AXTA - Axalta Coating Systems: Share Price Rise Triggers Sell Rating

2023-06-15 05:57:08 ET

Summary

- Sell is our assessment of Axalta Coating Systems Ltd. shares, as the price approaches its 52-week high. Several upside potentials to underpinning a hold or buy assessment.

- There are too many downward pressures including underperformance in two of AXTA's segments and its substantial debt to justify any other performance assessment for retail value investors.

- AXTA stock is highly volatile, and shareholders can be potentially vulnerable.

Sow Or Harvest

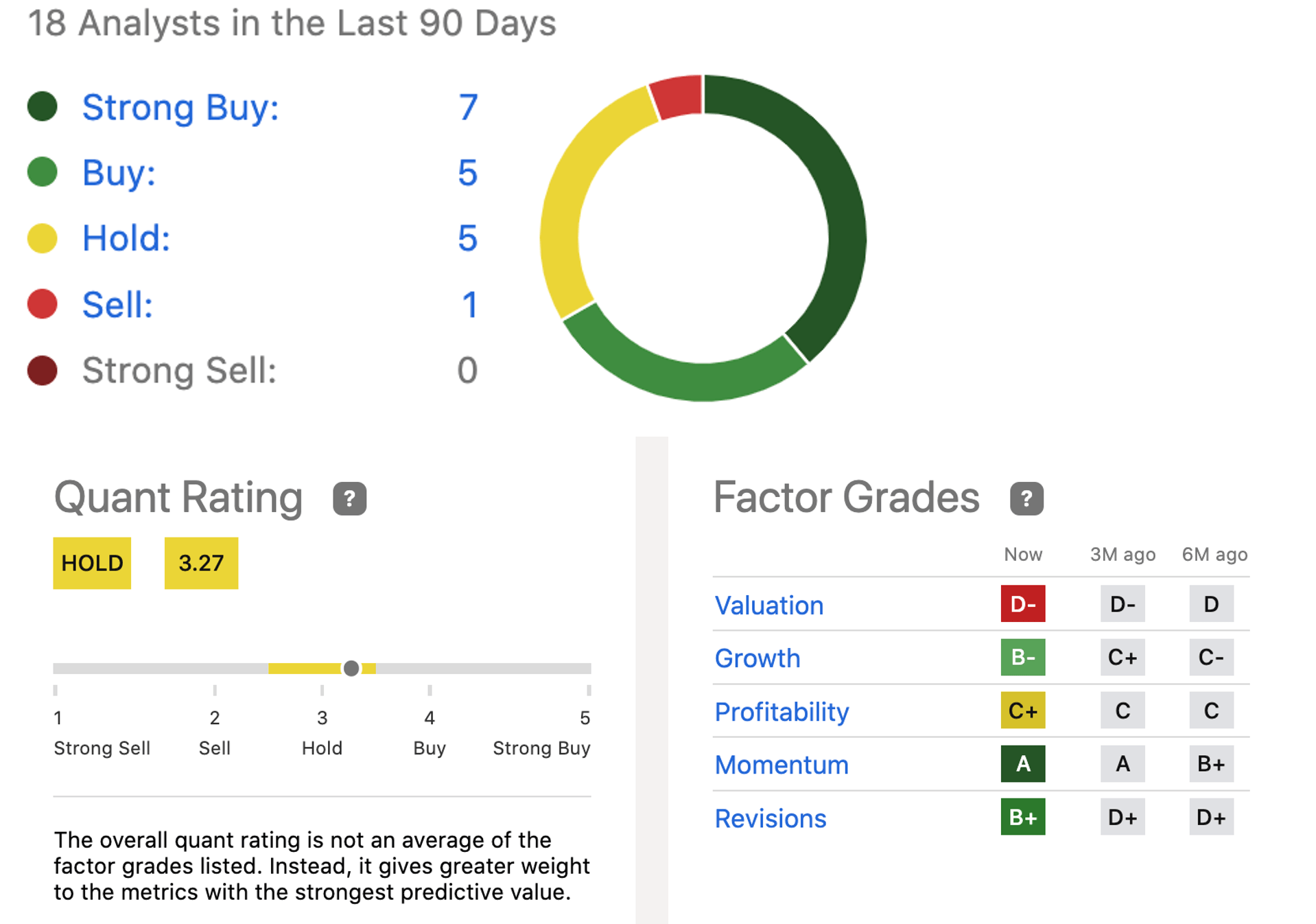

Sell is our rating assessment and rating of Axalta Coating Systems Ltd. ( AXTA ) shares, as the price approaches its 52-week high ($32.88). Neither we nor investors expect a tumble in the share price; short interest is just 2.6% and the Seeking Alpha Momentum Factor Grade is a solid A. But most valuation metrics get Cs and Ds.

We base our assessment on several factors.

- The stock is volatile with a 1.38 Beta rating.

- We do not foresee any substantial long-term organic growth in earnings despite expected revenue growth. Last year's Q2 EPS was $0.41. The consensus for Q2 '23 is $0.39.

- Caveats facing the company include persistent macroeconomic challenges including a possible recession, continuing slowdowns in Europe and China, higher interest lending rates, and competition from behemoth paint and coatings players.

- A long-rumored buyout of Axalta lumbers along after failed moves allegedly by Nippon Paint, Akzo Nobel , and PPG .

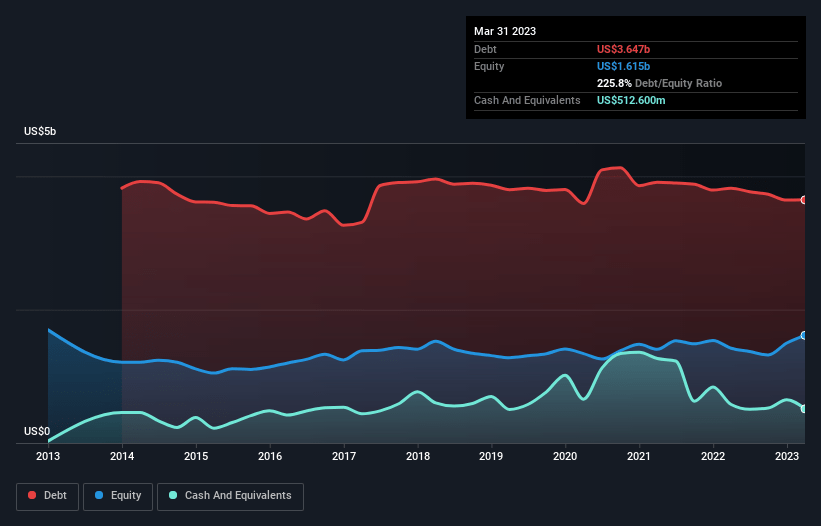

- We deem the capital structure tentative: the market cap is $7.14B, debt is $3.65B, cash and equivalents total ~$513M, and the enterprise value is $10.32B. One analyst recently warned investors to “closely examine whether it can manage its debt without dilution.”

- Another factor includes the wide range of opinions among Wall Street analysts. Seeking Alpha’s Hold Quant Rating primarily tilts to the Sell-side.

- Seeking Alpha assigns incremental increases in Factor Grades for growth and profitability, despite the positive receptions to the last two financial quarterly announcements. Then there is the D- for valuation.

Analysts, Quant Ratings, Factor Grades (seekingalpha.com/symbol/AXTA/ratings/quant-ratings)

{kind=link}

Contributing Factors

The share price has been on an upswing since last October. It has not been so high since reaching a pinnacle in January ’22 when the shares topped $33; they sold for ~$22 by late October that year. Over the last 12 months, AXTA shares are +35% and +27% YTD. Including the current price rise, the stock gained 4.5% over 5 years; that is less than the S&P 500 index inflation-adjusted return of 15.19% purported by Seeking Alpha.

Management qualified the Q4 ’22 earnings announcement, noting two headwinds causing a $30M combined impact. Management and the board chose to exclude the impact from adjusted earnings, resulting in a “fourth quarter adjusted EBIT (of) $147M, 22% higher versus the $121M reported in the prior-year.” The company spent $15M on a cost-saving initiative and another $15M on term loan refinancing.

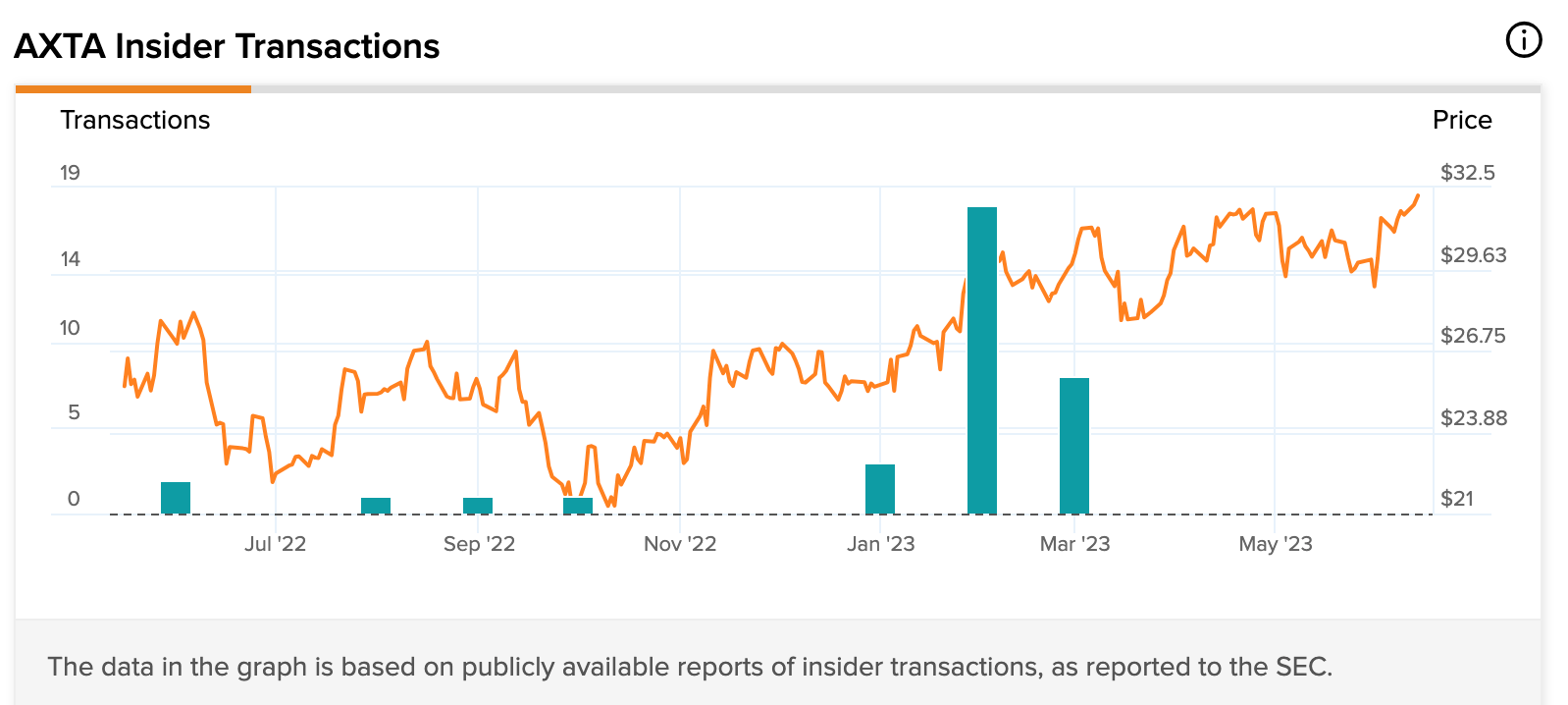

Insider share trades were not unusual in FY ’22. Their buying activity jumped ahead of the Q1 ’23 announcement in May ’23. Corporate insiders bought $1.1M worth of shares in the last 3 months. 40 hedge funds owned AXTA when the price hovered around $24.50 in Q3 ’22. 45 funds owned shares a year later but decreased their holdings by 1.6M shares over the last quarter. These and other institutions own 99.7% of the 239.33M outstanding common stock.

Insider trading history (tipranks.com/stocks/axta/insider-trading)

{kind=link}

Company Profile

Axalta Coating Systems Ltd. manufactures, markets, and distributes high-performance liquid, powder, and electrostatic paint and coatings systems worldwide. Operating through two segments, Performance Coatings and Mobility Coatings, Axalta sells products and systems to repair damaged and new vehicles, for industrial and architectural applications, cladding and coatings for building materials, cabinet, wood and luxury vinyl flooring, and the furniture market. The company was founded in 1866 and is headquartered in Philadelphia, Pennsylvania.

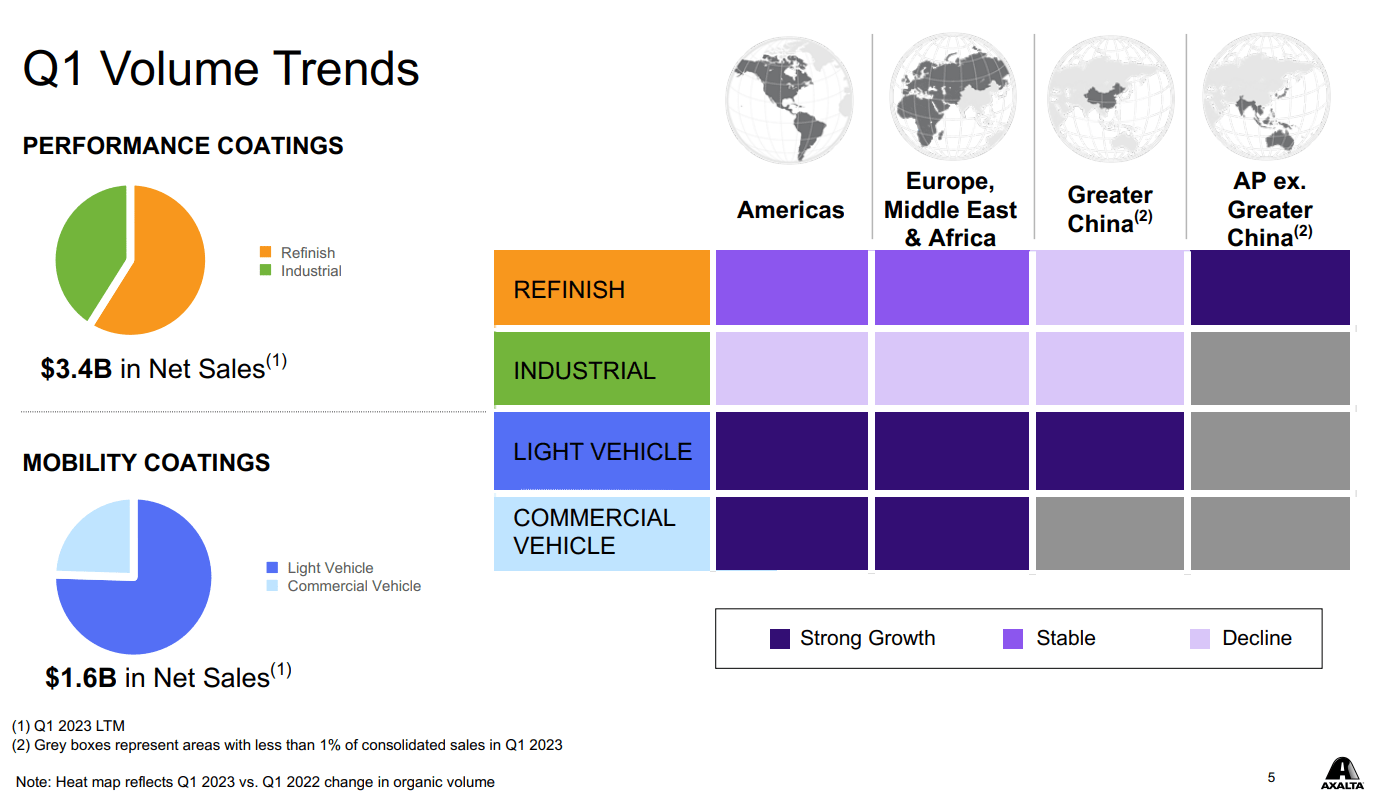

Q1 '23 Volume Trends (repairerdrivennews.com/2023/05/09/axalta-sees-nearly-half-of-9-4-net-sales-increase-in-performance-coatings-segment/)

{kind=link}

Better Past Quarters

In Q1 ’23, Axalta’s Mobility Coatings segment net sales grew 21.4%, while its Performance Coatings slipped 3.4%. The Performance Coatings segment still accounted for nearly half of the 9.4% net sales increase.

There was less industrial activity in Europe and North America, and China’s economic recovery stifled better numbers for Axalta. Near-term sales to the 90K repair shops and OEMs remain a challenge. Its “Body shop customers are still being impacted by parts and labor shortages, which is driving elevated backlogs and continues to strain volume growth.” To diminish the impact, management “increased points of distribution, and expansion into adjacent markets are driving growth in our business and the expected continuation of above-market performance.”

Regarding EBIT, Performance Coatings generated adjusted EBIT of $109.3M in Q1 ‘23 compared to $94.6M in Q1 ’22 with margins of 12.9% and 11.6%, respectively. Refinish segment finished strong. Refinish net sales increased 7.8% Y/Y to $497.6M.

Management told shareholders the company’s higher volume was generated largely from new business acquisitions and inflation in product prices. The company acquired 14 businesses, 3 in the last 5 years. Income from operations for Q1 ‘23 totaled $125.3M compared to $86.3M in Q1 ‘22. Axalta ended the quarter with total liquidity of more than $1B after slightly reducing its debt. Cash used for operating activities was $51.8M, up from $43.9M Y/Y despite deep cost cuts.

Axalta Coating Systems Debt (simplywall.st/stocks/us/materials/nyse-axta/axalta-coating-systems/news/these-4-measures-indicate-that-axalta-coating-systems-nyseax)

{kind=link}

Upsides

As an afterthought, we do not rule out upside possibilities. Axalta's shares have momentum. A host of analysts believe the share price can reach a high of $38 to $40 per share. A review of their positions and media buzz suggests the stock deserves at least a moderate buy appraisal.

For example, the Ariel Appreciation Fund has a positive rating as auto production improves and inflation lessens in 2023. Fund managers expect the company's margins will return to pre-pandemic levels.

On the chance that the company reports an EPS on the high side of estimates for FY '23, i.e., $1.63 each, with a PE of 20.78, the median target price is still stuck around $34. At the extreme high of $2 EPS, the shares might close the year closer to $42 each. Axalta beat EPS analysts' estimates over 8 of the last 9 quarters.

The CEO/President is enthusiastic. The focus going forward is to intensify SG&A cost cuts and inventory reduction (though inventories were +3% at the end of last quarter); supply chain issues and transportation costs plaguing the company and its customers are normalizing. He set the tone for a higher share price in his talk with shareholders, claiming that Axalta will realize:

benefits from market normalization in auto and truck production as well as an increase in body shop activity. We believe considerable market upside still exists in the portfolio. I expect us to continue to outpace end-market growth in mobility and certain refinish markets...

...we have deepened our relationships with many of the fastest-growing EV automakers.

Other factors underpinning a positive assessment of the stock's potential are its 10-Day exponential moving average is 31.35, while the share price is $32.63; the 100-day exponential moving average is under $30.

Takeaway

Three last points. First, Axalta Coating Systems sells to the top 10 OEM vehicle manufacturers. Its body repair shop customers are struggling. Now, word comes that in FY ’23, USA automotive sales are 10.6% better than last year but behind 2021 sales volume. Higher sticker prices and interest lending rates are expected to lower demand. Second, predictions are for a mild recession in 2023, or a deeper worldwide recession next year.

Axalta appears to be using debt to grow, but it might get more expensive. The share price has a high volatility rating. If all the company's segments do not improve in performance, shareholders are, in our opinion, potentially awfully vulnerable.

For further details see:

Axalta Coating Systems: Share Price Rise Triggers Sell Rating