AYASF - Aya Gold & Silver: Boumadine Continues To Grow

2023-10-16 17:13:58 ET

Summary

- Aya Gold & Silver Inc. is down ~45% from its highs, but has massively outperformed its peers since 2020, and for good reason given its continued per share growth.

- However, while the company already offers industry-leading growth with its Zgounder Expansion, a second major opportunity is emerging: Boumadine.

- With a strong pipeline of development assets, continued exploration success & a high-grade silver mine with a superior jurisdictional profile to peers, Aya Gold & Silver looks to be a buy on dips.

It's been a tough three years for the Silver Miners Index ( SIL ), which has struggled to hold on to any of its gains, down ~55% from its 2020 peak and suffering a drawdown of nearly 60%. However, Aya Gold & Silver Inc. ( AYASF ) is an exception, with a ~200% outperformance relative to its peer group, and for good reason.

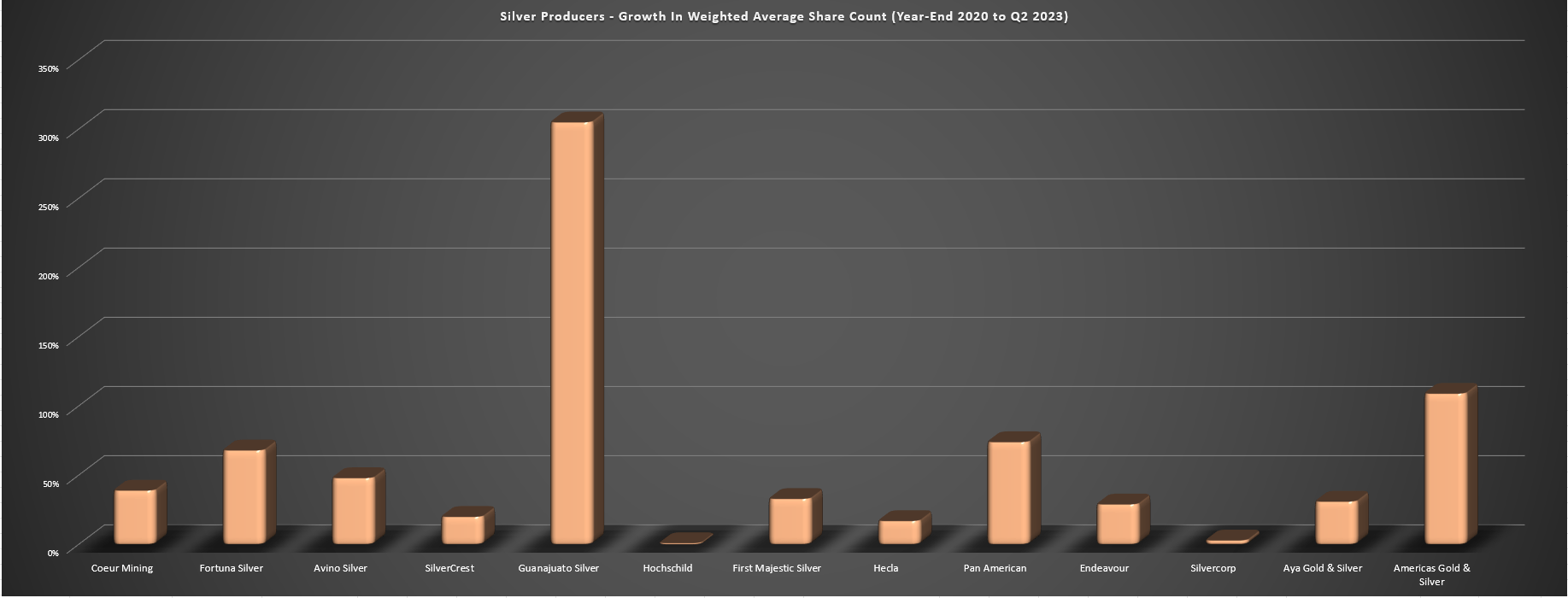

This is because not only has Aya seen significantly less share dilution relative to its peers, but any share issuance has gone a long way, with ~2.8 million shares issued to scoop up a high-grade gold project in Mauritania (Tijirit), ~11.1 million shares issued at an attractive price to improve its balance sheet ahead of its major Zgounder Expansion, ~0.6 million shares to add a historical copper mine near Zgounder, and the rest related to warrant/option exercises. And this is in stark contrast to some other miners like Americas G& S ( USAS ), First Majestic ( AG ), and Coeur ( CDE ) which have seen share dilution to keep the lights on with USAS, to add a project that's now found itself in care & maintenance with AG, and to help fund a massively over-budget expansion at its Rochester Mine in CDE's case.

Silver Producers - Growth in Weighted Average Share Count (Year-End 2020 to Q2 2023)

{kind=link}

In fact, if we look at the Aya of 2020 vs. the Aya of today, the company has more than doubled its resource base to ~102 million ounces of silver at its flagship mine, added a new potential mine in Tijirit to diversify outside of Morocco, significantly increased its land package with over 425 square kilometers at Zgounder and looks set to prove up a 200+ million ounce resource on a silver-equivalent ounce [SEO] basis at Boumadine. The result is that Aya is paving the way to potentially becoming a 28+ million ounce per annum producer on a silver-equivalent basis by the end of the decade (~370,000 gold-equivalent ounces), assuming it can put Boumadine and Tijirit in production, with these being permitted assets with what I would expect to be exceptional economics. And if successful, this will certainly warrant a meaningful re-rating. In this update, we'll look at the primary potential driver of this future growth, Boumadine.

Boumadine Camp - Company Website

{kind=link}

Boumadine Exploration Success

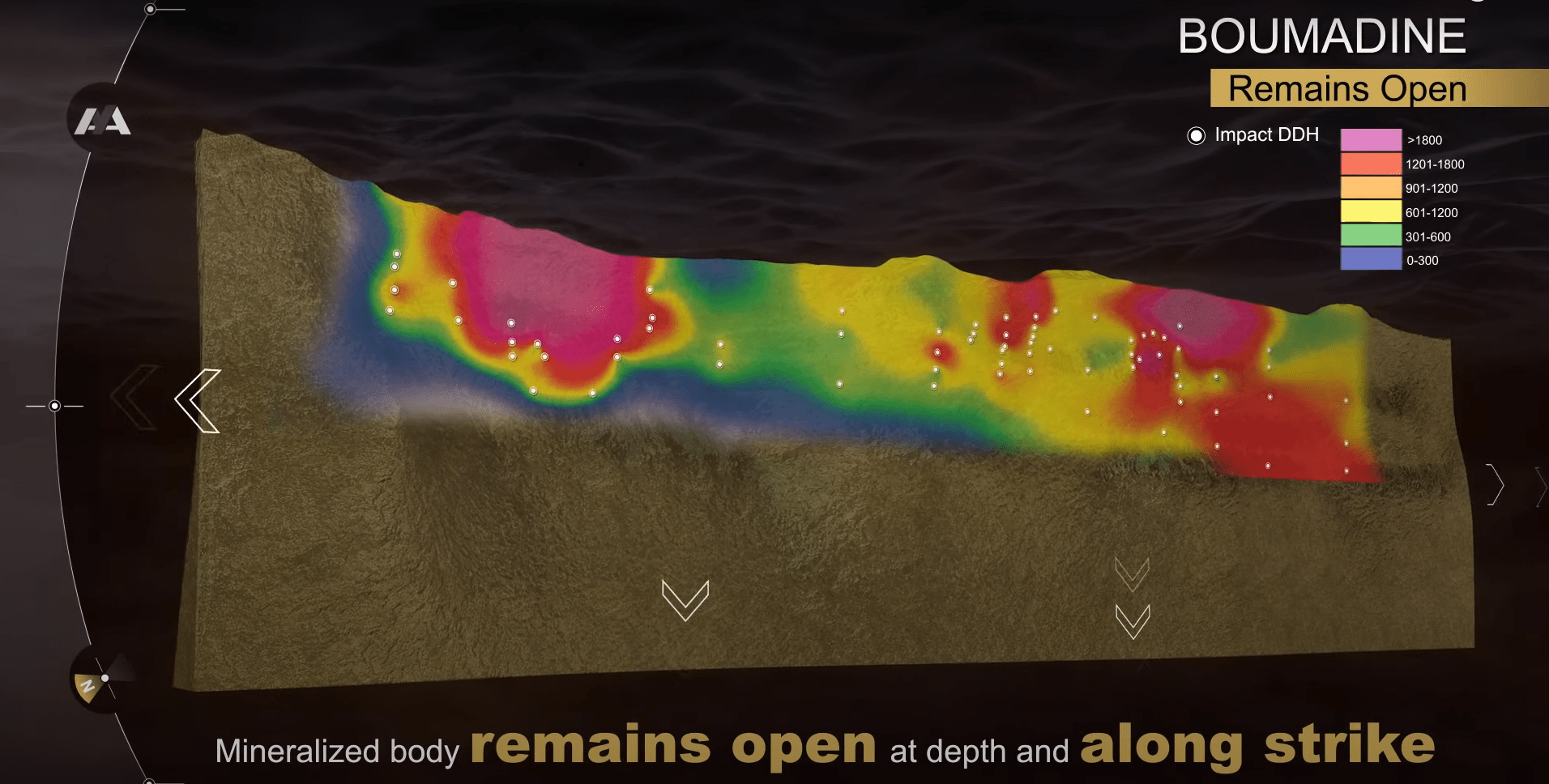

While Aya's Zgounder Mine has been the driver of much of its share price performance and the company is in the midst of a massive expansion to push production to ~6.8 million ounces of silver per annum as a pure-play silver producer, Boumadine (85% owned by Aya) has sat in the wings with little value ascribed to it. This is despite it being a former polymetallic mine on the massive and highly prospective Anti-Atlas Belt that's accessible from Ouarzarate City with a ~48 square kilometer land package. And while the company does not have a current resource on the property, Boumadine continues to grow at an exceptional rate, with the mineralized strike increasing from ~2.7 kilometers in September 2022 (when it confirmed the continuity of Boumadine mineralization between the Central and South Zone) to ~4.2 kilometers as of last month, a ~55% increase in just a year.

Boumadine Open at Depth and Along Strike - Company Presentation

{kind=link}

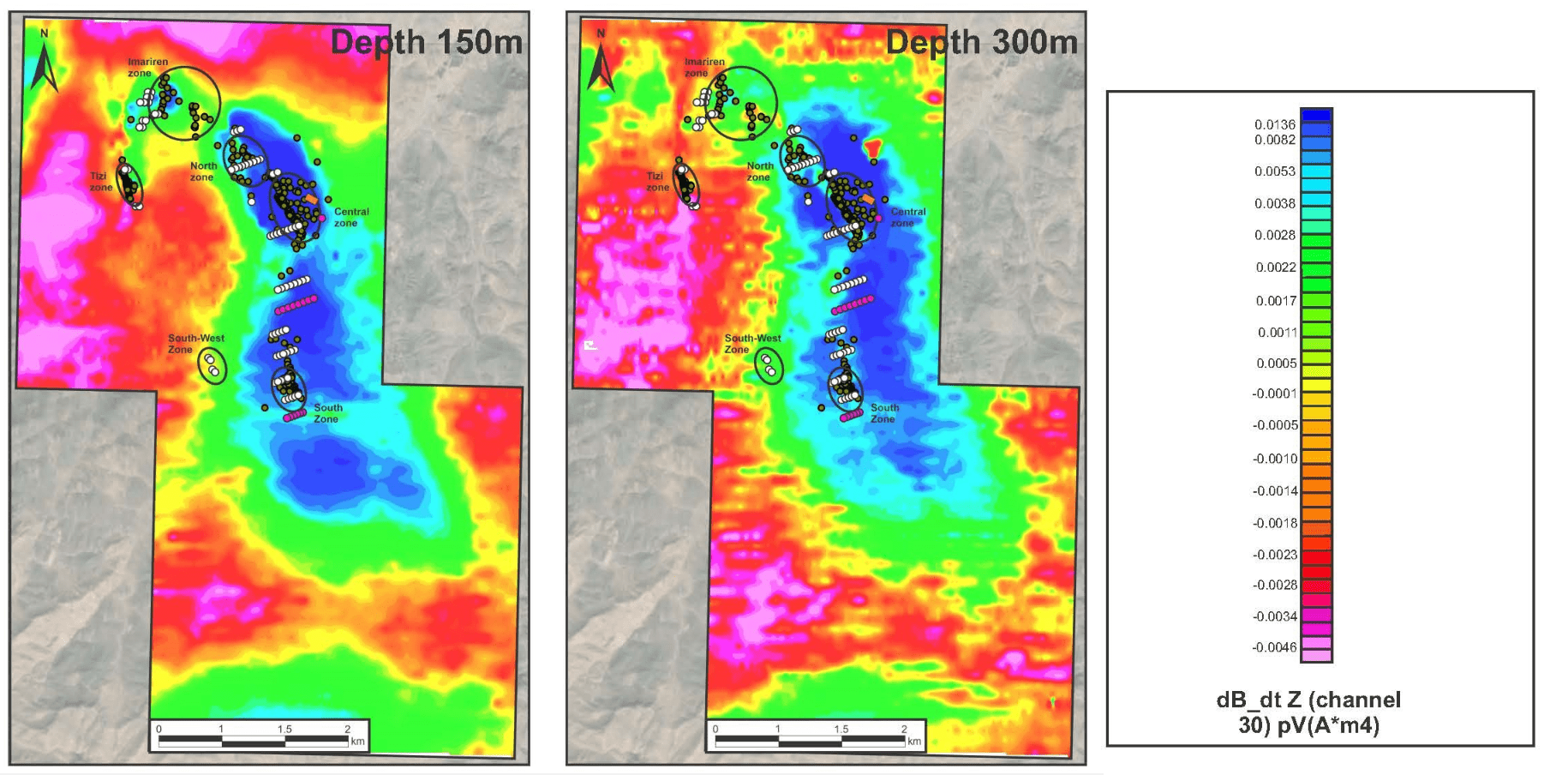

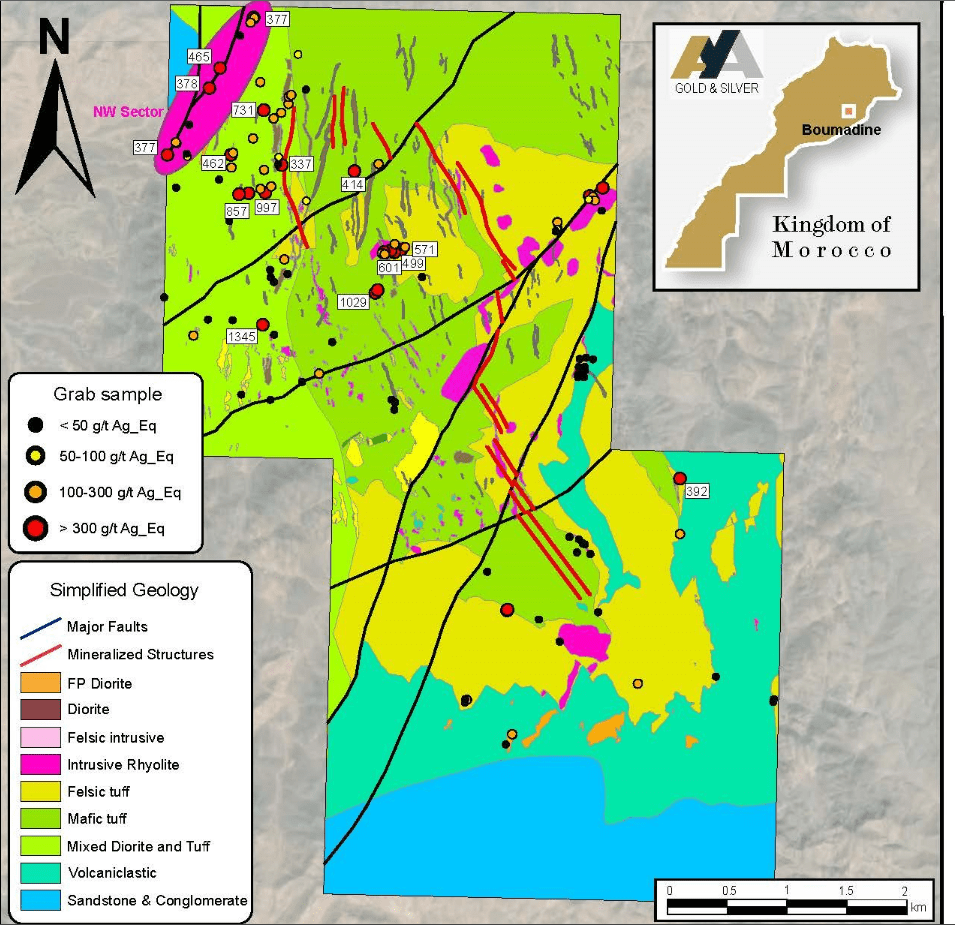

Although this increase in strike is quite meaningful and will add considerable ounces vs. the previous mineralized footprint, it's important to note that the total potential strike could be 6.0+ kilometers, never mind the potential at depth and to the west of the main Boumadine trend. This is because Aya noted last year that geophysics completed on the property pointed to the presence of a conductive anomaly down to at least 600 meters below surface along the dominant trend at Boumadine, suggesting further upside at depth relative to the resource expected to be released in Q1 2024. In addition, this geophysical work has identified new conductive anomalies south and west of the main Boumadine trend. And more recently, Aya has identified a new mineralized structure to the northwest (highlighted in the second photo below), with high-grade samples upwards of 300 grams per tonne silver-equivalent. And as stated by President & CEO Benoit La Salle at the time:

“We are very excited by the recent VTEM data from Boumadine suggesting continuity of the mineralized structure both south and at depth, which follow last month’s promising high-grade drill exploration results on the property. The presence of new conductive anomalies outside the main trend indicates the potential for new mineralized zones adjacent to and along the Boumadine main trend."

- Aya Gold & Silver, November 2022.

Boumadine Airborne VTEM Survey at 150/300 Meter Depths - Company Website 2023 Surface Samples at Boumadine Northwest - Company Website

{kind=link}

{kind=link}

This is important because although Boumadine Main (4.0 - 6.0 kilometer strike potential with further upside at depth) already looks to be a behemoth that could ultimately come close to rivaling Corani in size (but with much lower upfront capex), the company has barely scratched the surface outside of the area of focus (4.0 - 6.0 kilometer strike) on the main trend. And if the company continues to have drilling success outside of this main trend, Boumadine might grow into a 300+ million resource on an SEO basis, making it nearly triple the size of Zgounder (~106 million ounces across all resource categories). And as noted in my last update, this could conceptually be a ~20 million ounce producer on a silver-equivalent basis in its earlier high-grade years, assuming a ~4,600 tonne per day operation at ~500 grams per tonne silver-equivalent and 74% payability, or a ~$500+ million NPV (8% discount rate) using a $24.00/oz silver price.

I have used a $24.00/oz silver price over the mine life, which is above current spot prices given that I think this is a very conservative silver price assumption given that the timeline for this production is 2028 or later. In fact, $28.00/oz might end up being a conservative assumption by 2028, given that silver is overdue to start a new bull market after an 8-year bear market followed by a 3-year consolidation period, and at $28.00/oz the NPV (8%) increases to ~$800+ million.

To summarize, while Aya may appear to have a limited upside from a market cap of ~$650 million compared to some of its peers based on Zgounder alone (~6.8 million ounces per annum of silver production at sub $10.00/oz all-in sustaining costs), the opportunity at Boumadine is massive. Plus, with this being a relatively high-grade opportunity (~450 grams per tonne silver-equivalent or ~6.0 grams per tonne gold-equivalent), this means a smaller footprint of 4,000 to 5,000 tonnes per day could still support a very significant production profile vs. other undeveloped assets like Corani at 27,000 tonnes per day and Cordero at 25,000+ tonnes per day). Hence, Boumadine could potentially be put into production for less than $380 million (assuming continued inflationary pressures), with the potential to fund this with project debt and free cash from Zgounder, meaning significant reserve, cash flow, and production growth per share, with limited share dilution.

Obviously, putting cash flow projections on a pre-resource project is a stretch, and I should caution that these numbers are quite conceptual. But assuming commercial production in 2029 for Boumadine, this is an asset that could generate average annual free cash flow of $230 million in its first four years at $28.00/oz silver. And it's important to note that this is not the only growth opportunity in the portfolio, with Aya continuing to add exploration ground surrounding Zgounder, which might support a further throughput expansion down the line if Aya can delineate a meaningful resource at future satellite deposits.

Other Opportunities

As noted in a previous update , Boumadine could be a game-changer for Aya and certainly looks to have the ingredients with a massive mineralized footprint already delineated with impressive grades. However, a small opportunity that has received less air time because of the continued exploration success at Boumadine/Zgounder is Tijirit. This high-grade gold deposit is located in Mauritania barely 30 kilometers east of Kinross' ( KGC ) massive Tasiast Mine, which is ~75% owned by Aya, and where the company noted that it is actively looking for a partner to develop the asset. Notably, the project is already permitted until June 2047 with a permit that covers 5 zones of a 150 square kilometer area, with the initial focus on the two higher-grade deposits, Elenore and Eleonore East.

Tijirit Project - Company Website

{kind=link}

Of the deposits that have been delineated (Sophie, Lily, Eleonore), Eleonore is the highest-grade with ~1.6 million tonnes at 4.21 grams per tonne of gold for ~215,000 ounces, and based on potential production rates of 1,000 tonnes per day and 1,500 tonnes per day and assuming a ~3.2 million tonne reserve base, the project could support an ~8.8 and ~6.0 year mine life, respectively. And based on the smaller of the two potential production scenarios (1,000 tonnes per day), a 3.3 to 3.7 gram per tonne average grade in its earlier years and depending on terms of any future partnership, this could support a ~20,000 ounce attributable production profile at very high margins with zero share dilution for Aya given that it would be able to finance its portion of the modest capex bill with debt.

Judging by potential production rates, this is not be the needle mover that Boumadine could be, which is why it's moved to #2 in priority. Still, it's added cash flow with modest upfront capex (if Aya can secure a partner for the asset), with this future cash flow from Tijirit/Zgounder able to support plowing exploration dollars back into Zgounder and Boumadine to look at growing these assets that have considerable untapped exploration upside. Hence, although I think it's difficult to assign much to Tijirit today, I would argue that $45 million in value is reasonable, which is equal to an additional ~$0.35 per share in value (128 million fully diluted shares), and it potentially gives Aya diversification outside of Morocco, a key differentiator vs. other single-asset silver producers.

Summary

While production growth is important and there's no shortage of growth stories in the sector, permitting has become more difficult, jurisdictional is more important than ever, and above all, growth is hardly desirable if it isn't being accomplished on a per share basis. Fortunately, Aya Gold & Silver Inc. checks all the boxes, with an ultra-low discovery cost of ~$0.20/oz, a high-ranked jurisdiction in Morocco with extremely favorable permitting timelines (plus already permitted development projects), and a future cash cow in Zgounder plus a strong balance sheet ($50+ million) that supports per share growth, one of the key attributes of the largest winners in the sector over the past few decades. Plus, in a sector where silver producers command a premium, Aya certainly stands out as a pure-play silver producer at Zgounder, and it is emerging as a larger producer at the convenient time that other silver-producing jurisdictions are decreasing in investment attractiveness, with the major jurisdiction that hosts most publicly-traded silver producers being Mexico.

AYASF Weekly Chart - StockCharts.com

{kind=link}

Not only have we seen mining reforms recently in Mexico, but we've also seen multiple illegal blockades over the past few years, a strike at the massive Penasquito Mine that resulted in higher wages, the nationalization of lithium under President AMLO, and a recent armed robbery of concentrate at La Colorada, coupled with an already violent history in Guerrero State. And while it might have been hard to justify owning Aya as a small-scale producer when it traded above US$9.25, it is now down ~45% from its highs, its jurisdictional profile is looking better than ever relative to other silver names on a comparative basis, and the company has uncovered a monster in Boumadine which should help to put a floor under its valuation with a resource due by March 2024.

Hence, while I previously avoided Aya Gold & Silver Inc. given that I prefer out of favor names at deep discounts to fair value, that opportunity has arrived and the setup is more favorable than ever to own the stock, as noted above. In summary, I see this pullback below US$5.30 as a buying opportunity.

For further details see:

Aya Gold & Silver: Boumadine Continues To Grow