BTG - B2Gold: Oversold Undervalued And In Growth Mode Again

2023-09-01 07:15:03 ET

Summary

- B2Gold has faced challenges including increasing jurisdictional risk in Mali and a lack of near-term growth prospects.

- The company's AISC has progressively increased, impacting its performance in the sector.

- B2Gold's acquisition of Sabina Gold & Silver and the development of the Back River project offer potential for growth and improved financial strength.

For the last three years, there were a few issues with B2Gold (BTG), mainly:

- Already elevated jurisdictional risk was increasing because of its Fekola mine in Mali.

- The company's growth had plateaued, as output was flat to slightly declining after breaking the 1 million ounce barrier in 2020, and BTG didn't have any near-term major growth prospects.

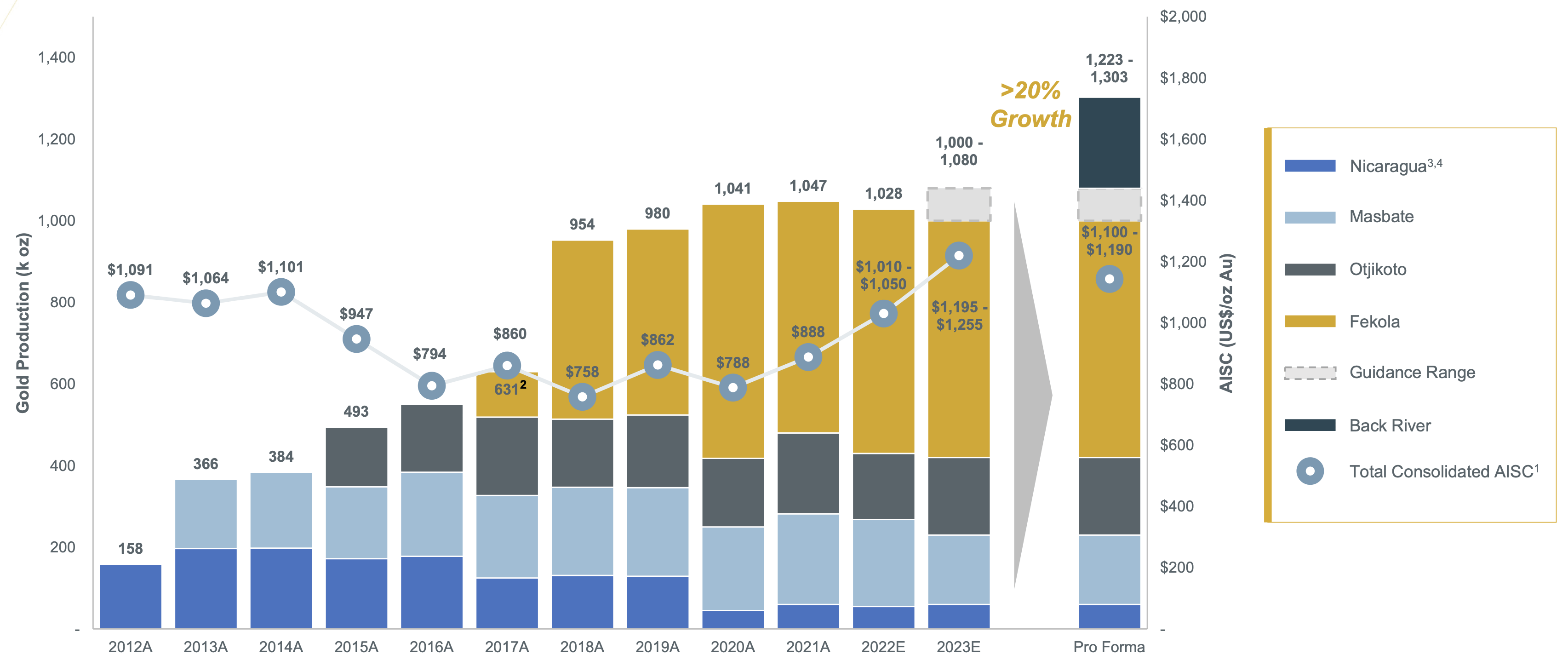

- Lower grades and recoveries at Fekola, combined with inflationary pressures, resulted in the company's AISC progressively increasing by over 50%, from $788 per ounce in 2020 to ~$1,200 per ounce this year.

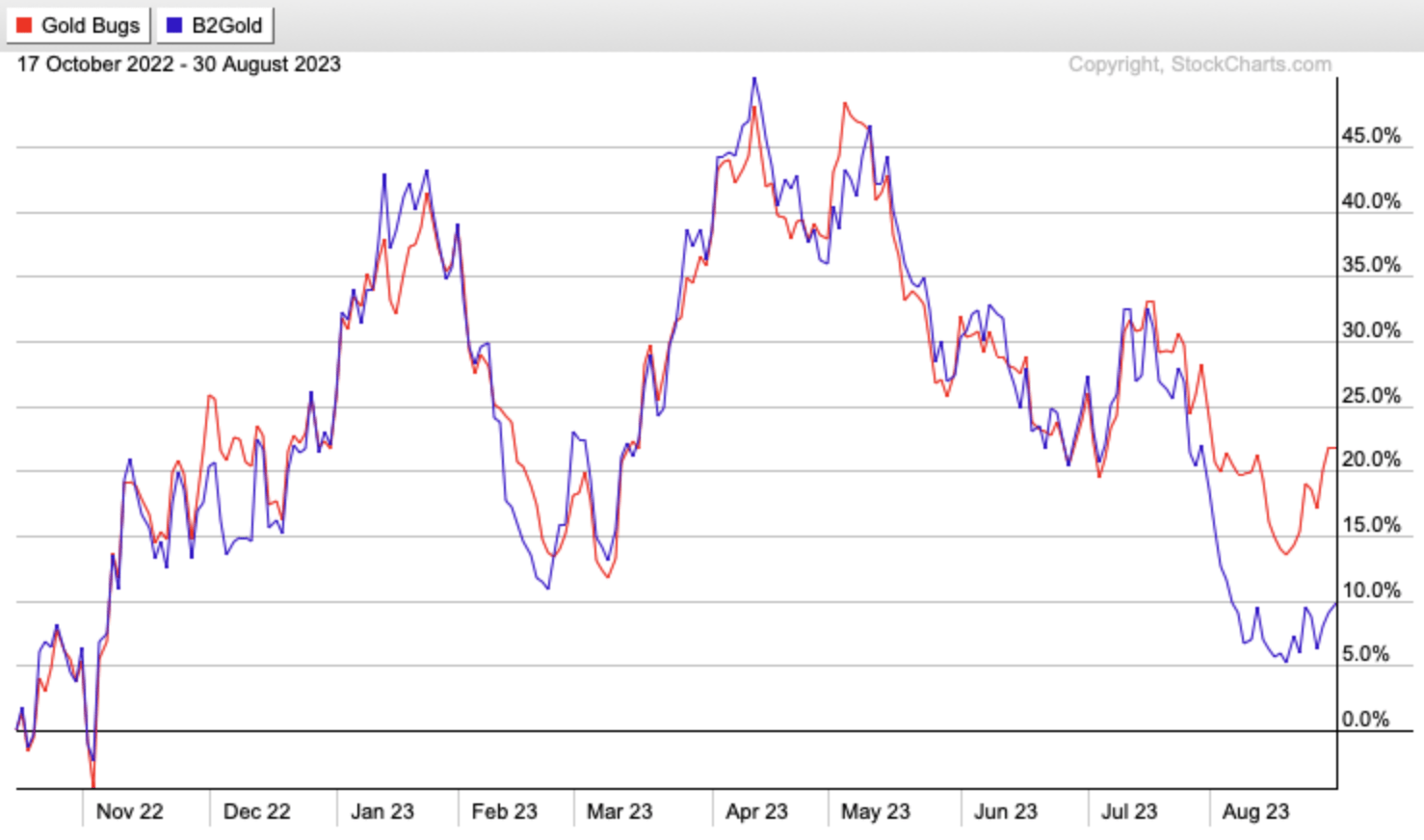

BTG has underperformed the sector since its peak in 2020 because of the just-discussed issues, as it's down over 50%, having notably lagged the group over the last year, with a 20% divergence between BTG and the HUI (an index of gold mining stocks) during that time. However, I believe B2Gold's shares are poised for a reversal higher as the stock is oversold and the company has strong growth in the pipeline again. After avoiding BTG as a long-term play over the past several years, I finally see an opportunity, especially if gold breaks out. Let's discuss.

StockCharts.com

The House That Clive Built

B2Gold is led by a proven management team and is one of the best mine builders and operators in the industry. Clive Johnson, CEO of B2Gold, has navigated the ship since the company's inception and steadily grew BTG into a 1+ million ounce, low-cost gold producer. It's not an easy feat to become a miner of this size - especially one with wide margins - and there have been very few hiccups along the way. It is a testament to Johnson and his team's abilities.

In terms of cash generation, BTG has been one of the more impressive miners. Over the last decade, the company's annual cash flow has increased 7-8x, or from ~US$100 million to over US$700 million, using the trailing 12 months of data. Despite the ~$400 per ounce surge in AISC, cash flow remains robust as the $150-$200 per ounce increase in the price of gold over the last few years has reduced the severity of the margin contraction. While BTG doesn't have the same cost advantage as it did before, it still remains a low-cost gold producer by comparison to its peers.

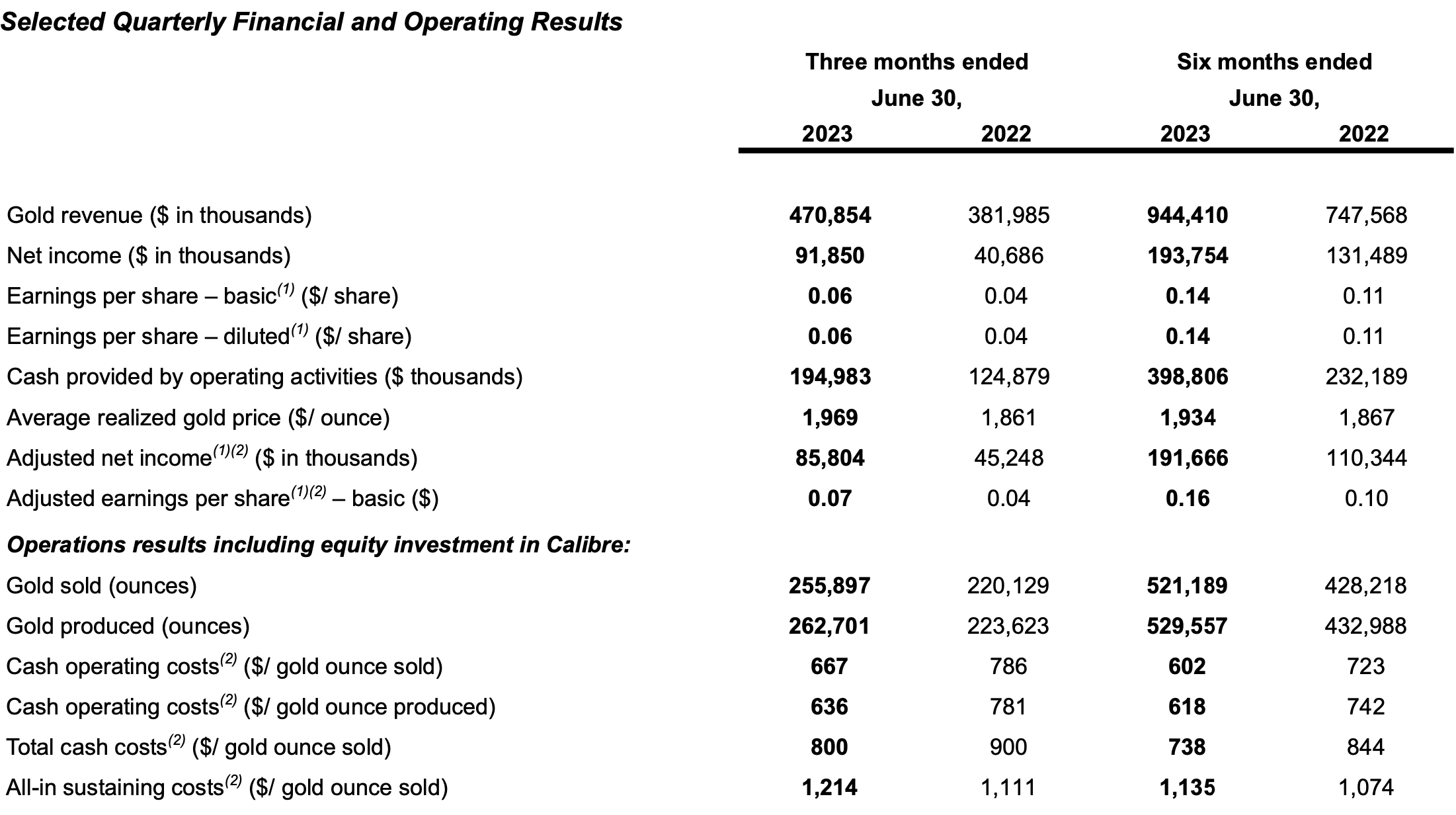

In the first six months of this year, B2Gold produced over 500,000 ounces of gold at an AISC of $1,135 per ounce. The average realized gold price was $1,934, giving the company a margin of almost $800 per ounce of gold sold. The free cash flow has been abundant, and B2Gold has one of the best balance sheets in the sector as a result.

{kind=link}

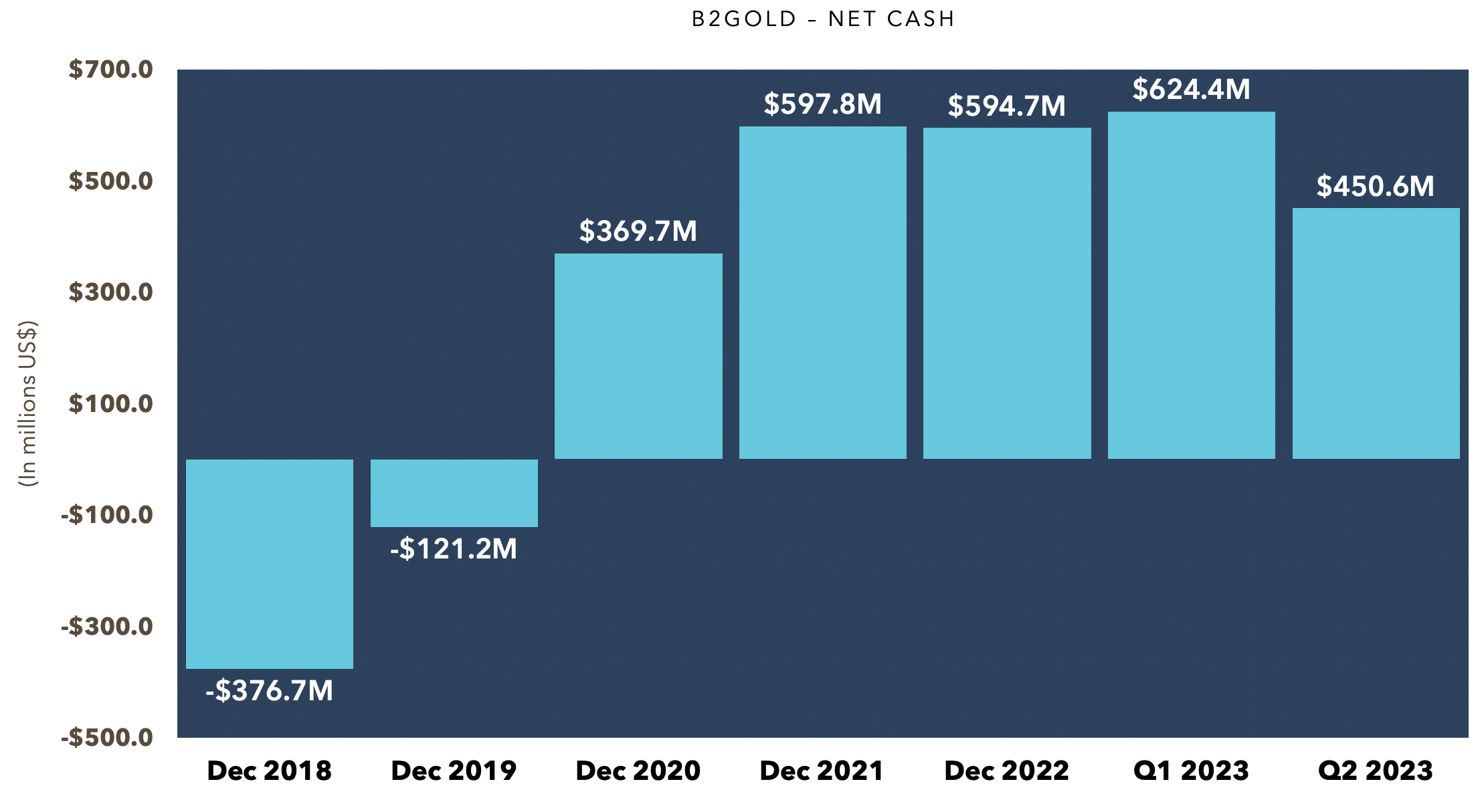

Analyzing the financial strength in more detail, there's been a ~US$1 billion turnaround in net debt over the last 4-5 years (from almost US$400 million of net debt at the end of 2018 to over US$600 million of net cash at the end of Q1 2023). Net cash dropped sharply last quarter because of the Sabina Gold & Silver acquisition, which saw the company spend $112 million to extinguish Sabina's construction financing obligations, including the senior secured debt facility for a $2 million payment, gold prepay facility for a $1 million payment, the entire gold metal off-take agreement for a $63 million payment, and one-third of the gold stream arrangement for a $46 million payment. The company is essentially debt-free, as it only had ~US$50 million of loans and lease obligations at the end of Q2 2023 and is sitting on just over $500 million of cash. Plus, it has $700 million untapped on its revolver, which gives it ~US$1.2 billion of liquidity. The net cash has grown little over the last few years as BTG is returning substantial cash to investors. The company expects to pay a $0.16 dividend this year, amounting to over $200 million distributed to shareholders. That gives investors an idea of the financial strength of the company. And not to be overlooked, that equates to a just over 5% dividend yield, which is another reason to like BTG at its current price.

{kind=link}

Now, let's address the main problem with BTG and the reason for the recent underperformance.

Fekola And The Proposed New Mining Code In Mali

The Fekola mine in Mali accounted for over 50% of the company's production. Fekola is an exceptional asset that generates robust cash flow, but the region has seen a surge in extremist activity and not one but two coups within the last three years.

In early April 2023, Mali's transitional authorities were reviewing mining contracts "after an official audit of the sector advised that the state was not receiving a fair share of gold-mining revenue."

The Malian government sought to renegotiate mining deals, and the news could significantly impact BTG.

It was a difficult situation to assess, with many unanswered questions. For example, was Mali targeting all mining companies in this review?

BTG owns 80% of Fekola, and the Malian government owns 20% and receives tax revenue from B2Gold. It wasn't clear how much more of the pie Mali wanted.

BTG was still holding up well at that time, but the comments made by the government about the review of mining contracts was a major red flag that investors were completely ignoring (likely because most were unaware of what had transpired).

This past July, we received more details, as according to a draft of the proposed new mining code, the government of Mali was looking to increase Malian state and private interests in new projects up to 35%, from up to 20% today. The government would initially receive a 10% stake in mining projects once a permit has been issued and also retains the option to buy an additional 20% within the first two years of commercial production. A 5% stake in new projects would go to local communities.

Another bill proposed as part of the law would require mining companies to employ more locals to top positions and put a cap on expatriate salaries.

BTG began to diverge from the sector only after the proposed new mining code was released, despite the warnings a few months prior of a potential change.

{kind=link}

It's still not 100% clear how this new mining code will impact the company. However, a few aspects give me some comfort.

First, given that the new bill (which has just been passed by parliament) allows for this additional 20% stake only within the first two years of commercial production, it doesn't seem that it would apply to the Fekola mine (or at least, the Fekola pit), as Fekola has been in production since 2017.

Statements earlier this month from Clive Johnson during B2Gold's Q2 2023 conference call support this assumption. Quote:

Any new mining code is not expected to impact the existing Fekola Mine operations, which will continue to be governed by the existing mining convention entered into under the 2012 Mining Code and the impact of the new 2023 mining code on Fekola Regional license -- sorry, I'll end it there.

So the bottom line is what we're saying is that the -- any proposed 2023 mining code that was not -- in my understanding and recent consultation with the government as last week, the government's confirming that they are not -- this code is not going to look back to previous existing code. That would be unlawful. The 2012 code and the mining convention that comes -- that came out of that dictates the terms; the ownership, 80/20, with ourselves and the government of Mali; and also dictate your taxes and all the details of that. That is in the code. And we expect this is implying to other gold miners in Mali as well who have valid outstanding codes and conventions from the past.

The company's COO also offered more color on the situation, which further relieves some concerns:

William Lytle

Absolutely. I mean what we've been saying over the last quarter in which I just validated being down there for 2 weeks, was that the Malian government considers B2 kind of the poster child of what they want in mining there.

So Clive didn't really hit on it, but the reality is that some of this talk about changing the mining code is really bringing up some of the other people that are not under the 2012 code to kind of what we're doing, right? So as far as we're concerned, we continue to have a very good relationship. And quite frankly, we expressed our concern on, one, really the way that these discussions around the mining code have been happening. And every one of the government officials I met was saying, we do not want to slow down mining in Mali. It is a cornerstone for our economy.

The Fekola pit still contains over 4 million ounces of gold resources and has many strong years ahead of it. If these ounces remain under the old code - and from what BTG is stating and what's being reported in the news, that certainly seems the case - then the near to medium-term impact is zero.

{kind=link}

What isn't clear is how this new law will affect the regional targets/deposits BTG is looking to explore/mine, including the Anaconda area north of the Fekola pit, which the company has contemplated building a second mill to exploit. We have to assume - just to be conservative - that these deposits not in production would fall under the new code, but I still don't see a considerable impact, at least anytime soon.

In fact, after the proposed new mining code was announced, I told my subscribers at the time:

I'm more concerned about how investors will interpret the news than I am about the overall impact on B2Gold. Since hitting the wires, there's been about a 5% negative divergence for BTG compared to the performance of the HUI. So, not a significant reaction, but it's likely that many investors haven't seen the news. In the short term, there could be more downside risk in BTG than in other mining stocks.

As I thought might happen, BTG underperformed over the following weeks, as the stock dropped from $3.63 in mid-July to just under $3.00 by mid-August, or about an 18% loss, which was roughly twice the percentage decline of the HUI and GDXJ. BTG is the 5th largest component of the latter, further reflecting how poorly it's held up relative to its mid-cap peers. However, there are signs of a potential bottom, given how far BTG has declined, how oversold it is, and I believe the Mali news is now priced in (maybe more than priced in).

StockCharts.com

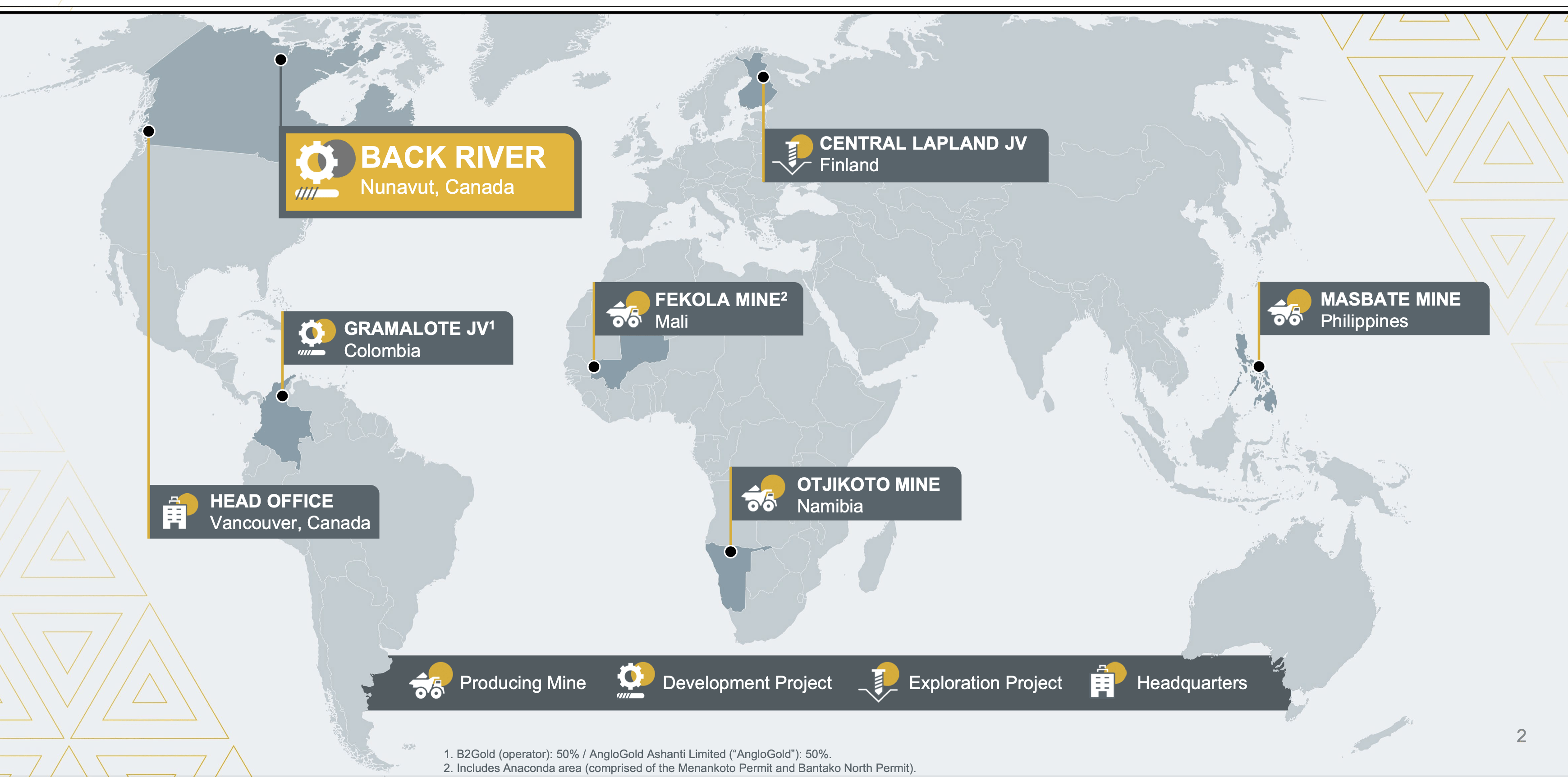

Back River Solves Several Problems

Earlier this year, B2Gold announced that it was acquiring Sabina Gold & Silver, which gave B2Gold a significant development project (Back River) in a Tier 1 mining jurisdiction, and it's the first foray into a "safe" jurisdiction for BTG. Clive Johnson and his team have always focused on higher-risk regions as they've successfully navigated the increased complexities and risks that come with operating in countries such as Mali, the Philippines, Namibia, and Nicaragua. This is a major shift in strategy for the company. One that I applaud.

{kind=link}

I've been bullish on Back River for years, pounding the table on Sabina at the lows in 2015 when it was trading at 30 cents. As I showed at the time, the NPV of Back River was around C$650 million at the then gold price and exchange rate, yet Sabina had a market cap of just US$66 million (or C$81 million). Since then, Back River has only gotten better, and the price of gold is substantially higher as well. B2Gold paid US$795 million (or C$1.06 billion) for Sabina, and this acquisition proves the bullish thesis was correct, even though trying to convince others was quite challenging. It also proves that while gold stocks can deviate greatly from their NAV and the market can severely underprice them, it doesn't stop these stocks from eventually reaching their fair value, or at least receiving a substantial re-rating.

I also appreciated what Clive Johnson said in the press release when the acquisition was announced:

Our extensive due diligence reinforced the scarcity of a gold district of the quality of Back River.

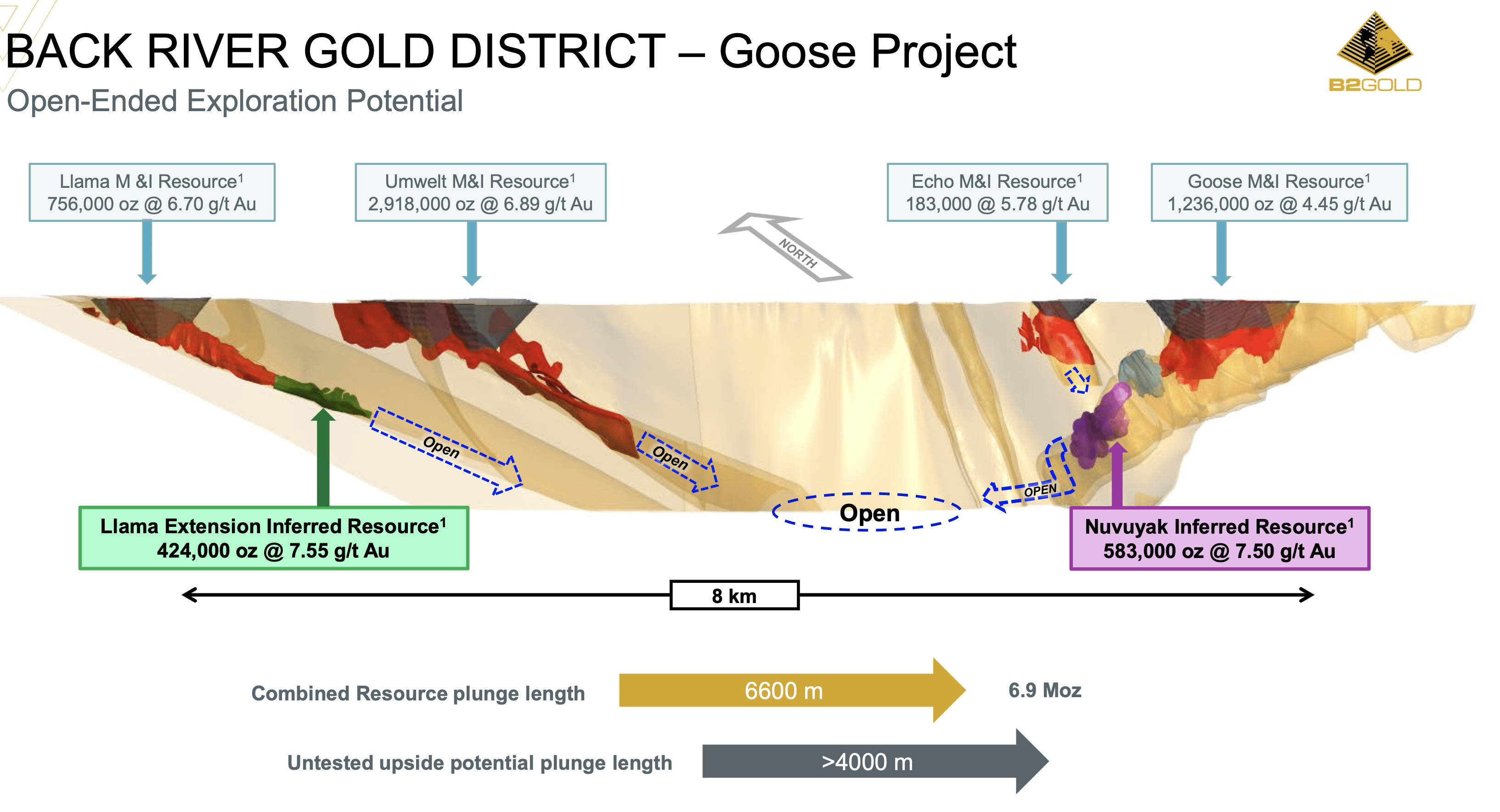

What makes Back River so special is the amount of ultra-high grade open-pit reserves/resources. There are ~1.7 million ounces of open-pit reserves at a grade of over 5 g/t. Most open-pit mines are around 1 g/t, and some of the best are 2-3 g/t. It's unusual to have this many open-pit ounces at this high of a grade.

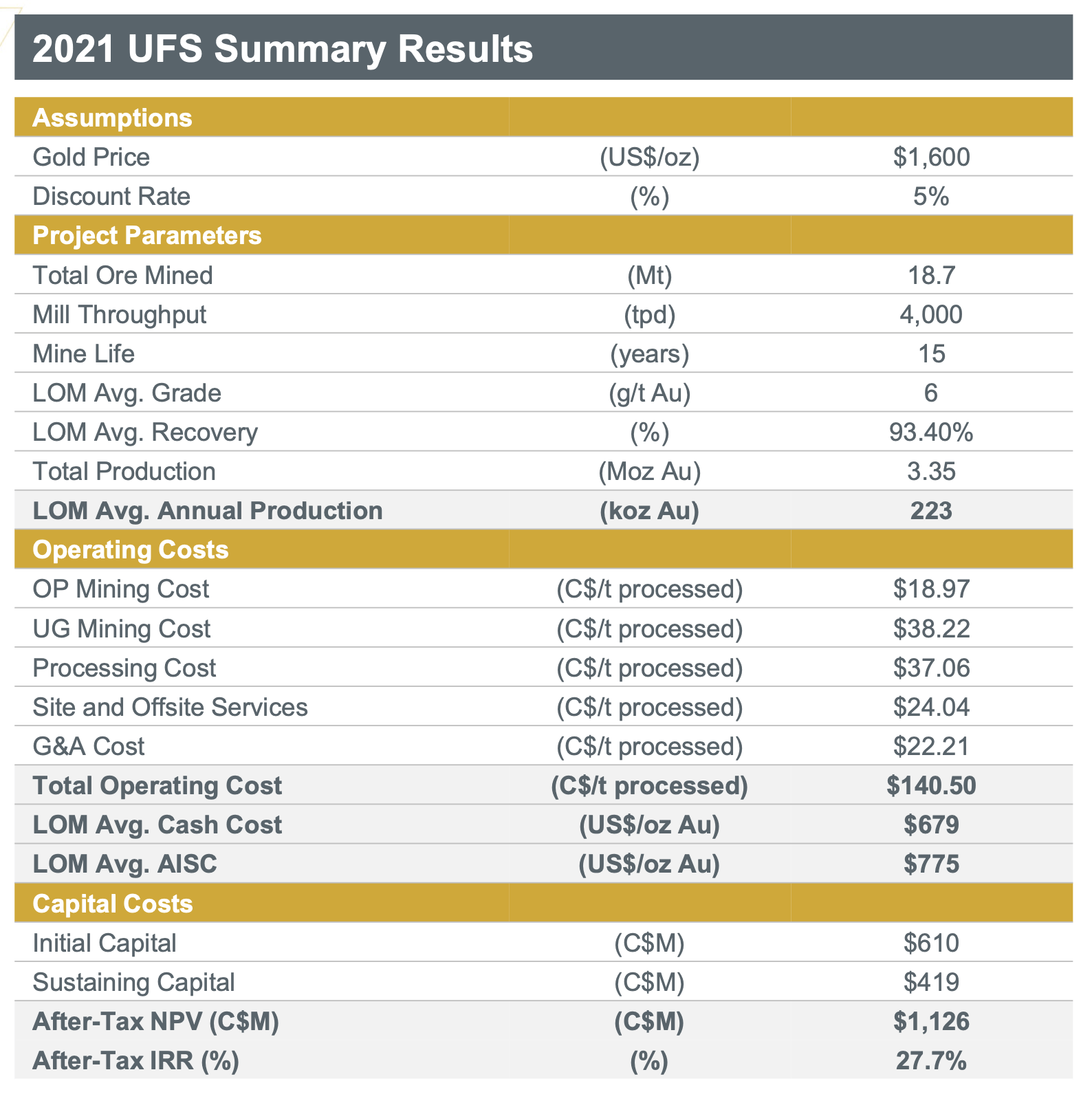

The 2021 updated Feasibility Study estimated the mine would produce 223,000 ounces of gold annually at an AISC of just $775 per ounce over a 15 year mine life. But that's just a starting point, as the FS only included 3.6 million ounces of gold of the almost 9.2 million ounces of total gold resources at Back River, and the exploration upside is off the charts. As B2Gold states:

The Back River Gold District has multiple high-potential mineralized zones which remain open, and we are confident that the district has strong untapped upside with numerous avenues for resource growth.

{kind=link}

Back River could be an asset that's in production for 2-3 decades, maybe longer.

The acquisition of Sabina was expected to result in production growth of greater than 20% for BTG - to over 1.2 million ounces of gold per year. However, Sabina, being a single-asset developer with limited funding, wasn't maximizing the potential of the project, and Clive and his team were looking to significantly expand the output at Back River. Since taking ownership, B2Gold has modified the plan and is increasing production to over 300,000 ounces of gold per year in the first five years of the mine life through accelerated development of the underground mine at Goose. At minimum, this "scale-up" of the project means that Back River will account for ~30% of production post-2025, which assumes the open-pit at Otjikoto winding down in a few years but underground and stockpile production at the mine continuing until 2031. Back River allows for BTG to enter growth mode again, helps lower the company's overall AISC, and meaningfully reduces the jurisdictional risk of the portfolio.

{kind=link}

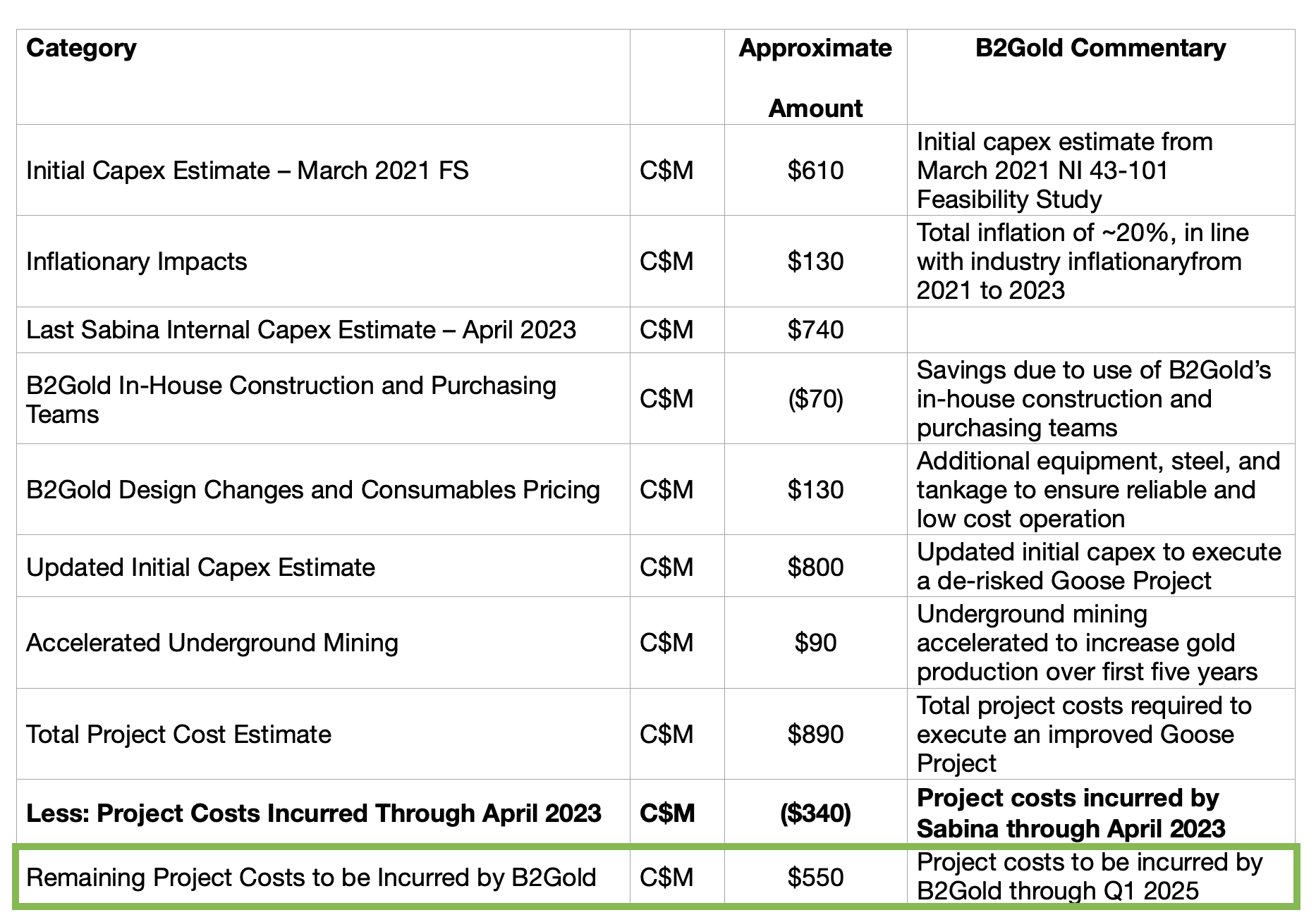

What also makes this acquisition so appealing for BTG shareholders is Sabina already invested a considerable amount of capital in the project by installing some of the infrastructure. Of the estimated C$890 million of total CapEx - which includes design changes by B2Gold to de-risk the project and increase gold production to over 300,000 ounces over the first five years - Sabina had spent approximately C$340 million. These are sunk costs, which effectively increases the NPV on a go-forward basis for BTG. The total project cost to be incurred by B2Gold through Q1 2025 (or when construction is expected to be complete) is just over US$400 million/C$550 million, and BTG has ample liquidity to fund construction. Given the project costs remaining and the free cash flow generated from this 1 million ounce per annum portfolio, I would expect B2Gold to maintain a healthy net cash position through the completion of the project.

{kind=link}

A team like B2Gold developing and operating Back River means that the mine and exploration potential will be fully optimized and realized. Sabina wasn't doing much exploration, as it was focused on development and project financing, but BTG is being aggressive on drilling because of the substantial upside.

All of the current deposits in the mine plan remain open at depth and are showing appreciable exploration potential.

{kind=link}

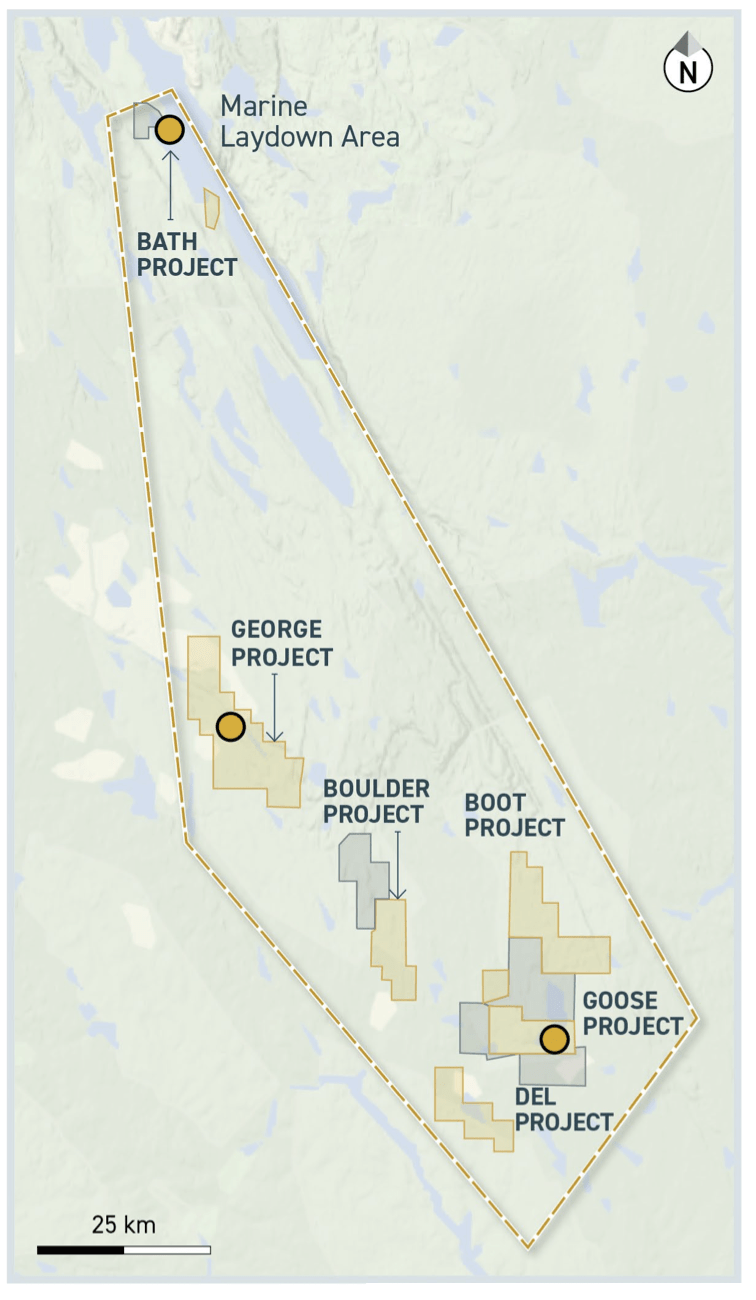

Also, the George project isn't part of the current mine plan, as it was removed due to the additional size and cost for Sabina. But with B2Gold's financial strength and expertise, the entire land package can now be aggressively explored and considered for inclusion in the project scope. If I had to guess, BTG will take the same path with Back River as they've done with other projects, including Fekola, which is continually increase the plant throughput and scale up the operation as more reserves/resources are proven up or added. What might start out as a 300,000+ ounce mine in early 2025 will most likely increase in several stages over the years that follow and could eventually become a 400,000-500,000 ounce gold operation.

{kind=link}

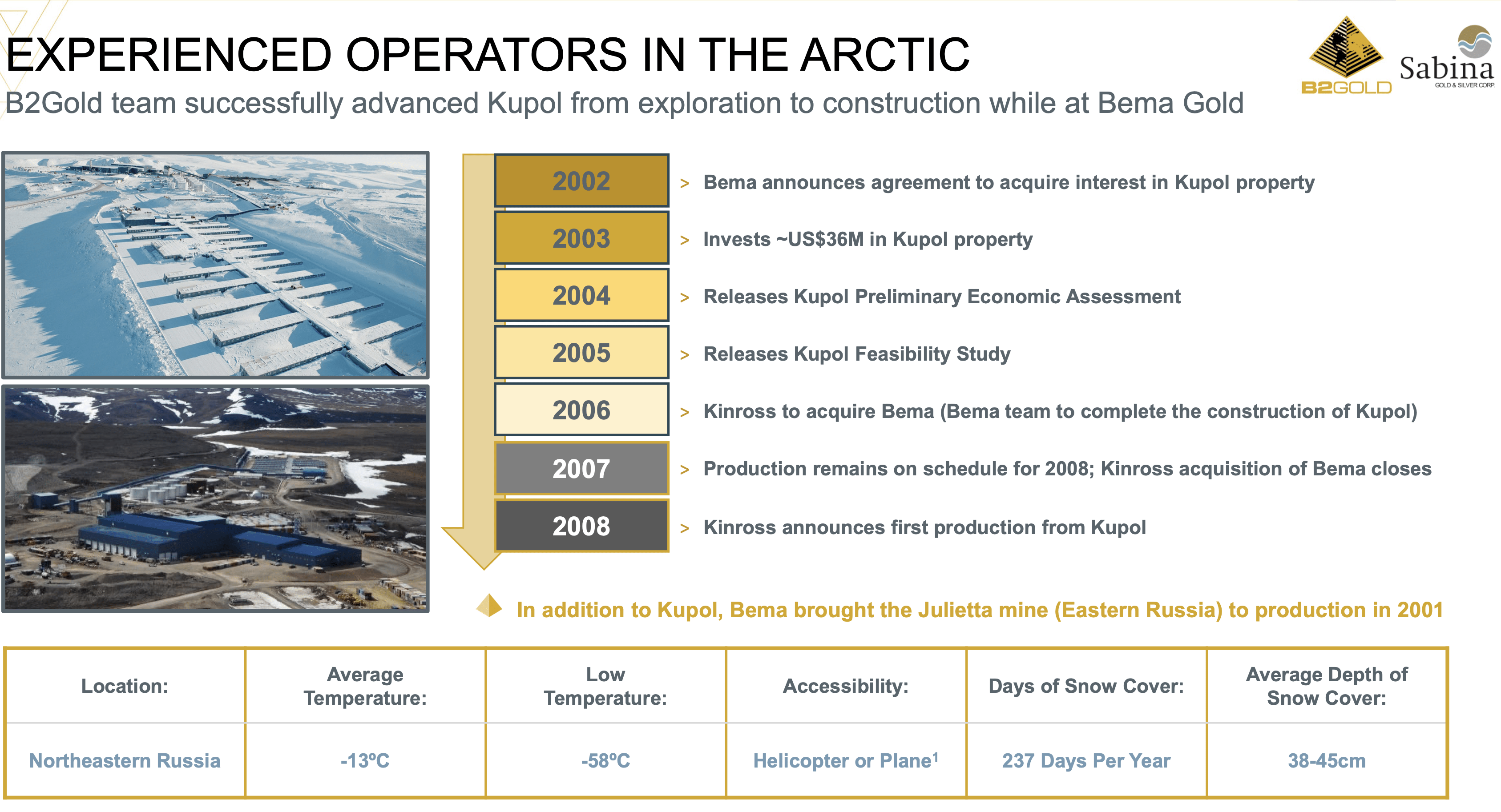

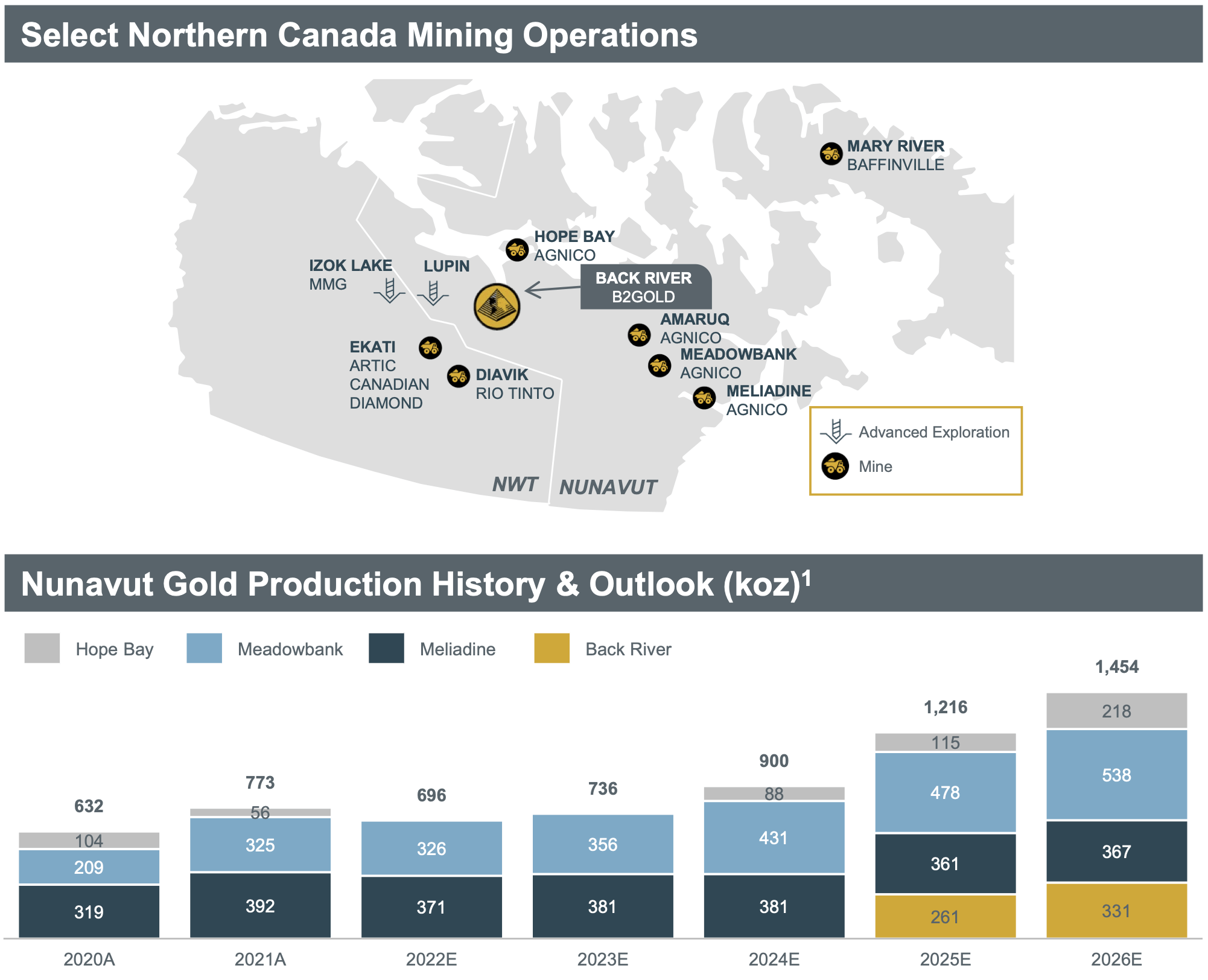

Back River is located in Nunavut, which is a highly challenging region to access and operate in because of the lack of development and cold climate. However, B2Gold's team has experience in the Arctic as they built the Kupol gold mine in Russia in the mid-2000s.

{kind=link}

Agnico Eagle - the only gold producer in Nunavut - has proven that mines in the region can be quite profitable. The company currently has two mines in production (Meadowbank and Meliadine) and a third (Hope Bay) that could come back online next year. Once Back River is in production in early 2025, it could rival Meliadine in terms of size and cash flow.

{kind=link}

Back River greatly improves the long-term outlook for the company and alleviates some of the concerns I've had about B2Gold's jurisdictional risk.

Valuation And Further Data That Supports The Bullish Thesis

B2Gold's current market cap is just over US$4 billion. Accounting for the ~US$450 million of net cash, its enterprise value is just over US$3.5 billion.

At the current gold price and CAD/USD exchange rate, the updated Feasibility Study released in early 2021 estimated the after-tax NPV of Back River was US$1.3 billion. However, costs have increased since then. We know how much CapEx has risen, but what isn't clear is where AISC will land. BTG has estimated around $1,000 per ounce, which is $225 per ounce higher than the $775 per ounce life of mine AISC estimated in the FS. But also keep in mind Sabina has already spent a significant amount of the CapEx, so that somewhat offsets the rise in CapEx and OpEx for Back River's go-forward NPV. The decision to increase the output at the start and bring forward a significant amount of production will also improve the NPV, so that needs to be factored in as well. I would estimate the current after-tax NPV (5%) is around US$1.1-$1.2 billion. That's just for the Goose project at Back River, and only includes a portion of the resources at Goose and none of the resources at George.

If BTG can maintain 300,000 ounces of gold production per year at $1,000 per ounce AISC over the original 15 year mine life (and there are plenty of ounces to accomplish this), the after-tax NPV (5%) of Back River is US$2+ billion.

Keep in mind BTG paid ~US$800 million for Sabina, so they clearly see far more upside than my first figure, and the second figure is likely a more accurate estimated fair valuation for Back River.

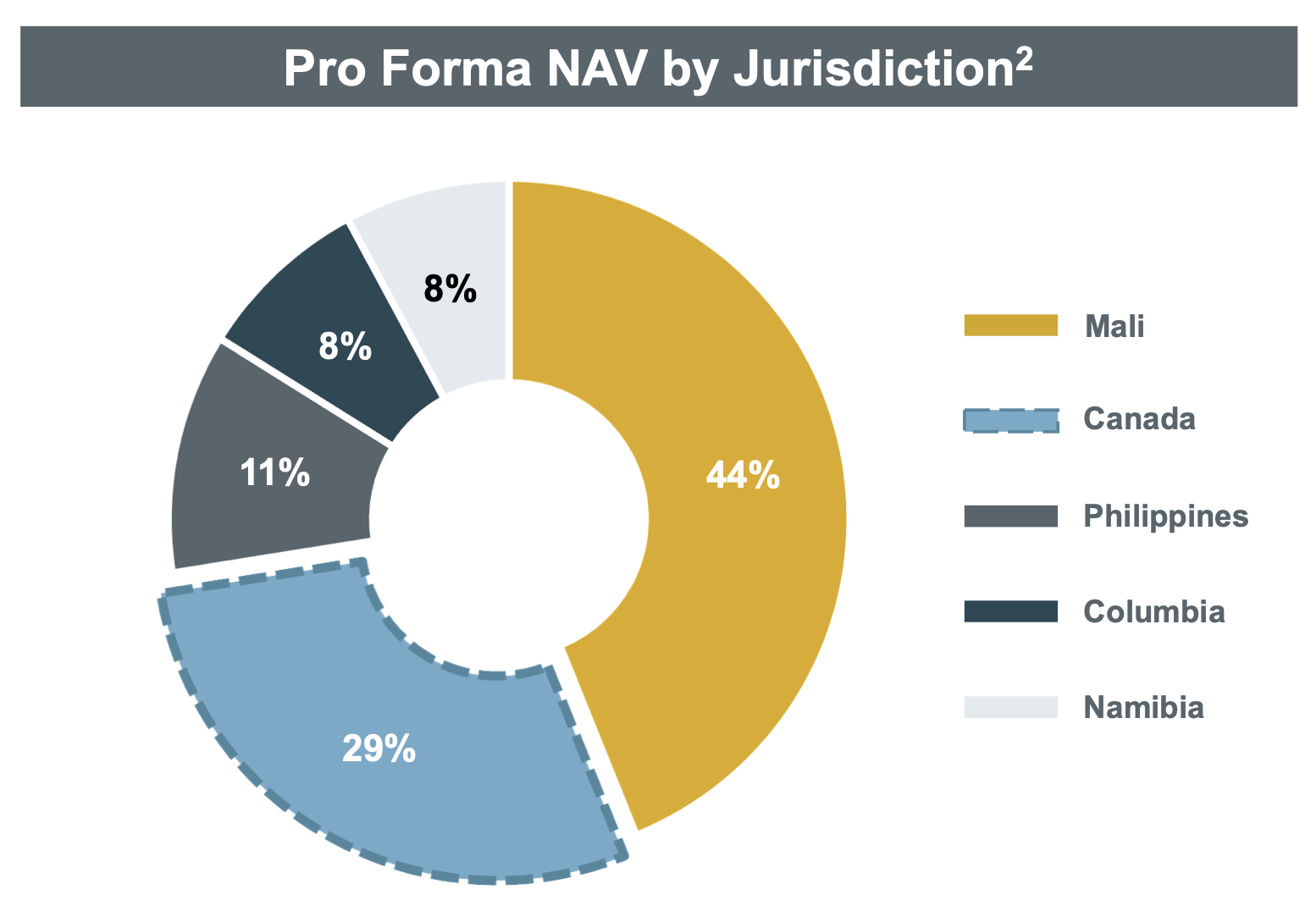

This means that Back River supports almost 60% of B2Gold's current valuation, and Fekola, Masbate, and Otjikoto - which are producing over 1 million ounces at a low cost - are only valued at ~US$1.5 billion. Fekola is still the workhorse and accounts for more of the NAV than any other asset in the portfolio. I would estimate that BTG is trading at 0.7-0.8x NAV, with the range based on how conservative or aggressive one is on Fekola's valuation. While that doesn't make B2Gold the cheapest gold producer in the sector, it's still undervalued and delivers consistent results for shareholders.

{kind=link}

I also want to highlight that BTG has declined 50% over the last three years while the price of gold has been flat. This divergence can't continue, especially with Back River now in the portfolio and more clarity on Mali.

There are additional regional risk (Philippines and Namibia), as it's not just Fekola that was a concern, but with Otjikoto becoming a smaller contributor to production in a few years, it's less of an impact.

I can't be 100% certain that BTG has bottomed. If gold moves lower, then I expect BTG will do the same. If gold at least remains stable, it's more than likely BTG will recover from current levels. If gold breaks out, then I would expect a sharp reversal higher in the stock. Either way, the risk that BTG will underperform is much lower today than it was ~6 weeks ago, or three years ago. I've been buying.

For further details see:

B2Gold: Oversold, Undervalued, And In Growth Mode Again