RILYK - B. Riley Financial: The Rout Count Get Worse On Derisking

2024-01-12 14:15:00 ET

Summary

- B. Riley Financial stock continues to struggle with a recovery as the combination of recent headwinds facing its FRG acquisition in August 2023 and weak Q3 results sour market sentiment.

- This has pushed RILY's dividend yield to ~20%, which is obviously very attractive if its underlying fundamentals remain sound and can help to offset some of the near-term volatility.

- However, credibility remains low. Mixed asset quality also underscores risks to the durability of cash flows supporting its highly leveraged business and dividends.

- Paired with its institutional-heavy investor base, which is typically more risk averse, we believe there is further room for de-risking selling in store that could worsen the RILY rout.

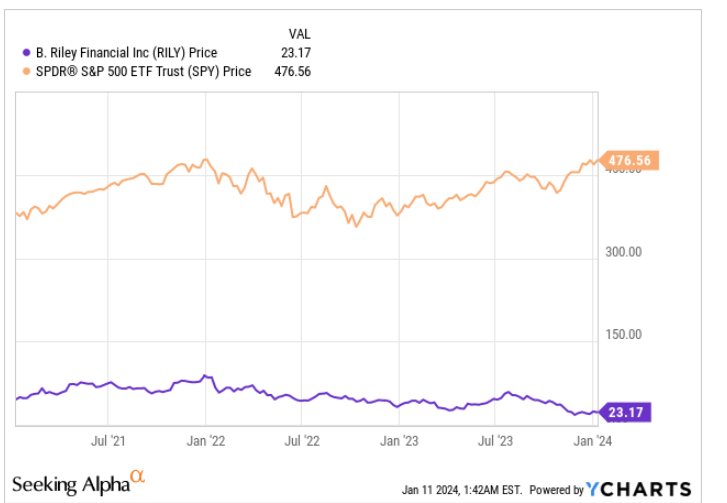

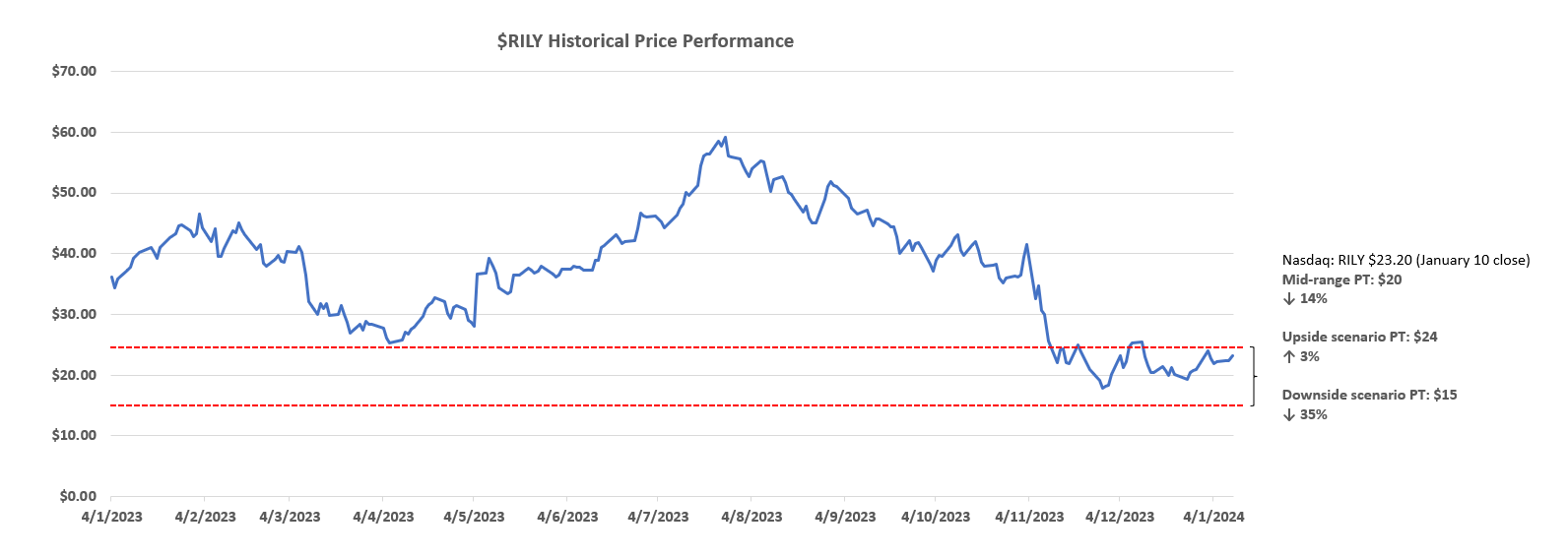

The B. Riley Financial stock ( RILY ) has kicked off the new year trading more than 10% higher than its 2023 year-end slump. Despite paring some gains over the past week, the stock has stayed resiliently above the $20-range. But investors continue to bear the brunt of a steep plunge experienced through November during the final two months of the year. RILY diverged from the broader market rally that took the S&P 500 to the brink of a new record high.

{kind=link}

The stock’s end-of-year plummet was largely triggered by weak Q3 results that underscored RILY’s rising exposure to impairment risks within its portfolio of distressed assets. The downturn was further complicated by a short-seller report on RILY near the end of 2023. Specifically, Prophecy Asset Management’s co-founder John Hughes had recently pleaded guilty to defrauding his clients of $294 million. And some investors have observed RILY’s indirect connection to Prophecy through its recent take-private acquisition of Franchise Group (“FRG”) in August 2023.

There is currently a 57% short interest in RILY, the highest amongst its finance peers and the broader market. With a quarterly dividend pay-out of $1 per share, the stock’s steep plunge has also resulted in dividend yield of more than 20% at one point. Its preferred shares ( RILYP ) and baby bonds are also nursing similarly bruising declines over the same period.

Yet optimism has recently been rising for the stock, with many believing that it has been oversold in response to recent short allegations. Signs of easing financial conditions, paired with RILY’s diversified cash generation portfolio has also reinforce confidence amongst income investors on locking-in the elevated yield at current levels. Arguably, with more than $250 million of cash on the balance sheet, the company remains well-positioned to service its existing portfolio of debt-related costs and, more importantly, quarterly dividends. The easing interest rate environment could also become a potential tailwind in the near-term for its core capital markets and financial services businesses, and reinforce RILY’s fundamental performance.

However, the growing chorus of questions and uncertainties over RILY’s investment in FRG is likely to harbinger continued multiple compressions risks ahead. In the downside scenario, the relevant fundamental implications could even spill over to RILY’s core investment banking and financial services businesses, which are structural to the stock’s valuation and the company’s overall cash flows.

The following analysis aims to provide an overview of RILY’s fundamental outlook, and discuss the recent challenges facing its operations. Specifically, the analysis will explore potential repercussions to the stock under a downside scenario. We believe a sufficiently de-risked trading range for RILY is between $15 and $24 in our opinion. This is corroborated by the stock’s recent performance in response to recent headwinds facing RILY’s brand and underlying operations.

We believe this exercise in sensitizing the potentially de-risked range for RILY is what will be used by markets as a de-risked price determinant for RILY until there is greater clarity over its operating outlook. With 48% of RILY owned by relatively risk averse institutional investors, we expect our anticipated de-risked scenario price range to be a key determinant of the extent of which the related selloffs will reach.

The RILY 6

RILY’s business portfolio is separated into six key operating segments – capital markets, wealth management, auction and liquidation, financial consulting, communications, and consumer. The portfolio is diversified in terms of end-market exposure, as well as cyclicality.

On end-market exposure, RILY operates primarily under two functions – 1) financial services, and 2) principal investing. The core financial services function consists primarily of RILY’s capital markets, wealth management, auction and liquidation, and financial consulting businesses. Meanwhile, the non-core principal investing function is composed primarily of its communications and consumer businesses. Specifically, the communications and consumer segments represent consolidated results from RILY’s control in subsidiaries within the respective industries. These include RILY’s investment in dial-up internet and web-based mobility service brands United Online and magicJack, as well as retail apparel brands such as Hurley. This set-up essentially differentiates RILY’s exposure to core institutional and commercial financial services risks and opportunities from retail consumer-centric ones.

The two operating functions also serve different purposes in our opinion. The investments within RILY’s communications and consumer portfolios are typically slow-growing or declining businesses facing irreversible secular headwinds. This suggests the principal investing function’s core focus is on cash flow generation. Meanwhile, we believe RILY’s core financial services is where the bread and butter to its valuation is, with a greater focus on sustained long-term growth.

On cyclicality considerations, RILY’s core financial services solutions are also well-diversified to perform under changing market conditions. For instance, the auctions and liquidation business typically outperforms during an economic downturn to offset weakness in deal flows coming through the capital markets segment. Taken together, you can say RILY has its hands on a bit of everything despite its core front as a financial services firm.

The Many Ways to Invest in RILY

In addition to its common stock, RILY also offers two classes of preferred shares and seven different baby bonds listed on the Nasdaq.

- RILY : Common stock, with a quarterly dividend of $1 equivalent to ~18% yield at the time of writing (January 4)

- RILYP : Series A shares, with a quarterly dividend of ~$0.43 per share equivalent to ~9.2% yield.

- RILYL : Series B preferred shares, with a quarterly dividend of ~0.46 per share equivalent to 8.9% yield.

- RILYO : 6.75% Senior Notes due May 31, 2024, trading at 97 cents on the dollar at the time of writing; $140.5 million outstanding

- RILYM : 6.375% Senior Notes due 2025 at 86 cents on the dollar; $146.4 million outstanding

- RILYG : 5.00% Senior Notes due 2026 at 65 cents on the dollar; $217.4 million outstanding

- RILYK : 5.50% Senior Notes due 2026 at 72 cents on the dollar; $180.5 million outstanding

- RILYN : 6.50% Senior Notes due 2026 at 71 cents on the dollar; $324.7 million outstanding

- RILYZ : 5.25% Senior Notes due 2028 at 55 cents on the dollar; $266.1 million outstanding

- RILYT : 6.00% Senior Notes due 2028 at 66 cents on the dollar; $405.5 million outstanding

These high-yielding income assets accordingly makes cash flow generation a key focus area for RILY’s investors’ base.

RILY Fundamental Analysis

Core Financial Services

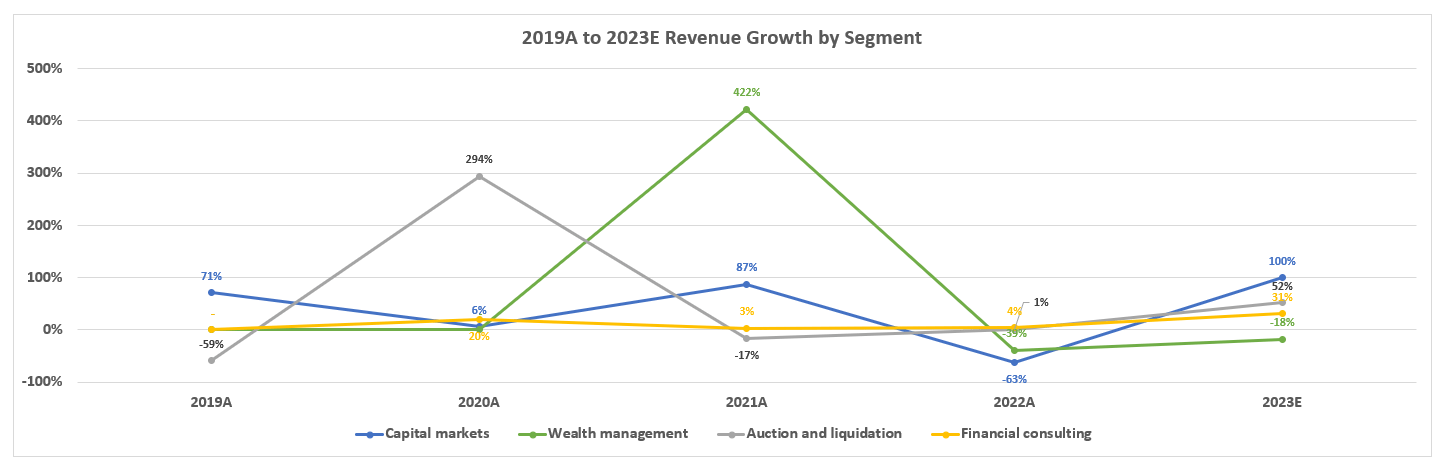

RILY’s core financial services operations are inherently exposed to a lumpy revenue structure due to their performance being a function of market conditions. But as mentioned in the earlier section, RILY’s diversified financial services platform offers a relatively stable outlook amid various stages of the economic cycle. For instance, the auction and liquidation, and financial consulting segments are typically better performing amid times of economic instability and uncertainties. The relevant services typically see jumps in demand during times of uncertainty due to the accompanying surge in company restructurings to adjust to market weakness.

This is corroborated by the robust expansion of fee revenues generated from the auction and liquidation business in the tune of multiple folds observed over the past year. RILY’s auction and liquidation business has been a key beneficiary of downsizing and cost-reduction efforts observed across all industries in 2023 amid tightening financial conditions. Revenue generated from RILY’s financial consulting segment has also ballooned during the same period. The business’ valuation and appraisal services were of high demand amid the volatile market backdrop triggered by the elevated normalized interest rate environment. The segment’s outperformance observed in 2023 was also in line with the double-digit percentage growth observed in 2020. Specifically, the onset of the pandemic had led to unprecedented implications across valuation, accounting, operations and risk compliance considerations.

This largely contrasts with breakneck industry expansion observed during the pandemic due to an extremely low capital cost environment at the time, alongside “COVID stimulus money”. The abundant deal flow and surging valuation multiples accordingly helped spur demand for RILY’s capital markets services at the time. The segment almost doubled its revenue year-on-year in 2021, while the auction and liquidation segment saw declines and demand for financial consulting services steadied.

{kind=link}

Data from RILY 10K filings

Heading into 2024, RILY investors are becoming increasingly optimistic that impending interest rate cuts and easing financial conditions would be a tailwind to the capital markets business. Particularly, small- and medium-sized businesses, which RILY’s services typically cater, to are likely to be the key beneficiaries of a lowered capital cost environment. Easing financial conditions generally improve the appeal and valuation prospects attributable to cash flows, which for SMBs are typically further out from realization.

However, we remain wary of persistent recession risks. The Fed currently estimates 75 bps of rate cuts by the end of 2024, with preference for a “higher for longer” set-up. This would take the Fed Funds Rate from the current 5.25% to 5.5% range to as low as 4.5%. Yet markets are pricing in as much as 150 bps of easing through 2024. Much of the motivation behind these estimates are driving by expectations for a soft-landing, given economic resilience alongside lowering inflationary pressures. While some argue that such an extent of rate cuts are warranted to adjust for a normalizing economy, others are swerving to the recession camp. The argument is that the Fed is unlikely to double the extent of their currently planned rate cuts over the next 12 months, unless a recession is imminent. Specifically, inflation has yet to fall back in line with the Fed’s 2% target. And the last stretch has proven to be especially tough, with CPI data in recent months being largely stuck in the 3% range. Fluctuations and large swings in oil prices due to geopolitical and macroeconomic uncertainties, and mixed labour data are also muddying the outlook. This accordingly favours the Fed’s higher for longer campaign, with limited room for incremental optimism.

Taken together, this set-up is not exactly the most convincing for those optimistic about an impending recovery at RILY’s core capital markets business. If the Fed cuts rates by 75 bps as expected, then the ensuing easing of financial conditions and effect on valuations will likely be relatively gradual. This is unlikely sufficient to materially jumpstart deal flows for RILY. Meanwhile, if rate cuts climb to 150 bps, the scenario will likely be paired with some bumps along the way with a potential resurgence of recession fears. Such a set-up would also be deterrent of deal flows. Both scenarios are not exactly offering the best grounds for a take-off in RILY’s core capital markets this year. And neither is it adverse enough to trigger another year of outperformance for the financial consulting, and auction and liquidation businesses.

{kind=link}

Author

Principal Investments

Meanwhile, we expect continued headwinds to the communications and consumer segments’ topline prospects. Most portfolio companies within RILY’s retail exposure are not only cyclical, but also subjected to structural secular headwinds.

Key businesses within RILY’s communications segment include magicJack, United Online, and Marconi Wireless. They currently offer largely obsolete technologies such as internet cell/mobile call services, dial-up internet, and other mobile virtual network connectivity services that cater to the marginal population. Management has publicly acknowledged and disclosed in their 10K filing that subscription revenue contributions from these consolidated investments are expected to keep declining.

This is consistent with the y/y declines observed in organic communications segment revenues in recent years. If it were not for the consolidation of Marconi Wireless in late 2021, and Lingo-BullsEye Telecom mergers in 2022, the communications segment would not have experienced growth in recent years. And we expect revenue from the relevant businesses to deteriorate further. This is corroborated by the rapid deceleration in communications revenue growth in Q3, as lapping dynamics from previous year transactions ease. Without consideration for future M&A activity, we would expect communications segment sales to deteriorate further, or expand in line with the pace of normalized inflation at best.

{kind=link}

Author

And the consumer business is unlikely to fare any better. While management remains optimistic that an emerging cyclical recovery in PC demand would benefit its consolidated investment in Targus, there is little respite for its brands business. In addition to the sale of computer accessories through Targus, the consumer segment also generates revenue from brand advertising and licensing fees through a portfolio of retail-focused names. They include Hurley, Justice and Scotch & Soda, which are often linked with less busy storefronts compared to neighbouring shops. There is also a “Six Brands” portfolio, which generates revenue through multi-year licensing contracts with apparel manufacturers that also include a guaranteed minimum royalty. If most of these consumer revenues are already contracted with a take-or-pay component, yet the business is still in decline, then you bet the ensuing cash flows will deteriorate further too.

{kind=link}

Author

RILY Consolidated

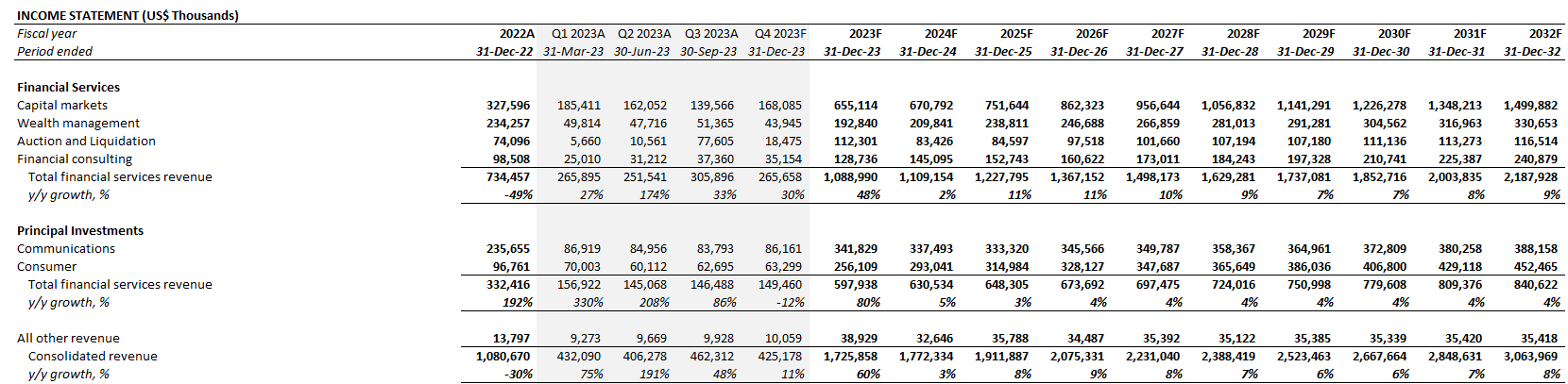

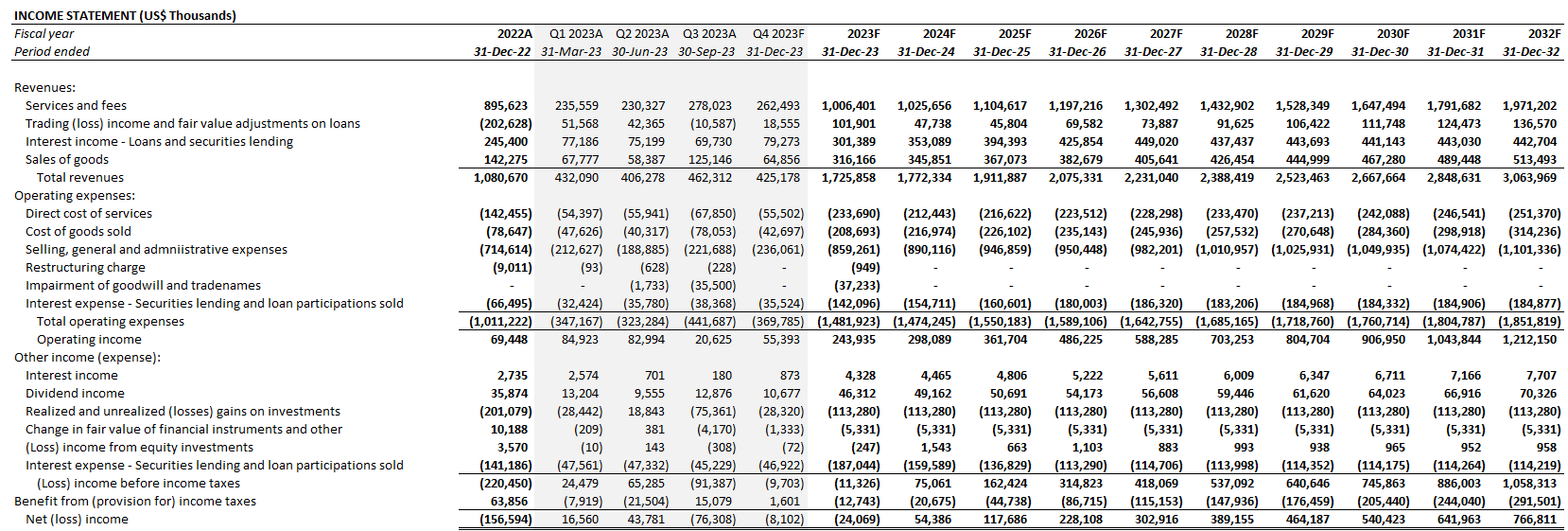

Taken together, we expect modest growth for RILY’s consolidated business in 2024, with a more structural pace of recovery in the financial services function through 2025 when market conditions gain clarity. In addition to our views on the economic outlook, we have also considered historical growth trends observed across RILY’s key operating segments to develop our assumptions applied in the forecast.

{kind=link}

Author

We expect the deteriorating nature of RILY’s consumer and communications business demand weigh further on cash flows. Even if their steady profit margins hold up, the absolute dollar return is on a structural decline. Management had previously alluded to RILY’s portfolio of relevant businesses as “strong cash flow contributors” to the company. And both the consumer and communications segments have historically contributed to about a third of RILY consolidated segment income (ex-impairment and restructuring charges) in past years. This underscores ballooning risks to RILY’s continued reliance on cash flows from structurally declining businesses in supporting its debt costs, core loans business, and capital returns program.

{kind=link}

Author

RILY_-_Forecast_Financial_Information.pdf

We also caution an increasing risk of additional impairment charges to goodwill and tradenames. The communications segment is most prone to impairments in our opinion, given the portfolio’s increasing obsolescence and declining demand environments. It is more likely for Targus than magicJack or United Online to benefit from an impairment reversion in our opinion, which says a lot about the situation here. We have not modelled said estimates in our base case projections, given the high level of judgment involved. However, our sensitivity analysis on the “worst-case scenario” valuation in the following section will touch further on this subject.

3 Immediately Overhanging Risks to Consider Before Investing in RILY

1. Risks of deteriorating asset quality – Investing in and underwriting loans to distressed or underperforming business is part of RILY’s core business strategy. This is primarily observed through RILY’s portfolio companies in the communications and consumer segment – declining businesses, with positive cash flows capable of positive returns on investments.

But the latest Targus goodwill impairment charge begs the question of why the communications segment has not been handed the same reality. The company wrote-down Targus goodwill by $35.5 million in Q3, citing weakness in the inherently cyclical PC market.

Yet cash flows from magicJack and United Online are clearly deteriorating at a rapid pace given their ongoing sales declines. Admittedly, management has likely modeled in structural declines to said businesses at the time of their respective acquisitions. The acknowledgement of this risk was clearly disclosed in the 2016 and 2018 year-end filings, and remains unchanged:

- 2016 10K :

{kind=link}

RILY 2016 10K

- 2018 10K :

{kind=link}

RILY 2018 10K

- 3Q23 10Q :

{kind=link}

RILY 3Q23 10Q

But a lot has changed in the relevant technologies since magicJack and United Online’s respective acquisitions. This accordingly draws questions to the durability of goodwill attributable to the communication business. RILY had recorded goodwill of $14.4 million pertaining to its $169.4 million acquisition of United Online in 2016, and goodwill of $109.7 million on the $143.1 million magicJack acquisition in 2018.

Despite accounting policy requirements for an annual review of goodwill, the communications segment has yet to report any impairment charges. Although management disclosed that RILY has already recovered their initial investments on the legacy communications businesses during the 3Q23 earnings call , there is little support for their lofty goodwill balances going forward in our opinion. Given the pace of which technology has evolved since the pandemic (cue expanding fiber to the home, 5G deployment, AI, accelerated computing, etc.), it is highly unlikely that the anticipated revenue declines modelled at the time of acquisition are still relevant under today’s environment. The rising risk of write-downs due to RILY’s increasingly obsolete portfolio of principal investments currently consolidated into its consumer and communications segments could potentially lead to further deterioration of its equity value in the near-term.

2. RILY and FRG – The RILY-FRG debacle raised by recent short-seller allegations has been a key culprit in driving the stock’s recent declines. The situation largely goes like this:

- RILY acquired a 31% stake in FRG in August 2023 as part of the latter’s take-private deal. RILY has already had previous dealings with FRG through a loans receivables purchase agreement with one of FRG’s portfolio companies, W.S. Badcock Corporation (“Badcock”).

- The fraudulent activity admitted to by the co-founder of Prophecy Asset Management, has, since November, dogged FRG CEO Brian Kahn due to his links to Prophecy. The allegations surfaced after Hughes – the co-founder of Prophecy – was found guilty of defrauding his clients of $294 million. During his trial, he cited partnership with two “ co-conspirators ”. Kahn is allegedly one of them based on Bloomberg reports . However, Kahn has subsequently denied the allegations in a November statement to Reuters. This was consistent with the conclusion of a recently completed FRG internal investigation that found “no ties” between its CEO and Prophecy. The denial was also confirmed by RILY management during the 3Q23 earnings call .

And I know that today, a statement came out from Brian denying any involvement and what happened with Prophecy, and that’s good enough for me.

- Yet the situation continues to raise questions among the investors’ community over RILY’s due diligence process in executing transactions, among other implications.

RILY management has already denied involvement with the accusations in the 3Q23 earnings call. During the latest earnings call, RILY CEO Bryant Riley said the company had only recently “learned of this matter”, and have had “no direct experience with what has been alleged”. As discussed earlier, FRG’s internal investigation completed in mid-December has also found “ no ties ” between the company, Kahn and the Prophecy co-founder's fraud case. Both RILY and FRG’s operations have also yet to report any direct impact from the situation.

Yet the credibility over RILY and names associated with the situation remain tarnished, as corroborated by the stock’s absent recovery. However, the situation potentially subjects RILY to adverse implications on its balance sheet, P&L through income from equity method investments (e.g. FRG), and ROI structure. There are also spillover risks to other aspects of RILY’s business, and add incremental pressure on its highly levered capital structure.

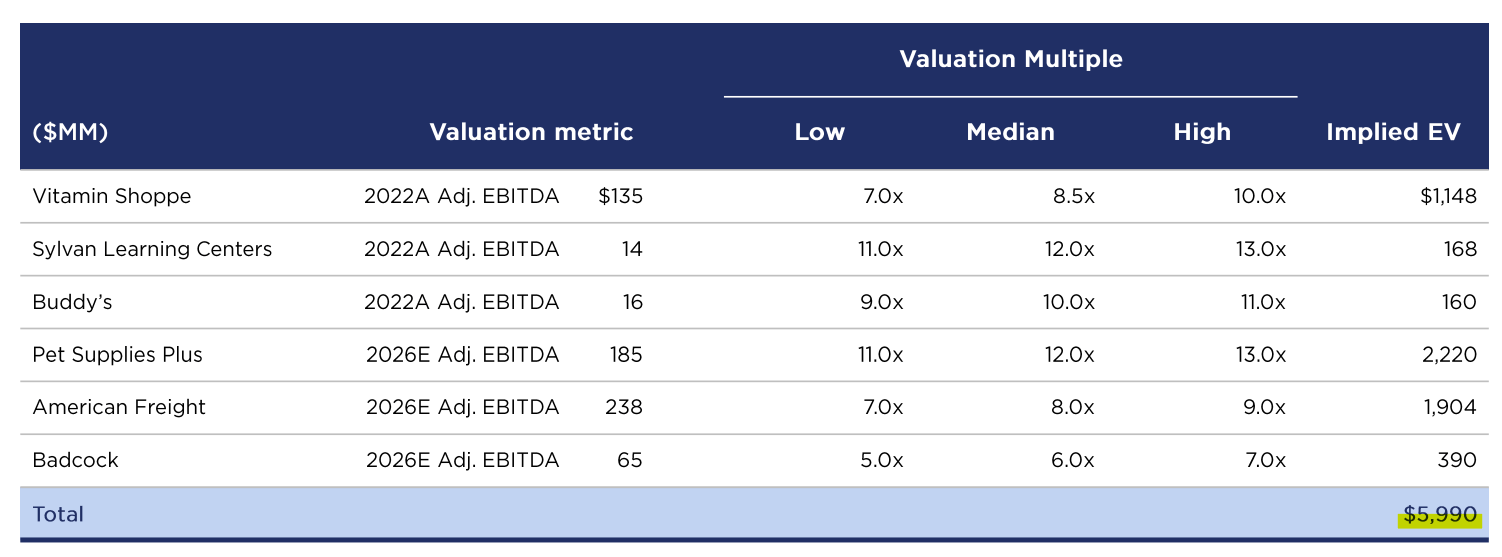

3. Collection Risks – As discussed in the earlier section, doing business with companies in declining industries is a core component in RILY’s business strategy. This includes underwriting loans, and sometimes directly investing into businesses with highly leveraged balance sheets. This is in line with disclosures within RILY’s latest Investor Day presentation, which highlights the wide differential between the equity and enterprise values of its latest FRG equity method investment. Specifically, the differential highlights that some of RILY’s assets boast a higher enterprise value than their respective equity values Recall that equity value is equivalent to enterprise value, less long-term debt and add back cash. Hence large equity-enterprise value differences are typically attributable to the size of leverage (or general capital structure) on a company’s balance sheet.

Specifically, RILY paid consideration of $281.1 million for 31% interest in FRG based on its equity value of $902.6 million. FRG’s equity value of $902.6 million determined on acquisition date is exclusive of almost $2 billion in net debt, which implies an enterprise value of $2.9 billion. This represents a ~70% difference:

RILY December 2023 Investor Day Presentation

The difference is even more stark when considering management’s sum-of-the-parts valuation estimate for FRG’s portfolio companies.

{kind=link}

RILY December 2023 Investor Day Presentation

The differential, which highlights the highly levered nature of RILY’s portfolio assets is also brought into focus through FRG’s recent sale of Badcock to Conn’s ( CONN ). Badcock was sold to Conn’s on December 18 – merely days after the RILY Investor Day presentation disclosures – in an all-stock deal. The consideration was equivalent to 49.99% of Conn’s outstanding common stock as of acquisition date, which works out to a notional value of about $35 million. The estimated notional value of the consideration paid for the transaction again represents a significant discount to the enterprise value (Badcock: $390 million) reported by RILY on its portfolio assets.

{kind=link}

ir.conns.com

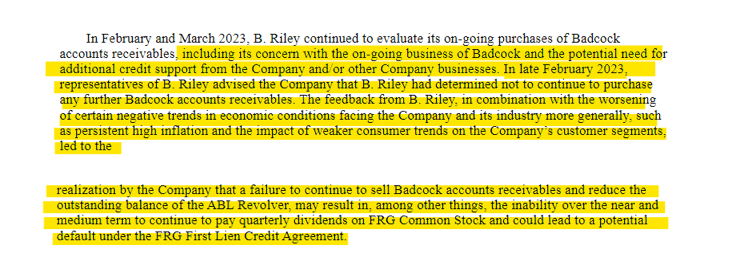

RILY itself already operates a highly leveraged balance sheet, and the highly levered nature of its portfolio assets further increases its exposure to collection risks. For instance, Badcock has long experienced a highly leveraged balance sheet needed to facilitate its working capital requirements. And RILY has been buying Badcock loans receivables since 2021 under a Master Receivables Purchase Agreement (disclosure details on page 18, RILY 3Q23 10Q ). But tones shifted in early 2023, with RILY deciding against additional purchases of Badcock loans receivables, citing “concerns” with Badcock’s business outlook. RILY proceeded to acquire a 31% interest in FRG in August 2023 instead.

{kind=link}

Franchise Group Inc. Schedule 14A, sec.gov

There are also growing signs of collection risks based on changes in RILY’s sales on credit in recent years. Tracing back to 2020 at the onset of the pandemic, RILY’s allowance for doubtful accounts balance and days sales outstanding on receivables have largely remained stable. Yet both metrics for gauging collection ballooned exiting 2022 following the Lingo-BullsEye transactions, despite stabilizing market conditions. Specifically, additions to the AFDA reserve have been choppy in recent quarters, outpacing the rate of acquisition-related A/R and consolidated revenue expansion observed at RILY.

{kind=link}

Author, with data from historical RILY 10Q/10K filings

Taken together, we remain cautious of heightening risks of potentially deteriorating asset quality on RILY’s balance sheet. This would drive adverse implications to RILY’s highly levered business strategy and capital structure, and, inadvertently, impact the durability of its dividend yield at current levels.

Sensitivity Analysis

As a result of RILY’s risk profile, we have performed a sensitivity analysis on its fundamental and valuation outlook to determine a reasonably de-risked price for the stock in our opinion. The sensitivity analysis is performed under a P/S multiple-based valuation approach.

We have selected this valuation approach to normalize for some of the impact from FRG-related risks at RILY. Specifically, much of the fundamental contributions pertaining to RILY’s FRG equity investment comes from “below-the-line” contributions. This includes dividend income and income from equity investments, which the P/S multiple-based valuation approach would remove from consideration.

Price Target

{kind=link}

Our sensitivity analysis yields a price range of $15 to $24 for RILY. The base case price is set at the midpoint of $20. With the stock currently trading between the base and upside scenario price range, while RILY’s underlying fundamentals show signs of quality deterioration, we believe the risks are still skewed to the downside in our opinion.

Downside Scenario

The downside scenario price is determined by only considering revenue contributions from RILY’s core financial services function – i.e. revenue generated from capital markets, wealth management, auction and liquidation, and financial consulting. We believe this business is less prone to risks of impairment charges and significant judgments / estimates based on our foregoing discussion. RILY’s core financial services businesses, despite their inherently cyclical natures, also demonstrates relative durability against secular considerations at its consolidated principal investments (e.g. magicJack), and uncertainties over its equity method investments (e.g. FRG). RILY also remains well within the net capital requirements set by the SEC. This provides an incremental margin of safety that reinforces the durability of value attributable to RILY’s core financial services functions, despite looming headwinds facing its principal (i.e. consolidated) and equity method investments.

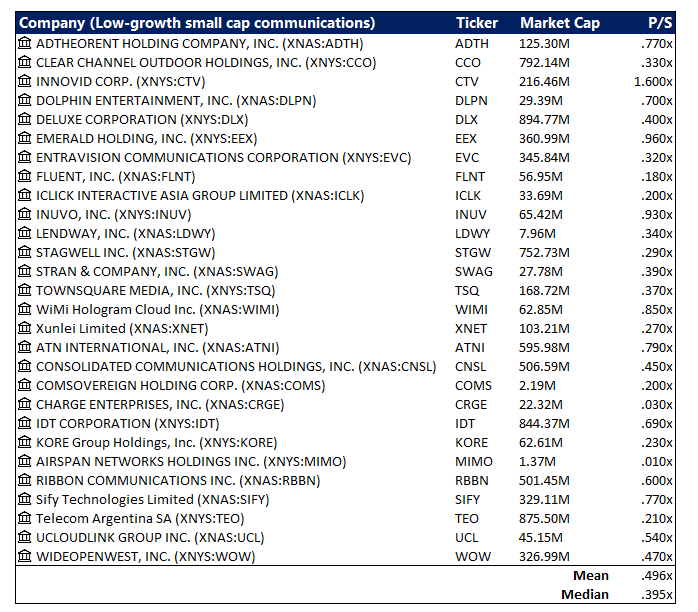

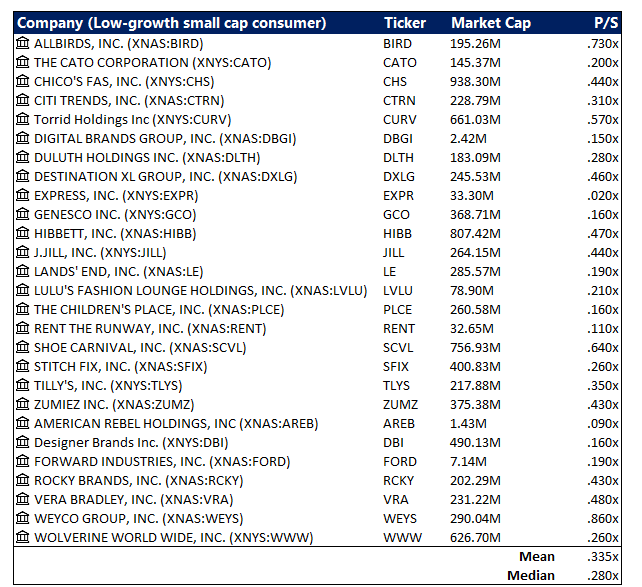

We have applied a NTM P/S ratio of 0.424x to related revenue estimates. The assumption applied is in line with the average of low growth capital markets peers that exhibit a similar growth profile as RILY.

Some investors may question our unusual use of a P/S multiple as the key determinant of value attributable to RILY’s financial services business component. Admittedly, the sector typically prioritizes earnings and cash flows due to their stable growth outlook. However, we have focused on the use of P/S multiple in determining the value attributable to RILY’s financial services component to ensure consistency across our sensitivity analysis exercise. The valuation multiples observed between RILY’s low-growth financial services peers considering both forward sales and earnings estimates also show a consistent rate of modest expansion due to their inherent steady-state cash flows. This is also in line with observations of stable cash flow expansion at RILY’s financial services components. Specifically, our forecast estimates net 3% growth across RILY’s capital markets, wealth management, auction and liquidation, and financial consulting segment income streams, consistent with its operating backdrop as well as historical trends. As such, we view the consideration of sales growth metrics as appropriate in performing a unified sensitivity analysis.

Narrowing-in on only lower growth small cap names also reflects relevance to RILY’s growth and profitability profile attributable to its financial services function. The approach normalizes the incremental valuation premium attributable to the broader peer group due to inclusion of secular peers such as fintech names, which RILY does not benefit materially from.

Author, with data from Seeking Alpha

{kind=link}

Author, with data from Seeking Alpha

Upside Scenario

For the upside scenario price, we have considered RILY’s entire revenue portfolio.

Author

The NTM P/S ratios considered for the communications and consumer segments are consistent with the average observed across RILY’s low-growth small cap peers across the respective industries. Similar to the approach considered in valuing RILY’s financial services business, the valuation multiple assumption applied normalizes for the incremental premium attributable to its higher growth communications and consumer peers. The NTM P/S multiple applied on all others revenue represents the average of assumptions applied across all of RILY’s financial services, communications, and consumer revenues.

{kind=link}

Author, with data from Seeking Alpha

{kind=link}

Author, with data from Seeking Alpha

We believe the upper range price is reflective of value attributable to RILY’s existing operations, with an assumption that its asset portfolio remains adequately marked to market. The upper range price only considers the impact if only RILY’s equity method investment-level asset valuations and ensuing cash flows, such as those from FRG, are affected due to ongoing brand and reputation headwinds (i.e. ex-spillover risks to existing operations).

Risks to the Downside Scenario

Given RILY’s weaker-than-expected Q3 earnings report, and recent negative headwinds facing the company, we believe risks remain skewed to the downside for the stock. This underscores potential for a continued de-risking sell-off in the near-term, given our estimated floor at $15. However, there are several risks that could reverse the downside scenario:

- Short squeeze : Short interest in RILY currently represents close to 60% of its share float. Highly shorted stocks are typically more prone to “short squeezes”, or sudden steep surges in valuation due to the volatile hedging mechanics for highly leveraged trading activity. For instance, any good news facing RILY could trigger a short squeeze. Say if the company’s upcoming Q4 results outperform, then short-sellers will need to start covering for their positions (i.e. buying RILY shares to cover for the positions they have sold short on). This could potentially lead to a surge in demand for RILY shares over what is currently available in the market. The company is also primarily owned by institutional investors (48%) and insiders (32%), which are likely less willing to offload their shares in the event of good news. This further exacerbates any potential short squeezes if they do occur.

- Consistent fundamental outperformance : There is a potential case for consistent positive progress at RILY in the coming months, particularly in its financial services offerings. As discussed in the earlier section, easing macro conditions could be a boon for deal flow to its core capital market business in the near-term. This could potentially underpin a more structural recovery to RILY’s valuation over the longer-term if relevant fundamental outperformance becomes reality and continues to outpaces impairment risks in the communications and consumer segments over the longer-term.

The Bottom Line

There is substantial credibility left for RILY to restore pertaining to the quality of its portfolio assets against rising impairment and collection risks. The subsequent adversities stemming from said risks could lead to further negative implications on future income and dividends received from RILY’s equity investments. The combination of rising impairment and collection risks are company-specific headwinds that could also result in adverse impacts on RILY’s balance sheet. The set-up effectively increases risks to the durability of RILY’s dividend payments and capital returns program to shareholders, since income generated from its portfolio assets are key contributors to cash flow. And recent negative headlines involving the company’s acquisition of FRG also exacerbates investors’ shaky confidence in the stock. Taken together, the collective set-up is expected to keep risks skewed to the downside for RILY stock and preclude potential of a swift recovery in the near-term

Price Target

Our sensitivity analysis yields a price range of $15 to $24 for RILY. The base case price is set at the midpoint of $20. With the stock currently trading between the base and upside scenario price range, while RILY’s underlying fundamentals show signs of quality deterioration, we believe the risks are still skewed to the downside in our opinion.

Price Target

Our sensitivity analysis yields a price range of $15 to $24 for RILY. The base case price is set at the midpoint of $20. With the stock currently trading between the base and upside scenario price range, while RILY’s underlying fundamentals show signs of quality deterioration, we believe the risks are still skewed to the downside in our opinion.

For further details see:

B. Riley Financial: The Rout Count Get Worse, On Derisking