RILYP - B. Riley: Good News To Investors (Rating Upgrade)

2024-01-02 07:09:05 ET

Summary

- The Bloomberg report alleging an investigation into Franchise Group, Inc. (FRG)'s CEO relates to a fraud case against one of his associates from a previous employment, unlikely to impact RILY or FRG.

- Management is committed to its $1 quarterly distribution, yielding 20% annually, and has the financial capability to maintain it.

- RILY's operations are tied to the SME sector, and the improving market conditions are poised to impact its business positively.

Note from the author : This article builds upon our prior analysis of B. Riley Financial (RILY). For a more comprehensive understanding of the context and insights presented here, we highly recommend that our readers refer to the previous piece.

Investment Thesis

In our last article, we cast a critical eye on B. Riley's ( RILY ) unexpected stock rally, questioning its alignment with the subdued market trends in the Small and Medium Enterprise 'SME' sector, its primary focus area. We also raised doubts over the robustness of RILY's business model, particularly the promise of extraordinary returns, and highlighted potential red flags behind its $115 million equity raise in August.

Since then, shares declined by two-thirds, while the SME market has shown signs of recovery.

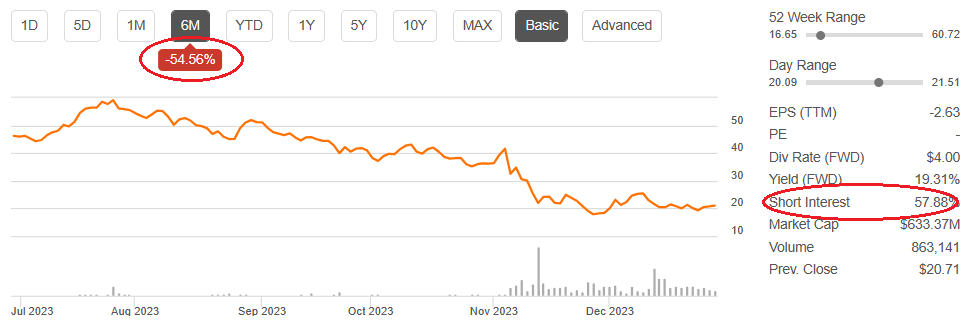

Our current perspective is that, despite friction in the value proposition of RILY's modus operandi, we see a nuanced investment opportunity going into 2024. Our analysis indicates that the structure remains robust enough to allow RILY time to address its drawbacks (potentially tightening its underwriting framework) while maintaining dividends and liquidity. We believe these dynamics create a favorable risk/reward opportunity to bet against prevailing short-seller positions holding 60% of RILY shares in short interest.

Improving market conditions in the SME market combined with a 55% share decline in the past six months offers an attractive risk/reward opportunity to bet against a currently-prevailing short-seller positions holding 60% of RILY's shares in short interest (Seeking Alpha)

{kind=link}

Improving Market Conditions

RILY's improving fundamentals, boosted by the Russell 2000 index (RTY) growth, contrast with its falling share price. This divergence offers a potential upside catalyst as investors' perceptions recalibrate with the new accommodative realities. These dynamics provide an attractive opportunity to bet against the dominant short-seller positions holding 60% of RILY's share in short interest.

Strong capital markets boost IPOs, benefiting RILY's Capital Markets and Financial Consulting divisions. Additionally, rising stock prices are expected to increase the value of Assets Under Management 'AUM', positively affecting its Wealth Management segment's revenue. Please check our March article for a detailed review of RILY's business segments.

Moreover, the current market strength presents an opportunity for RILY's customers, many of which are distressed SMEs, to engage in restructurings. This will likely boost RILY's underwriting revenue and help clients manage and repay the bridge financing from RILY. For example, highly leveraged Exela ( XELA ), a customer of RILY's Capital Market underwriting segment, could raise equity to repay some of the debts extended by RILY. For more examples of RILY's operations, please refer to the previous article.

A restructuring trend could improve RILY's $550 million loan portfolio, which had mixed results in Q3 23, including a rise in non-performing loans from 1% to 7.5%, but also a 10% positive fair value adjustment. The loan portfolio declined from $700 million to $550 million after RILY exited the lucrative Badcock receivables contract during the Franchise Group buyout. RILY sold this contract to a partner in the buyout, who was interested in the Badcock business. RILY still holds a 30% stake in the Franchise Group.

Is RILY's Dividend Sustainable?

RILY appears set to maintain its $1 quarterly dividend into 2024, defying short-seller expectations and suggesting a positive outlook for its shares. Despite recent non-cash losses, RILY's financial position remains strong, with a cash balance of 252 million and TTM adjusted EBITDA of 370 million, supporting its annual dividend payout of $124 million. Despite concerns over RILY's 'Vulture/Distressed' investment strategy, RILY consistently generates positive cash flow from its operating segments.

| Year |

| Adjusted EBITDA (million $) |

| 2017 |

| $ 21 |

| 2018 |

| $ 90 |

| 2019 |

| $ 208 |

| 2020 |

| $ 407 |

| 2021 |

| $ 422 |

| 2022 |

| $ 366 |

| 2023 (Q1-Q3)/TTM |

| $ 268 / $370 |

RILY's $300 million dividend and interest outlay leave little cushion against its $370 million EBITDA. We believe this is the reason behind RILY's restrained and inconsistent net share buybacks, despite management's conviction that the stock is undervalued. However, anticipated market improvements in the SME sector are poised to enhance profitability, increase this cushion, and encourage management to pursue a more aggressive and consistent repurchase program.

Since Q4 2021, RILY's management has consistently distributed $1 quarterly dividends, demonstrating a strong commitment to shareholders despite earnings cyclicality. RILY's CEO owns roughly a quarter of the outstanding shares. This consistent dividend policy, coupled with improving market conditions and profitability, counters the overly pessimistic views and could serve as a catalyst for the company's stock in 2024.

How I Might Be Wrong

Our optimistic view on RILY is based on the expected impact of the Russell 2000 Index's growth on its profitability. However, the impact of this growth on IPOs, M&As, and underwriting activities may not be as direct as anticipated. Still, we believe that the subdued capital markets and the Fed's unorthodox monetary policy in prior quarters hindered RILY's Capital Market services. With these conditions changing, we anticipate a fundamental shift in RILY's position, a possibility that hasn't yet been reflected in its share price.

Another concern is that RILY's operations are diverse and structured to offer countercyclical balance. For example, some segments, such as Auction and Liquidation, outperform during downturns. An improvement in one segment could be offset by a decline in another.

Still, we assess that RILY's operational balance is tilted towards upward cyclicality rather than downward. We also believe that the Auction and Liquidation segment stands to benefit from challenging market conditions in Europe, offsetting the potential decline in activity as economic conditions continue to improve in the US.

Finally, while RILY shows signs of undervaluation on many metrics, its NAV per share is negative, mirroring its significant leverage. With a combined debt of $2.4 billion, any perceived dip in profitability could spark liquidity concerns or, in the best case, dividend-cut fears. Our optimistic stance going into 2024 is rooted in RILY's strategic positioning post-pandemic. The pandemic rally, while subsided, provided RILY with an expanded customer base, solidifying its role as a key underwriter partner in the SME sector. The company helped numerous SPAC customers go public, and while IPO revenue has subsided, these now-established public companies have underwriting needs for additional equity and debt capital. Thus, although the number of IPOs and underwriting has decreased, RILY's market position has expanded along with its customer base. This change in RILY's market position differs from its stock price, which trades at 2019 levels when RILY was much smaller.

RILY's stock is trading below 2019 value despite the company's growth, echoing the lows of peak pandemic uncertainty. (YCharts)

Our confidence in our bullish outlook is also enhanced by the valuation gap between RILY and its peers, as shown in the chart below. Moreover, with a 20% dividend yield, the company's value proposition stands unique in the sector.

Far Fetched Concerns

The recent downturn in RILY's share price, sparked by allegations (paywall) against the CEO of Franchise Group 'FRG,' a RILY portfolio company, is a clear case of market overreaction .

The allegations against Brian Kahn, FRG's CEO, relate to his prior employment as a fund manager at Vintage Capital Management and are unrelated to FRG or RILY. The main defendant in this case, John Hughes, a fund manager at Prophecy Fund , has confessed to concealing losses from investors between 2017 and 2020, a time when Mr Kahn was not part of FRG nor RILY. Moreover, during the entire trial, FRG's name wasn't mentioned even once (and neither was RILY's). It wasn't until Bloomberg alleged that Mr Hughes implicated Mr Kahn that RILY's management even knew about the case, as pointed out by RILY's CEO during the Q3 earnings call.

Crucially, FRG operates independently from RILY. This is clearly stated many times, including in SEC filings (pp 46) from August, well before the allegations surfaced. FRG's CEO described RILY as a Minority Shareholder on a separate occasion. This designation is pivotal to dispelling any misconceptions about RILY's liability for FRG's current or future legal challenges, if any. RILY bears no more responsibility for FRG actions than an individual investor does for the misconduct of companies within their portfolio.

Equally important, the market's response, manifested in a $640 million drop in RILY's market capitalization in the two weeks following the Bloomberg report, is grossly disproportionate to its actual exposure to FRG. This exposure is limited to a $281 million equity investment. Even if FRG is implicated in the investigation, which we doubt, or engages in future legal troubles, its robust liquidity, with over $100 million in cash and $1.3 billion in current assets, indicates its capacity to address any legal issues independently, reducing the potential spillovers on RILY.

Finally, RILY's involvement in FRG's recent buyout (having raised funds for the deal from institutional investors and high net-worth individuals), while posing a potential reputational risk, should not overshadow RILY's proven expertise in the SMEs, often characterized by their volatility and ESG risk. This is most likely not the first time RILY has faced such challenges, given its focus on distressed SMEs. Moreover, we believe that ultimately, RILY's reputation will be judged by the financial performance of FRG compared to the expectation bar set by its brokers during the fund-raising process instead of ESG challenges common in the SME sector and well-known and accepted by RILY's associates, investors, and partners.

Given this dislocation of market price to the fundamentals of the issue, we believe that RILY and its bonds/preferred shares offer an attractive risk/reward opportunity going into 2024.

Opportunity in RILY's Baby Bonds and Preferred Stock

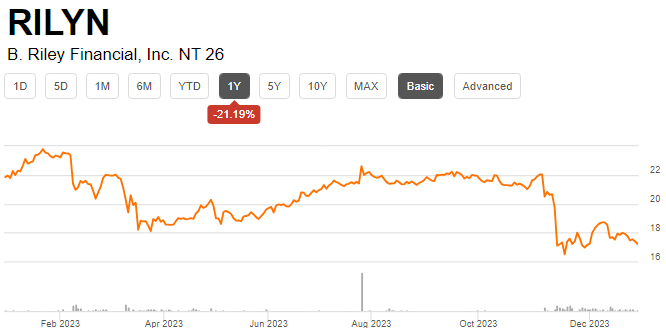

The Bloomberg report triggered widespread panic, affecting RILY's common stock and its publicly traded baby bonds and preferred shares. While some securities like ( RILYO ), the senior notes maturing 2024, have almost fully rebounded from their Bloomberg sell-off, now trading at $24.2 vs. $24.6 prior to the article, others haven't been as fortunate. RILY's other securities, such as ( RILYM ), ( RILYG ), ( RILYK ), ( RILYN ), ( RILYZ ), and ( RILYT ) still trade substantially below their values as of November 3, 2023, one day before the date of the Bloomberg article. This disparity in recovery rates suggests a potential investment opportunity in those assets that haven't yet recovered. The charts below show the November 2, 2022 , sell-off and subsequent divergence in recovery pace among RILY's baby bonds.

RILYO senior notes maturing in 2024 have quickly recovered after the rapid decline subsequent to negative publicity related to one of its portfolio companies. (Seeking Alpha.) Seeking Alpha Seeking Alpha

{kind=link}

{kind=link}

{kind=link}

A similar pattern is evident in RILY's preferred shares. Series A preferred ( RILYP ) has largely shrugged off the negative impact of the Bloomberg report. In contrast, Series B preferred shares ( RILYL ) have not yet recovered and are trading at a lower yield of 9.25% despite having a call option date a year later than RILYP. Both series are cumulative preferred stocks.

We expected that RILY's securities would move in tandem, given their interconnectedness around RILY's business fundamentals. We see the trade dynamics in recent weeks present an arbitrage opportunity before the correlation between these securities returns to normal. In addition, our positive outlook on RILY's preferred and baby bonds is rooted in our expectations of improving the fundamentals of RILY's operations.

Summary

Our analysis suggests a compelling investment opportunity in RILY as we move into 2024. The disconnect between RILY's stock performance and the improving conditions in the SME sector, particularly in light of the Russel 2000 index recovery, indicates potential for significant upside. While acknowledging the risks associated with its high leverage and the recent challenges around its loan portfolio, manifested in an increase in non-accruals, we remain optimistic about RILY's capacity to sustain its dividend, backed by its history of profitability and robust EBITDA that is enough to cover its interest and dividend. Given management's commitment to the $1 dividend quarterly distribution, we see the 20% yield as an attractive opportunity and a potential catalyst going into 2024. Our rating upgrade is also a strategic response to a rigid short-seller position that failed to adjust to changing market dynamics, manifested in a 65% decline in RILY's share price and improving fundamentals as mirrored in a 14% surge in the RTY index in Q4 while overreacting to far fetched concerns over one of its portfolio companies.

For further details see:

B. Riley: Good News To Investors (Rating Upgrade)