AXSM - Axsome Therapeutics: Reviewing Q1 2023 Financials And Pipeline Updates

2023-05-09 14:17:57 ET

Summary

- Axsome reported its Q1'23 earnings yesterday - net loss was $(0.26) per share.

- The company's 2 commercial products - newly approved Auvelity and Sunosi, acquired from Jazz Pharmaceuticals earned $29m.

- Axsome smashed analysts' estimates thanks to its out-licensing of Sunosi to Pharmanovia in a deal worth $65.7m.

- Auvelity has blockbuster potential and could also win approval in Alzheimer's Agitation.

- A Migraine therapy - AXS-07 - could also be approved soon, as well as narcolepsy and fibromyalgia candidates. The outlook is relatively bright, but CNS can be a tricky space, and I anticipate cheaper entry points.

Investment Overview

Axsome (AXSM) stock has been making some good gains in recent weeks - the stock price is +36% over the past few months, and +14% across the past week (at the time of writing). Its current traded price is $79 - up >2,000% over the past 5 years.

Axsome is, according to its Q1'23 10-Q Submission:

a commercial-stage biopharmaceutical company developing and delivering novel therapies for central nervous system, or CNS, conditions that have limited treatment options

The company has 2 commercial products - again, borrowing from the 10-Q:

Auvelity (dextromethorphan-bupropion) is a novel, oral, N-methyl-D-aspartate (NMDA) receptor antagonist with multimodal activity approved by the FDA for the treatment of MDD in August 2022.

Sunosi (solriamfetol) is a novel, oral medication indicated to the treatment of excessive daytime sleepiness, also known as EDS, in patients with narcolepsy or obstructive sleep apnea.

Axsome reported its Q1'23 earnings this week. Auvelity earned revenues of $15.7m for the quarter, whilst Sunosi, a drug acquired from Jazz Pharmaceuticals ( JAZZ ) - my note here - in exchange for a $54m upfront payment, and royalties on net sales, earned $12.9m.

The bulk of Axsome's $94.6m of revenues recorded for the quarter were actually from license revenues, which :

represents the upfront payment from Pharmanovia for Sunosi commercialization rights in Europe and certain countries in the Middle East and North Africa region, and the royalty revenue associated with sales of Sunosi in the out-licensed territories.

By the terms of this licensing deal, Axsome could earn another $101m of milestone payments, and royalties on net sales in the mid-twenties percentages.

Axsome also reported a current cash position of $246.5m, current liabilities of $101m, and a long term loan repayment which currently stands at $148m. Loss from operations in Q1'23 was $6.3m, and net loss $11.2m.

The licensing revenues helped Axsome easily beat analysts' expectations both in terms of revenues - consensus estimates were for revenues of ~$27m - and earnings per share, where the consensus estimate was for ~$(1.14), whereas the actual loss per share was $(0.26). Axsome stock has risen in response to a value of $78.5 per share, giving the business a market cap valuation of $3.41bn.

Oddly - for a commercial stage biotech - management did not provide any revenues or earnings guidance for 2023, instead commenting in a press release that:

Axsome believes that its current cash, along with the remaining committed capital from the $350 million term loan facility, is sufficient to fund anticipated operations into cash flow positivity, based on the current operating plan.

For a company with a $3.4bn market cap and 2 commercial products, I must say I am surprised that guidance consists of discussing when the company may run out of funding. Presumably, the company is not expecting to be profitable this year - losses have amounted to $(187m), $(130.4m), and $(103m) in FY22, FY21 and FY20 respectively - and the licensing deal is a one-off windfall, but with $100m of revenues a reasonable target for a company whose product sales were ~$29m in Q1'23, management must at least be confident of narrowing its annual losses this year?

If Q1'23 product sales performance were to be repeated in the remaining 3 quarters of 2023, then it is also difficult to justify the current market cap - price to forward sales would be ~30x, which seems unjustifiably high.

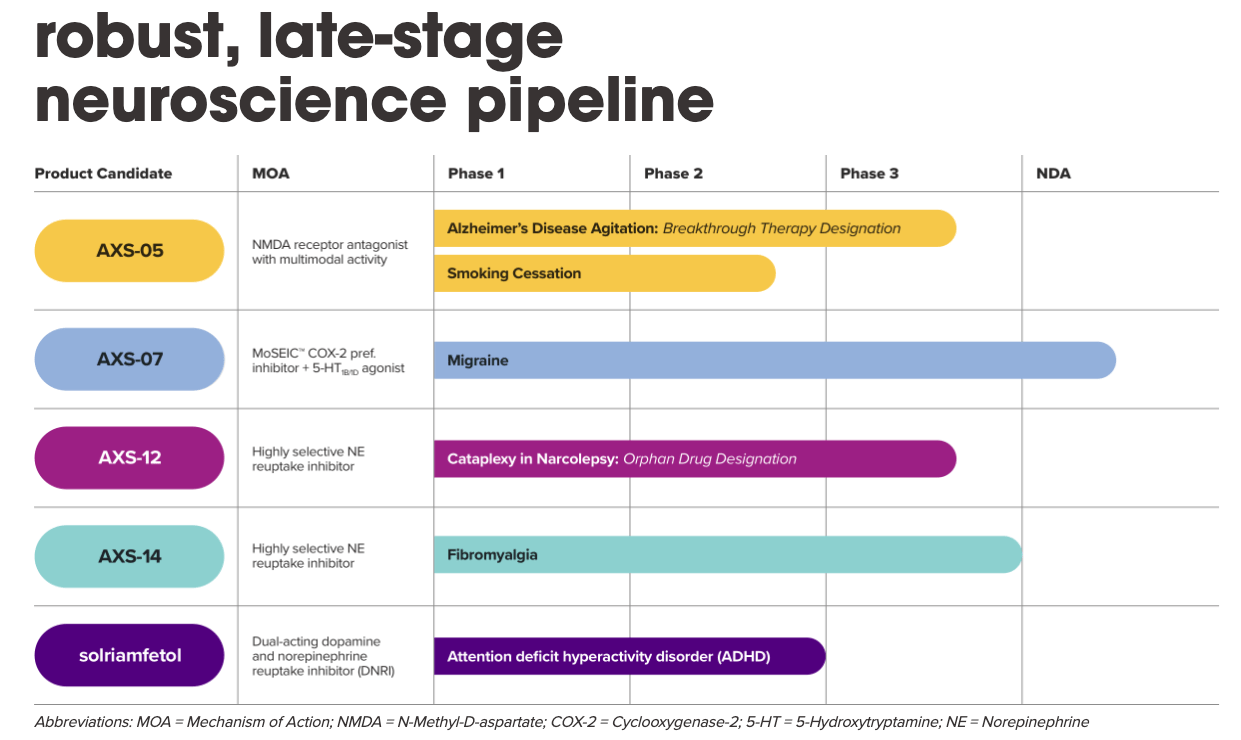

Luckily for Axsome, however, the company has a substantial pipeline with plenty of late stage opportunities in play, as shown below:

Axsome pipeline (Axsome website)

{kind=link}

Axsome Pipeline - Bubbling Away Nicely & Providing Support To Auvelity

As shown above, Axsome has 4 late stage (Phase 3 or beyond) pipeline opportunities. Let's consider each in turn.

AXS-05

The first is AXS-05, which is the same drug approved to treat MDD last year i.e. Auvelity. In MDD, a major selling point of Auvelity is how quickly the drug gets to work - i.e. in 1 week, as opposed to the normal 6-8 week wait for a treatment effect, based on pivotal study trial results in >300 patients.

Auvelity will rival another N-methyl D-asparate (NMDA) receptor antagonist - Johnson & Johnson's (JNJ) Ketamine based drug Spravato - in the MDD market, and analysts have speculated that Auvelity could generate peak sales of ~$1.6bn in that indication alone. That number is certainly more appealing than quarterly sales of $16m, and would almost justify the $3.4bn market cap on its own.

Analysts also believe that an approval in Alzheimer's Disease Agitation could add another $750m to Auvelity's peak sales however, and Axsome's Phase 3 study in that indication, ADVANCE 2, which is expected to complete in H1'24.

That would make an approval unlikely before 2025, but in an area of unmet need, and based on Phase 2/3 data from the Advance 1 study, in which the drug achieved its primary endpoint, showing "rapid, substantial, and statistically significant improvements in the Cohen-Mansfield Agitation Inventory ("CMAI") total score versus placebo", the odds of an approval in this indication seem good.

Balanced against that, back in February the FDA requested to see more long-term safety data from Axsome. This seems likely to come from the ongoing ADVANCE 2 study, therefore an approval before 2025 would seem unlikely, and despite the MDD approval is not necessarily guaranteed that Axsome will accrue the necessary safety data.

AXS-07

AXS-07 - indicated for treatment of migraines - "consists of MoSEIC, or Molecular Solubility Enhanced Inclusion Complex, meloxicam and rizatriptan", according to Axsome's 10Q, which goes on to state:

We have completed two Phase 3 trials of AXS-07 for the acute treatment of migraine, which we refer to as the MOMENTUM and INTERCEPT trials. AXS-07 achieved the co-primary endpoints in both the MOMENTUM and INTERCEPT trials.

We have also completed an open-label, long-term, safety study of AXS-07 in patients with migraine known as the MOVEMENT trial. In the MOVEMENT trial, administration of AXS-07 resulted in rapid, and substantial relief of migraine pain and associated symptoms and was well tolerated with long term dosing.

AXS-07 was rejected for approval in the US by the FDA in May last year, who said it needed more data around chemistry, manufacturing and controls ("CMC") when issuing its Complete Response letter (outlining reasons for the rejection).

CMC is the "best" kind of rejection because it is usually resolvable, and means that the agency would approve the drug on safety and efficacy grounds. As such, Axsome plans to resubmit its New Drug Application ("NDA") this year, and is expecting a 6-month review period. As such, we could see AXS-07 approved next year.

In terms of product sales expectations for this drug, the migraine market is relatively crowded, but also large, with AbbVie's ( ABBV ) Ubrelvy earning >$600m of revenues last year, and forecast for blockbuster sales. Pfizer's ( PFE ) migraine nasal spray ZAVZPRET was also approved in March this year, AbbVie's Qulipta makes triple-digit million sales after being approved in 2021, and Amgen's Aimovig generated >$400m in product revenues last year.

If AXS-07 is approved, peak sales expectations are relatively low - Cowen set a target of $200m by 2030 - but nevertheless, another approval would likely buoy Axsome's stock price, and if approved the company could begin at least to generate some revenue from the product rather than funding studies and administrative work.

AXS-12 / 14 & Repurposing of Sunosi

These 2 pipeline opportunities refer to the same drug, Axsome's "highly selective and potent norepinephrine reuptake inhibitor". After a successful Phase 2 study, in which the candidate "significantly reduced the number of cataplexy attacks as compared to placebo in patients with narcolepsy", according to a 2019 press release , a Phase 3 "Symphony" study is underway, with topline results expected imminently.

Narcolepsy is perhaps not the easiest market to penetrate, given the presence of Jazz Pharmaceuticals' Xyrem and Xywav currently rule the roost, and with Avadel Pharmaceuticals having won approval for a once-nightly sodium oxybate formulation and set to launch commercially this year, but with that said Xyrem and Xywav generated nearly $2bn in revenues last year. AXS12 is apparently mechanistically similar to Sunosi, a drug Jazz was prepared to license to a direct rival, hence my conclusion would be this could be not much more than a high double-digit, or low triple digit revenues opportunity.

With AXS-14 Axsome is having a tilt at the fibromyalgia market - some estimates suggest this is a >$3bn annual market - and a New Drug Application is being promised for this year - according to the Q1'23 earnings press release:

AXS-14 has previously met the primary endpoints and demonstrated positive and statistically significant results in a Phase 3 and in a Phase 2 trial for the management of fibromyalgia.

When it comes to the Jazz / Sunosi deal, it certainly seems as though Axsome got the better of this deal, based on the significant windfall realised in Q1'23 by outsourcing overseas rights, and the company's intention to repurpose the drug for the Attention Deficit Hyperactivity Disorder ("ADHD") market. The update provided in Q1'23 was as follows:

ADHD: The Company is on track to initiate a Phase 3 multi-center, randomized, double-blind, placebo-controlled trial to evaluate the efficacy and safety of solriamfetol in adults with ADHD in the second quarter of 2023.

Research suggests that ADHD is a >$15bn market, although it is well saturated, with treatment options, including Adderall, Concerta, Focalin, Ritalin, and 6 others at least. Whether Sunosi could make a dent in this market remains to be seen, but it is an interesting, opportunistic move by Axsome nonetheless.

Concluding Thoughts - So Many Options, Although Axsome May Not Quite Add Up To Sum Of Parts

There are very few Seeking Alpha analysts making the bear case for Axsome shares - in fact the last article with a "Sell" recommendation was written back in 2019 - and I am not about to make that case either.

Clearly, Auvelity should not be judged too harshly on its Q1'23 sales, having only recently been launched, and although analysts' peak sales estimates often turn out to be wildly inaccurate, there seems to be a consensus that this drug could match e.g. JNJ's Spravtao and target blockbuster (>$1bn per annum) sales.

That in itself is sufficient to justify the current market cap valuation, although if we then factor in risk and time, some additional ballast is required to support a market cap of $3.4bn today.

That ballast comes in the form of the Alzheimer's Agitation and migraine approvals for AXS-05 and AXS-07 respectively, which could potentially add $1bn per annum to Axsome's top line, whilst AXS-12 / 14 looks good for potentially an additional $500m.

If we stop there, we already have theoretical peak sales of ~$2.5bn, let's say by the end of the decade, and if we use a rule of thumb that 5x price to sales is a good yardstick for valuing a company, arguably, there is a case for Axsome enjoying a double-digit-billion market cap in 2030.

Rarely is anything so simple in the CNS markets, however, with scores of biotechs and Pharmas targeting every indication with innovative new drugs. Axsome does not have a great deal of commercial experience, and as such, were e.g. AXS-07 and AbbVie's Qulipta to share a similar safety efficacy profile, it is not hard to imagine the Big Pharma's drug grabbing the lion's share of the market.

That is why, on balance, after reviewing Axsome's products and portfolio after Q1'23 earnings, despite there being a number of important catalysts in play - from Phase 3 results, to approval decisions, to more mature sales figures, I'll stick with a hold recommendation for now. The company's stock is trading at its highest price since mid-2021, and close to all-time highs, but as recently as June last year shares traded <$25.

The gains since then have no doubt been deserved, but rarely is a path to approval in a CNS field straightforward - as Axsome knows well based on previous experience - hence my advice would be stay on the sideline and wait for a, hopefully minor, setback that results in a downward correction.

Provided the setback is not too troubling, Axsome shareholders may one day see the stock price reach triple-figures in my view, but there is enough volatility in these markets to suggest we will see lower lows than $78, before the ascent to that target price.

For further details see:

Axsome Therapeutics: Reviewing Q1 2023 Financials And Pipeline Updates