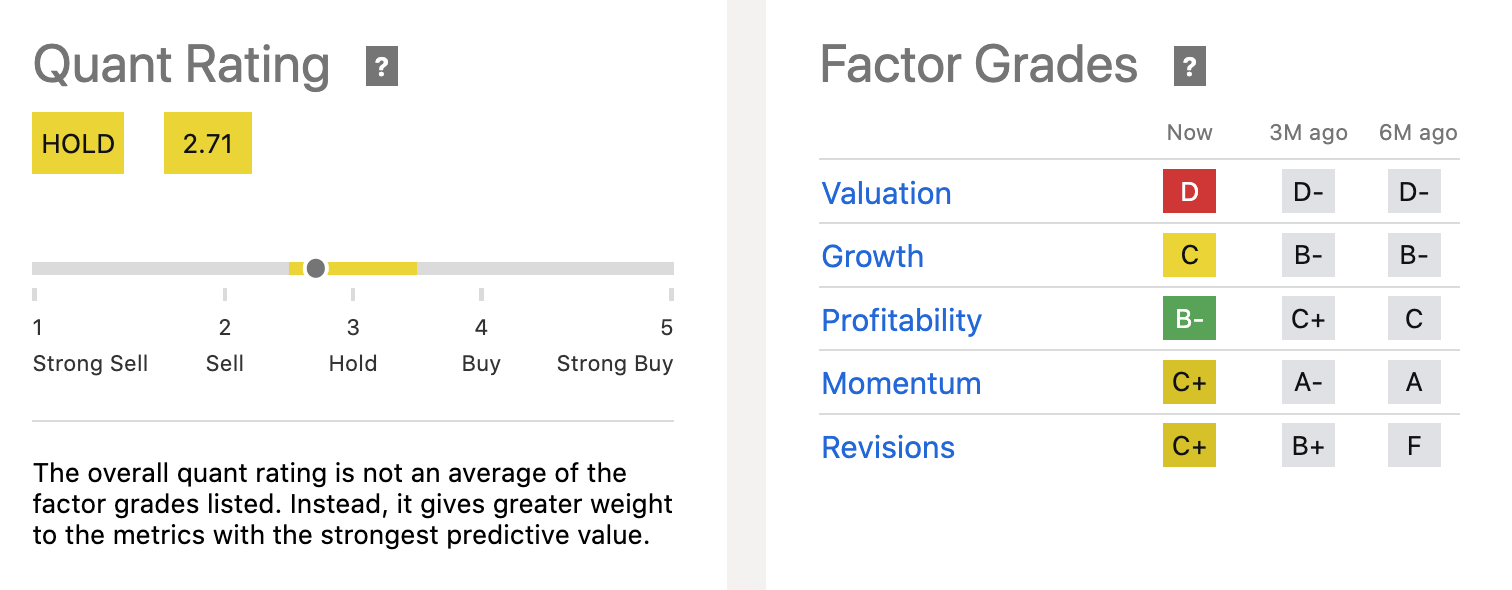

The share price is volatile and macroeconomic headwinds might undercut the share price driving it down another 10% to 15% this year. SA's Factor Grade for momentum is down to a C+. We urge retail value investors to sit tight until we get closer to the Q3 earnings report due on October 24, ’23. This follows a disappointing second quarter of misses from analysts' estimates for the earnings reported on August 1, ’23.

The stock also has an opportunity to pop up 20% into the low $30s by the end of the year. The situation leaves us vacillating between maintaining our Sell rating but we are leaning toward a Hold rating and recognize the viability of analysts taking a more aggressive stance on Axalta shares. After all, the share price is up ~7% YTD. Short interest is steady at about only 2.5%. The PE is about 19, higher than its historical average of 15.4 and lower than the industry average of 28.

Mixed Results

The high volatility of the stock (Beta of 1.32) and lack of any dividend contribute to our negativity. Highlights in the Q2 earnings report include

? Net sales +4.8% Y/Y led by growth in Mobility Coatings; net income rose from $43.6M in Dec ’22 to $60.9M in Q2 ’23.

? Price mix improved 6.8% Y/Y with strong contributions from every end-market

? Volume fell 3.7% Y/Y from production constraints.

? Income from operations climbed $137.6M versus $103.6M in Q2 last year.

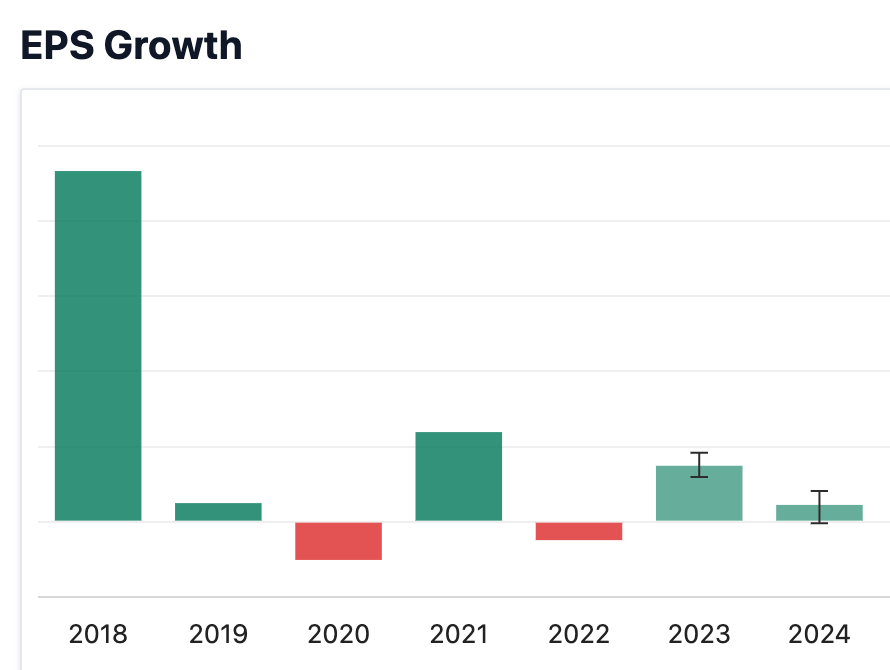

? Earnings and cash flow improved; cash flow from operations of $131.0M in Q2 '23 was markedly better than the -$51.8M in March ’23. Free cash flow was $0.44 per share in June versus -$0.42 per share at the end of the previous quarter but lower than in December ’22 when it hit $0.92 per share.

Improvements in the company financials, i.e. profitability, did not change S A's Quant Rating from Hold. The Factor Grades as a whole are mixed over the last 6 months. The Quant Rating leans toward the Buy-side of ratings in comparison to the Quant Rating tilt towards the Sell-side in June. Valuation metrics improved somewhat with most graded with Cs. Price/Book, Price/Cash Flow, and Price/GAAP languish in the D range grade contributing to our notion the share price might slip further before improving. Without any dividend, there is no rush for retail value investors to be more aggressive at this time.

{kind=link}

Outlook

A lot will depend on the next earnings report if our position is to change; here are four factors to consider:

First, the Industrial Select Sector SPDR Fund ETF ( XLI ) is up almost 8% YTD. This sector will have to continue gaining momentum if Axalta is to enjoy the ripple effects. More impressive is the S A Buy Quant Rating it gets; shares are selling for over $106 near their recent 52-week high of +$111. Nevertheless, news about China’s economy , auto, and industrial sectors is not inspiring.

U.S. domestic auto production, industrial production, and manufacturing output are important to Axalta’s future economic health. The latest report from the Federal Reserve on domestic auto production ruffles us; the report claims that industrial production declined in June and July ’23 and manufacturing output rose just 0.5% in July which does not inspire much confidence.

{kind=link}

Second, 13 of 19 Wall Street analysts have rated Axalta stock as Buy to Strong Buy in the last 90 days despite the company missing their estimates in the last quarterly announcement.

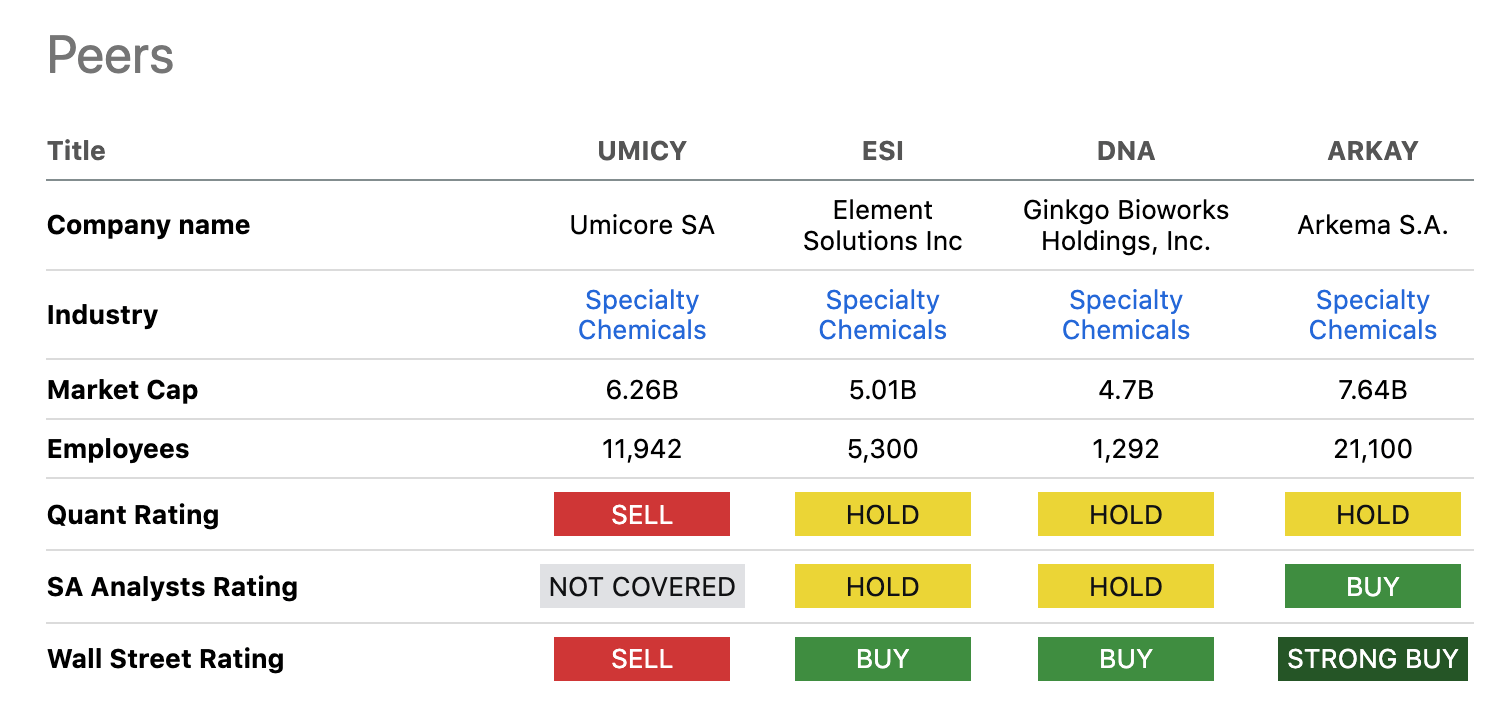

S A’s Hold rating of Axalta’s peers, including companies with bigger market caps than Axalta (~$6B), as Sherwin-Williams ( SHW ), PPG , and RPM make us think the share price is too volatile and conditions in the industry risky at this time to up our assessment.

{kind=link}

A third factor in our assessment of Axalta is its debt of $3.57B. The company holds about $563M in cash and equivalents. The debt-to-equity ratio of about 2.09 is high and that weighs on investors. The free cash flow allowed management to pay down debt in the best and we expect them to do so if revenue, earnings, and free cash flow are stronger in the remainder of the fiscal year. The ratio was 2.78 at the end of 2022.

Finally, more hedge funds bought into Axalta than sold out their positions during the last quarter. Their average purchase price was over $31 per share. Corporate insiders , who own +63% of the shares, sold more often than bought but the number of shares resulted in net activity last quarter. Over the last 12 months, they sold nearly 50K more than they purchased. These numbers do not portend any trend for small investors.

Takeaway

Axalta Coating Systems Ltd operates in an essential sector of the economy. Paint and industrial coatings are like food. If not used today they are in demand tomorrow; vehicles, facilities, and machinery must be maintained or end-up in the dust bin.

Management’s focus “has been to drive improved efficiency and performance across the portfolio businesses” upgrading supply chain and pricing intelligence and optimizing purchasing to keep a lid on prices in order to remain competitive. According to company leaders, “We expect this to provide substantial benefits, which will start to be realized in the fourth quarter.”

{kind=link}

The achievements in Q2 ’23 put the company on the right track for growth and profitability. It reassures investors there is but minimal financial stress on the company. Yet, there are factors we still consider unsettling. We believe there is an opportunity for retail value investors to profit from watching and holding on to the stock and perhaps accumulating shares if the price slips further. For now, we are going to maintain our Sell assessment.

For further details see:

Axalta Coating Systems Not Quite Reassuring