AZUL - Azul's Q1 Earnings: Results Climbing Fast But Stock Faces Turbulence

2023-05-15 14:30:46 ET

Summary

- AZUL traded lower on Monday despite robust Q1 results, an encouraging 2023 outlook, and the prospect of a cleaner balance sheet.

- Signs of demand cracks have emerged in the airline space, while stocks do not seem discounted enough to reflect the likely challenges ahead.

- Until the economic cycle resolves in favor of emerging market airlines, which may take several months, I remain neutral on AZUL.

Azul S.A. ( AZUL ) continues to post impressive numbers.

This time, the Brazil-based airline printed Q1 revenue growth of 40% year-over-year in local currency. The R$4.48 billion top-line figure represented an impressive annual increase of 15% since the comparable quarter in 2019, before the start of the pandemic. EBITDA also shot through the roof, nearly doubling on the back of strong revenues and contained costs.

Yet, AZUL traded quite a bit lower on Monday, down 4% as I write this sentence. Below, we review the company's earnings release in detail and discuss the pros and cons of the investment opportunity in this stock, whose rating I maintain at neutral.

Rising fast to 30,000 feet

Azul's revenue roundtrip from pre-COVID to the current post-pandemic environment has been one of the most impressive in the industry. The chart below shows trailing 12-month sales for Azul and some of its peers in Brazil and the US between early 2019 and early 2023. The recent Q1 results only served to underscore the full recovery in air travel activity as well as Azul's ability to perform better than its competition through the pandemic.

To be fair, Azul's January-to-March operating performance already had been preannounced , so none of the top-line numbers should have caught investors by surprise. What may have done so instead were the costs of operations. Despite per-unit revenues (PRASK, or passenger revenue per available seat kilometer) having climbed by an astonishing 23% YOY, per-unit costs ex-fuel barely moved. As a result, Azul's EBITDA margin expanded YOY by 440 basis points to 23%, despite fuel costs having climbed by more than 20%.

Elsewhere, on the three main financial statements, I was pleased to see free cash flow land at positive R$1 billion, much better than last year's negative R$420 million. The ability to produce cash flow is crucial for Azul, whose balance sheet has become debt-heavy following COVID-19, and the cost to service that debt is substantial relative to EBITDA.

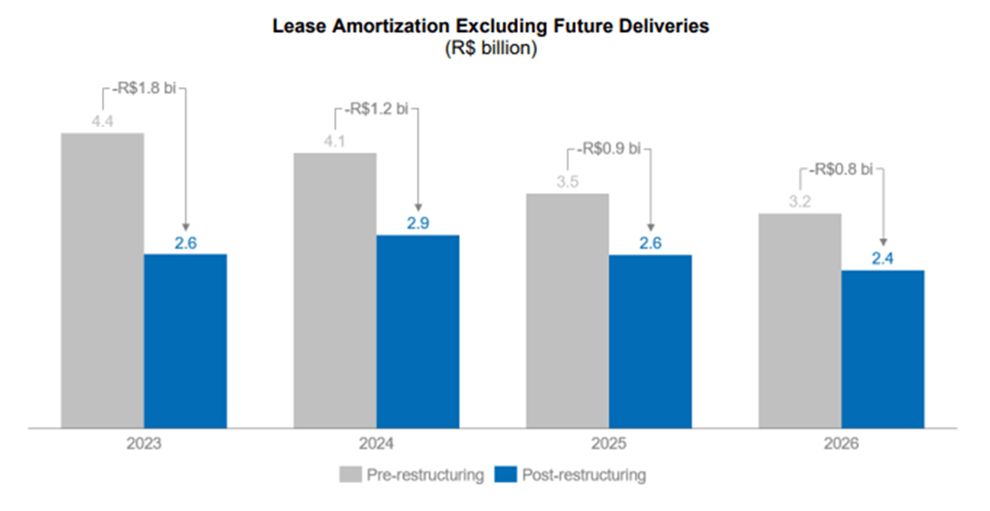

In that regard, Azul provided additional color on its efforts to restructure the company's shorter-term obligations, which effectively helps to push cash outflows further out into the future or eliminates them altogether at the expense of some equity dilution. It's hard not to see the reduction in lease payments (see chart below) through the next few years and the guided reduction in net debt-to-LTM EBITDA from 5.7x in 2022 to a projected 3.0x in 2024 as positives.

{kind=link}

Azul: Very tricky stock

Considering the above, it seems like issuing a buy rating on Azul stock would make the most sense. However, I remain reluctant to do so, given the bigger picture.

As I have argued in the past few months, a global recession seems like a near certainty to me. In fact, the key leading indicators suggest that economic deceleration and/or contraction may already be underway. Lately, signs of demand cracks have emerged in the US airline space. Meanwhile, stocks do not seem discounted enough to reflect the likely challenges ahead.

This is not to say that Azul is an overly expensive stock. As the chart below suggests, the share price in dollars is still down 83% from the pre-pandemic peak. On a forward basis, using Azul's 2023 EBITDA guidance of R$5.5 billion issued today, I estimate an EV/EBITDA of 4.2x, which is not bad. But there isn't a highly cyclical stock that could not get hurt badly by a recession, regardless of how cheaply it may be trading today.

To be clear, I think that Azul is as good a non-US airline as one can find. The management team seems to be making the right moves to clean up the balance sheet. Meanwhile, the growth strategy (new international routes, an expanded schedule at the important Congonhas airport in São Paulo) coupled with the fleet upgrade that leads to lower operating costs have been bearing fruit. Were I to enter a long-short pair trade between Azul and peer Gol Linhas Aéreas ( GOL ), for example, I would most likely be long the former.

But until the economic cycle resolves in favor of emerging market airlines, which may take several months if not a couple of years, I remain neutral on AZUL.

For further details see:

Azul's Q1 Earnings: Results Climbing Fast, But Stock Faces Turbulence