AXTA - Axalta Coating Systems: Some Signs Of Life In The Last Report

2023-12-27 00:37:34 ET

Summary

- Axalta Coating Systems' stock price has risen close to 40% since October, but the last earnings report does not justify a buy case.

- The company trades at a premium to the sector and has lackluster growth numbers, making it unreasonable to buy at the current valuation.

- AXTA's margin has improved, but concerns about shipping expenses and inflation may impact future performance.

Investment Rundown

When Axalta Coating Systems Ltd (AXTA) released its earnings report in early November the market saw the updated and increased outlook by the company as a sign of life after being in a pretty steady decline since July, at least for the stock price. Since the lows in October, the stock price has risen close to 40% and I am asking myself whether or not the last earnings report is enough to justify a buy case here. After looking at the guidance and the current valuation the company trades at I find it hard to make a strong buy case here. The management seems to continue to prioritize investors by spending $50 million on buying back shares, but with only mid-single-digit growth in sales being expected for 2023, I think it's not enough to make a bullish thesis.

The company trades at a premium to the sector based both on p/s and on p/e and combined with what I consider slightly lackluster growth numbers makes it unreasonable to make a buy here. What I would like to see is for prices to go back to the low levels of October because at that point you got a far better entry point in terms of price and margin of safety. For the moment I am therefore rating AXTA a hold, to possibly make it a buy when the valuation makes more sense to me.

Company Segments

AXTA. and its subsidiaries are actively involved in the production, marketing, and distribution of high-performance coating systems on a global scale. The company's operations span across North America, Europe, the Middle East, Africa, the Asia Pacific, and Latin America. AXTA operates through two distinctive segments: Performance Coatings and Mobility Coatings.

Within the Performance Coatings segment, AXTA provides a diverse range of water and solvent-borne products and systems. These offerings are specifically designed to address the needs of various stakeholders involved in the automotive industry, including independent body shops, and multi-shop operators. The Mobility Coatings segment of AXTA business further emphasizes its commitment to delivering cutting-edge solutions in the coatings industry. This segment likely focuses on coatings tailored for a broad spectrum of mobility applications, aligning with the evolving needs of industries related to transportation and mobility solutions.

{kind=link}

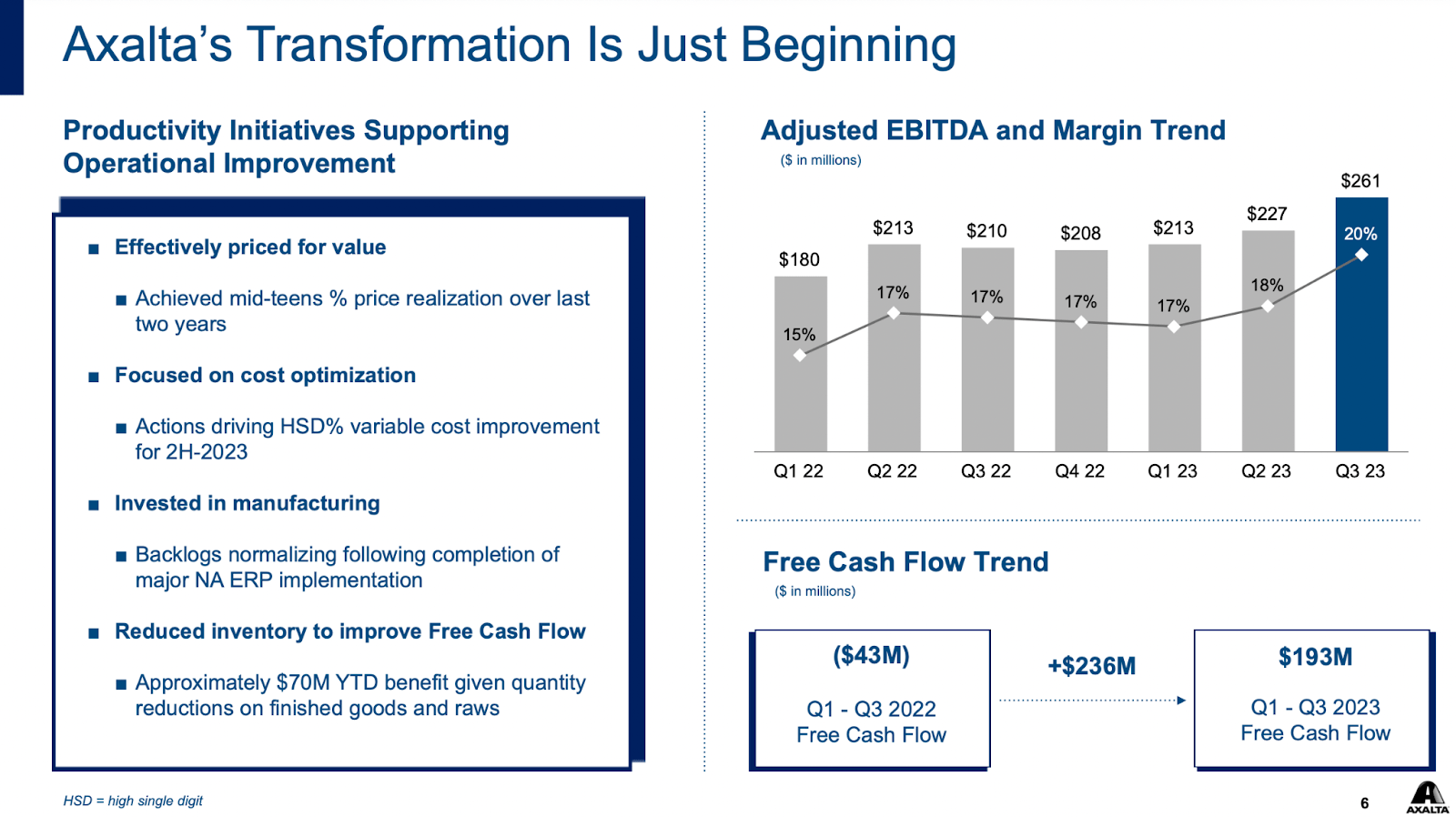

One of the key things that AXTA has been able to achieve in the last few quarters is margin improvements . EBITDA margins sat at 15% back in the first quarter of FY2022. Since then it has improved to 20% and a big factor I think for the stock price jump in the last few months. My concern is about the reliability of these margins. We have seen increased attacks in the Red Sea the last few weeks and I am along with I think a lot of others in the industry worried about the effects of prolonged shipping on inflation. Should shipping expenses rise again then I think it's likely we might see inflation rise and be a reason for rates to be increased again, or potentially stick around at these levels for a long time.

I think however that the partnerships that AXTA is entering are ensuring they will still have viable revenue sources despite potential shipment issues in the short term. One of the key partnerships is with BMW where AXTA has been named the exclusive supplier of BMW Group's private label paint system in around 730 body shops in 15 different European countries and South Africa as well.

Earnings Highlights

{kind=link}

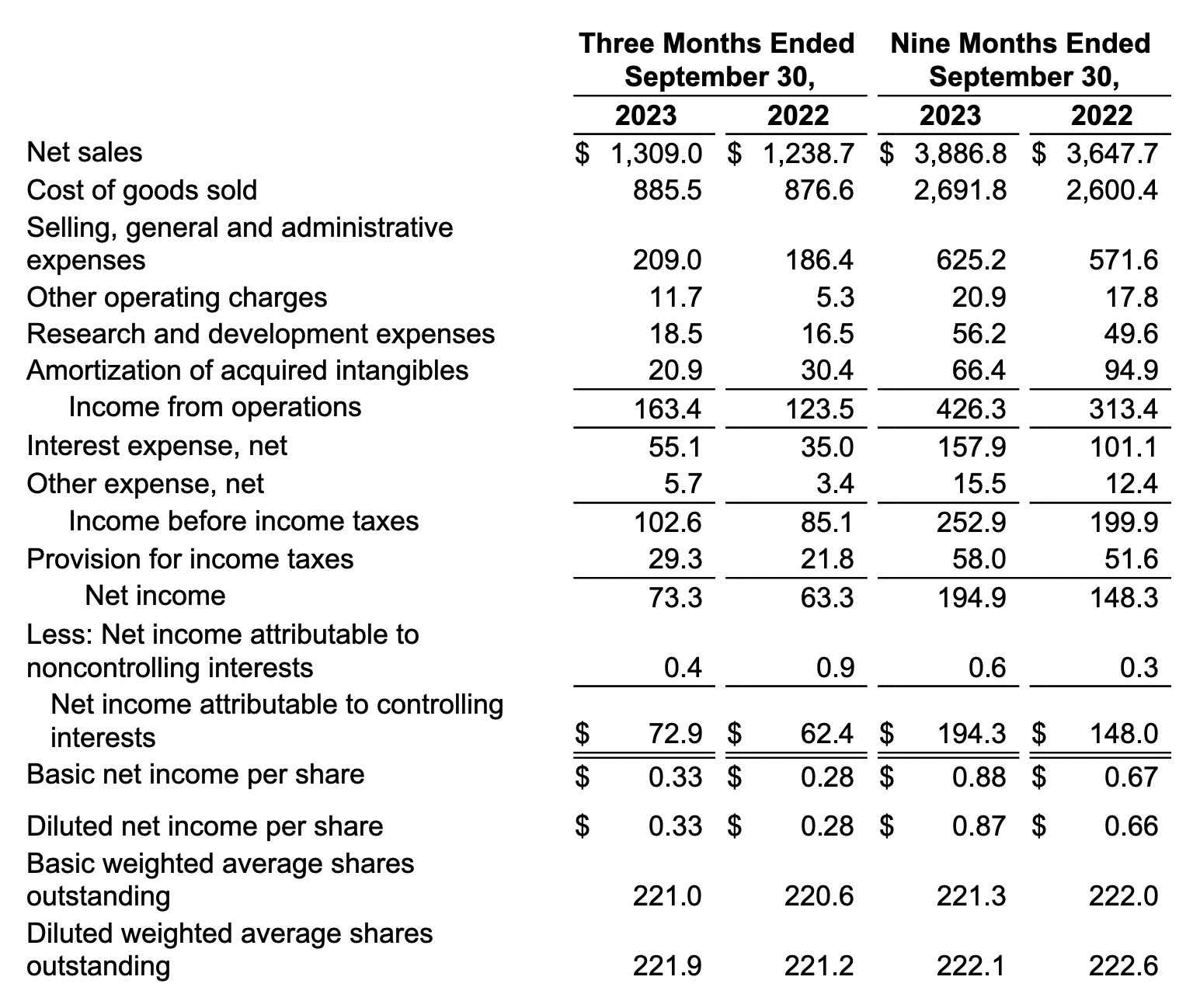

From the last earnings report , I think the market appreciated the improved margins by the company, now sitting at 20% for the adjusted EBITDA. The EPS reached $0.33 for the quarter, an improvement of 17% YoY. The earnings estimate for FY2024 is $1.89 right now, putting it at a FWD p/e of 18. Historically, the company has been trading at a p/e of 18.2, which still is a slight premium to the sector's 17x earnings multiple. I think that we need to see the same trend as the last quarter showcased in Q4 for 2023 and in the first half of 2024 as well. AXTA needs to showcase that they can maintain the margins at these levels and not falter should interest rates, not decline or material expenses rise. With the partnerships that AXTA has entered into, I hope that they can efficiently put some of the expenses on customers and translate that to maintained bottom-line margins. I want to see this executed before suggesting a higher rating here than my hold.

{kind=link}

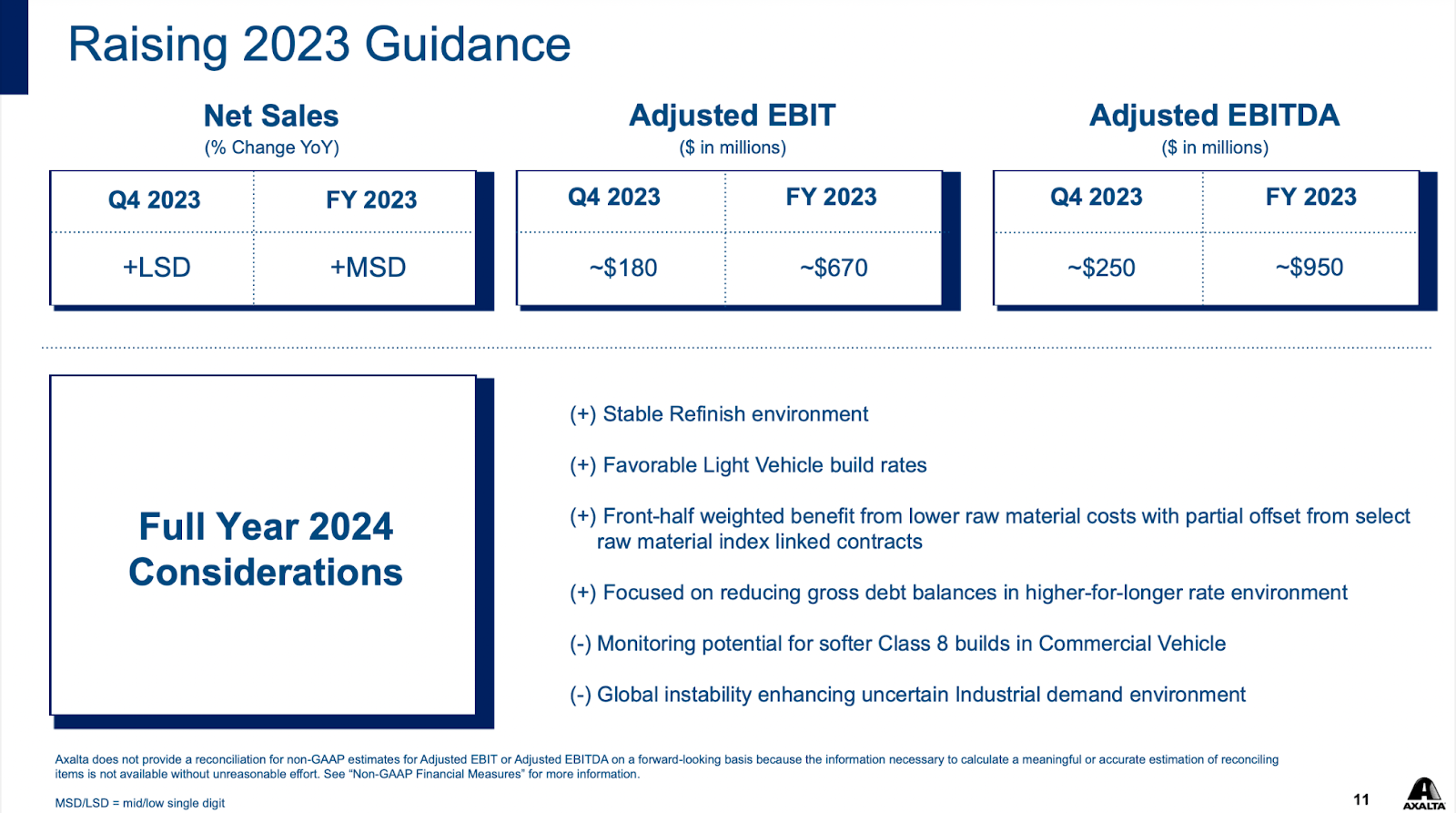

The rising stock price in the last 2 months can be attributed to the positive outlook update AXTA provided. They now see the FY2023 net sales climb by the mid-single digits and EBITDA reaching $950 million in total.

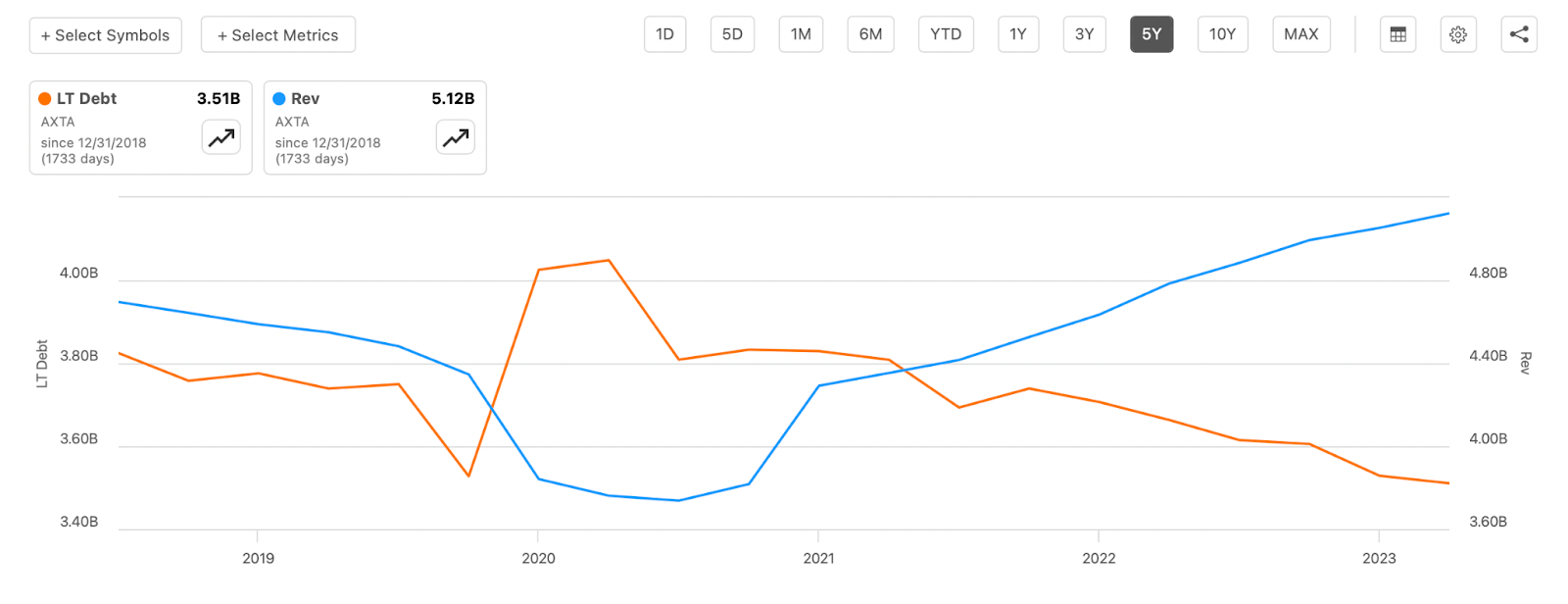

Some of the factors that are contributing to this improved guidance have been a more stable refinish environment and favorable light vehicle build rates too. Demand for vehicles is still on the rise and I think this will benefit AXTA for Q4 and some decent low single-digit sequential sales growth might be visible. Going back to my thesis on the company right now, is still that the uptrend that AXTA seemingly has entered needs to be proven viable. I will decide this whether the company can continue increasing sales and maintain the margins. If the EPS of $1.89 for FY2024 can be achieved depending on the guidance the company provided I might be a buyer instead. Something that would help is lower interest rates seeing as AXTA has $3.5 billion in debt and is paying over $200 million in interest expenses too.

Risks

Over the past several years, AXTA has maintained relatively consistent levels of debt while experiencing a steady increase in revenues. However, a notable concern arises from the observation that the company may not be effectively reducing its debt burden. This raises apprehensions about AXTA's ability to enhance its financial flexibility, positioning itself to navigate environments characterized by higher interest rates, as is the case presently.

{kind=link}

Using debt to fund expansion is not an ad thing necessarily, but there is a limit to it I think. For AXTA to have $3.5 billion in debt and EBITDA of just under $850 million pits them in a strained position I think. It results in a leverage ratio of 4.1 which I think is quite high. I tend to lean much more for something under 3 at least as it provides stability in paying down debts in a timely fashion without having to resort to share dilution instead. Even with the guided $950 million in EBITDA for 2023 it still puts them above my threshold at 3.6. If they can't maintain this and it declines to 2022 results of under $760 million it would make it an even more risky investment and we might very quickly see the same stock prices as in October of this year.

Final Words

AXTA has managed to do quite well over the last several years growing the top line but they are in a pretty leveraged position of 4.1, which is above my preferred range of 2.5 - 3, when we compared EBITDA and LT debt. If interest rates don't decline next year I think the predicted EPS might have to be adjusted downwards and then AXTA doesn't look like such a good deal anymore, unfortunately. I want to see consistent sales growth and a margin maintained above 20% for adjusted EBITDA. Until I see that I will be rating it a hold, with the intention of a higher rating should those points be achieved.

For further details see:

Axalta Coating Systems: Some Signs Of Life In The Last Report