AZUL - Azul Stock: Still A Strong Buy But Watch Oil Prices And Macroeconomics

2023-11-16 14:26:58 ET

Summary

- Azul stock has outperformed the broader market, gaining 42% since May compared to a 10% gain for markets.

- Azul's Q3 2023 financial results showed growth in total revenues, driven by passenger and cargo revenues and a lower fuel bill.

- The airline has manageable debt and several growth drivers, but risks include macroeconomic factors, pricing strength and competition on routes.

Airline stocks have been under pressure in recent months as oil prices started climbing and higher labor costs are putting a more permanent pressure on airline cost structures. Azul ( AZUL ) stock, however, has done well showing share price appreciation that easily outperformed the broader markets. In August, I put a $17.50 price target representing 90% upside for Azul stock. In this report, I will analyze the most recent quarterly results and discuss why I think Azul is still a strong buy but with caution for higher oil prices.

Azul Stock: A Stellar Outperformer In Recent Months

In a report published in May, I put a buy rating on Azul stock as the company’s results had significantly improved but this was not reflected in the company’s share prices. Since then, the stock has gained 42% compared to the broader markets gaining 10%. From the time of publication of my report to the 52-week high, Azul stock even appreciated 80%.

The outperformance of Azul stock is clear as we see that U.S. Global Jets ETF ( JETS ) lost around 6.4% of its value since my buy call for Azul stock. So, it is highly interesting to analyze whether results and outlooks provide a solid base for continued outperformance.

A Discussion of Azul Q3 2023 Financial Results

{kind=link}

Azul

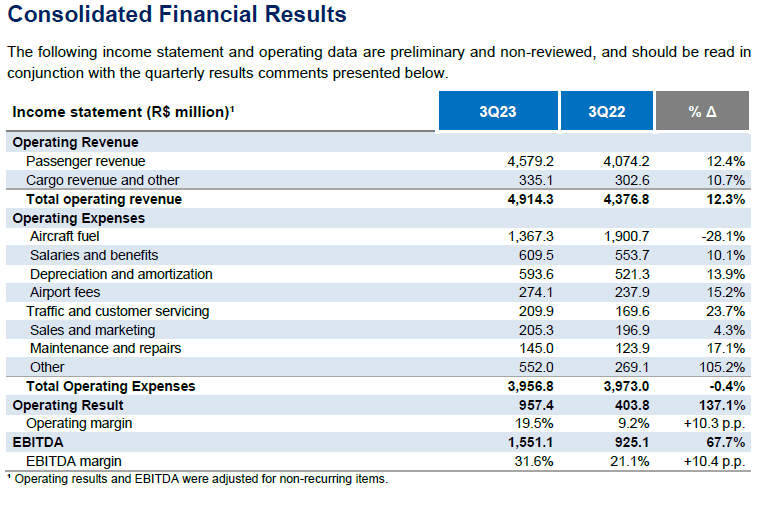

Total revenues have grown by 12.4% carried by 12.4% growth in passenger revenues and 10.7% growth in cargo and other revenues. The growth was driven by an 11.5% expansion in capacity while unit revenues increased by 0.8% and passenger air fares even increased by 5%. This already gives somewhat of an indication why Azul stock has been outperforming peers in the US where unit revenues have been dipping year-over-year. Also interesting was the growth in cargo revenues, which also goes against the trend of declining cargo revenues and was driven by strong domestic demand.

On the cost side, operating costs excluding fuel grew 25% driven by a combination of typical higher costs on international routes and higher capacity operated. The real cost element that was a benefit to the bottom line was the lower fuel bill which brought the total operating expenses in line with last year and led to operating profit improve 137% to R$957.4 million and EBITDA margins of 31.6%.

While I do like the results, I think it's fair to point out that the strong results were achieved by relative stability in the unit-revenues and a lower fuel bill. Unit costs excluding fuel for example were up 12% which also includes inflation and weakening of the Brazilian real against the US dollar. An element that's difficult to account for is the fact that there's more high international travel related costs for Azul as well which also skews things. So, I wouldn’t say the cost execution is or was bad, it was probably as good as it can get but there are some pressures still.

It's also not the case that we can equalize the fuel costs on a year-over-year basis as this would not incorporate any ability to pass through of fuel costs to the top line, but if we were to do this the Q3 2023 fuel bill would have been R$670 million higher and slim the operating margins to 5.8% compared to the 19.5% reported now. What this does tell us is that margin protection stands or falls with passing through the fuel price fluctuations to passengers.

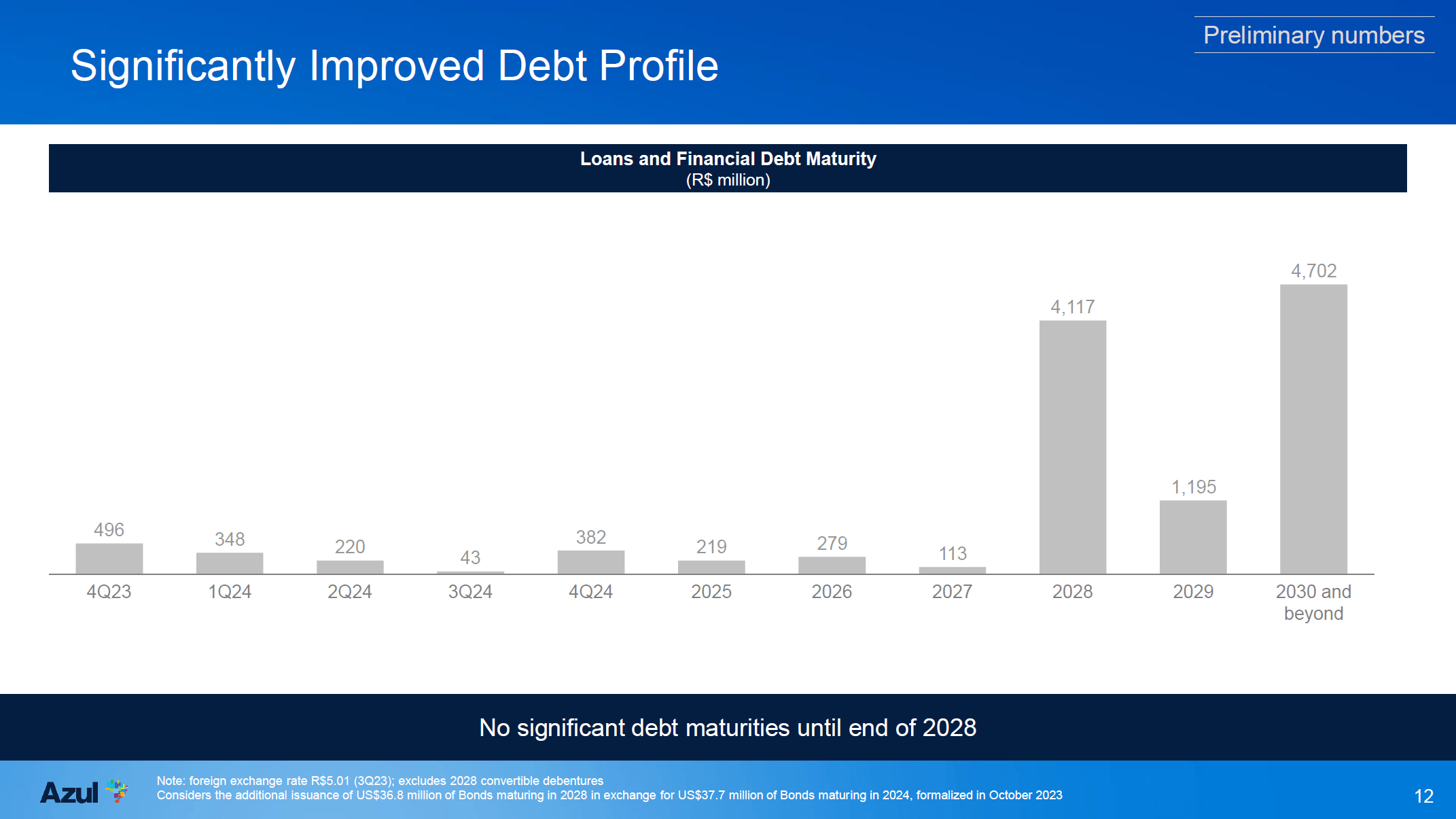

Azul Has Extremely Manageable Debt

{kind=link}

Azul

During the quarter, liquidity increased to roughly R$3.5 billion from R$2.1 billion after a R$4 billion raise. Some of the proceeds were used to pay down debt in the coming years providing Azul with an extremely manageable debt maturity profile as debt obligations are minor until 2027. Normally we see more details in terms of leverage, but those details are not available yet as the recapitalization plan is rather complex and as a result the audited financial report has yet to be published.

What's The Price Target For Azul Stock?

{kind=link}

Azul

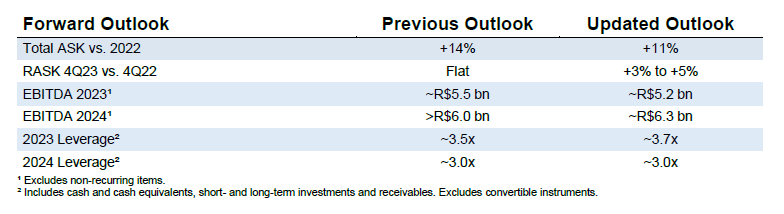

As the detailed financial report has not yet been published, I'm currently unable to provide an updated price target and maintain my $17.50 price target noting that the capacity increase this year will be lower than previously expected due to delivery delays which positively layer into the unit revenues which are now expected to be up 3% to 5% compared to a previous flat outlook. Driven by higher fuel prices, Azul expects R$300 million lower EBITDA in 2023 but has increased its outlook for 2024 which can either be interpreted as the missed profits for 2023 slipping into 2024 or the initial >R$6 billion outlook being detailed to approximately R$6.3 billion in EBITDA. As a result of the adjustments to guidance, leverage will be slightly higher than initially anticipated for 2023 while remaining unchanged for 2024.

As soon as the audited financial results are released I will be able to provide a full review of the stock price target which I would expect to be slightly lower for 2023, but still provide significant upside.

What Are The Growth Drivers For Azul?

Many of the growth drivers can also turn into risks. Those drivers include lower fuel prices and less negative forex impact. Beyond that, however, Azul has some operational growth drivers that we could be seeing on annualized scale next year. Those include the full year impact of the growth of the Embraer ( ERJ ) E2 fleet which provides a significant reduction in fuel consumption compared to the previous generation airplanes and somewhat shields the company from oil price fluctuations which is extremely important given that fuel prices are the highest in the world as claimed by Azul CEO John Rodgerson:

Remember, though, that fuel prices are still higher than 2019 and fuel prices in Brazil are the highest in the world.

Significant strength in the business also exists because the airline is the only operator of 80% of the routes and accounts for 90% of the departures. Furthermore, due to slot allocations effective late March 2023 Azul has increased doubled its slots at Sao Paulo Congonhas Airport meaning that in 2024 we will see the full year effect of that slot allocation in the results.

Azul also indicated that fares need to be in line with the cost of capital and fuel prices, which strictly speaking means that Azul will be looking to pass through some of the added costs it might see to the consumer with a longer term objective to get more of the Class C (lowest rank of middle class in Brazil) to fly. For Azul the trick will be get more people to fly and also guard its business against the cost fluctuations and it's looking at the Brazilian for that although it is not quite clear what measures Azul hopes to see or not see from the government. Either way Azul, has been one of the few airlines guiding for higher unit revenues in Q4 and among its competitors it has the lowest unit cost structure.

What Are The Risks For Azul?

The risks for Azul are mostly related to macroeconomics. The Brazilian real is a commodity currency meaning that its value mostly fluctuates with commodity prices and as there are concerns about the economic growth not only in Brazil but also globally, that could result in weakening of the Brazilian real and affect Azul’s business beyond any demand impact. Fluctuations in oil prices are another risk and I think we're already seeing that with the downward EBITDA guidance for Q4 and the fuel price normalization that I applied to Q3 2023 already showed that Azul’s ability to price in higher cost items are extremely important to its ability to execute its ambitious path forward.

Another risk for which there currently is no evidence that it will happen is that airlines will start competition on the routes where Azul currently is the only operating airline.

Conclusion: Azul Is Still Attractive

I think Azul is still extremely attractive with around 70% upside for 2023 against my previous price target that I will update once the audited financial report is published. Q3 2023 showed the positive impact of the fuel bill on results and what I will be watching in the quarters ahead is how much of the costs increases in for instance oil prices Azul can pass through to the flying public as that is key to remain on track for its annual targets. With oil and forex playing such an important role, one could be expecting a downgrade for the stock as the guidance for 2023 has been revised downward but I would like to point out that Azul currently is not even valued according to its 2023 earnings and in several weeks it will be 2024 and in case Azul stock does not appreciate, it would mean that Azul is not valued according to its 2023 earnings let alone its 2024 earnings.

All in all, the financial report which better profiles the expected cash flow includes balance sheet data will provide better insights on whether we have to adjust our 2023 expectations for the stock.

For further details see:

Azul Stock: Still A Strong Buy But Watch Oil Prices And Macroeconomics