BTG - B2Gold: An Attractive Valuation But Also More Jurisdictional Risk

2023-03-28 17:24:19 ET

Summary

- The recently announced Sabina Gold & Silver acquisition seems like a good fit for B2Gold as it will boost reserves and improve the jurisdictional risk.

- B2Gold trades at a lower earnings multiple than peers, even after adjusting for the 20% increase in the number of shares following the acquisition.

- The big question is whether the discount to peers is large enough to justify the higher geopolitical risk.

Investment Thesis

B2Gold ( BTG ) is an almost debt-free gold producer, with a market cap of around $4.2B today, and did in 2022 produce about 1M gold ounces. The company primarily operates in a few countries with higher geopolitical risk, which partly explains the lower valuation.

{kind=link}

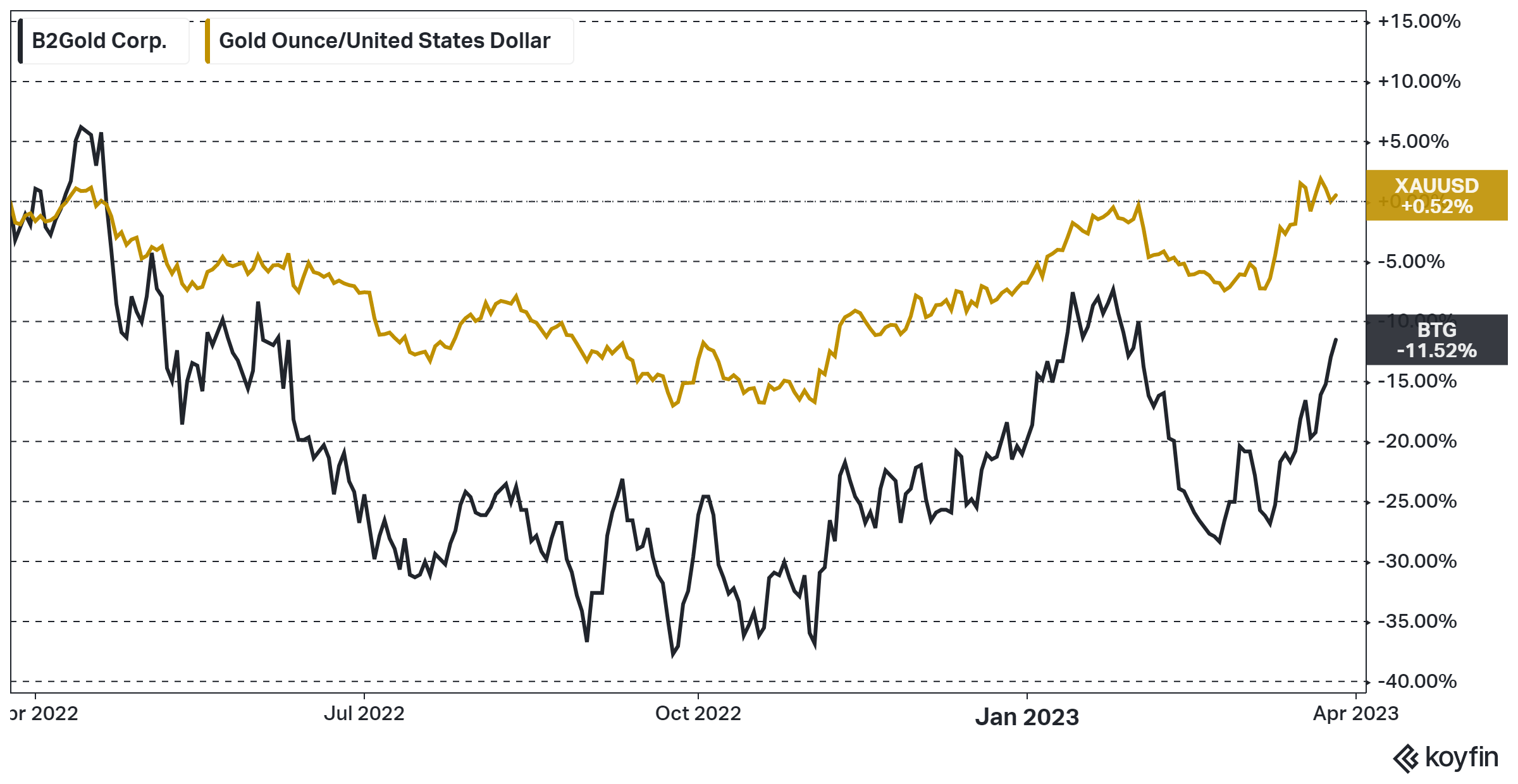

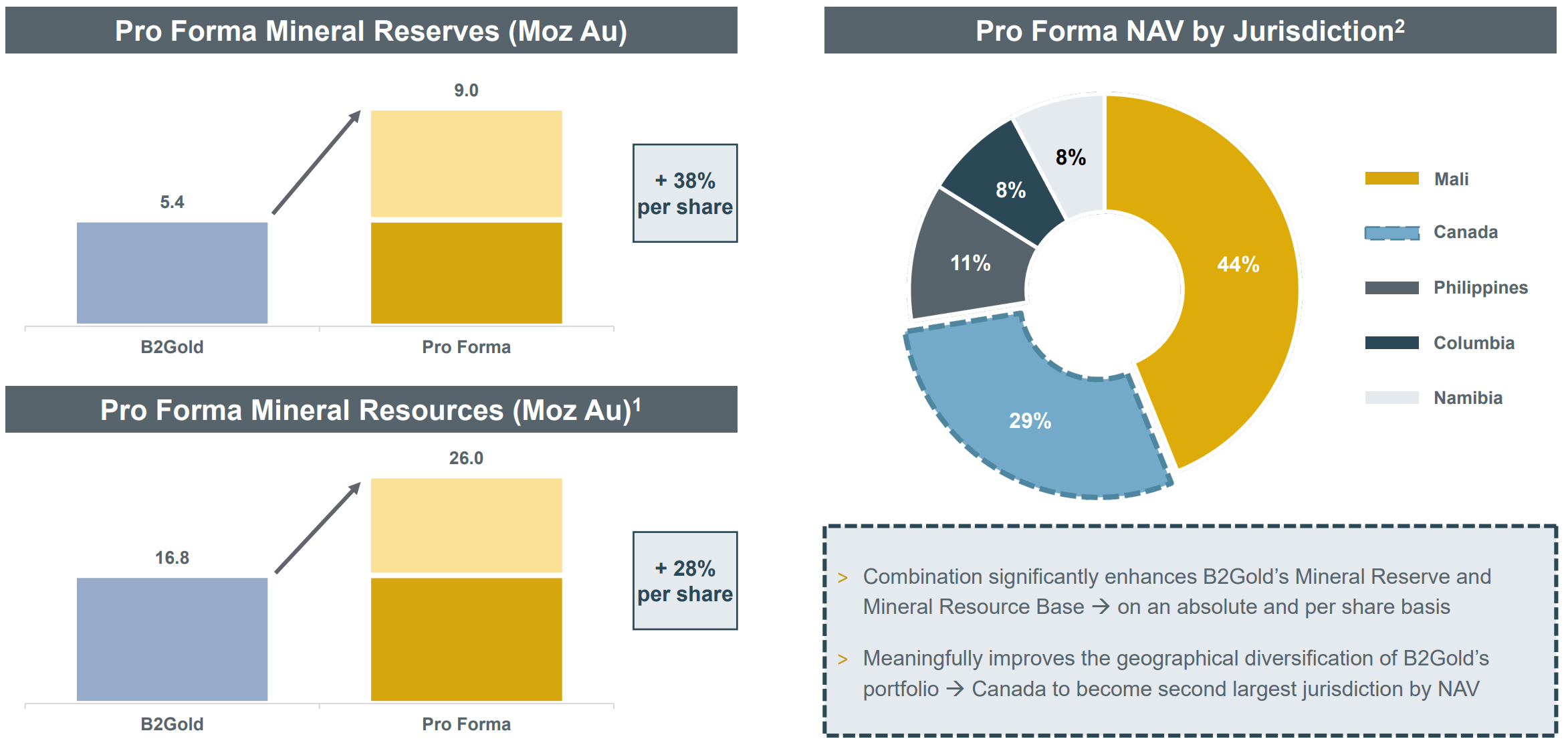

The stock price has underperformed the price of gold over the past year, which is true for many miners, but part of the recent decline came when the C$1.1B all-share acquisition of Sabina Gold & Silver ( SGSVF ) was announced . This could potentially be an opportunity as the acquisition seems like a good fit for B2Gold. It will improve the jurisdictional risk of B2Gold and significantly boosts the company's total reserves, which are two areas the company has been criticized for.

Geopolitical Risk

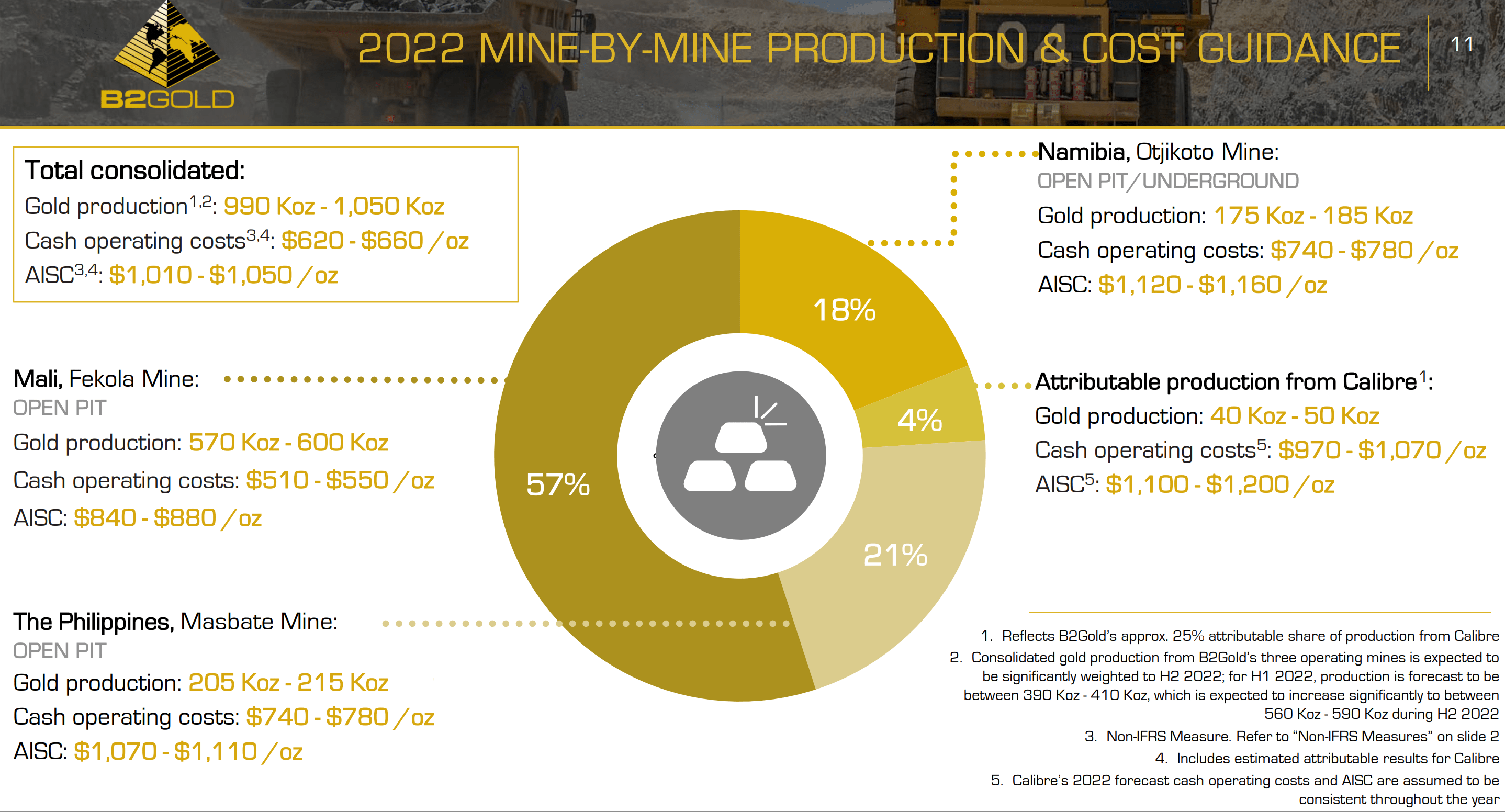

The below slide illustrates B2Gold's gold production and cost guidance for 2022. We can see that more than 50% of the production comes from Mali and the rest are from countries like Namibia, and The Philippines. There is also an ownership interest in Calibre Mining ( CXBMF ), which primarily operates in Nicaragua. I would argue just about all these countries do carry more geopolitical risk.

Figure 2 - January 2023 Corporate Presentation Figure 3 - January 2023 Corporate Presentation

{kind=link}

{kind=link}

B2Gold has however been very successful operating in more challenging jurisdictions for quite some time. It has also in my view become increasingly difficult to predict geopolitical events, which is why diversification is an approach I frequently employ. So, for anyone with an already large North American precious metals mining exposure in the portfolio, this could be an interesting addition.

Sabina Gold & Silver Acquisition

The C$1.1B all-share acquisition of Sabina Gold & Silver was announced on the 13th of February . The acquisition implied a 45% premium to the 20-day volume weighted average price, which probably makes it relatively likely to close, even if the deal will need to be voted on by the shareholders in April.

The initial market reaction on the announcement was to sell off B2Gold, but I like this deal for a reasonable cost. We are looking at a 20% increase in the number of shares, and it would substantially improve B2Gold's overall geopolitical exposure and long-term growth prospects. I know retail owners of junior development companies always want closer to full price, but there are always risks in developing large remote projects like this, so I do think the price is relatively fair.

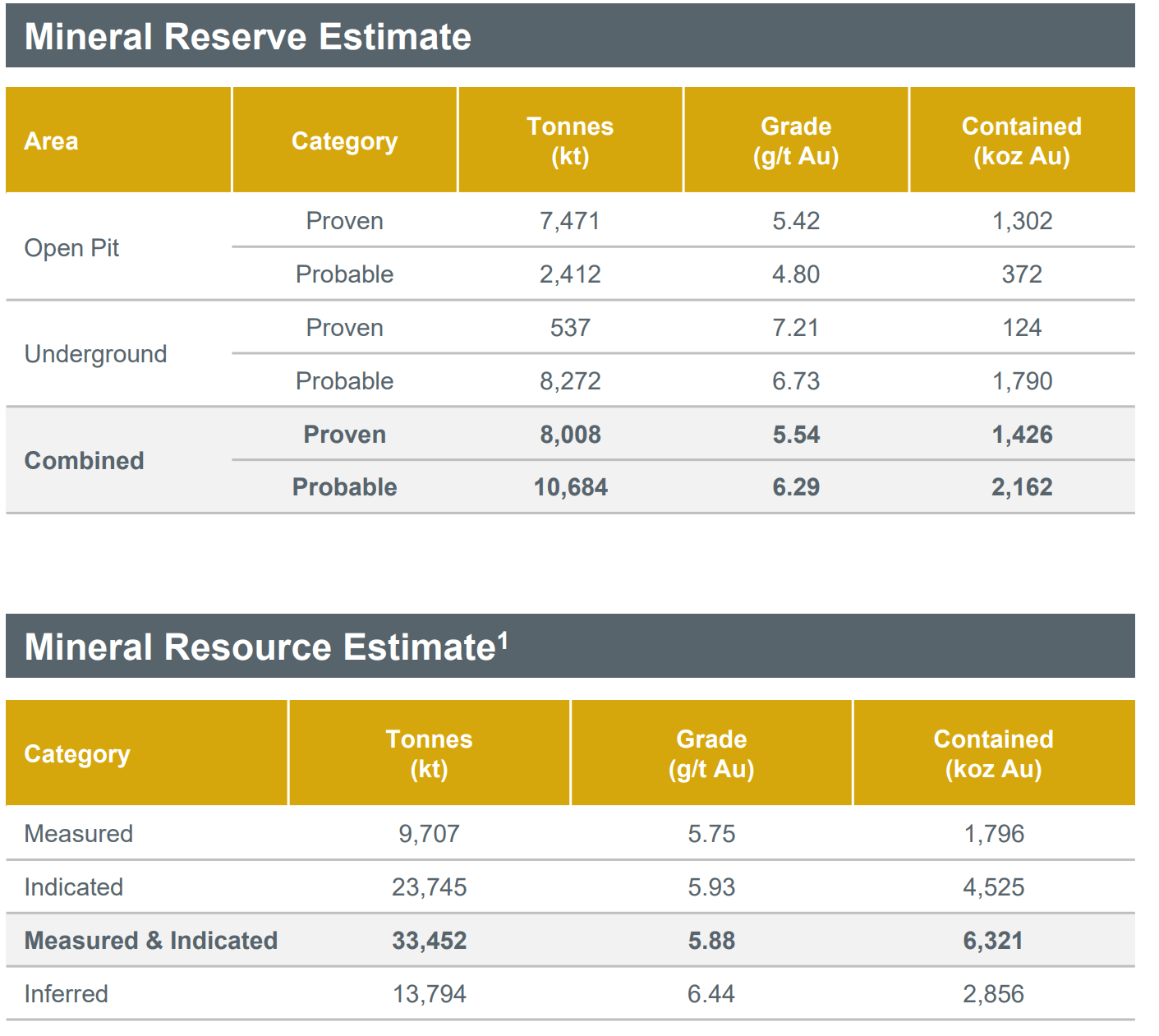

Sabina Gold & Silver has permitted assets in Nunavut, Canada. Where we are talking about 3.5Moz of reserves and more resources at extremely attractive open pit grades, around 6 g/t. This is an asset which could be in production as early as Q1 2025 if everything goes according to the plan and has substantial growth potential in the long run as well.

Figure 4 - B2Gold February 2023 Acquisition Presentation

{kind=link}

Valuation

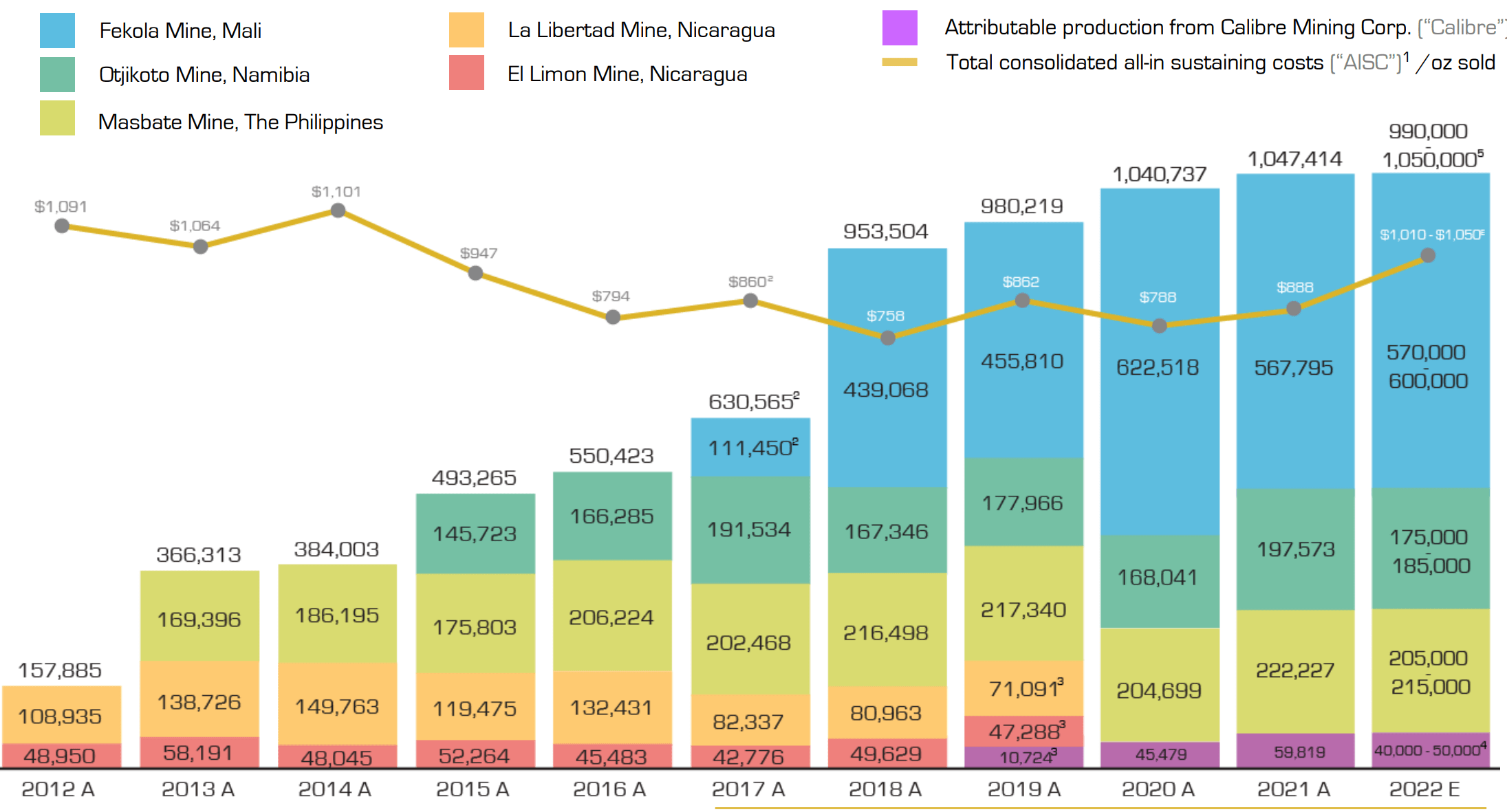

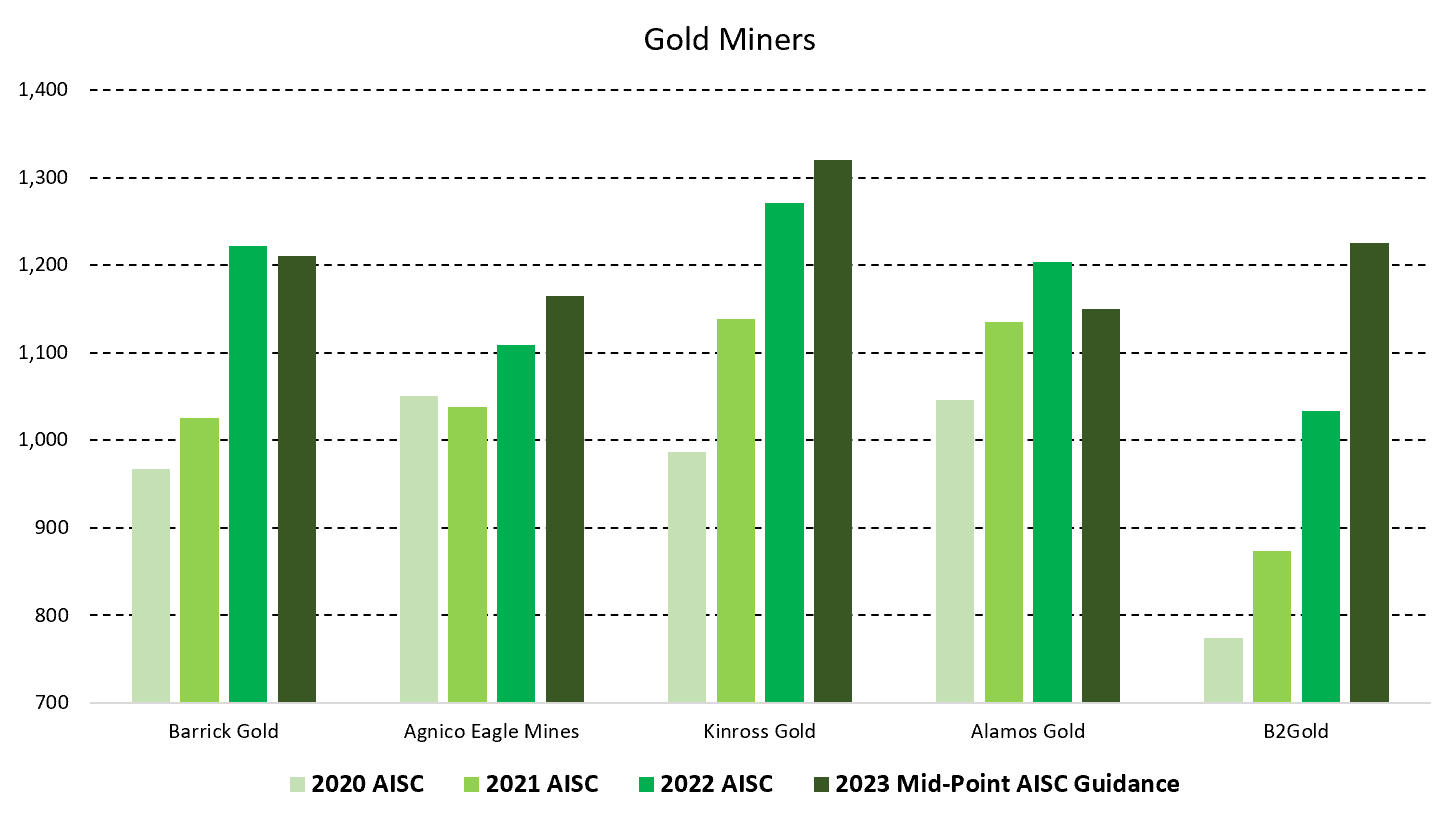

Over the last few years B2Gold has seen its All-In Sustaining Cost increase and the 2023 guidance is now just above $1,200/oz, in line with many other larger gold producers.

{kind=link}

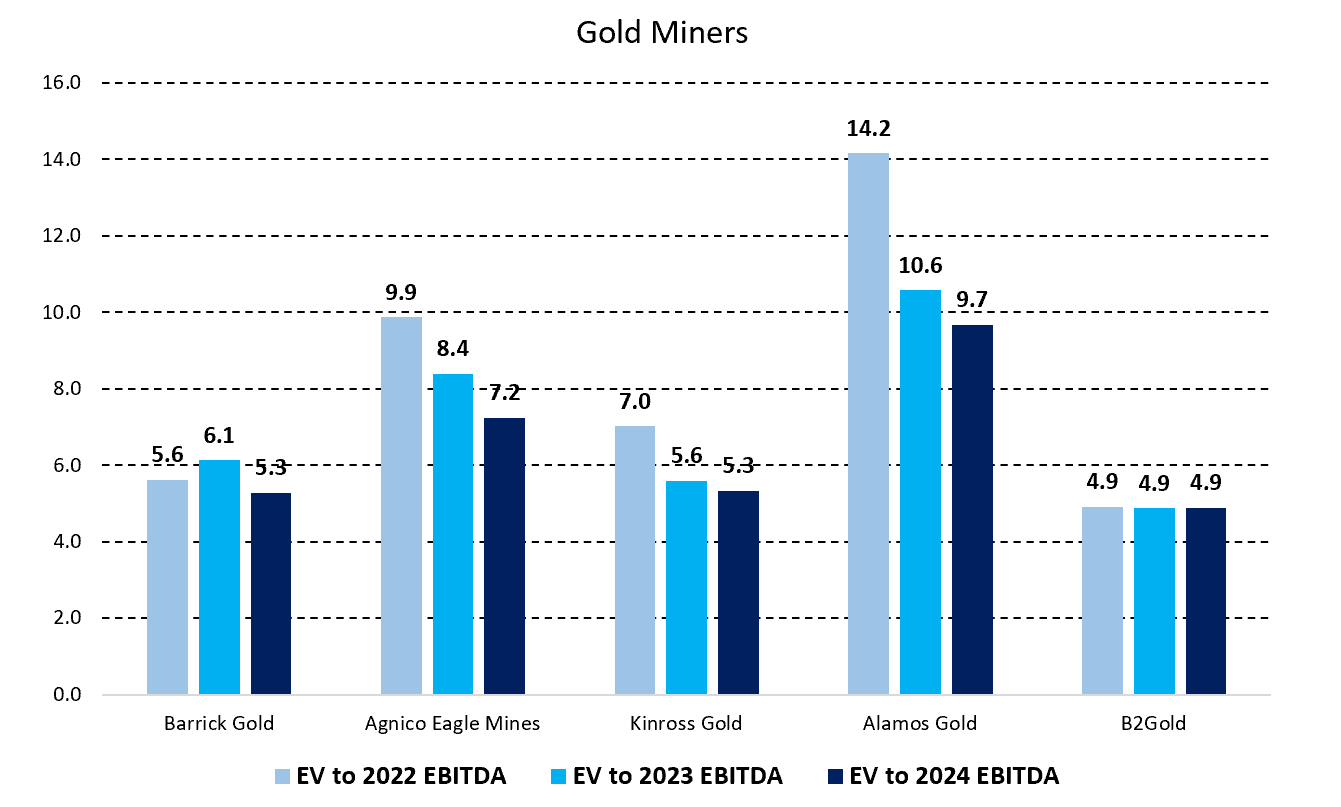

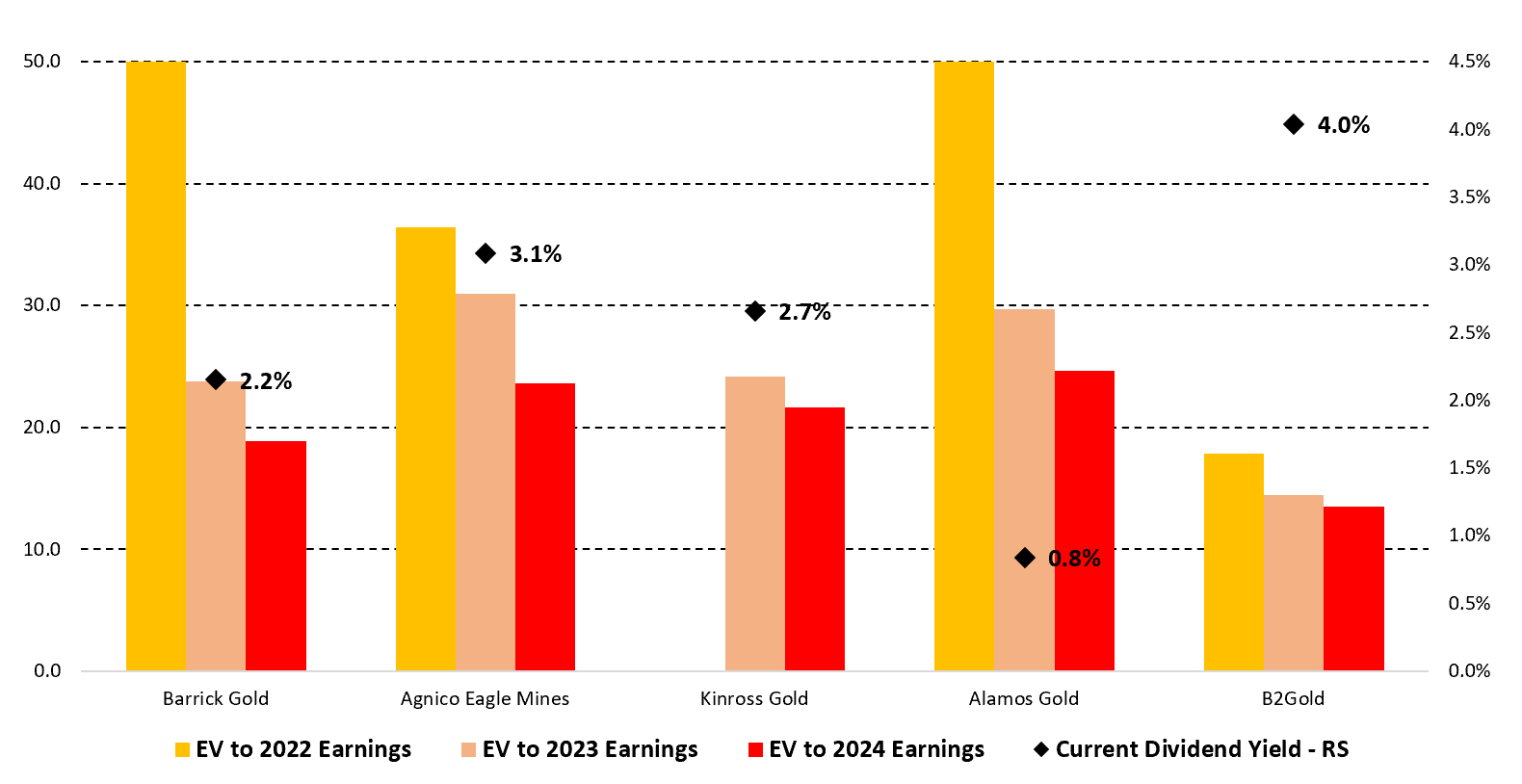

The below charts illustrate the EV to EBITDA and EV to Earnings for B2Gold and a few other gold producers, with comparable AISCs in 2023. Note that the figures for B2Gold have been adjusted for the expected 20% increase in the share count, and the other reported figures are from Q4-22.

Figure 6 - Data from Koyfin Figure 7 - Data from Koyfin

{kind=link}

{kind=link}

B2Gold trades with a substantially lower earnings multiple compared to the peers, with an EV to Earnings around 14 for 2023 and 2024. The dividend yield is also more attractive than the other companies at 4.0%.

Conclusion

With $57M in debt and $652M in cash as of Q4-22, there are no leverage or liquidity concerns for B2Gold. The stock offers one of the most attractive dividends in the industry, together with very healthy margins. So, there is a lot to like about the company.

{kind=link}

The big question is whether the valuation is cheap enough for the higher geopolitical risk. For me, the answer is not quite. Provided the Sabina Gold & Silver deal is closed, the pro forma jurisdiction will improve, but we are still looking at a company with a very large portion of production coming out of Mali. So, the company carries higher concentration and geopolitical risk.

I would need an even larger valuation discount compared to peers to add B2Gold to the portfolio. It is worth pointing out that another reason for the lower valuation multiple, is the lower reserve life than some of the peers. So, it is not all due to geopolitical risk.

With Sabina Gold & Silver, the company does have excellent growth prospects from 2025 and beyond, but that is still some ways out, and not enough incentive for me to invest today.

Figure 9 - B2Gold February 2023 Acquisition Presentation

{kind=link}

For further details see:

B2Gold: An Attractive Valuation, But Also More Jurisdictional Risk