BGS - B&G Foods: In Need Of A Major Strategic Shift

2024-01-05 17:20:09 ET

Summary

- B&G Foods is facing structural and financial challenges, with declining sales volumes and increased competition across major brands.

- The company's aggressive growth strategy through acquisitions has left it overleveraged and with limited cash flows.

- A turnaround seems unlikely given the structural declines in the center-store grocery categories that B&G competes in.

Investment Thesis

B&G Foods (BGS) is a packaged foods company that has aggressively grown through acquisitions over the years, but is now facing structural and financial challenges. The company is seeing concerning declines and increased competition across major brands like Green Giant and Crisco with multiple brands having falling sales and volumes. The acquisitive growth strategy has also left B&G overleveraged, with limited cash flows to support operations and capital allocation. There also appears to be inefficient use of capital with the continued dividend payouts despite organic struggles. A turnaround looks unlikely given structural declines in the center-store grocery categories that B&G competes in. This offers limited upside even at the currently depressed valuation.

With limited catalysts for multiple expansion, I'm rating B&G Foods a Sell. Any upside in the stock relies on flawless execution of a turnaround which seems unlikely unless there are major strategic shifts. The business is facing structural pressures across its brand portfolio along with a stretched balance sheet. Cost-cutting and financial engineering will not be enough to drive growth in the current environment. Significant innovation, brand reinvestment, and shifting of resources to faster-growing categories would be needed to alter the trajectory of the business.

Company Deep Dive

B&G Foods primarily competes in the center-store grocery section with shelf-stable and frozen foods. Its portfolio consists of 50+ brands spanning baking ingredients, condiments, meals, vegetables, syrups and more. The company has aggressively grown sales by acquiring brands like Green Giant (2015), Crisco (2020), Clabber Girl (2019) and others.

However, the base business is now struggling with structural decline across its categories:

Leading Brands Facing Competition: Flagship brands like Green Giant saw a 10.7% sales decline in Q3 as the frozen category is losing share to fresh produce based on the lower price differential. B&G's Crisco oils and shortening also saw a 16.4% sales drop in Q3 as private label gained share. The issue seems to be widespread rather than isolated.

Elasticity Kicking In: B&G has taken significant price increases in 2022-2023 to offset input cost inflation. But volumes are declining showing elasticity. Brands like Ortega Mexican Foods saw a 4.3% sales decline in Q3 despite pricing gains.

Lack of Innovation: Beyond pricing, B&G has failed to expand distribution or gain share through innovation. There hasn't been any mention of major new products driving growth, showing an innovation void.

Divesting Declining Assets: B&G recently sold the shelf-stable Green Giant canned vegetable business in the U.S. but held onto the struggling frozen division, showing its options to reignite sales are limited.

The shift away from traditional center-store grocery brands does not bode well for B&G's portfolio. Categories like baking ingredients, canned vegetables, plain oats and others face structural pressure from fresh perimeter departments, private label growth and discount banners.

B&G's heavy debt load also limits its ability to invest behind brands to drive relevance. Given the widespread declines across its brand portfolio so far, an inflection looks unlikely without major strategic changes.

Financial Profile

B&G Foods holds significant debt of $2.1 billion resulting in a Debt/EBITDA ratio of 6.5x as of Q3 2023. This leaves the company with limited financial flexibility for turnaround efforts. The asset side of the balance sheet seems to be mostly inflated by intangible items.

Its recent sale of Green Giant's shelf-stable business was used to repay debt instead of re-investing for growth. Cash interest expense was $35.9 million in Q3 2023, consuming ~45% of Adjusted EBITDA.

Debt reduction efforts are commendable, but the company continues to pay a large dividend with a yield of 7% despite facing organic struggles. This raises questions about efficient capital allocation.

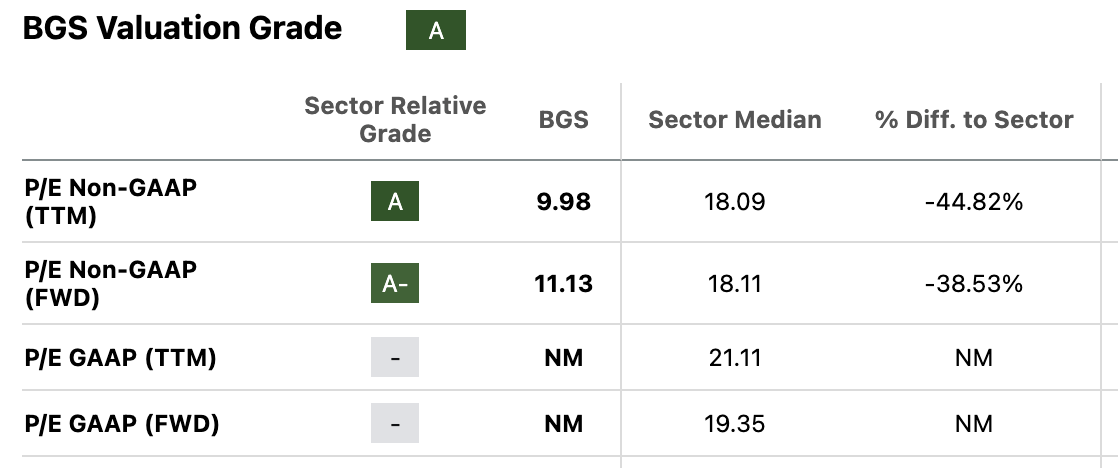

Valuation

Despite the business challenges, B&G Foods trades at a forward P/E of 11x as of writing, which is way below the sector median.

{kind=link}

This discounts the poor trends and leaves some margin of safety from a valuation perspective even if fundamentals deteriorate further. To some, this may seem like a value play on the long side, but investors should be wary of owning a structurally challenged business even at a low valuation.

For the stock to re-rate higher, B&G needs to show an ability to reignite top-line growth and market share gains. Until then, I see the stock trading sideways at best amidst declining sales volumes.

Catalysts to the Downside

1) Input cost inflation returning to squeeze margins

2) Continued market share losses to private label and smaller competitors

3) High leverage leaving little room for more acquisitions and investments

4) Possible cuts to dividend if cash flows remain pressured

Catalysts to the Upside

The upside relies on B&G perfectly executing a turnaround despite its balance sheet constraints and structural shifts away from its categories. This seems unlikely unless there is a major change in strategy. Potential risks to my thesis are:

1) Sales re-acceleration of Green Giant frozen foods and Crisco in grocery

2) New product innovations that drive market share gains

3) Using ongoing balance sheet easing for a transformative acquisition

However, I view the above as low-probability events given management commentary on competition and lack of discussion regarding major strategic actions in the underlying businesses other than financial engineering.

Conclusion

B&G Foods is struggling with sales declines across major brands, showing its portfolio faces structural challenges in light of the shift away from traditional center-store grocery brands. The company's high financial leverage leaves little room for cash flows to fund a turnaround, and continued large dividend payouts highlight inefficient use of capital. Without a major strategic shift and top-line growth in underlying businesses, the upside in the stock looks limited even at the currently depressed valuation.

For further details see:

B&G Foods: In Need Of A Major Strategic Shift