BGS - B&G Foods: Slight Margin Improvements But Future Growth Remains A Concern

2023-08-21 02:56:09 ET

Summary

- B&G Foods pursued an expansion strategy relying on high levels of debt, leaving them vulnerable to ongoing challenges.

- Q2 2023 earnings report showed improvements in cash flow and operational margins, but volume decline and competition remain concerns.

- BGS stock has lost 62.29% in value over the last five years, indicating a lack of long-term growth potential. Sell position recommended.

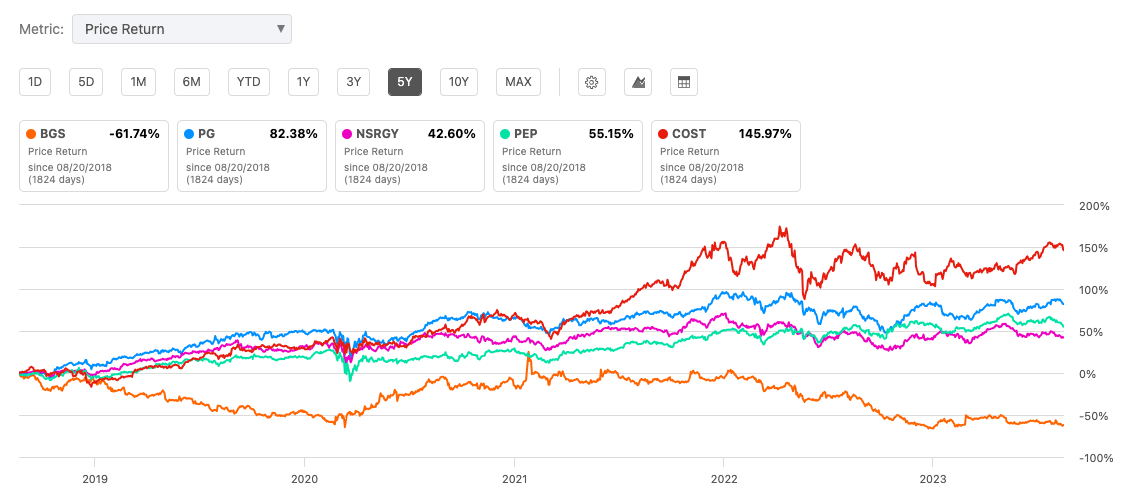

Half a financial year has passed since my previous article on B&G Foods, Inc. ( BGS ). I recommended a sell rating due to the company's high variable interest debt intake, rising costs cutting into its margins, unsustainable dividend, declining bottom line and a lack of significant future growth potential. B&G is divesting to improve its fundamentals. However, the company is still sitting with a considerable problem; across many of its brands, sales are in decline. Over the last five years, this stock has experienced a significant drop of 61.74% in value, a sharp contrast to the more positive performance of other consumer staple companies.

Five year stock trend versus consumer staple peers (SeekingAlpha.com)

{kind=link}

Although the company beat EPS and revenue expectations in the most recent Q2 2023 Earnings report , overall, we still see a decline in the top and bottom-line results. Unfortunately, without making substantial changes, having a positive outlook for the company's future is challenging. Therefore, my recommendation remains a sell for this stock.

Company overview and updates

B&G Foods has long pursued an inorganic growth strategy by acquiring a diverse range of less popular brands and incorporating them into its portfolio. This approach relies on the company's distribution network and marketing expertise to revitalise and expand the acquired products. While successes like Pirate's Booty, which was bought for $195 million in 2013 and sold to Hershey ( HSY ) in 2018 for $420 million, showcase this potential, the model necessitates substantial debt intake and carries inherent risks, as not all acquisitions yield profitability. The sale of Back to Nature to The Barilla Group recently impacted the top line, underscoring the risks. With revenue declines apparent across multiple brands, this inorganic strategy introduces a higher risk profile than industry peers.

Q2 2023 versus Q2 2022 (Sec.gov)

{kind=link}

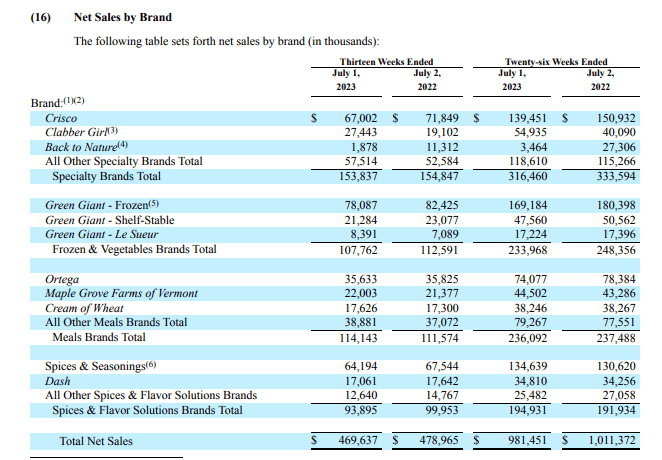

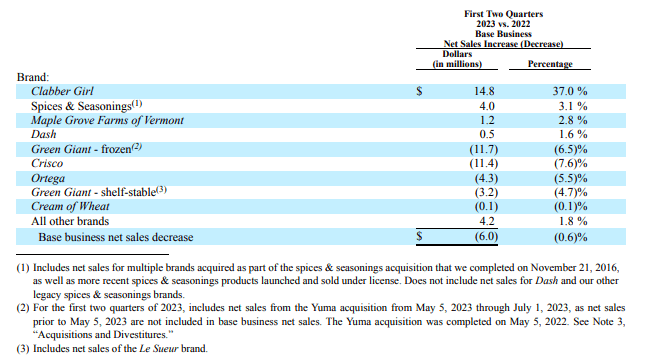

Looking at the different brands' performance over the last six months, we see many brands declining. Green Giant- frozen and Crisco are responsible for a more substantial portion of total sales, and we can see that the two have fallen by 6.5% and 7.6% YoY. Crisco experienced high price elasticities and lower volumes due to pricing strategies, while Green Giant faced volume declines due to the discontinuation of certain products and competitive pricing.

Brand sales first half 2023 versus first half 2022 (Sec.gov)

{kind=link}

Financials and valuation

Despite declining revenue compared to the previous year, the company's results were better than expected. Some of this decline was due to the divestment of Back to Nature. One positive aspect of the earnings report was the gross profit margin increase. However, compared to other companies in the industry, it is still apparent that the margins are pretty low. Rising inflation will also make it challenging to keep costs under control. I have compared B&G Foods with top consumer staple companies such as Procter & Gamble ( PG ), Nestle ( OTCPK:NSRGY ), PepsiCo ( PEP ) and Costco (COST) to put the margins into perspective.

Profitability margins versus peers (SeekingAlpha.com)

{kind=link}

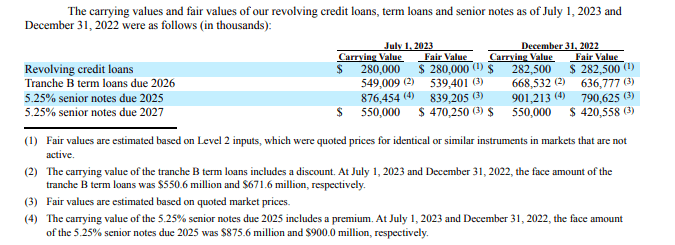

Over the last quarter, the company's cash from operations improved, and it strengthened its balance sheet. B&G Foods generated $132.4 million in net cash from operations during the first half of 2023, compared to $21.1 million in the first half of 2022. Inventory has been reduced by $50 million since the start of the year and is at $675 million. Below is an overview of the revolving credit loans and notes due in the upcoming years.

Credit loans and notes due (Sec.gov)

{kind=link}

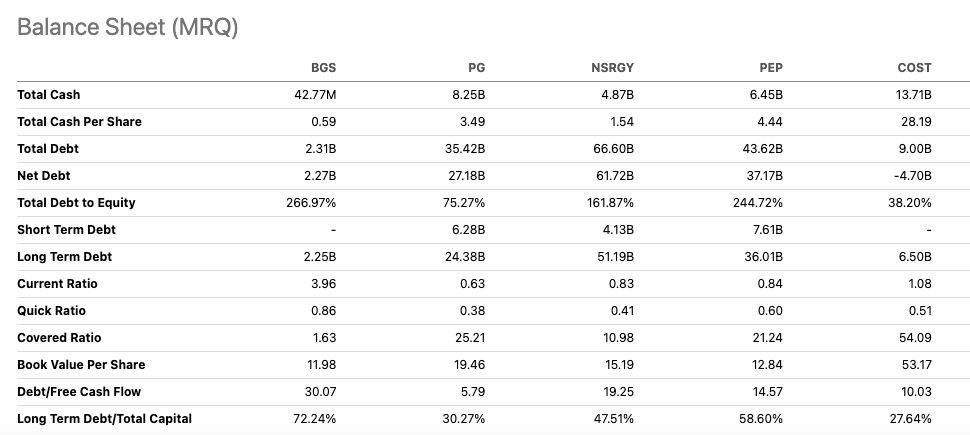

When evaluating the TTM results of the company and comparing them to its peers in the industry, it is important to note that there is a high level of debt intake in comparison to larger peers. This is a cause for caution.

Balance sheet versus peers (SeekingAlpha.con)

{kind=link}

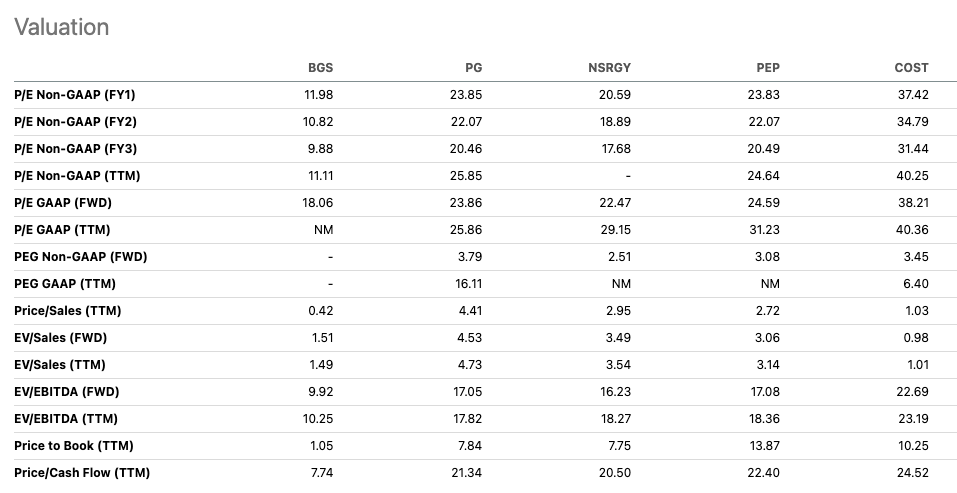

B&G Foods has an attractive FWD price-to-earnings ratio relative to its peers at 18.06 and a low price-to-book ratio of 1.05. However, investors should remain cautious that the company's bottom line has been in decline across five years, and the company is in a difficult financial position which has made it cut its dividend and will be looking again at divesting brands to better its financial situation.

Relative peer valuation (SeekingAlpha.com)

{kind=link}

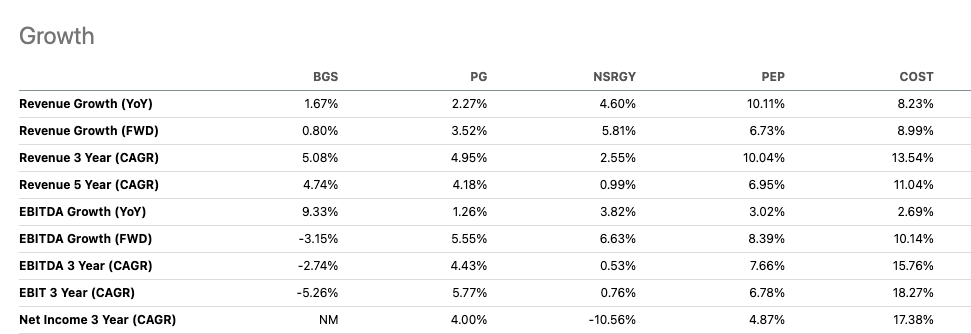

When compared to its peers, B&G Foods appears to be lagging behind in terms of growth.

Growth versus peers (SeekingAlpha.com)

{kind=link}

Risks

B&G Foods faces tough competition in the food industry, with established and emerging players vying for market share and potentially affecting prices. Investors should be aware of declining sales across many brands due to pricing elasticity and competitive pressures. Although profit margins improved this previous quarter, the company has indicated that future improvements may slow down, particularly in FY2023. Ongoing fluctuating interest rates and macroeconomic trends could also continue to impact financial performance.

Final thoughts

Although B&G Foods exceeded expectations regarding EPS and revenue in the latest quarter, they faced significant challenges. While margins have improved, volumes have declined, and brand-related hurdles are causing concern. Additionally, there are limited growth prospects for the remainder of the year and macroeconomic uncertainties to consider. Given the struggles with some of its key brands, high levels of debt, and other consumer staple companies performing better in the current environment, I recommend maintaining a sell position.

For further details see:

B&G Foods: Slight Margin Improvements But Future Growth Remains A Concern