AZUL - Azul Is Flying Higher But Its Stock Is Not

2023-05-16 05:52:16 ET

Summary

- Azul has significantly improved its quarterly results.

- The company has structurally reduced costs.

- At current prices the stock is undervalued.

- Risks for airlines remain and some additional risk is tied to Brazilian airlines and companies.

Last year I started covering Azul ( AZUL ), and while the company was bullish on its future, I didn't adopt a buy rating and most likely my Hold rating on the stock wasn't the best one as the company lost nearly 30% of its value ever since. It should serve as a reminder that airlines remain risky investments and Brazilian carriers continue to carry an even higher risk with forex fluctuations as well as the political system which at times isn't shining for its stability.

The most recent Hold rating from March 6th has been more fruitful with a 33.33% increase in the stock price since. So, the risks are certainly there, but it should also be kept in mind that at times you can lock in a steep loss or you can continue holding a stock as there could be prospects of higher stock prices. In this report, I will be covering the first quarter earnings and provide a valuation on the stock based on the interactive valuation tool that I have developed for subscribers of The Aerospace Forum.

Azul Reports Strong EBITDA Margin

{kind=link}

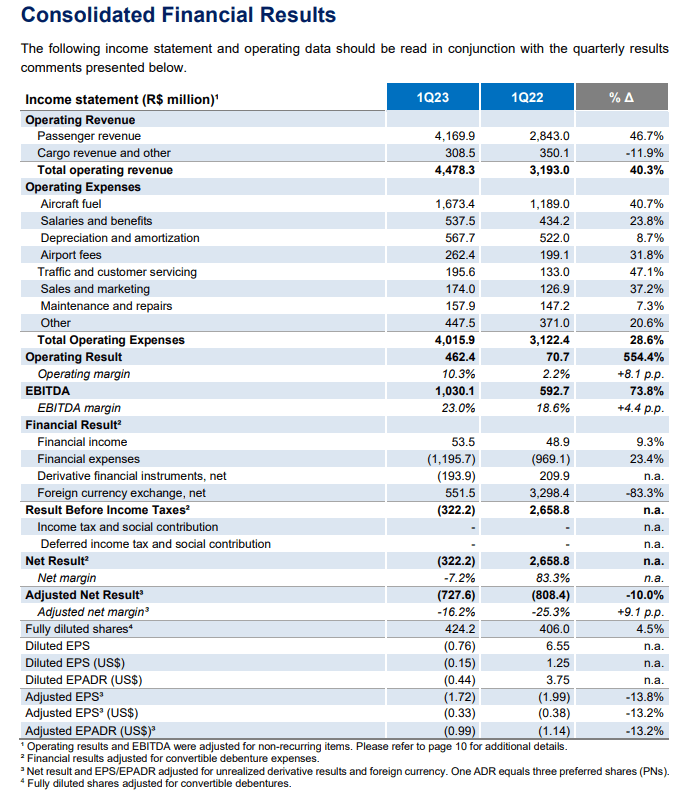

During the first quar ter , revenues increased by 40%. Passenger revenues increased by 47% while cargo revenues declined 12% for a total revenue increase of 40%. Just the revenue trajectories of passenger and cargo tell us two stories. On cargo, it really tells us that the times of booming cargo demand where just having a plane to fill with freight and rake in profits are over. On the passenger revenue side we are seeing the continue improved in the demand environment but also the relatively favorable comp where we can compare a quarter impacted by Omicron last year with a world where we barely take note of the pandemic anymore.

The top line growth was driven by a 20% increase in capacity and an 18% increase in unit revenue. For a long time, Brazil has actually managed inflation quite well. So, while operating expenses grew by nearly 30%, in the earnings call I haven't heard anything about inflation. The year-over-year inflation was 6% down from 11.3% a year earlier. So, what fuels the higher cost balance is a combination of having a bigger flight footprint, the higher growth in international flying which is more costly, and inflation, but overall we are seeing better operating and EBITDA margins which are primarily adjusted for lease restructuring announced and discussed earlier. During the quarter, the unit costs excluding fuel rose 2%. I think that is extremely strong. Most certainly with double digit capacity growth in a normal setting you would expect lower unit costs, but from an inflationary standpoint we are still not in a normal setting.

For 2023, the restructuring will lead to a 40% reduction in lease payments and 30% and 25% in the two years after. So, the lease restructuring significantly enhances the debt balance since lease obligations are recorded as debt.

{kind=link}

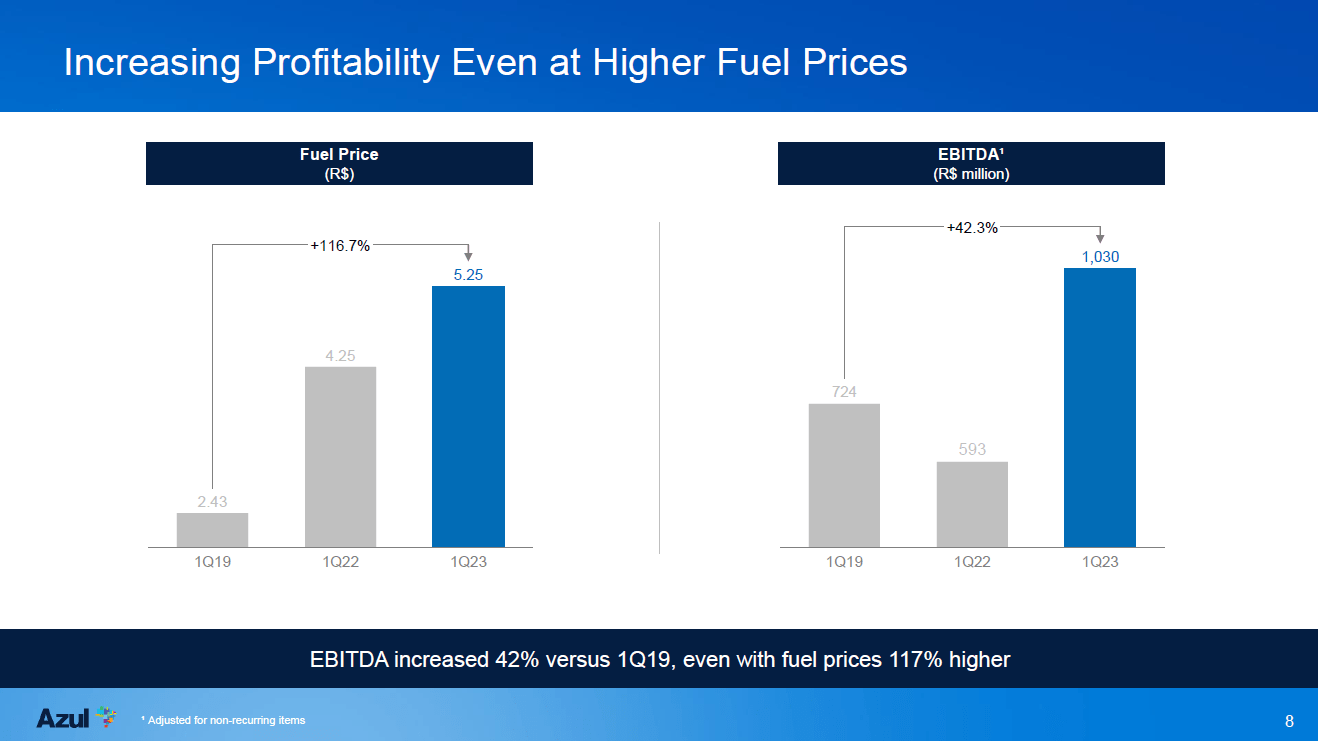

The slide above says a lot about how Azul has managed to make its business more worthwhile. I have no doubt the company put a rising fuel price and a rising EBITDA together on purpose, and while I am not one to jut accept what a company puts on my plate during a presentation, having EBITDA increase by 42% while fuel prices more than double shows how the company has used the pandemic to make its business better.

Azul Posts Significant Deleveraging

{kind=link}

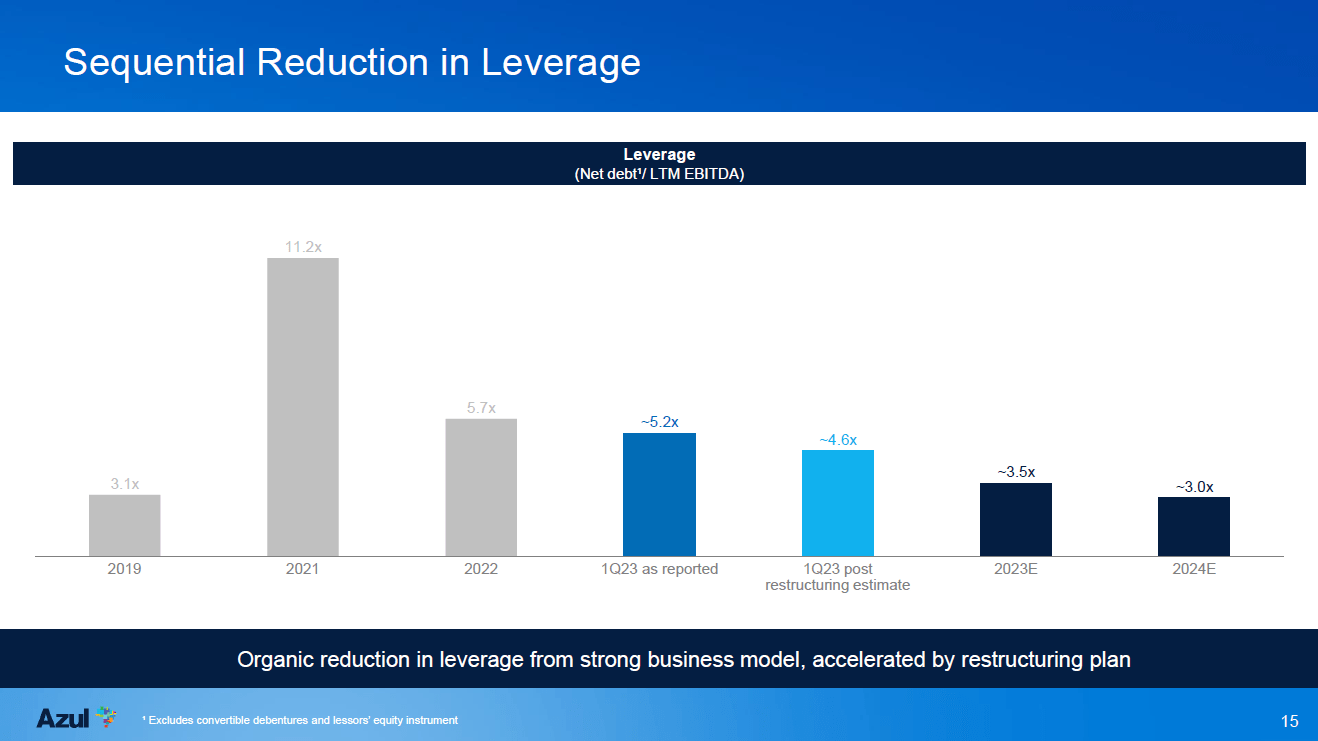

For many airlines, the big challenge on the recovery trajectory has been to deleverage and we see that Azul is making big steps there. It is not the only airline to do so, but they are doing it. The airline ended with a 5.7x leverage in 2022 and brought that down another 0.5 points in Q1 and even 0.9 points with the restructuring in mind with 3.5x targeted by 2023, and by 2024 it should be back to normal for Azul.

Azul Expects V-Shape Growth, Updates Guidance

{kind=link}

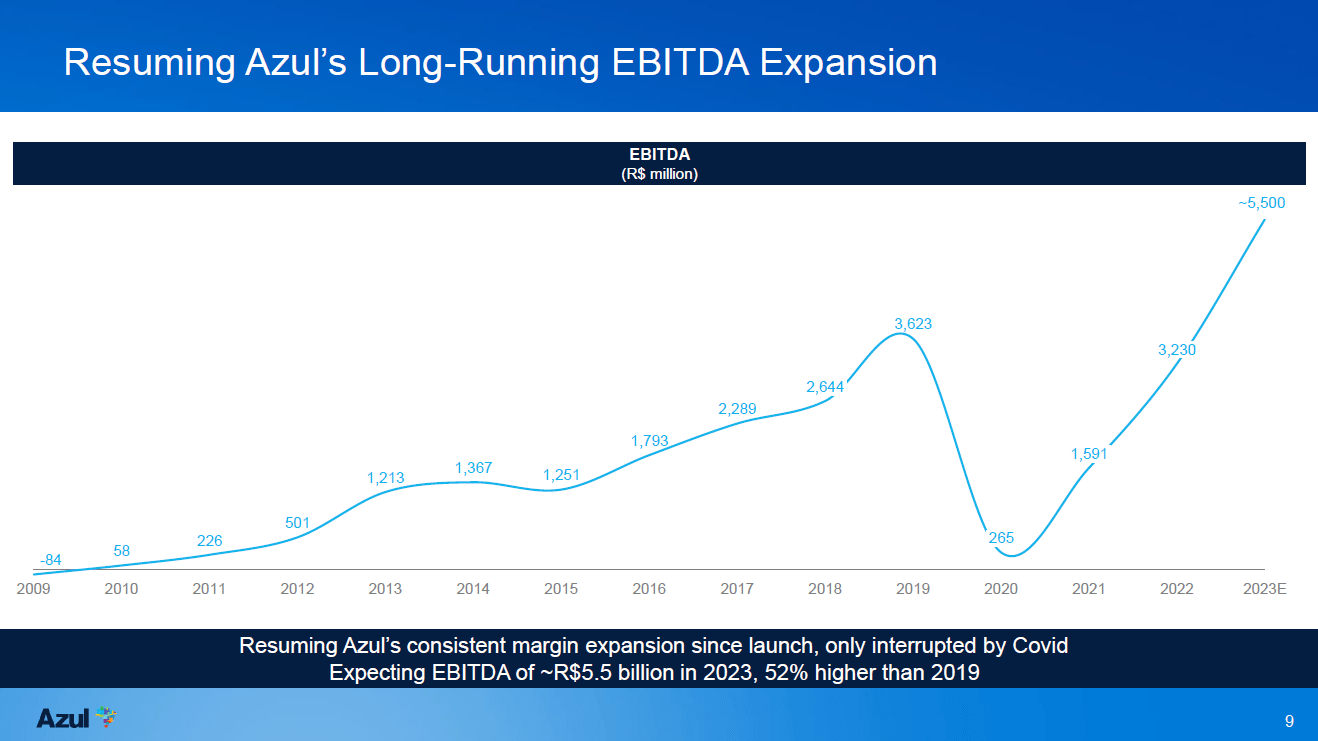

Azul has guided for R$ 5.5 billion in EBITDA in 2023. That is up 10% from its previous guidance and up 70% year-over-year on a 14% expansion in capacity. So, the company is expecting a very strong year, and, more importantly, the results will be exceeding pre-pandemic levels by almost 50%, which is another sign of the overall restructuring of the business. It looks very much like a V-shaped recovery. It's not a perfect V-shape but pretty much near perfect.

Is Azul Stock A Buy?

When entering the numbers into my model, significant upside for the stock becomes visible. Based on the industry median, 25% upside exists based on the industry enterprise multiple and up to $11 for next year while a valuation of using the typical company EV/EBITDA suggests even 35% upside. While I am wary of putting buy ratings on airlines, and in particular Brazilian airlines, I do think that Azul is significantly undervalued at current prices.

Conclusion: Azul Flying Higher Out Of The Pandemic

So far, I have been somewhat hesitant to put a buy rating on Azul stock, but with improving results and a structural reduction in big cost items, I do believe that the current share prices does not reflect these positive items and the expected earnings going forward. I see double digit upside for Azul, and in an ideal world that will materialize. However, it should also be taken into account that, while I believe Azul is a buy, there are several factors that could weaken the business. A downturn in demand is a risk for all airlines, but for Azul the political stability or lack thereof at times could play a role, and macroeconomic cooling could hit the airlines as the Brazilian Real is a commodity currency. These factors should also be considered by investors.

For further details see:

Azul Is Flying Higher, But Its Stock Is Not