AXNX - Axonics: Fundamentals Remain Constructive For Intelligent Investors

Summary

- Axonics presents with robust fundamentals and unit economics around its sacral neuromodulation segment.

- The company confirmed FY22 numbers above consensus, guides to FY23E revenues above the Street as well.

- Shares attractive given top-line growth rates, current sales multiples.

- Net-net, reiterate buy.

Investment Summary

Active management of equity portfolios has become absolutely paramount for intelligent investors in the current investment landscape. It is essential for those concentrated in equities to maintain a tactical grasp over their allocations in order to protect the downside, whilst positioning against selective opportunities that offer uncorrelated alpha potential.

With that in mind, as a specialist healthcare investor, it's equally important to understand and get the 'theme' right. We play several thematics in this space, one being centred around urinary incontinence. Specifically, we are long several names making breakthrough's in the prostate surgery domain [with prostate surgery often associated with poor outcomes for urinary incontinence] and have seen reasonable upside across the basket over the past 6-months. Check our extensive publications on each here:

– PROCEPT BioRobotics ( PRCT )

– Profound Medical ( PROF )

– EDAP TMS S.A. ( EDAP )

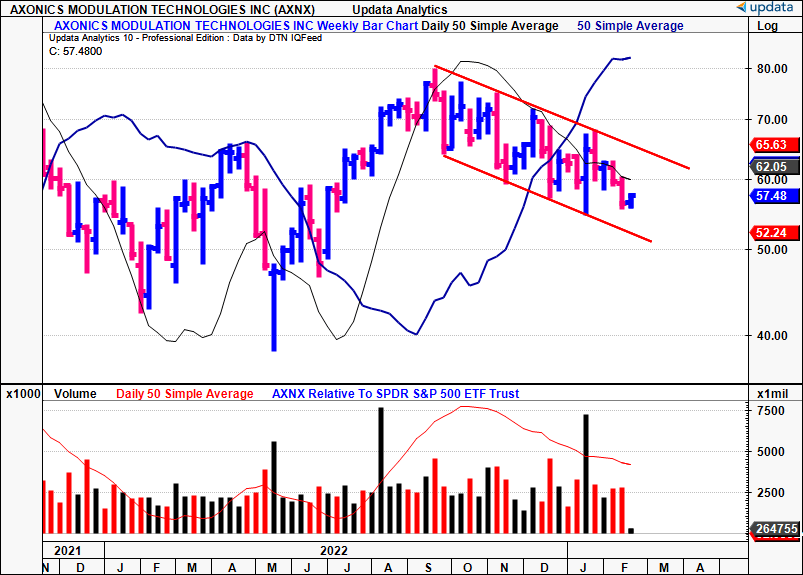

Extending the reach we are back covering Axonics Inc (NASDAQ: AXNX ) today. AXNX has now firmly broken to the downside since our last two publications [Figure 1]. Investors have been net sellers of AXNX stock, and the company currently has ~7% short interest of its float. Question is, does this impact the investment thesis or not? Being fundamentally orientated investors, we remain constructive on the long-term prospects of the company, notwithstanding its propensity to create a medical breakthrough in the otherwise complex segment of incontinence. Hence, the short-term machinations of the market don't change our long-term view. Net-net, after analyzing the company's unit economics in greater detail, we retain AXNX as a buy at 10–13x forward revenues. Read on for more details.

Before doing so, I encourage you to check out the last 2 AXNX publications here:

Fig. (1)

{kind=link}

Data: Updata

AXNX fair view of fundamentals

As a reminder, and most important to this report, AXNX's primary insulator is its implantable sacral neuromodulation ("SNM") device. Unlike the current standard of care for incontinence [surgery, physiotherapy, etc.], SNM stimulates the sacral nerves [including the cauda equina] that regulate bladder and bowel function. Ultimately, the SNM implant offers a completely differentiated method to solving the complex issue of urinary incontinence. It's worth noting that AXNX's second segment, Bulkamid, is equally as beneficial to those suffering urinary incontinence, acting as a bulking agent to prevent bladder leaks. We are most concentrated on its SNM segment, however. To sell SNM units, AXNX operates a DTC sales model, moving unit volumes directly through providers [urologists, urogynecologists, and colorectal surgeons], in the U.S. and EU. Hence, growth and unit economics are dependent on the uptake of its products, growth in end-patients, reordering rates from existing accounts, plus acceleration of new accounts from providers. Importantly, AXNX also gives support to both patients and providers post-surgery, adding a tail of revenues from each implant.

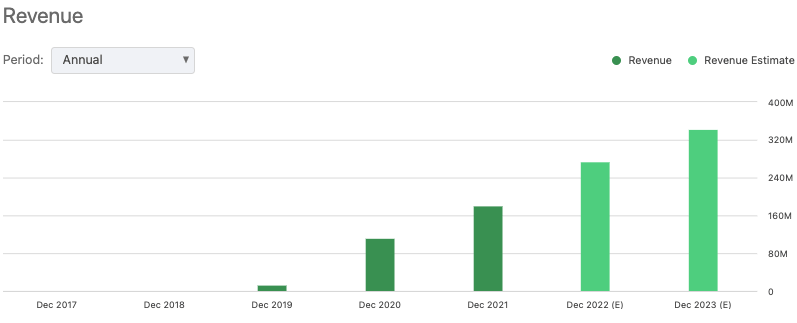

AXNX has grown top-line revenues sequentially since Q1 FY19 to its last report, but hasn't yet turned an operating profit, even when capitalizing its R&D investments as an intangible asset on the balance sheet. Nevertheless, AXNX is investing heavily into future growth and this is reflected in three obvious ways: 1) Sequential growth in R&D; 2) Reinvestment of available cash flows [inc. cash obtained from external financing] into growing top-line revenues; 3) Gross margin decompression over the last 4-years to date to 70%, above the industry. Using TTM numbers, the company has generated a cumulative $1.55Bn in sales, and invested an additional $394mm in capital, including R&D. Hence, we estimate that AXNX has reinvested ~25% of cumulative revenue toward additional tangible and intangible capital for future growth over the FY20–22 period.

Fig. (2)

{kind=link}

Data: Seeking Alpha, AXNX

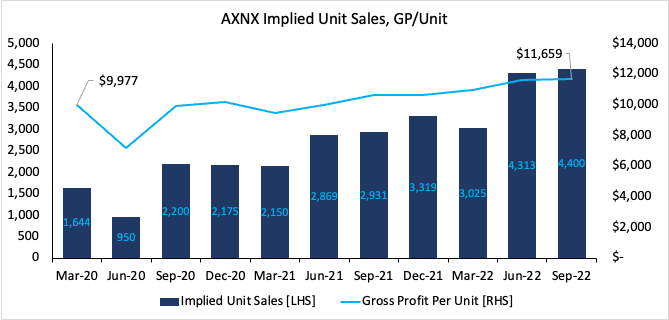

Looking at this in further detail, revenue and gross profit upsides have been driven by uptake in SNM volumes. In its last report, it booked a record $57mm in SNM turnover, reflecting a 42% YoY growth schedule, securing $148mm in SNM revenue volume from Q1–Q3 FY22. The unit economics are important here:

- Each unit is sold for ~$16,000 per management, hence, it had more than 9,200 SNM implants in situ across the first 3 quarters of FY22, 3,562 in Q3 alone.

- Next, it confirmed FY22 SNM revenue growth of 41% YoY – above consensus – calling for $222mm in contribution. Q4 SNM top-line is expected at $70.4mm.

- Presuming no cost increases, this implies that 13,875 unit sales across the entire year for FY22. It also implies AXNX sold 4,400 units in Q4 FY22.

- Subsequently, it realized a 50% YoY growth in FY22 SNM unit volumes and a 23.5% sequential growth from Q3.

- If it holds a 70% gross margin, the gross profit per unit is $11,600 on these numbers for FY22, up from ~$10,000 3-years ago.

Hence, the growth curve over the past 2-years to date on a rolling quarterly basis has been one to take note of, both in terms of unit sales and gross profit per unit [Figure 3].

Fig. (3)

{kind=link}

Note: Assumes constant $16,000/unit price with no price increases or decreases, quarterly data presented. (Data: Author, using data from AXNX SEC Filings)

AXNX growth route looking ahead

Subsequently we estimate that AXNX has a clear path of growth ahead of itself. Most importantly, the optionality means it can 1) continue growing unit sales; 2) push for price increases to increase the profit per unit; 3) continue innovating around its SNM segment; and 4) reinvest into new R&D to drive profitability down the P&L. Regarding point 3, we've already seen the FDA approve the company's 4th generation SNM unit in January.

Further, the sacral nerve stimulation is a high growth market, with various market forecasts pointing to 12–14% geometric growth into FY30. A big lever driving the market is the ageing population, with a large substratum of this populous diagnosed with urinary incontinence. Moreover, urge incontinence is expected to be the main segment leading the market's growth into the future. Strategic Market research cites additional research from 2019 noting "the prevalence of urinary incontinence in postmenopausal women aged 45 to 90 years was around 26.47%" . These points bode well for AXNX in several ways. Mainly the fact that its SNM device is clearly indicated in resolving urge incontinence. The recently approved 4th gen SNM unit also has a functional life in the body of 20 years, offering a long-term solution for patients impacted by the condition. Second, unlike the companies we listed earlier, that focus on improving outcomes following prostate cancer surgery, AXNX's offerings target both male and female populations, and don't have to require a previous cancer diagnosis, or prior surgery to be a candidate. This widens up the addressable market substantially. In addition, compare the market forecasts to AXNX's top-line growth percentages – 12 to 14% per year for the market, versus the 41% in AXNX's YoY revenue growth rates, notwithstanding the 54% growth forecasts for FY23. Subsequently, it's not unreasonable to ascertain that AXNX is obtaining additional market share at rapid speed.

Valuation and conclusion

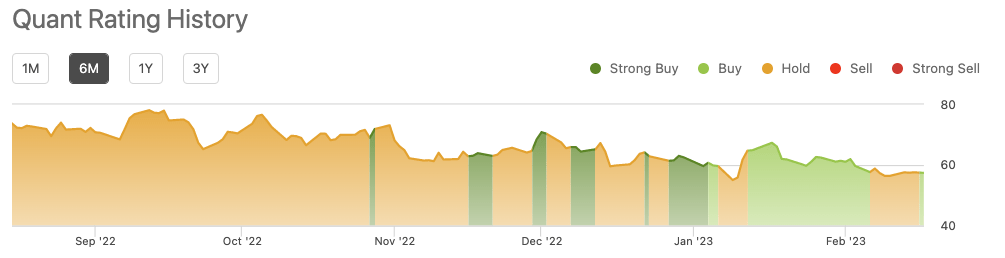

At ~10x forward sales , buying AXNX stock today presumes that we expect the company to multiply its future sales by that amount at some point into the future. That's a $2.2Bn top-line based on its FY22 revenue numbers, roughly in-line with its current enterprise value. Taking a 10-year horizon, we'd expect revenues to reach an average 25% compounding growth rate into FY33 to achieve this. The question one has to ask, can AXNX grow its top-line at CAGR 25% over the next 10-years? We believe it can. Assuming its growth curve flattens as the company itself expands, this isn't an unreasonable expectation, considering 1) forward top-line YoY growth estimates of 54% in FY23E; 2) AXNX's top-line momentum to date; and 3) the unit economics outlined above. Hence, we'd be prepared to pay 10.4x sales today, valuing the stock at $71 on FY23 company revenue estimates, leaving a price gap of 26% at the time of writing. In fact, we're happy to pay up to a 13x forward sales multiple, which values the stock at $86, as discussed last time. The buy rating is also supported by a recent buy call from the quant rating system here at Seeking Alpha [Figure 4]. Net-net, we retain AXNX stock as a buy.

Fig. (4)

{kind=link}

Data: Seeking Alpha, AXNX, see: "Ratings"

For further details see:

Axonics: Fundamentals Remain Constructive For Intelligent Investors