MDT - Axonics: Growing Duopolist With Superior Product And No Debt

2023-09-07 08:27:07 ET

Summary

- Positioned as one of two companies in an underserved healthcare segment with recession-resistant demand for its services and a better product than the legacy monopolist.

- Strong historical revenue growth while still in the early stages of company maturity and poised to continue to take market share.

- Demographic tailwinds from an aging population and increased pelvic dysfunction awareness through an aggressive marketing campaign.

- A safe balance sheet with zero debt and large cash balance provides a shield against liquidity risk that is uncommon for a small cap stock in a rising rate environment.

- We are initiating coverage with a strong buy and a long position. We believe that this stock could easily return +30% by even just returning to prices from last year.

Editor's note: Seeking Alpha is proud to welcome Three Forts Capital as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Thesis

We believe there are many signs of an impending recession in the next 12 plus months due to the inversion of the yield curve and delayed effects of the Federal Reserve's aggressive tightening policies . Therefore, when looking to deploy capital for a long position, we look for companies that demonstrate recession-resistant demand and a strong balance sheet. In general, we believe that well capitalized, non-discretionary healthcare companies will outperform the market over a recessionary cycle.

Axonics ( AXNX ) safely meets and exceeds these criteria. We see tailwinds for demand due to increased patient awareness, an aging population, and the reimbursable nature of its revenue (money not necessarily coming out of the pocket of a consumer in a recessionary environment). The company is also ideally positioned in a rising interest-rate environment thanks to its zero-debt balance sheet. We further see near-term catalysts in the form of beneficial patent litigation outcomes against the entrenched monopolist , continued market share growth on a quarter to quarter basis, and increased operating margins through benefits of scale and increased business maturity.

Company Profile

Axonics is a US-based, global medical technology company founded in 2012 and launched commercially in 2020. They specialize in devices and treatment options for overactive bladder ((OAB)), fecal incontinence ((FI)), urinary retention, and stress urinary incontinence ((SUI)). Axonics's sacral neuromodulation ((SNM)) division features devices that have quickly rivaled the incumbent monopolist, Medtronic ( MDT ). In 2021, Axonics acquired a UK-based company, Contura with its leading product Bulkamid. Bulkamid is a bulking agent used for the treatment of female SUI and held 80% of the market share for bulking agents in 2022. In April 2023, Axonics also acquired Radian LLC and plans to use the newly acquired technology to improve the nerve evaluation lead placement for their SNM devices once they gain FDA approval (targeted roll-out date of mid-2024). This new technology will make the overall device placement process safer for patients and easier for providers.

Source: Company filings

Market/Sector Opportunity

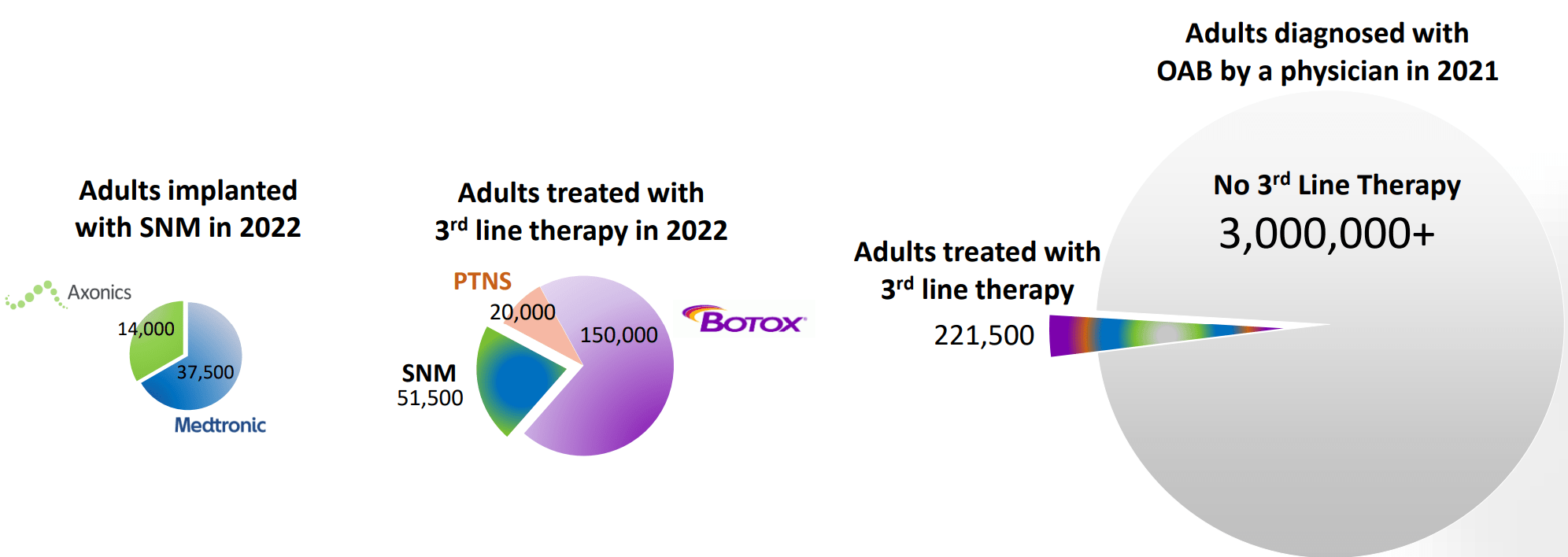

The SNM device market is anticipated to increase by a compound annual growth rate ((CAGR)) of 11.99% by 2028, according to market research from DelveInsight. This is largely due to the increasing risk factors associated with pelvic floor dysfunction such as: prevalence of neurodegenerative disease (specifically Alzheimer’s), obesity, a growing geriatric population, and other chronic diseases. According to Definitive Healthcare ( DH ) claims data, Axonics held 27% of the SNM market share in 2022.

Source: Definitive Healthcare claims data and company estimates

{kind=link}

The even greater market opportunity is that SNM as a whole only held 23% market share of adults treated in 2022, with Botox historically being the predominant treatment choice. However, a study from 2017 published in Neuro Urology Monthly points out a high rate of discontinuing treatment for Botox users due to "insufficient effect, the need for clean intermittent self-catheterization, and urinary tract infections", which see as a reason for continued growth in market share. Zooming out even further, only 7% of adults diagnosed with OAB sought any sort of treatment at all.

Source: Definitive Healthcare claims data and company estimates

{kind=link}

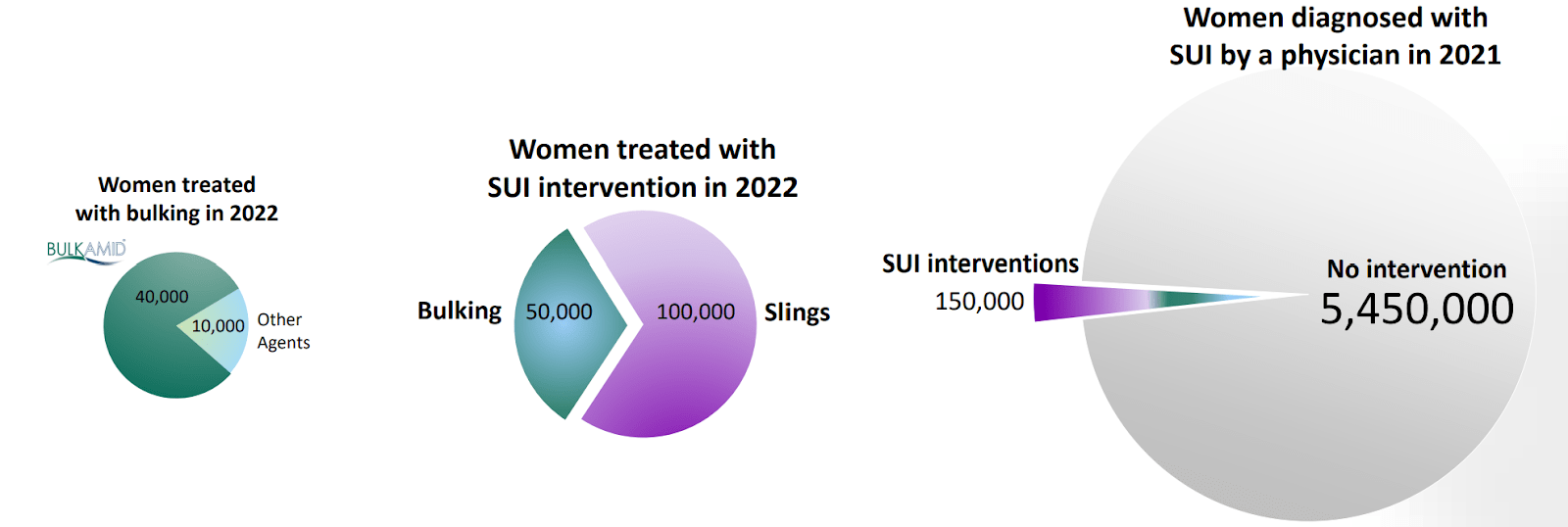

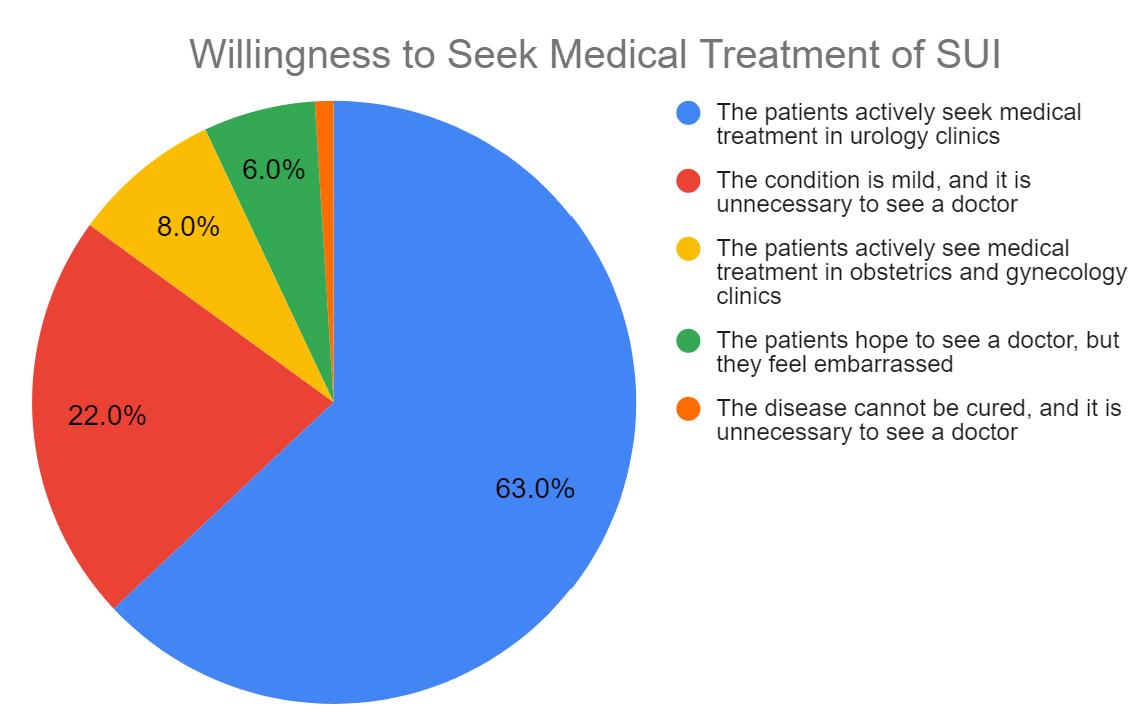

Approximately 22 million women in the US likely have moderate to severe SUI symptoms and less than 3% of those diagnosed actually received treatment. An independent study published in BMC Women’s Health found that 77% of women diagnosed with SUI were willing to seek treatment. This further highlights the untapped market for SUI treatments.

Historically, the sacral neuromodulation devices and bulking agents available on the market required frequent device replacement, large and uncomfortable devices, and repeated injections to maintain efficacy. As a result, many patients would opt to forgo these treatments or stop them prematurely. Increased awareness of pelvic floor health dysfunction, less invasive technology, longer term treatment options, and safer outcomes will lead to higher patient confidence in SNM devices and bulking agents.

Source: BMC Women's Health Survey

{kind=link}

Recent Results

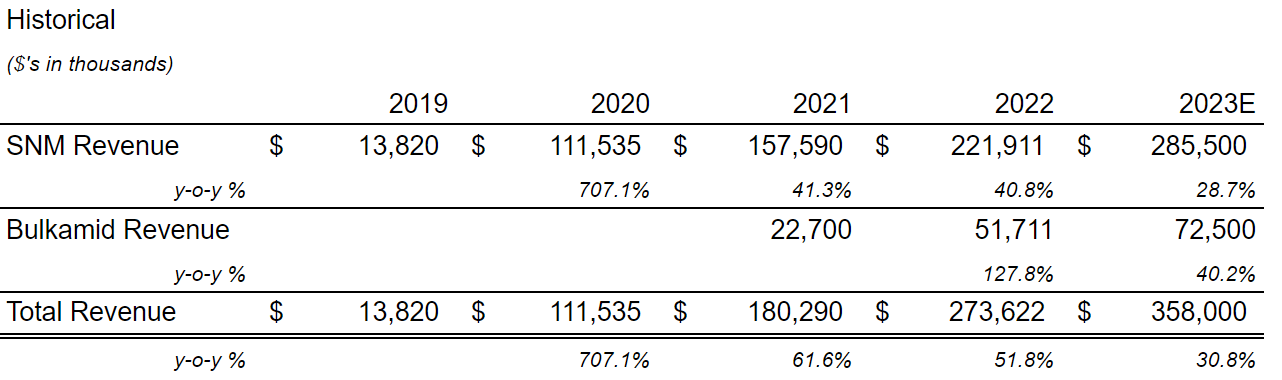

The company generated 35% year over year revenue growth in the second quarter of 2023, released on July 27th , and raised its 2023 revenue target for the year to $358 million, which represents a 31% increase from 2022. It is important to break out the difference in top-line growth between its SNM product suite and Bulkamid. This updated revenue guide reflects a 29% growth in SNM sales and a 40% increase in Bulkamid sales. It is also worth noting that the sales based milestone payment as part of the Bulkamid-related acquisition (exceeding $50 million in sales in a 12 month period) was completed in this most recent quarter.

Source: Company SEC Filings and press releases

{kind=link}

Adjusted operating margin for the quarter also improved to 28% from 13% a year ago, which demonstrates the inherent operating leverage in the business model referenced by management. Adjusted EBITDA for the quarter jumped to $18.4 million, 19.8% margin, from $1.6 million in the prior year period. Assuming a similar margin for the remaining two quarters of the year, adjusted EBITDA could be around $56.5 million for the year (358 million revenue guide minus 163.5 million through 2Q multiplied by margin of 19% added to adjusted EBITDA of 19.3 million through 2Q).

The retirement of CFO, Dan Dearen, announced on 21 August made some waves in the stock, but we believe that this is not a material concern. Ray Cohen, CEO, expressed nothing but confidence in Dan's replacement, Kari Keese. She has been with the company since 2014, well before commercial launch, and we do not expect any missteps in the transition. The company also used the press release to reiterate its 2023 revenue guidance.

Investment Case

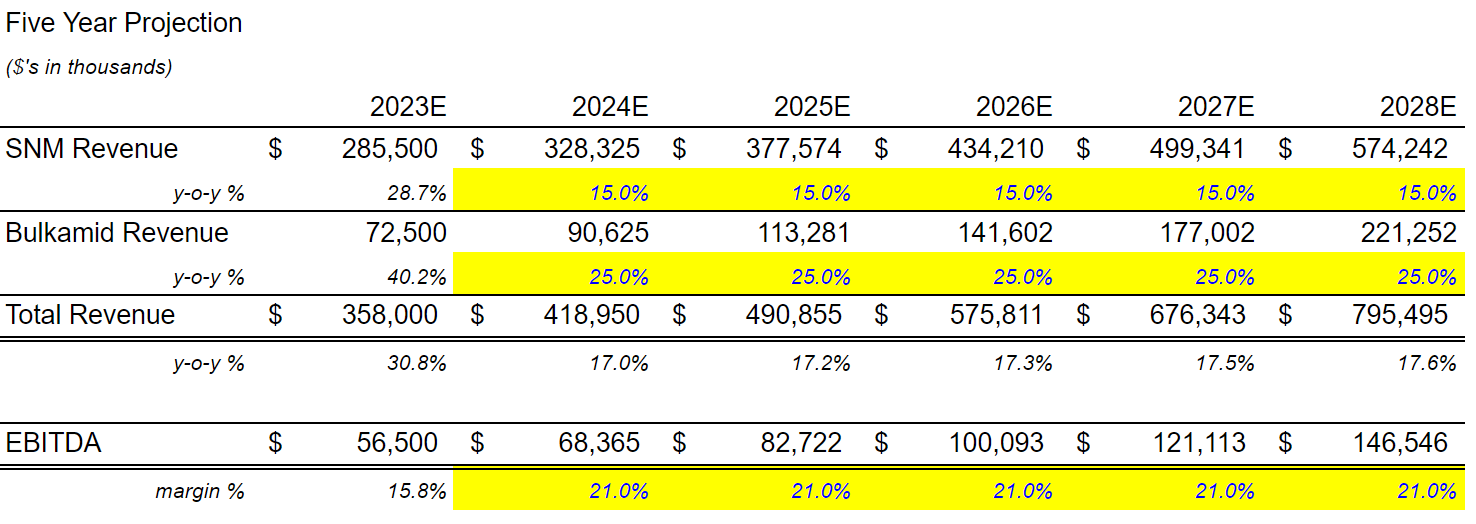

We have a 3 to 5-year plus time horizon for this investment, which we view as enough time for the company to reach a mid-stage of maturity and for revenue growth to start to moderate. The company presents a 15% CAGR for the SNM market over the next 5 years, which when applied to its estimated 2023 SNM revenue of $285.5 million leads to revenue of approximately $574.2 million in 5 years, assuming no upward change in market share. The company does not provide any such estimates for long-term growth of Bulkamid, but we believe that based on recent performance and strong international growth that the CAGR for Bulkamid could easily be 25%. A 25% CAGR over 5 years applied to Axonics’s estimated 2023 Bulkamid revenue of $72.5 million equals $221.3 million. Combined this would put revenue at approximately $795.5 million 5 years from now. On the most recent quarterly earnings call, management estimates gross margin to be in the mid-70's at scale as well. With gross margins at approximately 75%, we believe that a long-term EBITDA margin of 21% is appropriate. The company is projected to reach profitability in 2024 ( consensus estimate of $0.14 EPS, with some targets as high as $0.71 ); and our estimate of roughly $68 million in EBITDA translates into net income of approximately $25 million and $0.50 EPS, on an EBITDA to net income ratio of 2.5 to 1.

Source: Author's model and company estimates

{kind=link}

The company is currently valued at roughly 7.9x its estimated 2023 revenue per share. We do not believe that there are any true comparable companies to AXNX. The only other player in AXNX's market is Medtronic, and SNM is one of three business lines within "Specialty Therapies", which consists of Neurovascular products, ENT (Ear, nose, throat) products, and pelvic health products. For Medtronic's 2023 fiscal year, Specialty Therapies as a whole accounted for 9% of total revenue, according to SEC filings, and we are unable to estimate what fraction of this 9% was actually for pelvic health products. Seeking Alpha provides some comparable market cap, med-tech companies ; and the closest peer is likely iRhythm Technologies ( IRTC ). However, IRTC has over 3x the number of full-time employees, is highly leveraged ($129 million in debt vs $165 million in cash), and has a consensus EPS estimate of negative $2.07 for the year 2014. Yet, IRTC currently trades at 7x estimated 2023 revenue as well, despite being in a much poorer financial position than AXNX but in a similar growth-stage.

The company historically has been a net issuer of shares to fund various requirements but as the company transitions to overall profitability in 2024; we expect the diluted share count to stabilize no higher than around the 52 million range over the next 5 years. This would put revenue per share in the realm of $15. At a more reasonable 5x revenue per share for a mid-stage growth stock, our price target is $75. It is also worth noting that the stock has already traded as high as $77 as recently as September of 2022, reflecting a +30% return from present levels.

Risks To Thesis

Will Axonics continue to increase sacral neuromodulation market share while combating lawsuits involving patents from their competitor? This patent dispute has led to questions from healthcare professionals regarding the long term technical support of Axonics products as they compete against the previous monopolist. Since the release of second quarter results, the Federal Circuit has already ruled in favor once for Axonics and management reiterated its confidence that it does not infringe on any patents.

As awareness for pelvic floor dysfunction increases, will patients turn to devices and injections or will they opt for less invasive first line interventions such as the growing field of Pelvic Floor Physical Therapy? In the past, treatment options were much more invasive and less effective, which we view as the primary barrier to patients seeking treatment. It is our view that any sort of increase in physical therapy usage would still be in conjunction with second and third line treatments.

Will a recession in the United States affect Axonics stock performance? While a broad-based recession would likely lead to a sell-off in equities and a flight to quality, we believe Axonics has outperformance potential due to the non-discretionary nature of its demand and revenue.

Summary

Axonics is a quality stock that has demonstrated sustained, superior revenue growth. We especially like the reimbursable nature of its revenue in a potential recessionary environment, in which consumer discretionary spending theoretically decreases. Whether you believe a recession is imminent or unlikely, Axonics’s revenue should continue to grow and be relatively unaffected by the general state of the consumer and economy.

We believe Axonics is ideally positioned from a solvency-risk perspective due to the strength of its balance sheet and its ability to grow without any looming debt servicing issues. There will be many companies of comparable size but more highly levered that will not survive sustained high interest rates.

Finally, Axonics has already carved out a significant piece of the market for itself, despite battling an entrenched monopolist of 20 years. In our view, this is a result of a determined management team that has undertaken the first ever guerilla marketing campaign to educate patients on solutions to these medical issues. Over time, we see Axonics continuing to demonstrate that it truly has the superior suite of products for this market.

For further details see:

Axonics: Growing Duopolist With Superior Product And No Debt