AXNX - Axonics: Attractive Strong Growth Profile

2023-05-12 08:48:10 ET

Summary

- AXNX reported impressive 1Q23 earnings with revenue of $70.7 million, representing a remarkable 46% year-on-year growth.

- The success of Axonics' F15 and Bulkamid products played a significant role in driving their strong performance.

- AXNX raised its sales forecast for FY23, and I expect it to continue gaining market share in the SNM space.

- The company's ability to innovate and develop new products, such as their chargeable Axonics R20 device, positions it well for capturing a larger market share.

Overview

Axonics ( AXNX ) is a medical technology company that specializes in sacral neuromodulation solutions for the treatment of urinary incontinence, fecal incontinence, and overactive bladder. Sales for 1Q23 were above expectations, led by a better-than-expected performance in sacral neuromodulation [SNM] and Bulkamid. Consequently, AXNX increased its sales forecast for FY23 by 200bps to 27%. I am recommending a buy rating as I believe the underlying SNM will continue to grow and AXNX will continue to gain share. Together, they should ensure low-teens revenue growth, which, when combined with margin expansion, ought to yield a manageable high-teens to low-twenty percent growth rate over the medium to long term. The continued outperformance of Bulkamid, the creation of new accounts, and the fruitful outcomes of the DTC strategy should all contribute to market share gains. Growth should be supported by the continuation of the current upswing in F15 and upcoming R20. The current valuation is also relatively cheap if it continues to grow at >20%, as such I am recommending a buy rating.

1Q23 Earnings

Revenue for the period was $70.7 million , indicating a significant growth rate of 46% compared to the previous year. This surpassed the consensus estimate of $64.4 million. The EPS for the period stood at -$0.19, also exceeding the consensus estimate of -$0.29. AXNX also saw its gross margin expanded by more than 500bps to 74.3%.

F15 And Bulkamid

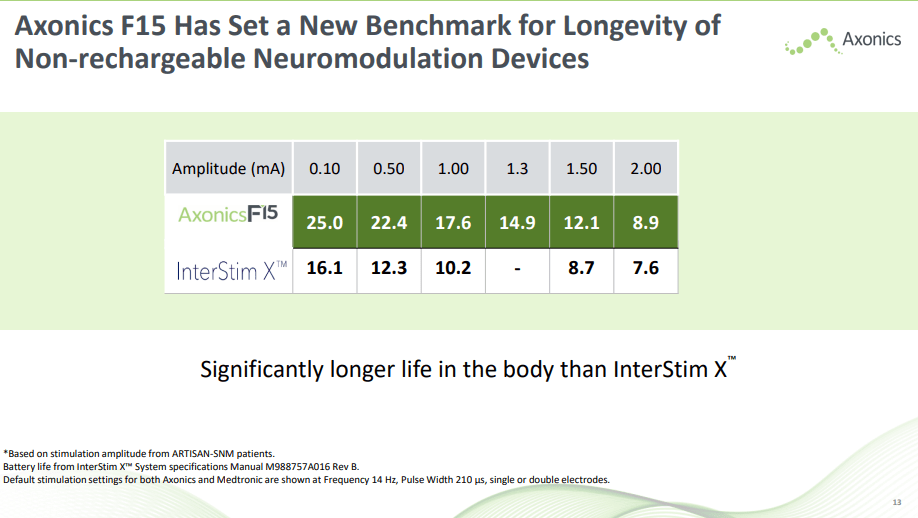

The F15 SNM system has been a constant driver of growth in the SNM market because of its advantages over the InterStim X non-rechargeable system, particularly the significantly longer battery life.

{kind=link}

In my opinion, AXNX is gaining market share from MDT thanks to the F15, and it should be able to keep doing so thanks to the company's propensity for innovation and the ability to develop new products. For instance, AXNX was the first to introduce a rechargeable SNM device (Axonics R20). The rechargeable device is small and compatible with a long functional life of more than 20 years and also reduces the need for charging to once every 6–10 months. I believe this new rechargeable market will allow AXNX to continue capturing share, even though the R20 is still small and the F15 still accounts for most of its sales. In this crucial respect, if the market demand picks up steam, AXNX will have a product lead. Moving on to Bulkamid, the product experienced sustained and robust growth, primarily fueled by increased demand from both existing and new customers. The success of AXNX's DTC campaign, which generated over 10,000 qualified leads per month in 1Q compared to 33,000 in 4Q, should also contribute to the company's overall growth.

Raised Guidance

AXNX has increased its sales guidance for FY23 from $342 million to $348 million. Given the tough comparisons the company faces after lapsing the launch of its F15 rechargeable device, management has reaffirmed its forecast for low to mid-20s SNM sales growth through the rest of 2023. I think the moderation in SNM sales growth due to tough comps is fair, but I think the gross margin expectation here seems too conservative given the strong start to the year. I find management's forecast of a 100-bps improvement in gross margin for FY23 to be conservative. That said, this conservative strategy, in my opinion, allows AXNX to keep beating guidance/estimates and releasing positive guidance revisions, which in turn pushes up consensus estimates.

Radian Acquisition

After acquiring Radian , AXNX intends to use the firm's X-ray technology to facilitate needle insertion and lead positioning during peripheral nerve evaluations [PNE]. I believe this acquisition will help AXNX place PNE lead more quickly and precisely. Ultimately, I believe that more people will undergo SNM because of the increased patient and physician satisfaction that can result from using this technology. However, the effects won't be seen until the 2H24 it gains FDA approval and go on sale.

Valuation

Because AXNX is not currently profitable, the best way to value it is through a revenue multiple with an opinion on what long-term earnings the company should trade at. At the current valuation of 6.3x forward revenue and a possible net margin of 25% to 30% (74% gross margin - OPEX assumption of 35% - tax), AXNX trades at 20 to 24x long-term earnings. When compared to a large mature medtech company like Medtronic ( MDT ), AXNX trades at a significant premium, but I believe the premium is justified because AXNX is growing significantly faster than MDT at the moment. I should mention that AXNX's gross margin is expected to increase further, so the net margin could be much higher (pushing implied long-term earnings multiple down).

Conclusion

AXNX exceeded expectations in 1Q23 with a revenue of $70.7 million, growing by 46% compared to the previous year, notably, gross margin also expanded to 74.3%. The success of their F15 and Bulkamid products were the key drivers of this performance. AXNX also raised its sales guidance for FY23 to $348 million and is expected to continue gaining market share in the SNM space. The current valuation also seems cheap when we take into the growth and a mature medtech company multiple. Overall, I recommend a buy rating for AXNX based on its robust growth potential and attractive market position.

For further details see:

Axonics: Attractive Strong Growth Profile