MMM - Axon Enterprise And A Lesson In 50000% Gains

Summary

- While Amazon, Apple, and the like get plenty of talk, there are plenty of lesser-known stocks which have produced equal or greater gains during the past two decades.

- Here we take a look at Axon Enterprise, Inc., best known for Tasers and more recently, body-cams for the police.

- Without hindsight, this was not a surefire investment. There were periods of bankruptcy rumors and major litigation. Yet, a $10k investment 20 years ago would now be worth nearly $5.2M.

- Of course few held through the ups and downs. How can you apply long-term logic to your potential multi-baggers, without being scared out of your positions during rough times?

- In addition to analyzing Axon's current valuation, I'll discuss a microcap name in law enforcement, VirTra, which has some similarities to that of Axon 20+ years ago.

From memory I can't tell you the exact years, let alone exact months, each of the following events happened. Since I was in 8th through 12th grade as I chatted on the now defunct Yahoo Finance and MSNMoneyCentral message boards about Axon Enterprise, Inc. ( AXON ), I can assure you the time period spanned the earliest years of the 2000s. You don't need to cherry pick the buy date for ridiculous gains, but if you bought exactly 20 years ago — January 2003 — you would be up over 50,000% today.

Yet in 2003 and 2004, Axon Enterprise, Inc. was an immensely controversial stock. Many argued, with sound reasoning, it was going to zero.

Before Axon, it was Taser International

They didn't change their name until 2017. From their IPO in 2001 until then, they were Taser International and the ticker was TASR. During the earlier years, the "International' was more aspirational than reflective of actual customers, which were mostly U.S.-based.

Being that it went up over 500x (a 500-bagger!), I know you must be thinking " I'm sure it was some obscure penny stock back then" and that's simply not the case.

The reason you see prices as low as 29 cents on the long-term charting is because of the subsequent stock splits. Axon Enterprise, Inc.'s IPO was at $13/share, or about 56 cents before splits.

Don't assume it was some obscure stock back then, either. TASR traded on the Nasdaq, not OTC, and it was a name you would see frequently brought up on those message boards, CNBC, and the discontinued CNNfn (financial news) channel. A meme stock before such existed. Equivalents today might be names like SoFi ( SOFI ) or Palantir ( PLTR ). To be clear, I'm talking equivalency of how often it was mentioned, not investment equivalency.

A battleground stock

As with today's battleground stocks, each having their own controversy, you had some people thinking TASR was the next big thing while others thought it was a perfect short.

The controversy for TASR was that people were allegedly dying from these "non-lethal" weapons, particularly those with cardiac conditions and/or under the influence of drugs. Here's an excerpt from an AP National Briefing dated 11-6-2004:

NEVADA: RULES ON STUN GUNS - Las Vegas police officers will be banned from using Taser stun guns on handcuffed prisoners and discouraged from applying direct multiple shocks after a department review and two deaths of people in custody. Police officials spent about four months evaluating Taser policy after the February death of William Lomax, who the authorities said was shocked repeatedly while handcuffed.

Even good ol' Johnnie Cochran got in on the action. Before TASR was public, he had filed and successfully settled one of the first wrongful death suits allegedly related for $885,000 in 1995 (yes, the same year he got O.J. Simpson off). That suit was just the start. Then came the Torres case in 2002. From the Madera Tribune :

On Oct. 27, 2002, Torres was shot by Madera Police Officer ed. Marcie Noriega, who said she intended to grab her Taser to subdue Torres and accidentally drew her 40-caliber instead. She fired a single shot into Torres’ chest.

While Cochran was suing the city for that, the city was suing TASR. They argued the design of these weapons meant they could easily be mixed up for a firearm during the heat of the moment:

The lawsuit against Taser International, Inc., an Arizona-based corporation, cites negligence, product liability and breach of express and implied warranties on the part of the manufacturer. That case is also pending in federal court.

That opened the floodgates:

{kind=link}

According to Reuters , from 2004 through 2009, TASR faced an average of 14 wrongful death suits per year. In 2010, once they began using more stringent product warnings, the claims slowed but were still plentiful; a peak of at least 44 in 2009 to at least 31 in 2016.

Reuters identified more than 1,000 incidents in which people died after being stunned by police with a Taser, typically in combination with other types of force. (Emphasis added.)

Put a price tag on each of those and it's easy to envision the company going under.

It is somewhat reminiscent of the nightmare 3M ( MMM ) is facing today, where there are 230,000+ plaintiffs alleging faulty ear plugs made them lose hearing and/or get tinnitus. With some of the first cases resulting in verdict awards of up to $77.5M per person , you have some analysts predicting $100B in losses . Keep in mind 3M's market cap is only $73B and they already have hefty debt. We'll come back to 3M in a moment.

Stealth growth while in danger of bankruptcy?

The bears would have you believe that Taser was on a one-way street to Chapter 11 and indeed, the company's net profit might also suggest the same:

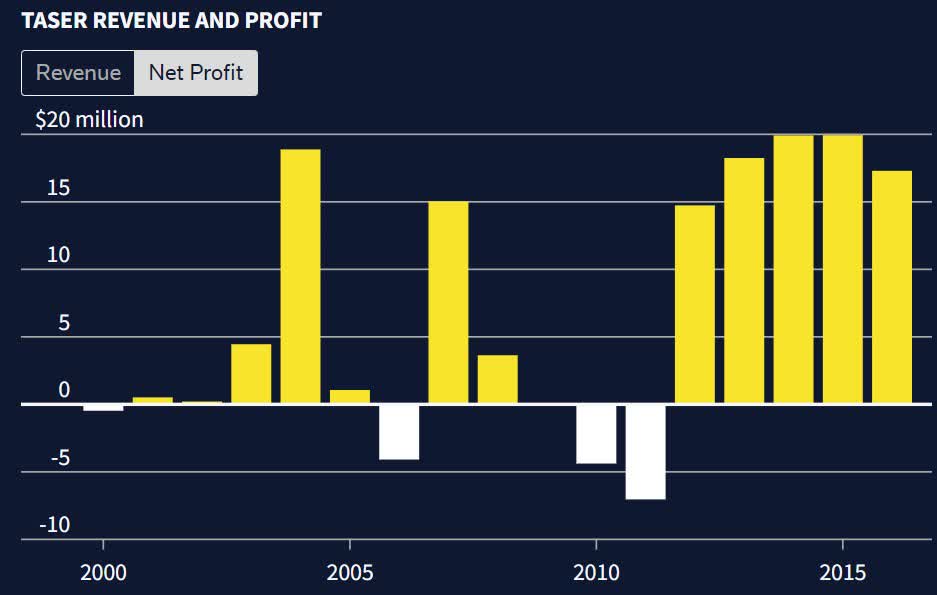

{kind=link}

Hmm... earning the same amount in 2012 that they did in 2004. Net profit of just $15 or $20M a year isn't much of a margin when you have up to 1,000 wrongful death suits, right?

However during this time, they are growing. Just look at their revenue:

{kind=link}

Here's their employee count:

{kind=link}

Last, let's take another look at their share performance only during these years:

A decade-long roller coaster. What was previously a high-flyer in 2003-2005 turns into a toxic stock no one wants to touch.

Yet, if you held through, this would be the result:

That drama between 2005 and 2015 almost looks like a rounding error, in context of where the stock has gone since.

Most things are not as bad as feared

Not just with Taser, but with everything in life. More often than not, the worst does not come to fruition. In fact, usually the bad outcomes we face are not anywhere near the worst-case scenario we conjured up in our mind.

Well, the same applies to Taser and public companies. For every worst case and bankruptcy that really does happen, there are countless others who dodge the bullet, despite what may seem like the bleakest of circumstances.

Perhaps 3M really will go bankrupt and have to pay $275k to each of the 235k plaintiffs. But what if they don't? You get a Dividend King at an unusually high yield of 5%.

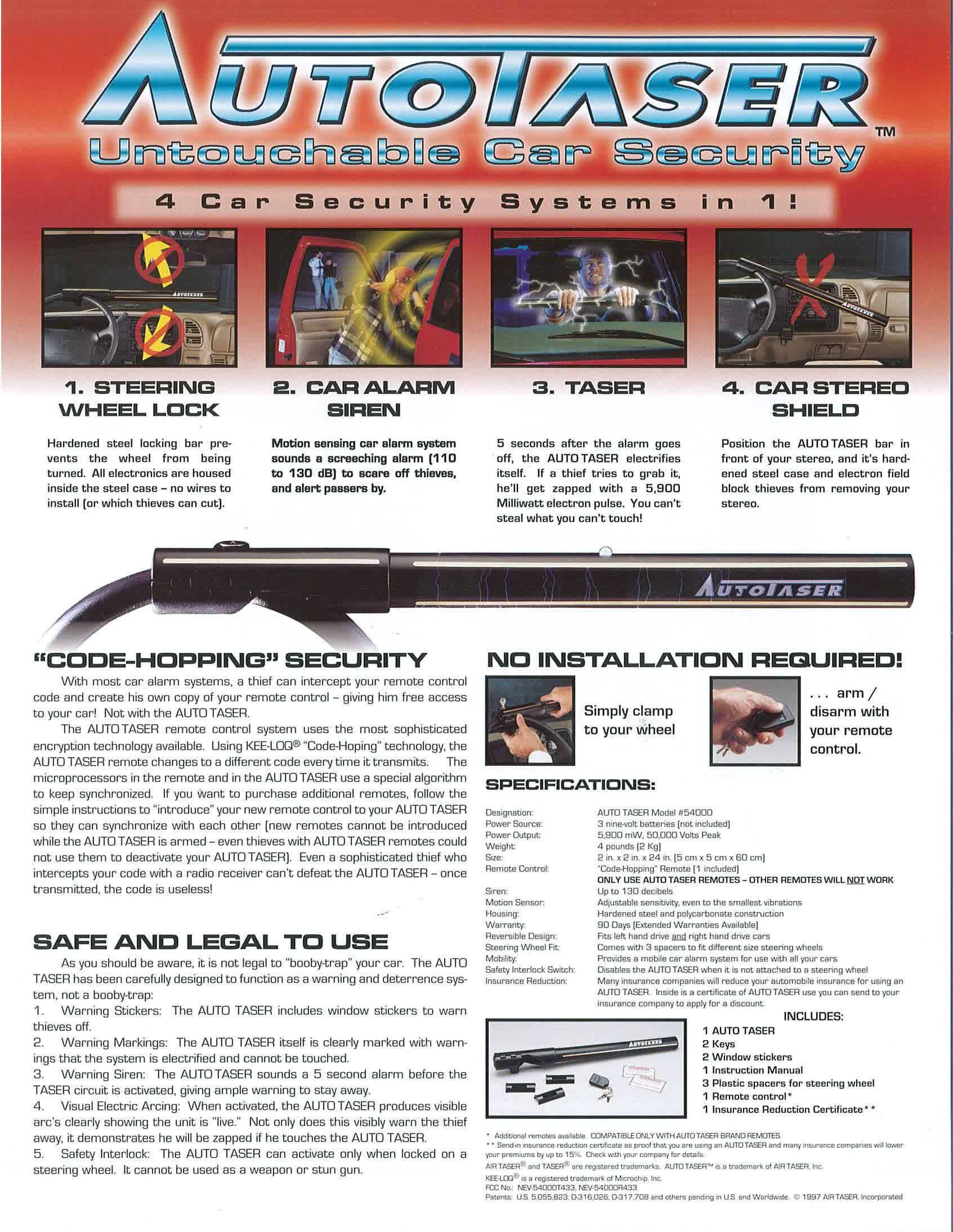

Product pivoting

Did Tasers go away? No, they just became safer, to minimize the odds of accidental discharge and potential effects on the human heart. Yes, settlements were paid, but nowhere near the worst case.

While this was all going on, Taser pursued other products. Not all were a success. They had Auto-Taser, which was basically an electrified version of The Club.

Taser International/Axon Enterprise

{kind=link}

As much as I love the cartoon character being electrified in image #3 above, consumers didn't love the product. Tom Smith, who co-founded the company with his brother, was certain it would be a bestseller, however this is how he described it to the LA Times in 2002 :

'No one bought it,' Smith said, still mystified. 'My brother started calling it the Bearded Lady: Everyone wanted to look at it and no one would take it home.'

Before going public, the article further discusses how three times the company was headed into bankruptcy. Smith said:

From 1993 to 2001, we only had two months where we had the end-of-the-month payroll covered at the start of the month.

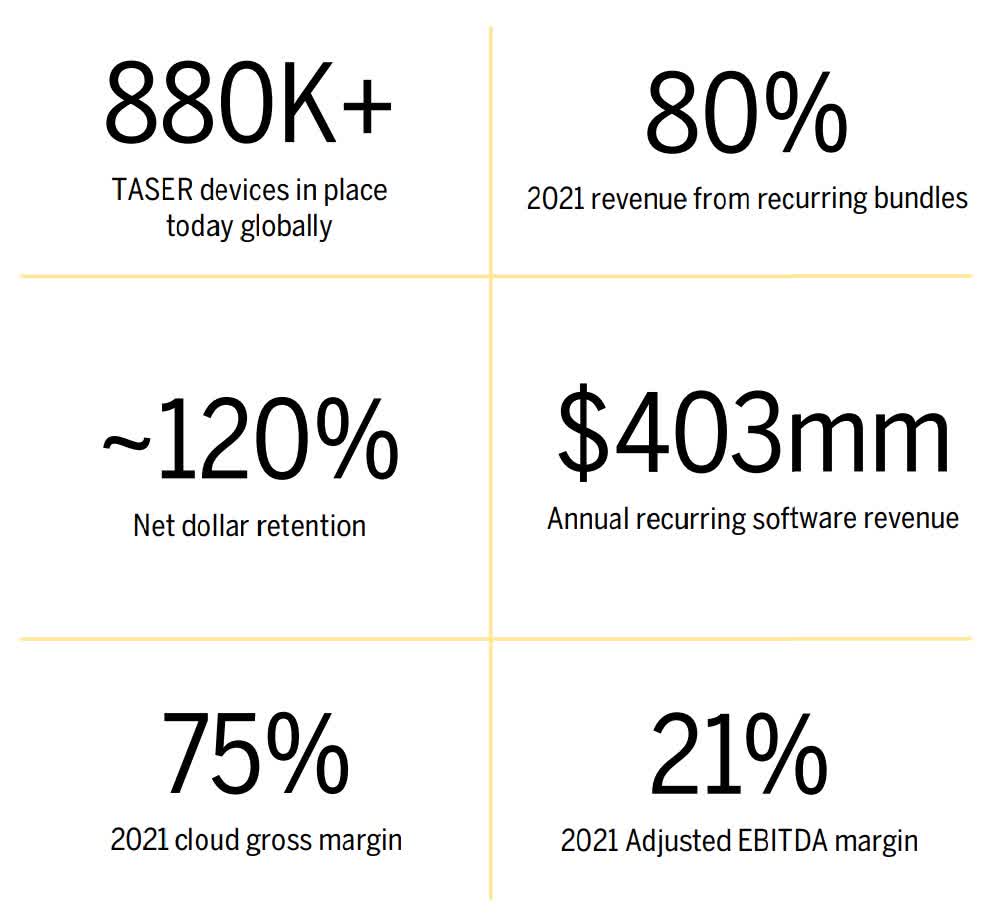

In 2005 they created Taser Cam, which was a grip-mounted camera accessory that was activated once a Taser's safety was dis-engaged. In other words, so the use of the Taser would be video recorded. This eventually morphed into a body cam, in 2008. The footage would be uploaded online, where police departments and others could access footage. Little did they know that this would eventually grow into one of the stickiest Software as a Service ("SaaS") products used by law enforcement today.

Axon investor deck, Nov 2022 Axon investor deck, Nov 2022

{kind=link}

{kind=link}

They were doing SaaS before that buzzword was even born. Their Evidence.com portal, where body cam footage is uploaded, has been in operation since 2008. Here's a look at their stock from that point onward:

So even if you missed the stock 20 years ago, you could have bought it pretty much anytime between 2008 and 2013 — the first 5 years of their subscription service — and you would still have ended up with a 10-bagger, or better.

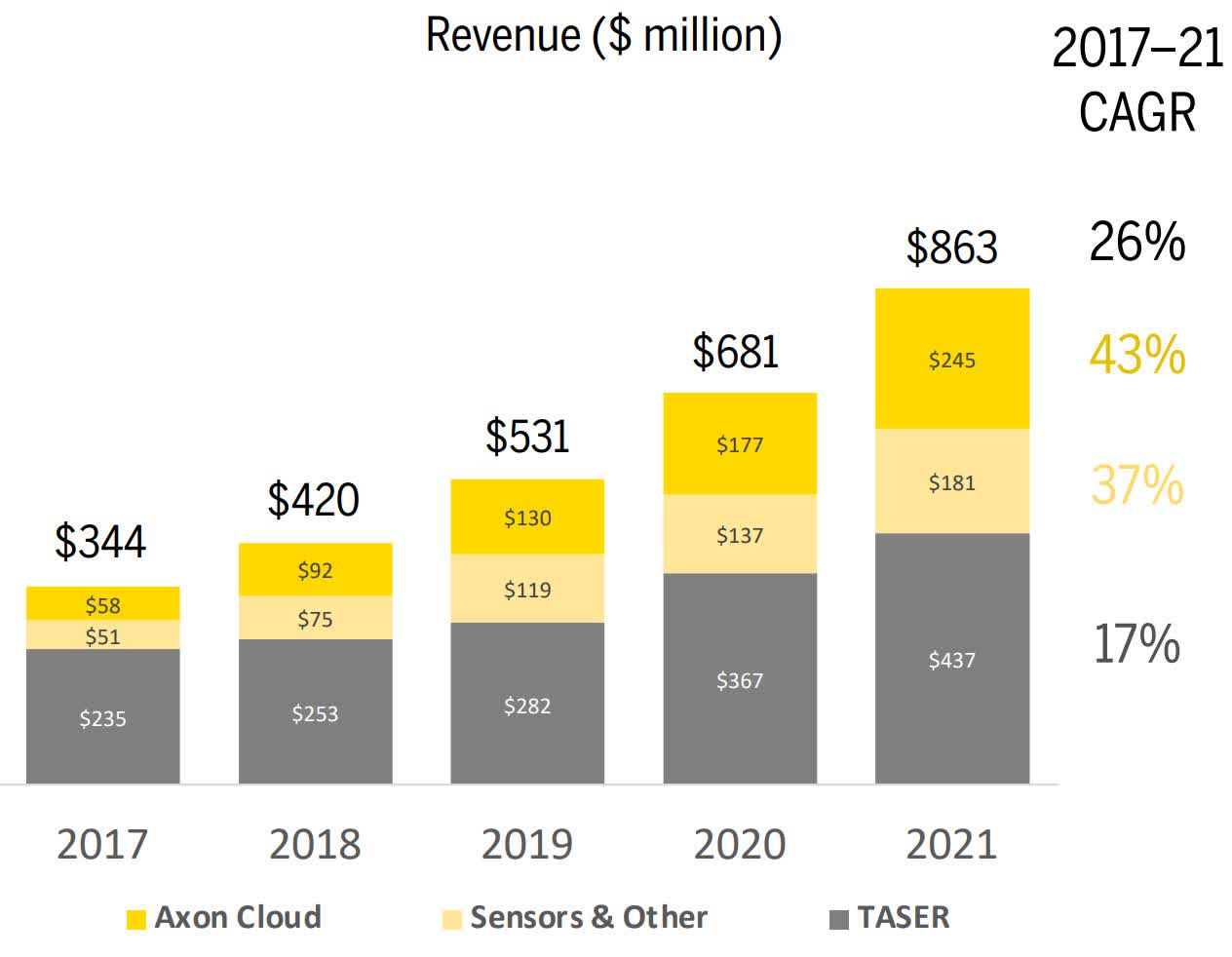

Today, Axon body cams are in use worldwide, with it being omnipresent with most police departments across America. Yes, the Taser guns are great sellers, but it's the body cam cloud business which has really turned this stock into one of the best performers of this century.

That cloud biz has grown at a 43% CAGR the last 5 years, while Taser hardware is only a 17% CAGR. I say "only" not because it's low (it's impressive) but rather, a 17% compounding hardware business will not garner the valuation multiples the stock enjoys today.

Is it too late to get on board?

With an EV/sales of 11.9, Axon Enterprise, Inc. stock by no means cheap. As expensive as it looks though, the forward multiple is 9.2 which is still expensive, but within the realm of reason according to its average multiple the past 5 years. If you go off earlier data, it's about 50% higher versus the average 5-6x it traded at.

That's sales, so what about earnings?

Sorry, I can only take this next chart back 2 years for the numbers to be legible. Prior to that, the P/E spikes into the hundreds and thousands temporarily during Covid.

You can see its EV to EBITDA is the most consistent metric to evaluate. Its very rich 46x, which it presently trades at, is near the lower end of its range surprisingly.

So it doesn't obfuscate the aforementioned metrics, I didn't include FCF. That's sky high at 222 and has been as high as 2,100. Obviously, they're not optimizing for FCF.

Something to keep in mind is that they use 5 to 10 year contracts. They're only realizing 1/5th to 1/10th of contract revenue per year, despite the rest being locked in with very reliable payers (law enforcement agencies). There is no acquisition cost and minimal expense for that customer after year one.

Did I buy 20 years ago? Nope. I fell for the litigation scaremongering on the message boards. I did come very close to buying last July when the price was in the $90s, but I wanted to wait for the $80s, the price is traded at summer 2020. It never got there.

Whether it's too late or not I believe depends on your time horizon. While I personally will not buy here, or anywhere close to here, I have little doubt this seemingly very expensive stock will have a market cap multiples higher in 10-15 years than what it is at today, at just $13B. The question is, what will the share price do between now and then? That is why I'm not buying right now.

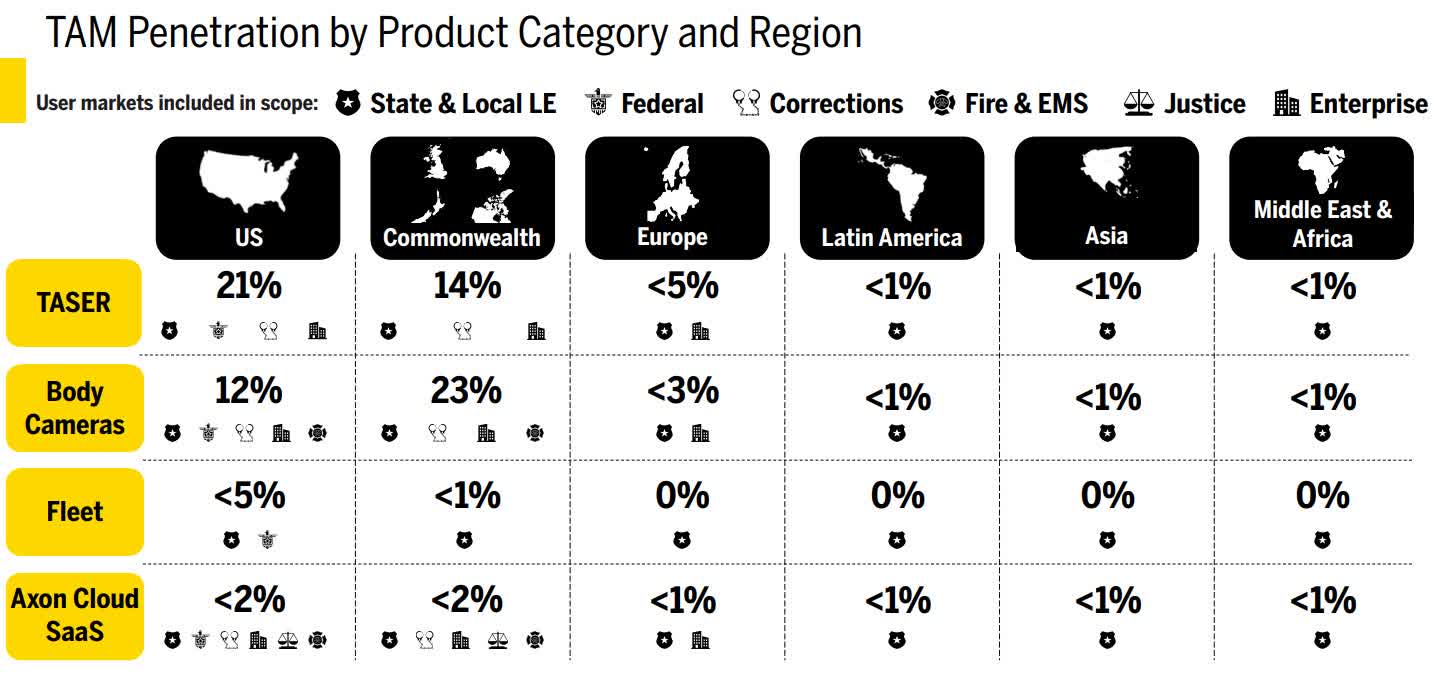

$13B is not a lot when you consider they essentially have a monopoly on police body cams. In our litigious society, these have become de facto for departments. Not just to ensure cops are in-line but also to prove such in court, when claims are made otherwise. Taser guns are also a monopoly. There is not really an equivalent alternative.

{kind=link}

I really hate total addressable markets ("TAMs") because they can be misleading. For example, on the body cam TAM they include Fire & EMS (perhaps some, but it's hard to envision most using them). Regardless, even if you chop down their own TAM projections, they still have a large runway of growth ahead, particularly overseas.

Their goal is to cut gun-related deaths between police and the public in half by 2033. They also count on converting gunowners to Taser owners for self-defense. While both of these are admirable goals, I'm skeptical of success on the latter. At least in America.

The lesson?

Rarely is the road for anything in life a straight line. Twist, turns, and detours are to be expected. Whether it's Axon, Amazon ( AMZN ), Monster Beverage ( MNST ), or another monster gainer, it's almost never predictable from the get-go. Each of these journeys was chock-full of times when all logic would tell you it would be smart to sell. Only those investors who stuck with it, through thick and thin, are the ones who reaped the largest gains.

Of course not all stories are a happy ending. In fact, for every Axon there are countless other companies who floundered and failed. Statistically, the odds are very much against you when it comes to finding just one big winner. But when it works, it can offset many losers. I discuss this math in my recent post titled: "10 Potential 10x Return Stocks For The Next 10 Years." I emphasize potential does NOT mean probable. Most will fail.

While nothing I say is investment advice, I will tell you the methodology I use myself when it comes to growth investing and resisting the temptation to sell, either when times get tough or when I want to lock-in gains. For that, please read this interview I did with my friend: "Buyandhold 2012 Grew $4k To $87 Million, His Advice For You."

VirTra has a niche, can it have more?

In that recent article about potential 10x return stocks, Seeking Alpha user " PatentMan " brought up this company in the comments. It intrigued me, so I dug a bit deeper.

Founded in 1993, VirTra, Inc. ( VTSI ) provides firearms and force training simulators for law enforcement, military, educational, and commercial markets worldwide.

{kind=link}

Here's how they make money:

- Sales and leases of simulators, which range from $150-300k each when purchased.

- Training and support.

- Software customization to create desired training scenarios.

- Accessories such as drop in recoil kits, which convert real guns into simulation ready firearms complete with a realistic recoil.

On that last bullet, I want to highlight an accessory which directly pares with Axon Tasers:

{kind=link}

VirTra’s V-T7 incorporate precision-aligned lasers to for accurate and realistic training of the TASER 7 CEW device. This cartridge features a close quarters twelve-degree probe spread to guarantee true-to-life training experience. This training cartridge uses cross connection capabilities to accurately register top and bottom probe hits for a more efficient training process.

As you see above, they also have OC spray (pepper spray) simulators. Not shown are laser-based 37MM and 40MM launcher munitions for training.

Kind of like how sexual harassment, diversity, and inclusion trainings have gone from obscurity to mandatory in corporate America, police departments are facing their own renaissance. With increased tension between our police and the public, especially since Covid, there's ever increasing training for firearms, de-escalation techniques, and similar.

Because of that, VirTra has found itself in an important growth niche. But it is definitely a niche. Can they pivot and expand to become something more?

As you see, early investors in the company have not fared well. It went public during the dot-com era. But if you bought after the hangover, say the mid-to-late 00's, you have had some very nice price appreciation. Here's a look at their finances from that period onward:

From 2010 to 2020, the dilution was reasonable, yet the annual revenue grew from around $2M to $24M. However during this time EPS went nowhere. If you recall from above, Axon had nearly a decade-long lull in earnings but then again, they were facing litigation expenses.

To be clear, there are more differences than similarities between Axon and VirTra. Both were founded in 1993, yet today one is a $13B market cap while the other is just $56M. That sums up the stark difference in growth!

What makes VirTra somewhat similar to the Axon of 25 years ago is both offering a niche (yet needed) product to law enforcement. Both had a good cottage industry back then. Axon pivoted immediately to consumers, followed by body cams and more. VirTra has not. It still only has a cottage industry, albeit a successful and growing one. Now with decent revenue (relative to company size) will VirTra be able to become something more?

I don't know. The appointment last year of John Givens as co-CEO might be such a catalyst. He sold his prior company of which he co-founded, Bohemia Interactive Services, to BAE Systems ( BAESF ) for $200M. That press release touts Bohemia as "one of the most widely deployed simulation products throughout all branches of the U.S. and allied military forces." From what I gather, he intends for VirTra to target the military, which is currently a customer base they haven't really made inroads on.

I write on Seeking Alpha to bounce ideas back and forth with likeminded individuals. If you follow the company, I would love to hear your insight in the comments below.

An important warning about VirTra stock

VirTra, Inc. is about as small as a company you will find on a major exchange. The average daily trading volume is just 13.4k shares. At $5/share, that's only $67k per day. Thinly traded microcaps like this are highly prone to extreme volatility. They can also become targets of manipulation, which is why I feel it's important to re-iterate what my disclosure says below: I am NOT recommending buying this or any other stock.

Personally, I did purchase 500 VirTra, Inc. shares as a tracking position. This is merely for me to follow and as a motivator for research, as I am more inclined to do deeper research if I have at least something on the line. However, I do not intend to build a real position in VirTra, Inc. anytime soon.

For further details see:

Axon Enterprise And A Lesson In 50,000% Gains