RILYP - B. Riley Financial: The Bonds Preferreds And Commons Are Undervalued Against Risks

2023-12-17 23:11:11 ET

Summary

- The bear-induced pullback of B. Riley Financial has created an opportunity to build a position in its preferred shares RILYP.

- Total cash and investments of $2.05 billion at the end of the recent third quarter provide a near-fortress balance sheet to meet the $2 million per quarterly preferred payments.

- Despite recent headwinds, RILY has a strong potential for recovery with a favorable outlook for profit growth on a Fed funds rate cut.

B. Riley Financial ( RILY ) is an extensive and inherently complex company with six revenue-generating segments including capital markets, wealth management, and financial consulting. The common shares are down materially over the last few months on the back of a short call that raised concerns about its links to Franchise Group. RILY participated in the November $2.8 billion management buyout of previously NASDAQ exchange-listed FRG, investing $217 million. FRG owns several franchisable brands from the Vitamin Shoppe, an omnichannel specialty retailer of supplements and vitamins, to the pet-specialty store Pet Supplies Plus. The level of bearish sentiment is intense with a 53% short interest in the common shares rendering RILY as one of the most highly shorted stocks in the market. Downside volatility has been compounded by end-of-year tax loss harvesting, an executive margin call , and an S&P credit rating downgrade of FRG to "B-" from "B".

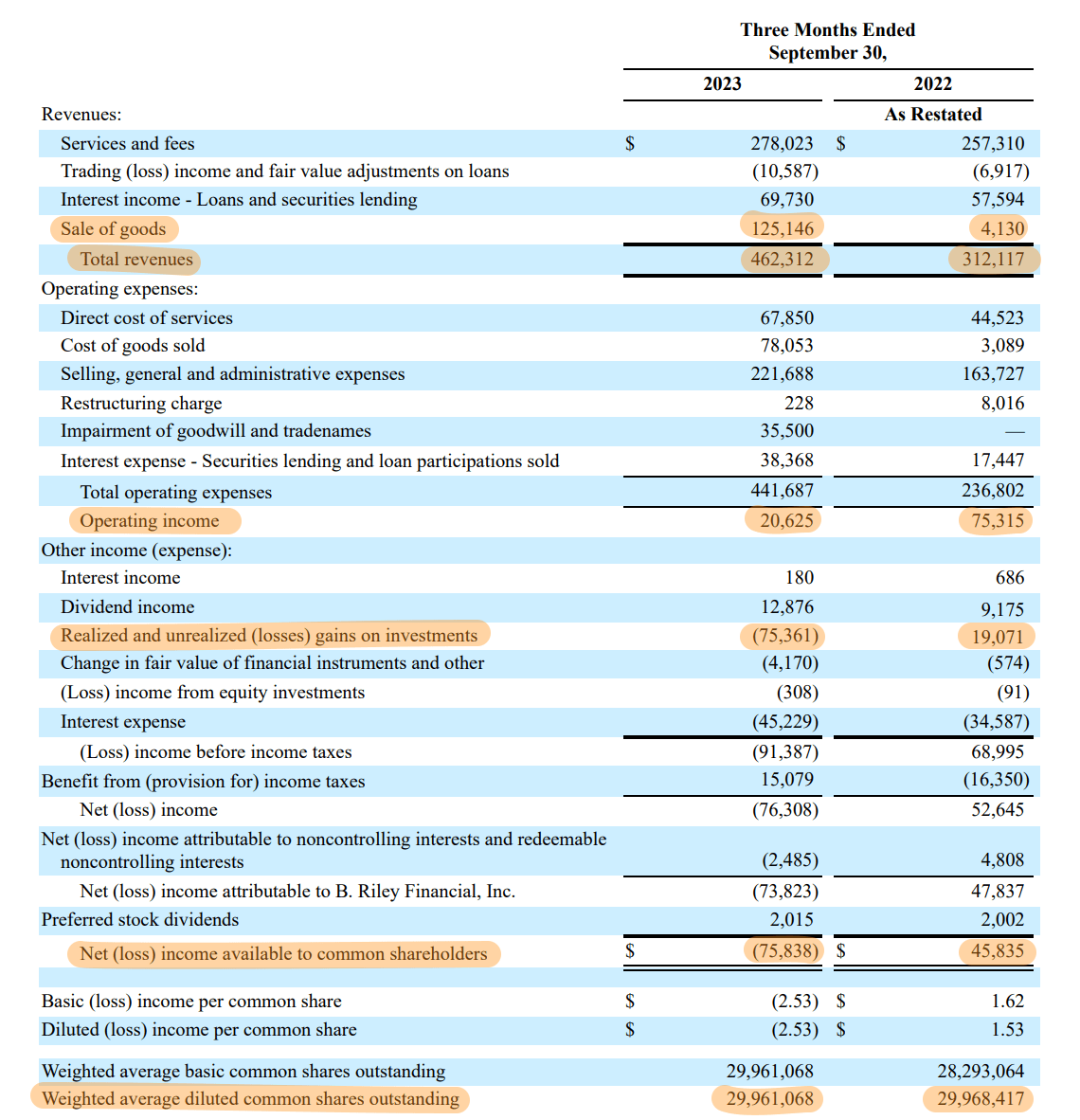

RILY also last declared a quarterly cash dividend of $1 per share , unchanged sequentially for what's currently a roughly 20% annualized forward dividend yield. The fat yield reflects market angst over the sustainability of the current distribution with RILY not covering the payout through its current earnings. A 20% dividend yield is not normal for any sector and the market is calling RILY's bluff on its ability to maintain the current distribution. RILY recorded revenue of $462.31 million for its fiscal 2023 third quarter, up 48% from its year-ago period with year-to-date revenue running at $1.30 billion for the first nine months of 2023, up 86% over the year-ago comp.

Recent Headwinds But Strong Balance Sheet And Fed Pivot Set Conditions For Recovery

B. Riley Financial Fiscal 2023 Third Quarter Form 10-Q

{kind=link}

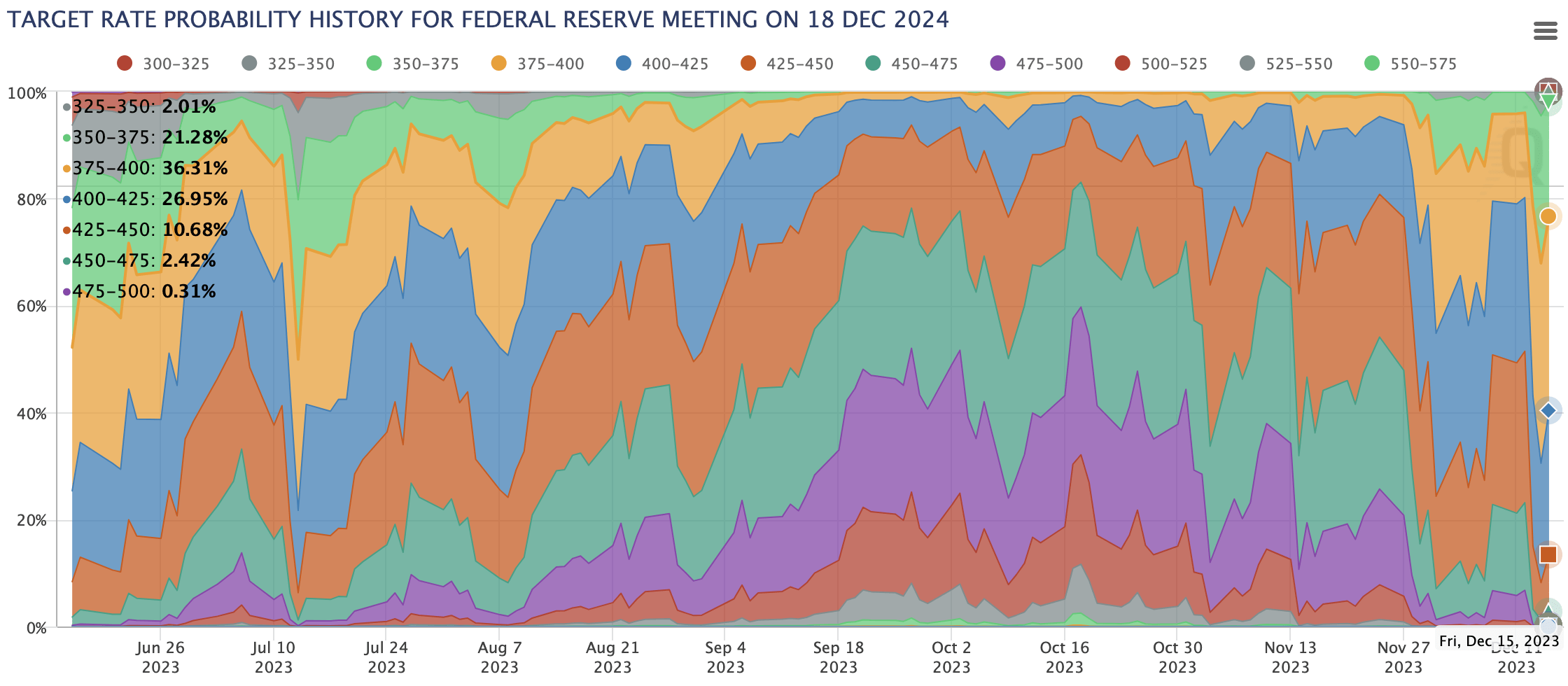

The company recorded a net loss of $75.84 million for the third quarter with underlying free cash flow negative at $120 million , a sequential deterioration. Third-quarter earnings were not great and the current selloff reflects that to an extent. The uncertainty now is how much is too much as RILY still recorded growth during the third quarter and is set to materially benefit from a pullback in the Fed funds rate. Capital market activity has dropped to record lows and the Fed's December dot plot is showing at least 3 interest rate cuts of 75 basis points in 2024. The CME FedWatch Tool is pricing in at least 2x this level of cuts with the base case for 2024 set to see the Fed funds rate at 3.75% to 4.00% , a 150 basis points decline versus current levels.

{kind=link}

Critically, RILY is now trading at its lowest price-to-sales multiple in over a decade despite the positive future outlook for revenue growth next year as rate cuts improve the backdrop for currently dire capital market conditions and boost the valuation of private and public equity. RILY's profitability has been lumpy on the back of poor conditions since the Fed started raising rates. However, the business is highly diversified and its investment banking segment is set to see a pickup next year. This outlook comes wrapped with an ever-increasing probability of the US avoiding a recession. The situation is fluid but non-farm payrolls continue to outperform expectations and US GDP is forecast for growth with the Atlanta Fed currently estimating a 2023 fourth-quarter GDP growth rate of 2.6% .

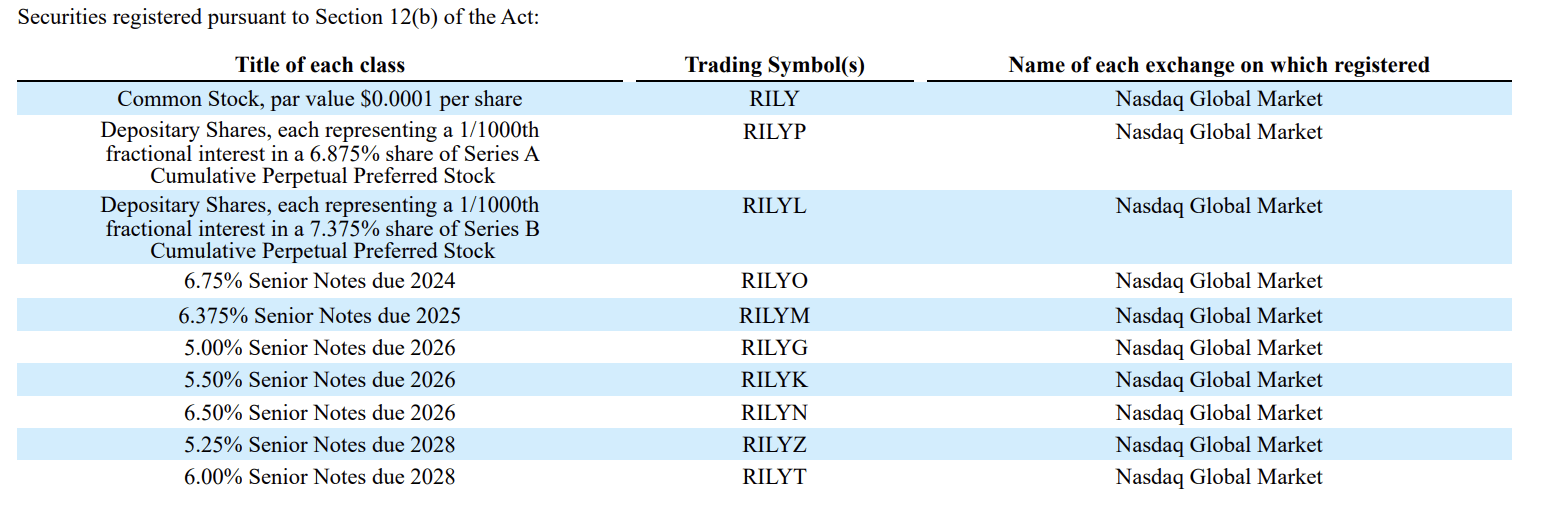

Even more glaring has been the reaction of RILY's outstanding securities to the short report. The company currently has a mix of publicly trading baby bonds and preferred shares that reacted violently to the short report and the more than 50% short interest. For example, the Series A preferreds ( RILYP ) fell from around $21 per share to $16.53 per share following the bearish attack, a $4.47 per share decline for what's currently a 10.4% yield on cost against a $1.72 annual coupon.

B. Riley Fiscal 2023 Third Quarter Form 10-Q

{kind=link}

To be clear, RILYP is currently trading for 66 cents on the dollar, down from 84 cents on the dollar in September from perceived and not an inherent underlying change in its financial performance. Bearish attacks are always brutal for existing shareholders but the market has priced in a discount that is fundamentally unhinged from RILY's balance sheet. I've been buying RILYP in recent days on the back of the sell-off.

{kind=link}

The company currently spends $2 million every quarter in paying dividends to its preferred holders. It spends another $37 million on its common stock dividends. This is set against a balance sheet with total cash and investments of $2.05 billion at the end of the third quarter. The cash component of this sits at $252 million, enough to cover the payment of the dividend for the preferreds and commons for years.

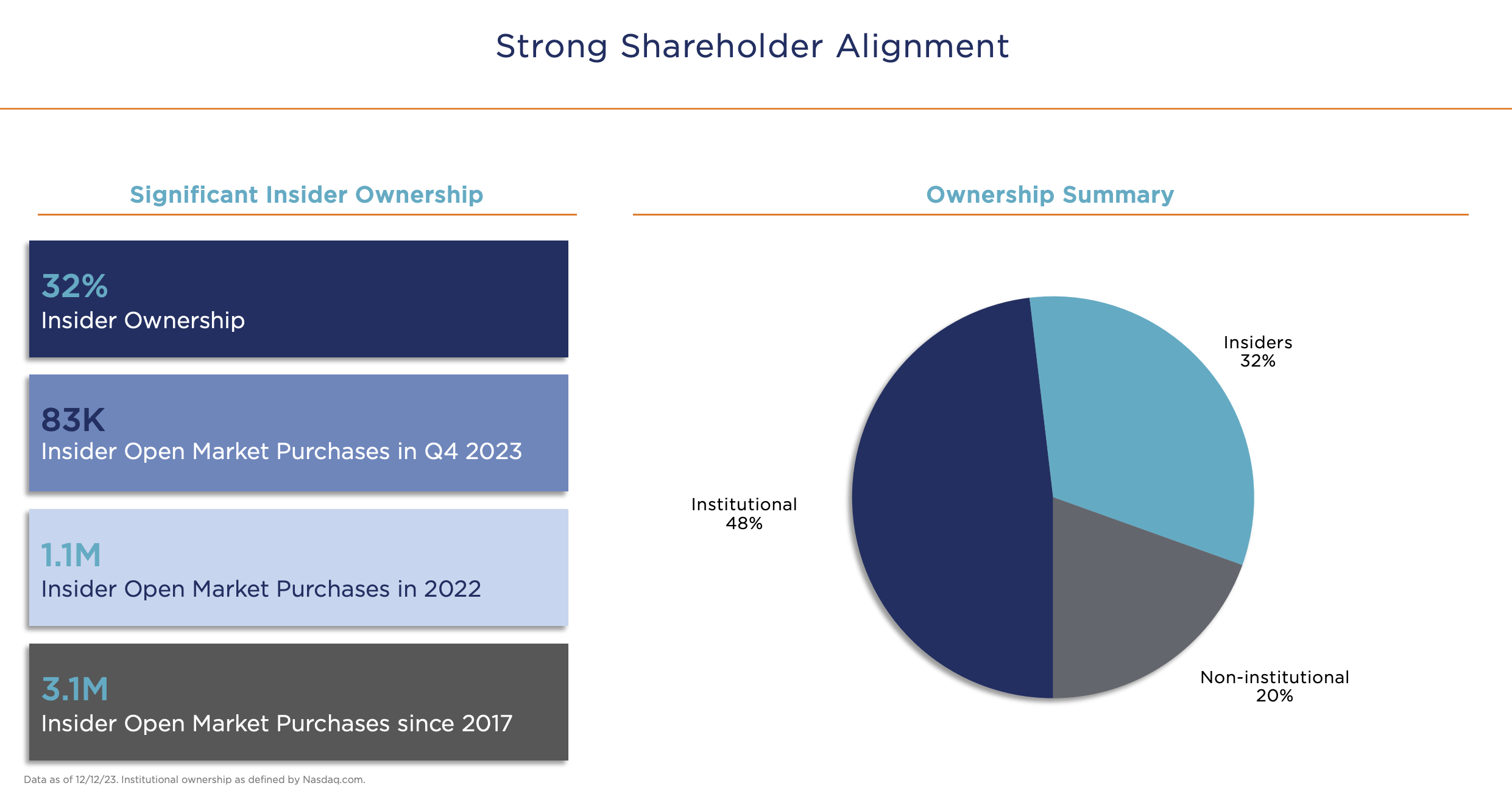

It also comes with an extremely strong 32% insider RILY ownership and significant open market purchase during the fourth quarter. This is before an improvement in underlying capital market conditions from a record low creates new opportunities for higher-margin revenue generation. For bulls, the risk here is a dividend cut on the commons or further negative news around FRG. FRG was a publicly audited company with a currently multi-pronged approach to retailing that reduces earnings volatility.

B. Riley Fiscal December 2023 Investor Presentation

{kind=link}

RILY could of course reduce the dividend but this would be premature ahead of a recovery of capital markets. Any dividend reduction decision should come at the end of 2024 after more certainty on the direction of the Fed funds rate. The next few months will likely see continued negative trading on the back of more than one in two shares being sold short. But a Fed pivot and a continued strengthening of the balance sheet should invert bearish expectations and set RILY up for enhanced quarter earnings. I'm rating the commons and preferreds as buys against this. The baby bonds have been more stable and offer less compelling capital growth and yields but are also buys with the 6.75% Senior Notes Due 5/31/2024 ( RILYO ) currently trading for 95 cents on the dollar despite their redemption being less than 6 months away.

For further details see:

B. Riley Financial: The Bonds, Preferreds, And Commons Are Undervalued Against Risks