BGS - B&G Foods: Too Expensive Even With A Single-Digit Forward P/E

2023-10-27 08:45:10 ET

Summary

- B&G Foods sells food products under a wide portfolio of brands.

- The company has poor financials, as the company's organic growth is bad, the company's EBIT margin has been falling, and it holds a significant amount of debt.

- Although the stock seems cheap at the current price, I believe it is still overpriced, as my DCF model estimates a significant downside.

B&G Foods ( BGS ) produces and sells food products under a numerous amount of brands and categories. The stock has been on a decline in the long term as well as short term as the company’s organic performance has been very poor – to fuel B&G Foods’ growth, the company has had a spree of acquisitions. Although the stock seems cheap with a forward P/E, I believe that the stock is still overvalued; I have a sell-rating for B&G Foods.

The Company & Stock

B&G Foods manufactures a large amount of different food products. The company’s food product categories include baking, dressings, meal solutions, sauces, seasonings, snacks, soups, and syrups among other categories. The company owns a wide portfolio of brands, totalling up to more than fifty brands. B&G Foods’ brands include names such as Clabber Girl, Cream of Wheat, Crisco, Cinnamon Toast Crunch, Devonsheer, Maple Grove Farms, and Old London.

As most of B&G Foods' portfolio relies on around basic food products, the company isn’t very exposed to macroeconomic risks – food is a basic necessity, so demand around products such as meal solutions, sauces, and soups stays very stable. In the current economy, I believe that a non-volatile offering in terms of the macroeconomic could prove to be valuable.

B&G Foods’ stock price has plummeted in the past ten years, losing three quarters of the stock’s value in the period:

{kind=link}

Ten-Year Stock Chart (Seeking Alpha)

The company’s investors have relied on a significant dividend. Currently, the company’s estimated forward dividend yield stands at 9.08% after the dividend was significantly cut in late 2022 from a quarterly dividend of $0.48 to a quarterly dividend of $0.19.

Financials

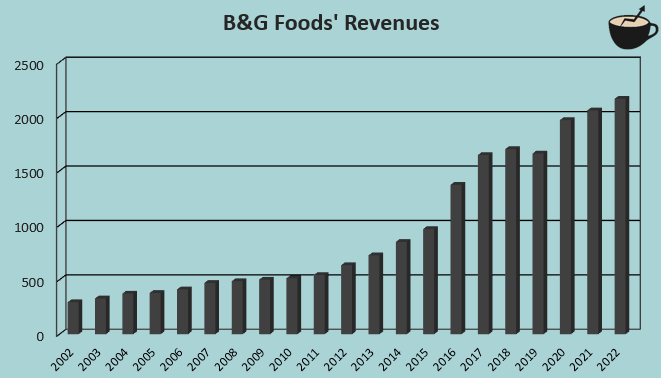

At first glance, B&G Foods’ historical growth has been excellent – from 2002 to 2022, the company has achieved a compounded annual growth rate of 10.5%, leaving investors wondering why the stock price has been on a slow downfall:

{kind=link}

Author's Calculation Using TIKR Data

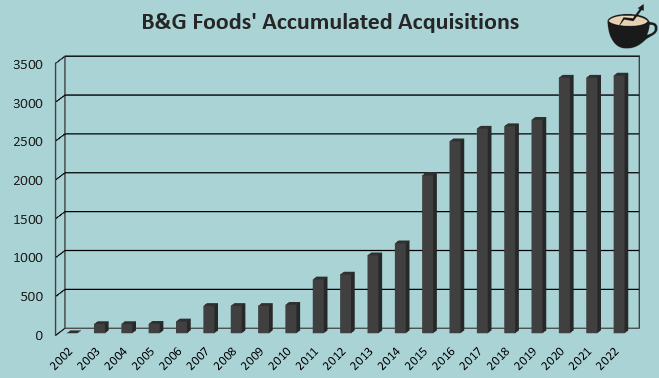

The disconnect between B&G Foods’ revenue growth and stock price is a result of the source of the growth: it seems that the company’s growth has been achieved only through extensive acquisitions. From 2002 to 2022, B&G Foods’ accumulated acquisitions add up to an amount of $3.3 billion – compared to the company’s current market capitalization of $0.6 billion and EV of $2.9 billion, the acquisitions seem to have only deteriorated in value.

{kind=link}

Author's Calculation Using TIKR Data

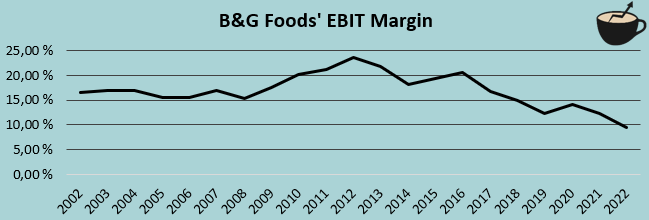

After the peak in 2012, B&G Foods’ EBIT margin has mostly been falling. From 2002 to 2022, the company’s average margin is 17.0%, with the current trailing margin only standing at 11.0% . The margin is on a slight upward trend in 2023 so far, as in 2022 the achieved margin was 9.4%. In 2022, the margin seemed to be tighter due to cost inflation; I believe that the current level is more representative of a sustainable margin in the medium-term.

{kind=link}

Author's Calculation Using TIKR Data

To finance the constant acquisitions, B&G Foods has had to draw an immense amount of debt. Currently, B&G Foods has long-term debts totalling over $2.2 billion on the company’s balance sheet . Compared to the market capitalization of $0.6 billion, the amount seems very excessive. In the last twelve months, interest expenses have been around 62% of B&G Foods’ EBIT.

Valuation

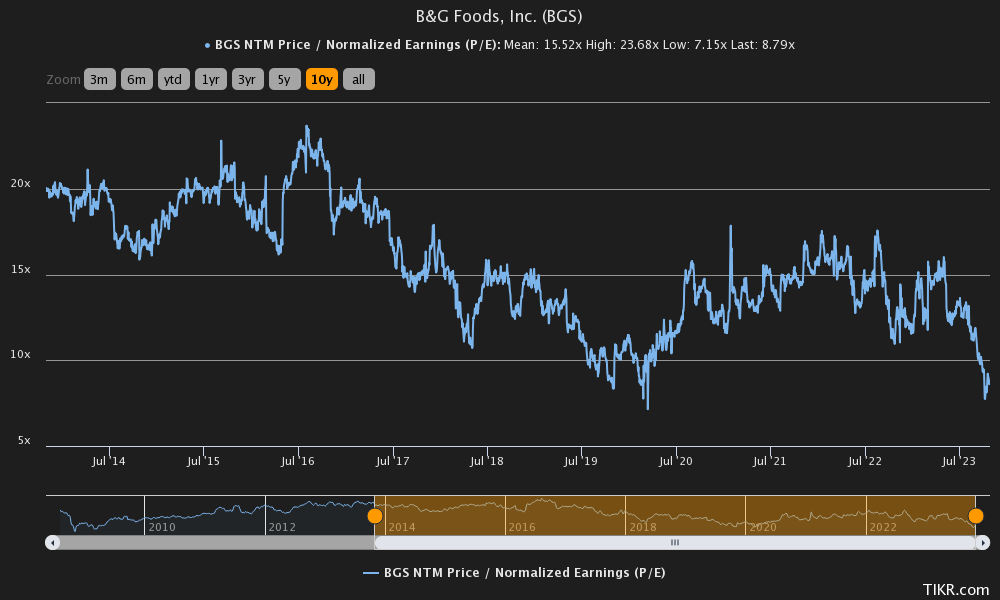

From the stock’s forward P/E ratio, it seems that the clearly poor organic performance is priced into the stock, as the current forward P/E stands at 8.8, significantly below the ten-year average of 15.5:

{kind=link}

Historical Forward P/E (TIKR)

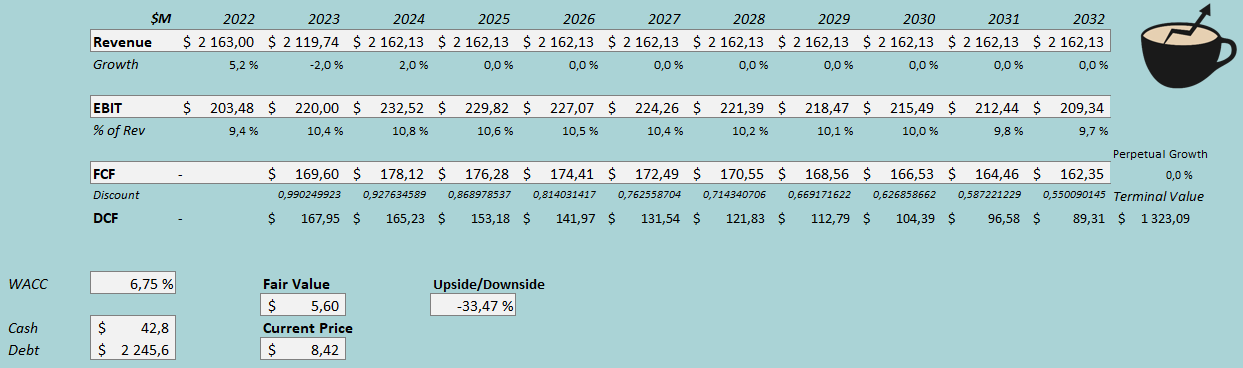

As B&G Foods’ EBIT margin history and organic growth has been poor, the cheap P/E ratio can be a deadly trap for investors. To further analyse the valuation and to get a rough estimate for a fair value, I constructed a discounted cash flow model as usual. In the model, I estimate B&G Foods’ revenues to fall by 2% in the current year, along the company’s guidance. After 2023, I estimate a slight growth of 2% as inflation is still partly heightened. After the year, I estimate a nominal growth of 0% - the company’s organic performance has been very poor historically, and I don’t see any catalysts for a better performance in the future.

As for the company’s EBIT margin, I estimate the margin to stay at the current trailing level of 10.4% for 2023. After 2023, I estimate some more margin expansion as a result of a possibly better economy. Yet, the company’s long-term margin history has been poor - I estimate B&G Foods’ EBIT margin to start falling slightly in 2025 and beyond into a perpetual EBIT margin of 9.7%. The company has a mostly good cash flow conversion as a result of a large amount of depreciation in B&G Foods’ accounting earnings.

The mentioned estimates along with a cost of capital of 6.75% craft the following DCF model with a fair value estimate of $5.60, around 33% below the price at the time of writing:

{kind=link}

DCF Model (Author's Calculation)

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

B&G Foods had around $36 million in interest expenses. With the company’s current interest-bearing debt balance, the company’s current interest rate comes up to an annualized figure of 6.38%. The company utilizes a very high amount of debt and seems to have done so for a long period of time – I estimate a very high long-term debt-to-equity ratio of 50% for the company.

On the cost of equity side, I use the United States’ 10-year bond yield of 4.96% as the risk-free rate. The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate made in July for the United States. Yahoo Finance estimates B&G Foods’ beta at a figure of 0.55 . Finally, I add a small liquidity premium of 0.5% into the cost of equity, crafting the figure at 8.71% and the WACC at an astonishingly low 6.75% - investors shouldn’t expect a large return from the stock, but not a ton of risk either.

Takeaway

B&G Foods checks multiple signs of a value trap. The company has a seemingly low P/E ratio with a stable product. The company has achieved some growth in the company’s history, but under the surface, the achieved growth is hiding a very poor organic performance. The company also has a very significant amount of debt, leveraging potential risks for investors. At the current price, my DCF model also estimates the stock to be overvalued – for the time being, I have a sell-rating.

For further details see:

B&G Foods: Too Expensive, Even With A Single-Digit Forward P/E