BTG - B2Gold: An Exceptional Q4 Performance

Summary

- B2Gold released its preliminary Q4 and FY2022 results last month, reporting quarterly production of ~367,900 ounces, a record for the company by a wide margin.

- This was driven by continued plant outperformance at Fekola and high-grade ore from Phase 6 plus a much better quarter from Otjikoto with contribution from Wolfshag UG.

- Although this will translate to robust Q4 results, FY2023 will be a softer year from a free cash flow standpoint, impacted by sticky inflationary pressures & elevated stripping costs.

- Given the temporary margin compression year-over-year if gold prices don't average at least $1,950/oz this year, I believe it's best to buy share pullbacks vs. pay up for the stock near US$3.70.

B2Gold ( BTG ) has a strong track record of over-delivering on its promises, and it's done an incredible job of growing in a disciplined manner from a junior explorer in 2007 to one of the top 12 largest gold companies globally (assuming the Newcrest/Newmont deal is successful). However, 2022 looked like it was going to be a rare exception. The company needed a 330,000-ounce quarter to meet the bottom end of annual guidance. Miraculously, B2Gold didn't only deliver into its range (990,000 to 1,050,000 ounces) but came in above the mid-point with a monster quarter from its Fekola Mine in Mali.

This impressive performance has extended B2Gold's track record of consistently over-delivering on promises, and investors can rejoice that it didn't engage in over-priced M&A like some of its peers and didn't pursue growth at any cost like others. The result is that B2Gold heads into 2023 with one of the strongest balance sheets sector-wide, an aggressive exploration/development program that aims to turn its Fekola Mine into a future Malian Mining complex and ultimately a path to ~1.20 million ounces per annum post-2025 if Anaconda stand-alone is green-lighted. Let's take a closer look at the recent results below:

Fekola Operations (Company Presentation)

{kind=link}

Q4 & FY2022 Production

B2Gold released its preliminary Q4 and FY2022 results last month, reporting quarterly production of ~367,900 ounces, a record for the company by a wide margin. This represented an 18% beat vs. its previous record of ~310,300 ounces set in Q3 2021. The record quarter was driven by Fekola, which produced ~244,000 ounces in Q4, trouncing the mine's previous record of ~165,600 ounces reached five quarters ago. The exceptional performance was driven by another quarter of outperformance from the plant (~2.47 million tonnes processed) and a significant increase in grades, with high-grade ore coming from Fekola Phase 6.

B2Gold - Quarterly Production By Mine (Company Filings, Author's Chart)

{kind=link}

B2Gold noted that the strong plant performance was attributed to favorable ore fragmentation, availability of incremental saprolite feed to top up the mill, and optimization of the grinding circuit, allowing for a more than 30% outperformance vs. nameplate capacity (~7.5 million tonnes per annum). Meanwhile, head grades came in at an impressive 3.31 grams per tonne of gold, with full production during the quarter from Phase 6 benefiting from improvements to the pit dewatering system. These figures far exceeded my estimates of ~2.35 million tonnes at 3.02 grams per tonne of gold, resulting in a significant beat vs. my rough (and clearly too conservative) estimate of ~216,000 ounces produced in Q4.

Fekola Operations (Company Presentation)

{kind=link}

Given the strong finish to the year at Fekola, B2Gold's flagship asset churned out ~598,700 ounces of gold on an annual basis, finishing the year well above its guidance mid-point of 585,000 ounces and just shy of the top end of guidance despite heavier than normal rainfall at the Fekola site. Looking forward, B2Gold is projecting another strong year ahead for the asset, with FY2023 guidance of 580,000 to 610,000 ounces, helped by a minor contribution from Bantako (incremental saprolite ore) and primarily ore from the Fekola and Cardinal pits, with plans to operate the plant at ~9.0 million tonnes per annum with an average grade of 2.20 grams per tonne of gold.

Moving over to the company's Otjikoto Mine, we also saw a much stronger Q4 performance, though production came in slightly below my estimates of ~62,000 ounces at ~60,100 ounces. This resulted in production coming in well below the initial annual guidance mid-point of 180,000 ounces and the revised guidance range of 165,000 to 175,000-ounce annual guidance range. That said, B2Gold reported record monthly production in December of ~30,500 ounces as it benefited from the ramp-up of underground mining at Wolfshag, and production rates are at budgeted levels to start 2023 and mined ore tonnage/grade are reconciling well with the resource model, both encouraging signs for a better year ahead.

Based on B2Gold's guidance in its Q4 preliminary results, Otjikoto should see a significant step-up in production, with FY2023 production expected to come in at 200,000 ounces at the mid-point, a 24% increase in production year-over-year. This is expected to drive a meaningful improvement in unit costs despite inflationary pressures. All-in-sustaining costs [AISC] are expected to come in at $1,110/oz at the mid-point vs. an FY2022 initial guidance mid-point of $1,140/oz and actual costs well of ~$1,200/oz.

Otjikoto Operations (Company Website)

{kind=link}

Finally, looking at Masbate in the Philippines, the mine had a solid year. Still, it didn't manage to deliver on its upwardly revised guidance (but it delivered into the top end of initial guidance) due to a weaker Q4 than planned. The miss was related to lower gold recovery rates (68.3%) due to the planned processing of an increased mix of sulphide and transitional ores due to changes in the mining sequence. Regarding FY2023, Masbate's production will drop off due to lower grades with a mix of fresh ore from the Main Pit and low-grade stockpiles. Fortunately, the planned increase in production at Fekola and Otjikoto will offset the dip in production at Masbate.

B2Gold - Quarterly Revenue (Company Filings, Author's Chart)

{kind=link}

Following the solid quarter of production, B2Gold reported record quarterly revenue of $592.5 million despite a much lower gold price ($1,746/oz), helped by the surge in sales volume. On a full-year basis, the huge quarter helped to push annual revenue to ~$1.73 billion, even with an average realized gold price below $1,790/oz. So, with similar output expected this year and what should be a higher average realized gold price, we should see another year of higher revenue (~$1.80+ billion), with B2Gold able to bolster an already strong balance sheet despite a year of elevated capital spending.

FY2023 Outlook

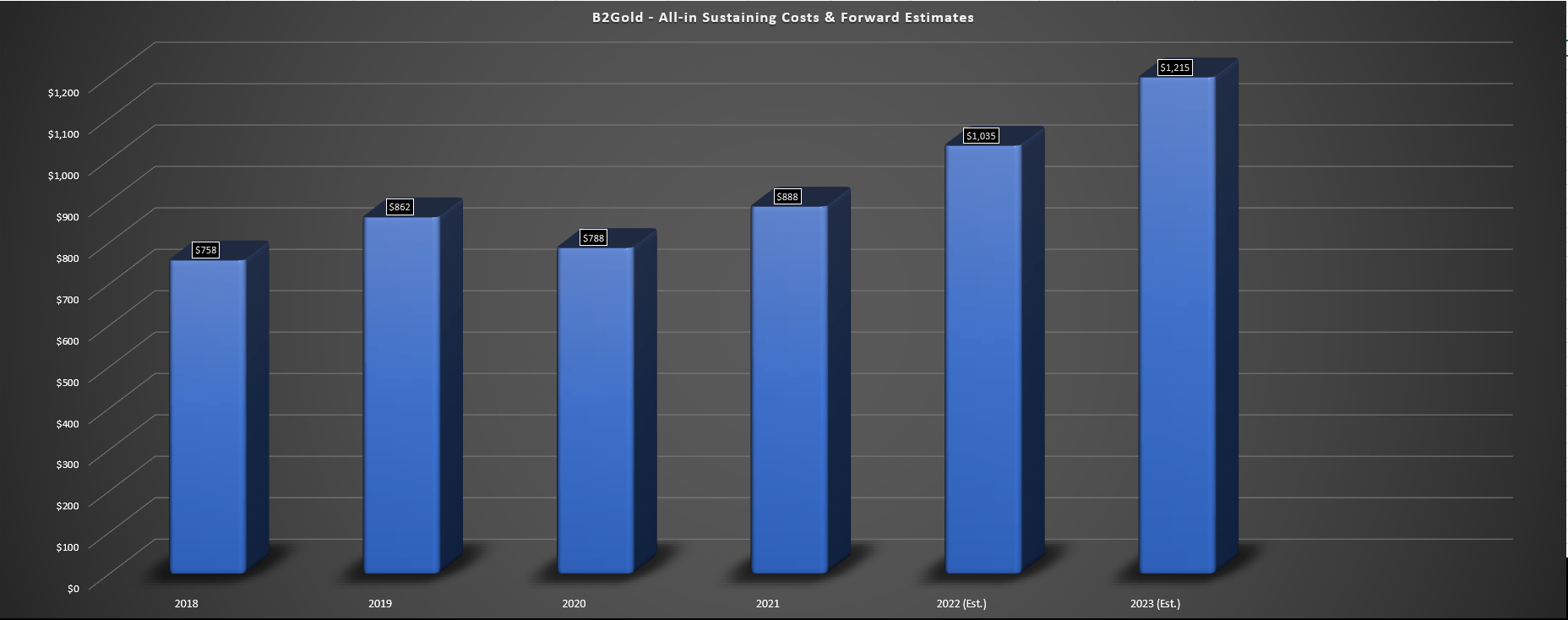

Although 2022 ended with a bang and FY2023 production is expected to remain robust with the guidance of 1,000,000 to 1,080,000 ounces, B2Gold's cost profile leaves much to be desired. This is based on expected cash costs of $700/oz and AISC of $1,225/oz at the mid-point, a significant increase from its FY2022 guidance mid-point of $640/oz and $1,030/oz, respectively, and actual costs that are likely to land closer to $660/oz and $1,035/oz. The sharp increase in costs is related to sticky inflationary pressures (fuel, labor, consumables) plus higher capital stripping expenditures at Fekola and Otjikoto, with ~$170 million in capitalized stripping/capitalized development combined at these two assets alone.

B2Gold - Annual Gold Production & 2023 Estimates (Company Presentation)

{kind=link}

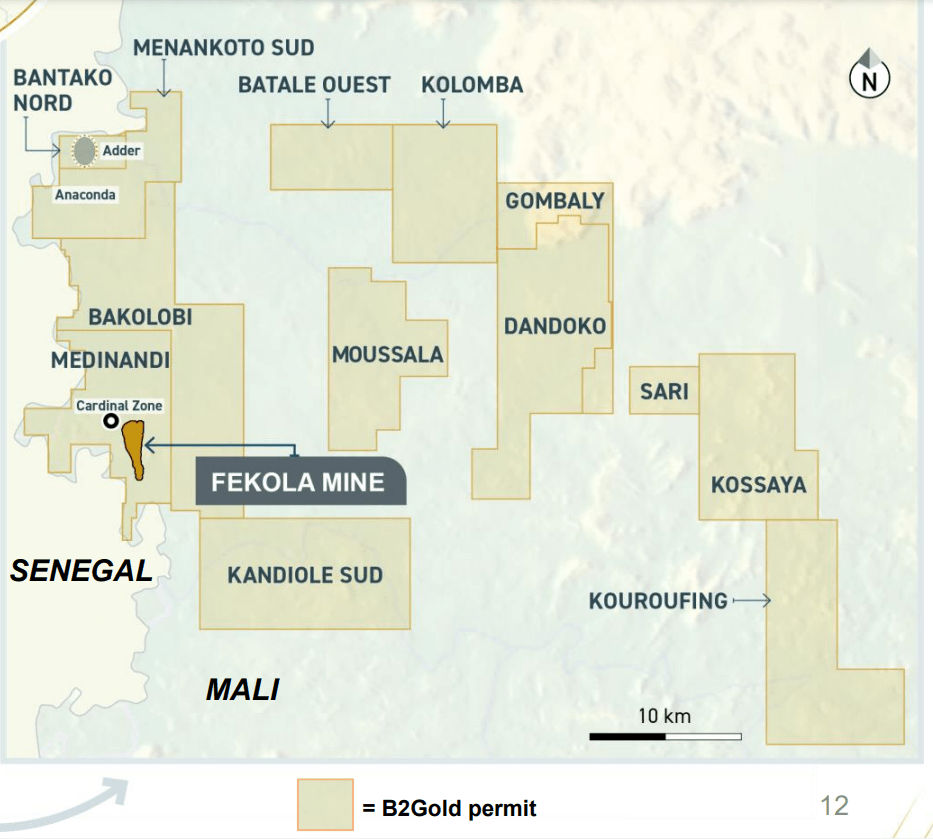

In the case of Fekola, the increase in capex is related to capitalized stripping ($101 million), new and replacement Fekola equipment and capitalized rebuilds ($51 million), and $35 million for the construction of a new TSF. Meanwhile, from a growth capital standpoint, B2Gold plans to spend ~$140 million on developing and equipping its Anaconda (north of Fekola Mine) and Dandoko projects (northeast of Fekola Mine) and $54 million for underground mine development at Fekola. Finally, $16 million will be spent on a haul road to the Anaconda and Dandoko projects. The result is that Fekola's costs will soar to $1,115/oz at the mid-point of guidance, well above the sub $950/oz costs expected last year.

Mali Land Package (Company Presentation)

{kind=link}

Although this is a significant cost increase that will impact the company's bottom line, and this heavier spending will lead to a sharp decline in free cash flow in FY2023, this is necessary spending to set the company up for a much larger mining complex down the road potentially and mine life extension by heading underground at Fekola. In fact, B2Gold is confident that it should be able to increase annual production from this complex by ~30% to 800,000+ ounces per annum, translating to a ~20% increase in B2Gold's production by as early as 2026. This is quite significant and combined with the exploration success it's enjoyed in Finland, there's certainly potential within this portfolio for 1.35+ million ounces long-term, even without an acquisition.

B2Gold - Annual AISC & Forward Estimates (Company Filings, Author's Chart)

{kind=link}

Although this is exciting news, we are likely to see a sharp decline in AISC margins this year, with AISC margins likely to come in at ~$660/oz even if B2Gold beats cost guidance and we assume an average gold price of $1,875/oz in FY2023. This would compare unfavorably to the estimated AISC margins of ~$750/oz in FY2022, with this margin compression despite a higher gold price. Meanwhile, although we should see a slightly higher output and a higher average realized gold price, free cash flow will decline materially with planned capital expenditures of ~$540 million, a more than 60% increase year-over-year.

Although this doesn't impact the dividend (which remains north of a 4.0% yield), and I would expect costs to dip below $1,060/oz in FY2024 as sustaining capital spend normalizes, this may lead to some underperformance in the stock. The reason is that while some producers could look at increasing their dividends and returning additional capital to shareholders through buybacks if we see a stronger gold price, B2Gold is likely to maintain its dividend and will most likely see margin compression year-over-year unless the gold price averages at least $1,950/oz which is unlikely. Let's look at the valuation:

Valuation & Technical Picture

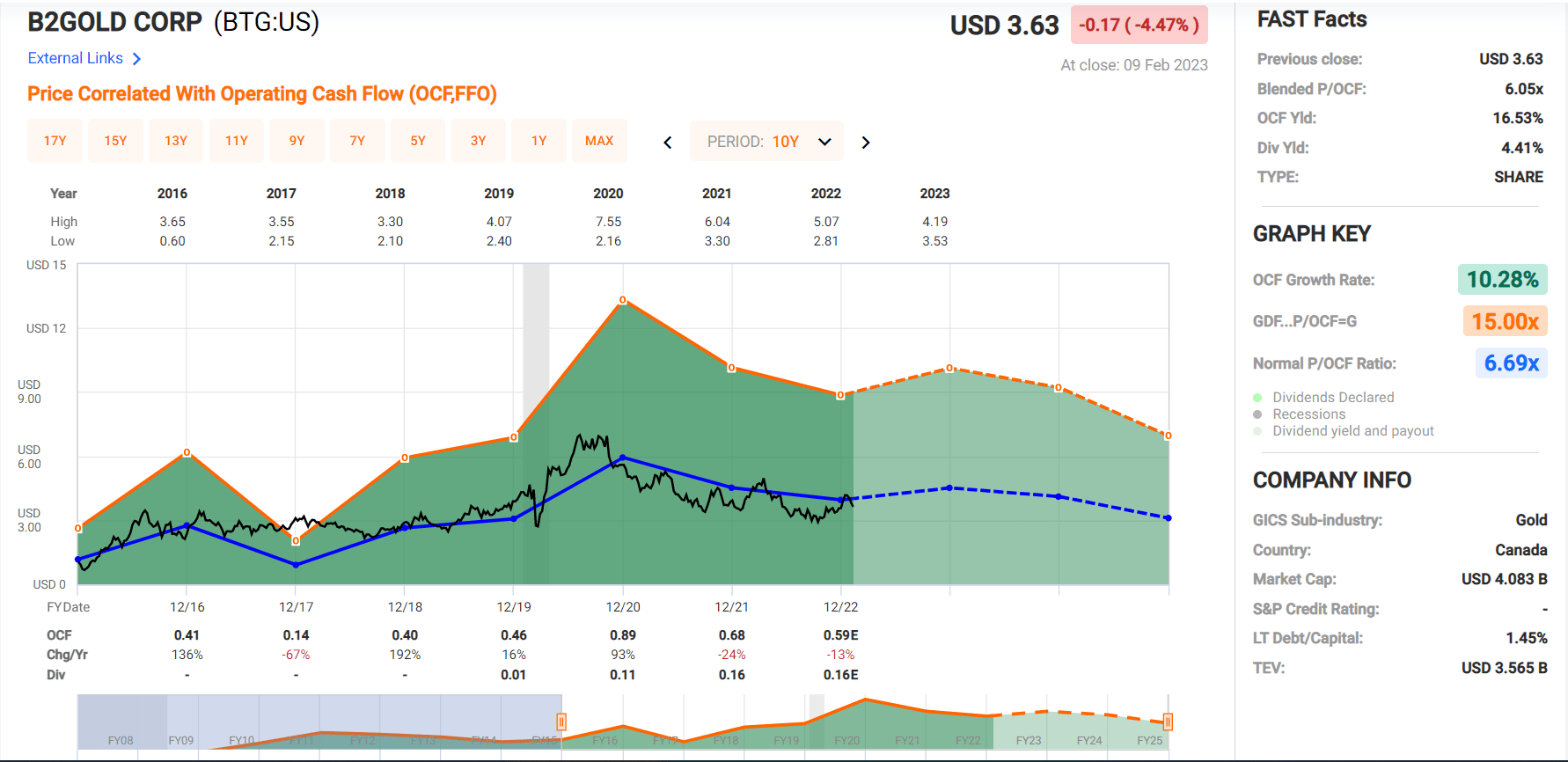

Based on my requirement for a minimum 35% discount to fair value to justify buying mid-cap producers, B2Gold is well outside my low-risk buy zone, which would come in below US$3.27. Obviously, there's no guarantee that the stock will retreat to these levels, but I prefer to buy at a deep discount to fair value and rarely ever pay up for cyclical names, and B2Gold spent plenty of time in this low-risk buy zone between September and October. So, while we should see an upgrade to its development pipeline (800,000+ ounces per annum post-2026) in its vision of a Fekola Complex, I believe the time to invest based on this potential was following the soft Q3 numbers and some uncertainty about meeting guidance, not after a record quarter and a 30% rally.

B2Gold - Historical Cash Flow Multiple (FASTGraphs.com)

{kind=link}

Moving to the technical picture, this recent pullback has improved B2Gold's technical setup, with BTG stock dropping back towards the mid-point of its support/resistance range. However, the stock is still hovering roughly 20% above major support. This is based on a new confirmed resistance level at US$4.20 and no strong support for the stock until US$2.90. Measuring from a current share price of US$3.63 translates to $0.73 in potential downside to support and just $0.47 in potential upside to resistance or a reward/risk ratio of 0.64 to 1.0. I prefer a minimum 5.0 to 1.0 reward/risk ratio to justify starting new positions, so I do not see this a low-risk buy setup in place just yet.

Summary

B2Gold put together a phenomenal finish to the year, and investors can look forward to its planned Q2 release of a stand-alone study for processing Anaconda area material at what could become a Malian mining complex for B2Gold (Fekola, Cardinal, Anaconda, Dandoko). Although this is an upgrade, FY2023 is expected to be a softer year due to increased stripping and sticky inflationary pressures sector-wide, resulting in a significant decline in free cash flow generation even if gold prices remain at current levels for 2023. So, while I continue to see B2Gold as one of the better producers sector-wide with an attractive yield, I see the ideal buy zone being at US$3.27 or lower.

For further details see:

B2Gold: An Exceptional Q4 Performance