AZUL - Azul Stock Offers Major Upside

2023-08-31 12:25:11 ET

Summary

- Azul's Q2 profit jumps on lower fuel costs, leading to a tripled operating result and an 88% increase in EBITDA.

- The airline is making significant strides in deleveraging, targeting a 3.5x leverage by 2023 and 3x by 2024.

- Azul expects V-shaped growth, with a projected 70% increase in EBITDA in 2023 and results exceeding pre-pandemic levels by almost 50%.

I have been covering Azul ( AZUL ) for some time, and initially it seemed as if Azul results were improving, but its stock price was not as commodity price and forex risk as well as the political situation in Brazil cast a shadow on improving financial results. Since my March report , the stock has gained nearly a third and since my report in May, where I marked the stock a buy based on a fundamental valuation, Azul gained almost 20% compared to 9.4% for the broader markets. So, the outperformance is clear, but it is important to continue assessing its results, outlook, and valuation as I will do in this investor report.

Azul Profit Jumps On Lower Fuel Bill

{kind=link}

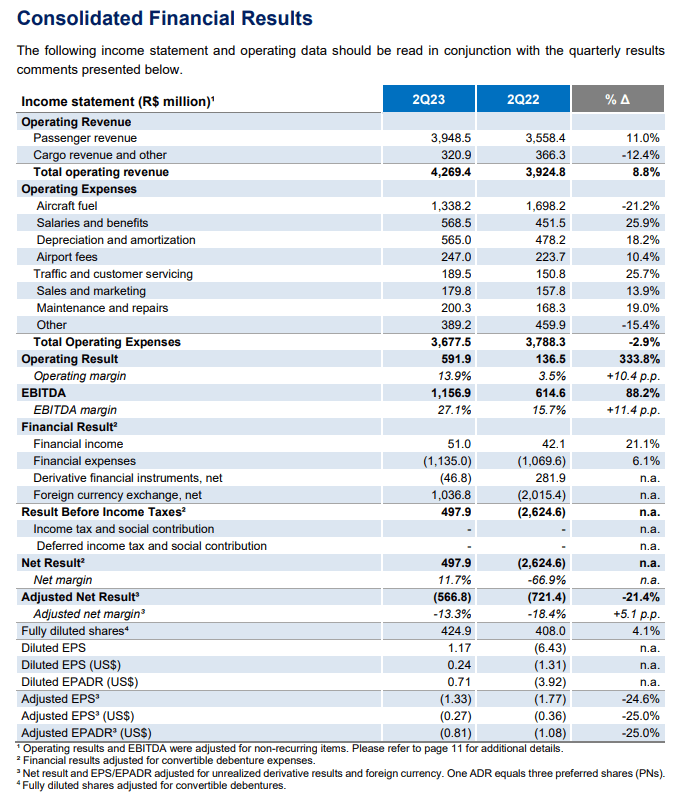

During the second quarter , revenues increased by 9%. Those who have the first quarter results fresh in their memory know that top line growth for the first quarter was 40%. So, the second quarter showed significantly lower top line growth. That, however, is also somewhat understandable given that the comp has become more challenging due to the onset of a strong demand recovery from Q2 onward last year, providing a higher basis to compare. Furthermore, the capacity increase of 8.4% on stable unit revenues were worse compared to the 20% increase in capacity and 18% increase in unit revenue seen in the prior quarter. So, indeed the growth rates are different, but we are simply comparing better comparable quarters at this stage.

Cargo revenues declined by 12.4%, which is similar to what we have observed in the prior quarter. The decline in cargo revenue really tells us that the times of booming cargo demand, where just having a plane to fill with freight and rake in profits, are over. On the passenger revenue side, we are seeing continued capacity additions, unit revenue plateauing and a better comparable base for the second quarter resulting in lower growth rates.

Operating expenses declined nearly 3% during the quarter, driven by a 21.2% reduction in fuel costs as fuel prices were nearly 25% lower. Excluding fuel costs, the costs were up 12%, which in combination with an 8.4% capacity expansion, resulted in 3.2% higher unit costs. With core inflation in the 6.6% to 7.3% range in Q2, I think the 3.2% increase in unit costs is showing strong cost execution. Overall operating results more than tripled and EBITDA jumped more than 88%.

While I like the overall deleveraging path of Azul, I do have to conclude that absent of a reduction in fuel prices, Azul would have seen no expansion on operating margins. So, while the company has been patting itself on the back for cost control, it wasn’t so much visible in the second quarter results when considering cost performance excluding fuel. At the same time, one could argue that if fuel prices would have increased, the unit revenues would also have climbed. What the year-over-year numbers also do not capture is that Azul is generating 63% higher revenues compared to 2019 and capacity per FTE is up 13% and over the past weeks, corporate travel volumes have been recovered on 50% higher fares.

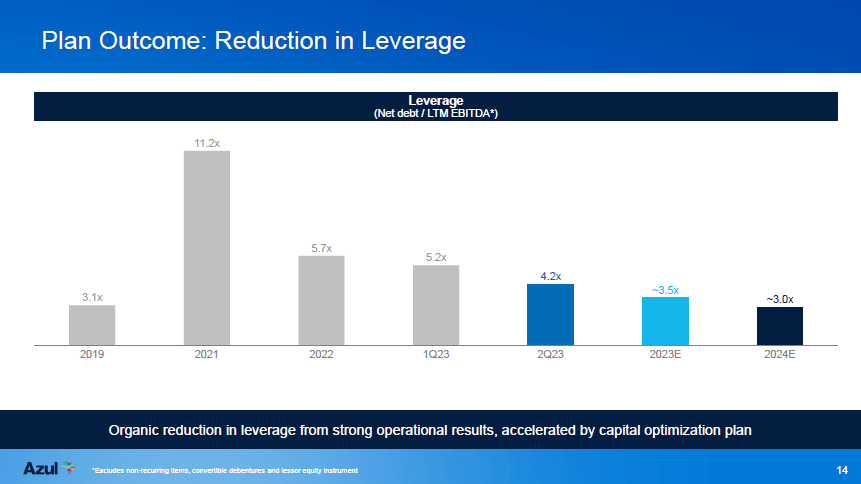

Azul Goes Strong On The Deleveraging Path

{kind=link}

For 2023, the restructuring will lead to a 35% reduction in lease payments and 27.5% in 2024. So, the lease restructuring, which is almost exclusively dollar-denominated, significantly enhances the debt balance since lease obligations are recorded as debt.

For many airlines, the big challenge on the recovery trajectory has been to deleverage, and we see that Azul is making big steps there. It is not the only airline to do so, but they are doing it. The airline ended with a 5.7x leverage in 2022 and brought that down another 0.5 points in Q1 and by another 1x in Q2, targeting 3.5x by 2023 and 3x by 2024 at which stage the leverage is back to pre-pandemic levels.

Azul Expects V-Shaped Growth

Azul has guided for R$ 5.5 billion in EBITDA in 2023, in line with its guidance update during the first quarter earnings release. The guided EBITDA would imply 70% growth year-over-year on a 14% expansion in capacity. So, the company is expecting a very strong year, and, more importantly, the results will be exceeding pre-pandemic levels by almost 50%, which is another sign of the overall successful restructuring of the business. It looks very much like a V-shaped recovery. It's not a perfect V-shape, but pretty much near perfect.

Is Azul Stock A Buy?

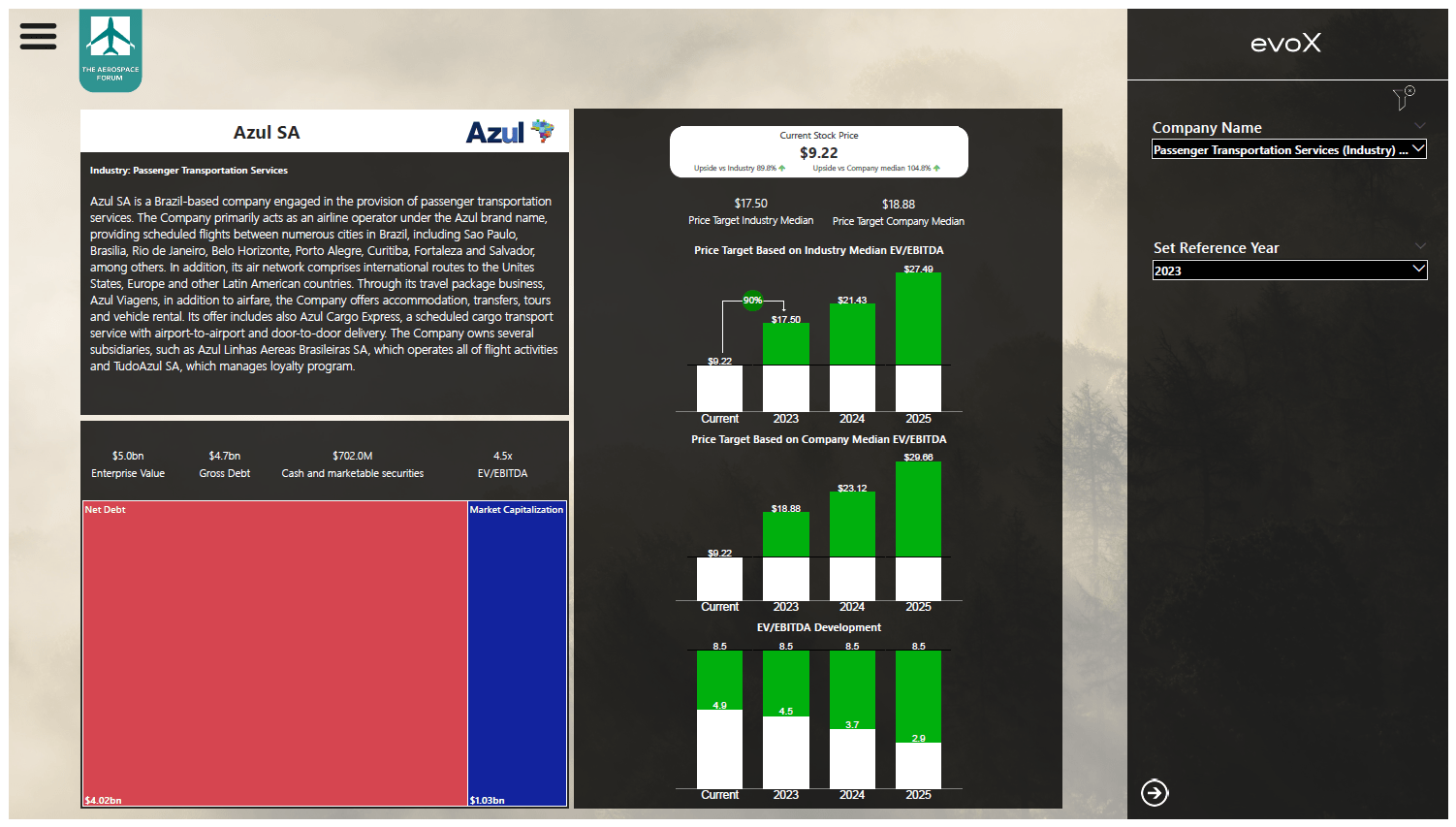

Stock price valuation for Azul using evoX Financial Analytics (The Aerospace Forum)

{kind=link}

When entering the numbers into my model, significant upside for the stock becomes visible. Based on the industry median, there is 90% upside for Azul stock in 2023 and more ahead in the years after. That is of course under the assumption that Azul reaches its ambitious targets. The company has extensively restructured its debt, of which the full effect have yet to be seen, but pro-forma figures do show that it is an overall positive for free cash and the debt maturity profile. The company has also successfully raised $800 million after the end of Q2, which I have included in the stock price valuation.

Furthermore, as part of the recapitalization plan, Azul has issued convertibles, which are exercisable after December 2024. In theory, this should not impact the valuation in 2023 and 2024, but the market is forward-looking and so the assumption more or less is that these convertibles will be swapped for equity, and it would dilute shareholders by up to 17%. Adjusting the calculated stock price targets for this, we get to a price target of $14.50 for 2023 or 57.5% upside.

Conclusion: Azul Faces A Better Future

The Q2 2023 results show margin improvement, but assessing the numbers shows that this was driven by lower fuel prices and not so much by strong efficiency gains. Azul, however, is looking beyond the quarterly results and has executed a lease restructuring plan, which should positively enhance the free cash flows in the years to come.

Even with shareholder dilution in mind assuming the convertibles that start maturing in December 2024 will be exercised, there is nearly 60% upside for the stock, which I think makes Azul stock a buy.

So far, I have been somewhat hesitant to put a buy rating on Azul stock, but with improving results and a structural reduction in big cost items, I do believe that the current share prices do not reflect these positive items and the expected earnings going forward. I see double-digit upside for Azul, and in an ideal world that will materialize. However, it should also be taken into account that, while I believe Azul is a buy, there are several factors that could weaken the business. A downturn in demand is a risk for all airlines, but for Azul the political stability or lack thereof at times could play a role, and macroeconomic cooling could hit the airlines as the Brazilian Real is a commodity currency. These factors should also be considered by investors.

For further details see:

Azul Stock Offers Major Upside