BTG - B2Gold: Sabina Deal To Materially Boost Reserve Inventory

2023-06-20 17:13:08 ET

Summary

- B2Gold has struggled to grow reserves per share in recent years, but recent acquisitions and exploration success should reverse this trend.

- In fact, the acquisition of Sabina Gold & Silver will result in a significant increase in B2Gold's reserve grade and total reserve base.

- That said, and although the stock is reasonably valued, the ideal buy zone for B2Gold is at $3.27 or lower.

It's been a mixed start to the year for the precious metals sector, with margins down year-over-year in Q1 combined with higher costs for planned capital expenditures, affecting free cash flow generation for most producers. Meanwhile, successfully replacing reserves was difficult, with most producers having to ratchet up cut-off grades at their mines because of inflationary pressures. In fact, less than 30% of the larger gold producers successfully replaced reserves in 2022 despite most increasing their gold price assumptions. One name in the group that has struggled to replace reserves in recent years has been B2Gold ( BTG ), with its total reserve base shrinking from ~7.4 million ounces at year-end 2019 to ~5.30 million ounces at year-end. However, this trend should reverse at year-end 2023, and we have seen a material increase in resources at its Fekola Complex. Let's look at the company's 2022 Reserve Report below:

{kind=link}

2022 Mineral Reserves & Resources

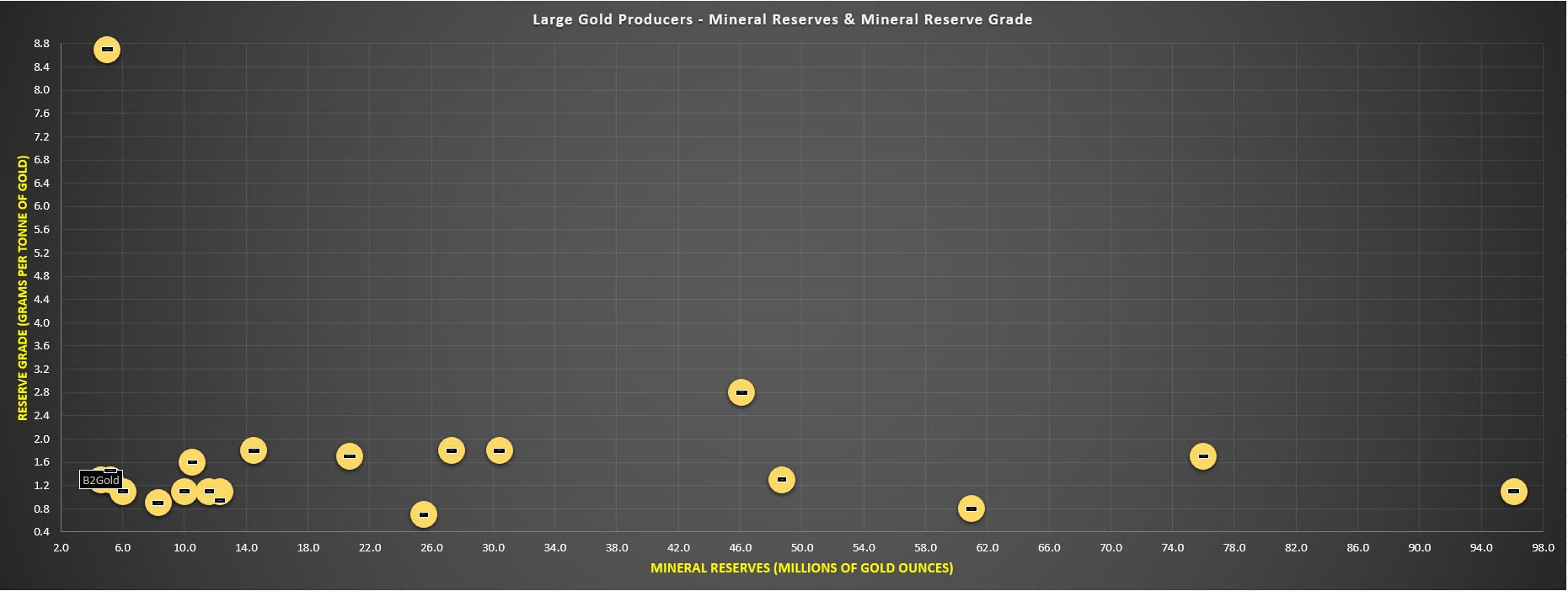

B2Gold released its year-end 2022 mineral reserve report, reporting total gold reserves of ~5.30 million ounces of gold, a ~15% decline from the ~6.22 million ounces of gold reserves reported in the year-ago period. This was one of the more significant declines in reserves sector-wide, and it continued a trend of overall declines in reserves since year-end 2019, when B2Gold's mines were home to a reserve base of ~7.42 million ounces. And while this is still a decent reserve base for any intermediate or senior gold producer, we can see that B2Gold was near the bottom of the pack from a total reserves standpoint as of last year, sitting among peers like OceanaGold ( OTCPK:OCANF ), Centamin ( OTCPK:CELTF ), and Lundin Gold ( OTCQX:LUGDF ), which are all much smaller producers.

Large Gold Producers - Mineral Reserves & Mineral Reserve Grade (Company Filings, Author's Chart)

{kind=link}

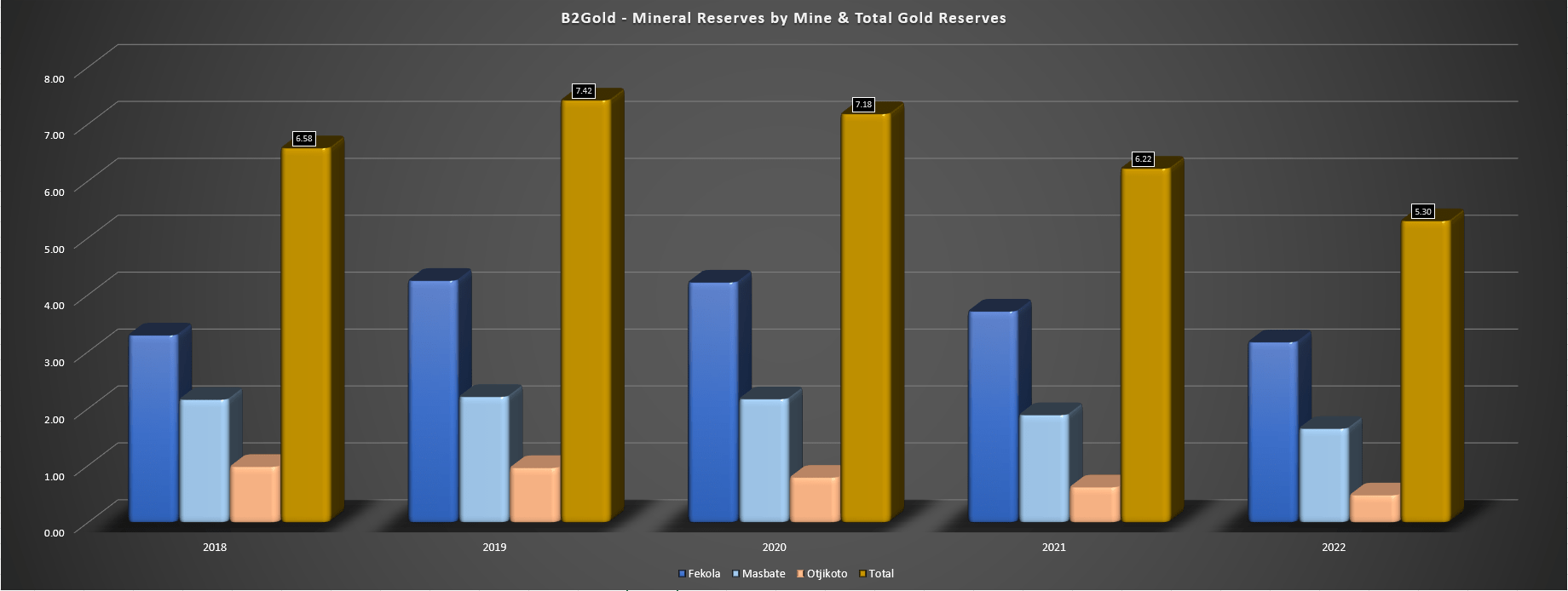

Besides the continued reserve declines among its asset base over the past few years, reserves have steadily declined at all three of its mines (Fekola, Otjikoto, Masbate), with the largest percentage decline at Otjikoto in Namibia (~480,000 ounces vs. ~960,000 ounces at year-end 2019). This has left Otjikoto with barely a three-year mine life with just ~8.0 million tonnes of ore remaining within reserves, even assuming a lower throughput rate over the remaining mine life vs. the 2021/2022 average processing rate of ~3.47 million tonnes per annum. That said, B2Gold has ~290,000 ounces at 4.25 grams per tonne of gold in the inferred category at Wolfshag Underground, continues to test regional targets and even if the asset is no longer in production post-2025, its production will be offset by output growth from the newly acquired Goose Project (~300,000 ounces per annum in the first five years).

The good news is that for B2Gold's flagship operation, Fekola, the mine is sitting on a reserve base of ~55 million tonnes, supporting eight years of mine life at an average throughput rate of 7.5 million tonnes per annum from Fekola Main (excluding material from Cardinal, Anaconda area saprolite material, or Fekola Underground). Plus, while Fekola's reserves have been in steady decline given the difficulty in replacing 500,000+ ounces per annum of mid-grade open-pit material, Fekola Complex resources continue to grow through exploration success and the recent acquisition of Oklo Resources. So, while one of B2Gold's three mines is getting lower on reserve inventory, Fekola and Masbate continue to have solid reserve bases, and the outlook for its Malian operating portfolio has never looked better, with the potential for two mills, multiple oxide/sulfide feed sources, and a total current resource base of ~9.4 million ounces of gold.

B2Gold - Mineral Reserves By Mine & Total Reserves (Company Filings, Author's Chart)

{kind=link}

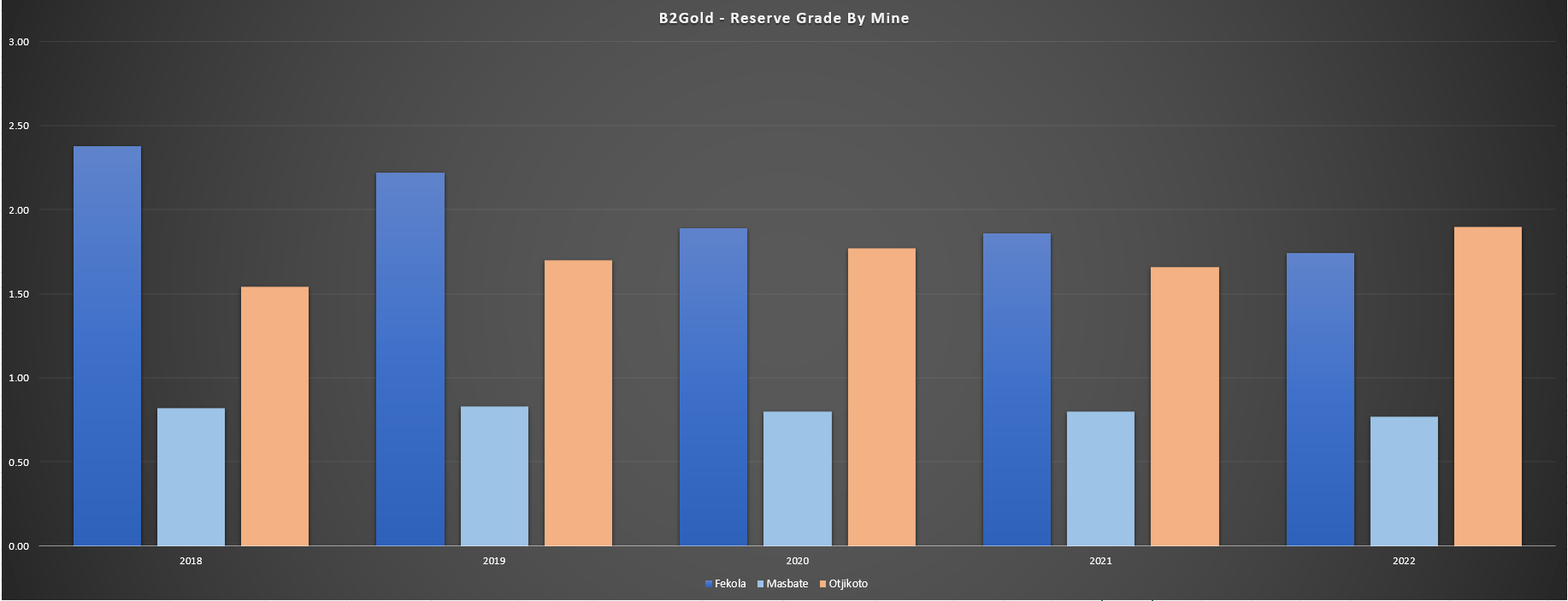

Finally, moving over to mineral reserve grades, we've seen a continuous decline in reserve grades, but this isn't surprising given that Fekola had a huge year in 2020 from a grade standpoint, with feed grades well above the reserve grade at 2.99 grams per tonne of gold, pulling a chunk of high-material from the Fekola reserve base. At other assets, Masbate's grades have declined slightly to 0.77 grams per tonne of gold, down from 0.82 grams per tonne of gold in 2018. Meanwhile, Otjikoto's grades have improved with the addition of high-grade ore from Wolfshag Underground, though as discussed earlier, the slight increase in grades has been offset by a sharp decline in tonnes. The result is that B2Gold's total reserve grade of ~1.27 grams per tonne of gold has slid well below the average reserve grade for larger producers (~1.80 grams per tonne of gold), as grades have continued to drop at Fekola.

B2Gold - Mineral Reserve Grade By Mine (Company Filings, Author's Chart)

{kind=link}

Overall, B2Gold's lack of reserve growth for a third consecutive year was not ideal, even if a significant resource base backs its reserve base up, with ~5.1 million ounces in the indicated category exclusive from reserves, even when excluding ounces likely for sale at Gramalote (Colombia). In addition, B2Gold has another ~4.0 million ounces in the inferred category across its operations, and while the Malian inferred ounces are lower grade, there is the potential for much of these to be moved into new mine plans assuming a stand-alone oxide plant is built later this decade north of the current Fekola Mine. Therefore, while I would normally be concerned with a smaller reserve base like this for a 1.0+ million ounce producer, B2Gold has done a solid job of adding ounces that will eventually make it into mine plans, and its recent takeover of Sabina will dramatically improve its reserves, to be highlighted later.

Reserve Growth Per Share & Relative To Peers

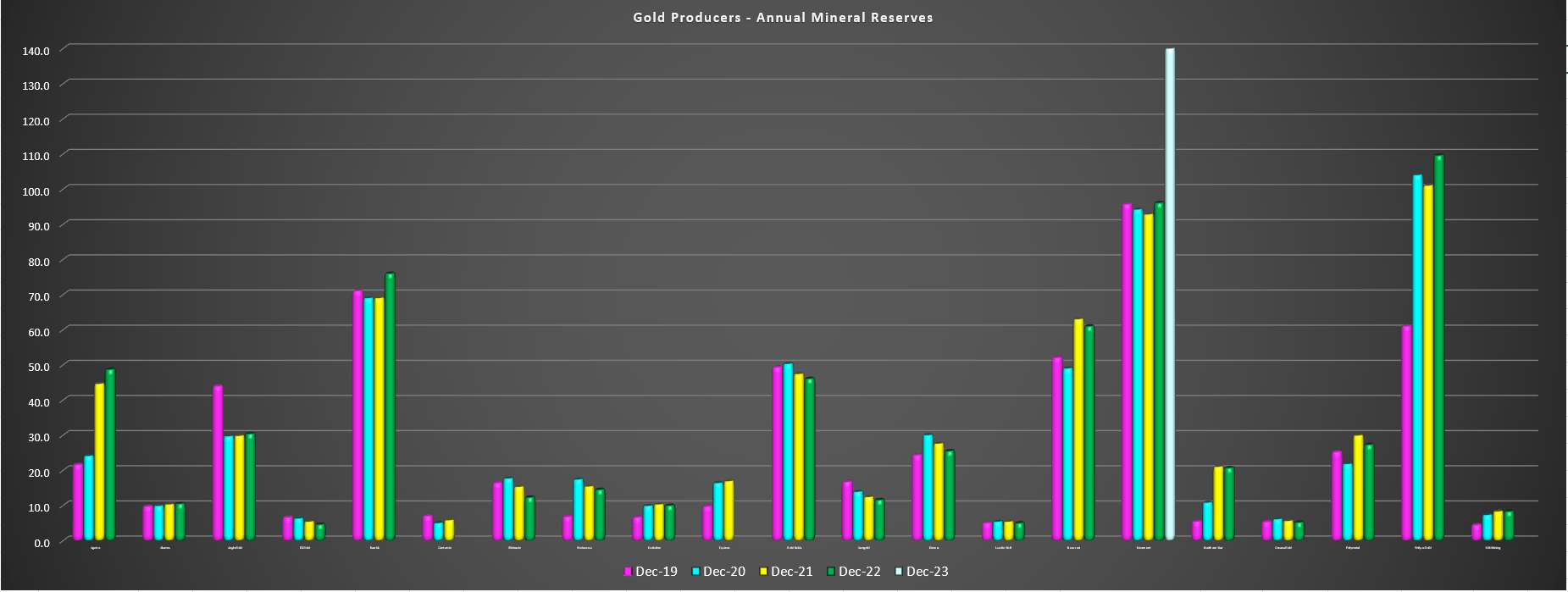

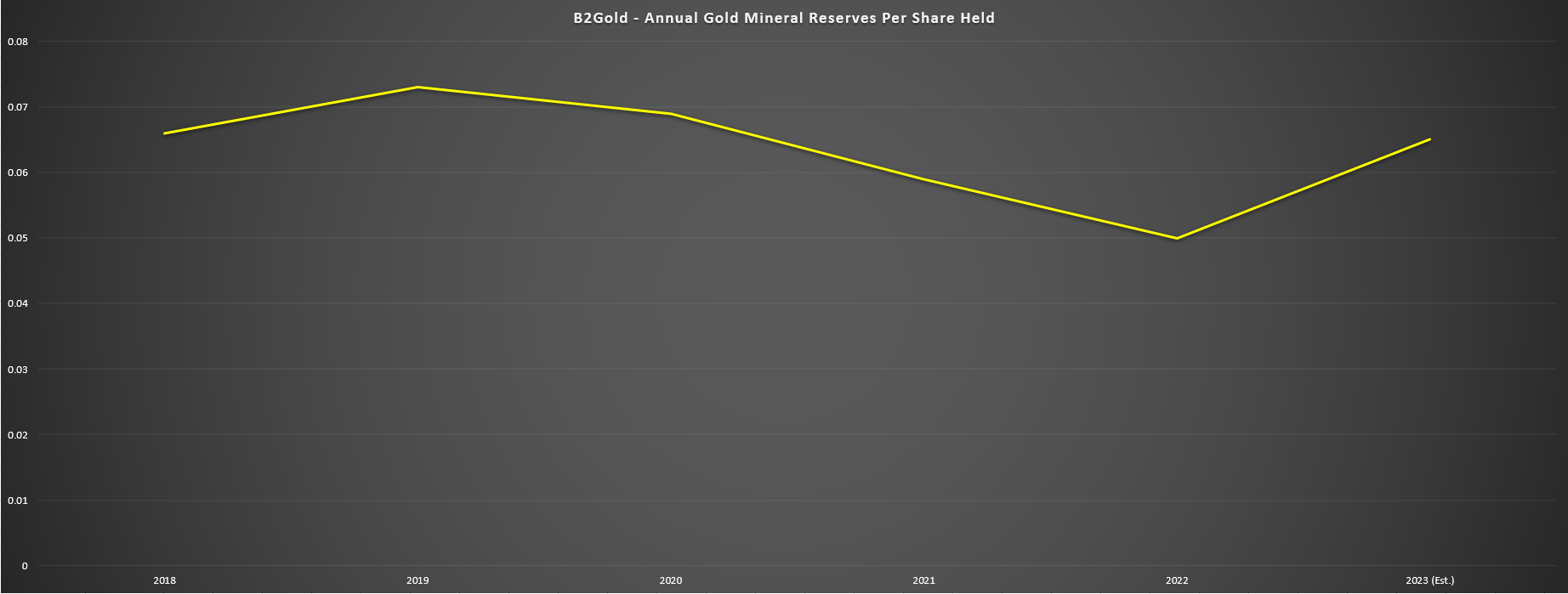

As for reserve growth relative to peers, B2Gold has seen total gold reserves decline for three years in a row, which isn't that surprising as we've seen a similar trend for most producers despite raising their metals price assumptions to an average of ~$1,400/oz gold (B2Gold's reserve price assumption is $1,500/oz). The exceptions to the rule are those companies that have merged or made large acquisitions, with B2Gold leaning on exploration success vs. M&A (until recently) to grow its resource and reserve base. That said, B2Gold has seen minimal growth in its share count during the period, resulting in a decent reserve per share trend relative to peers, and especially those like Coeur Mining ( CDE ) that have diluted at every imaginable opportunity. In fact, despite a steadily declining reserve base, B2Gold's reserves per share held have slid from ~0.067 to ~0.0050 from 2018 to 2022 despite divestments (Nicaraguan mines), which is better than the peer average.

Large Gold Producers - Annual Gold Mineral Reserves (Company Filings, Author's Chart)

{kind=link}

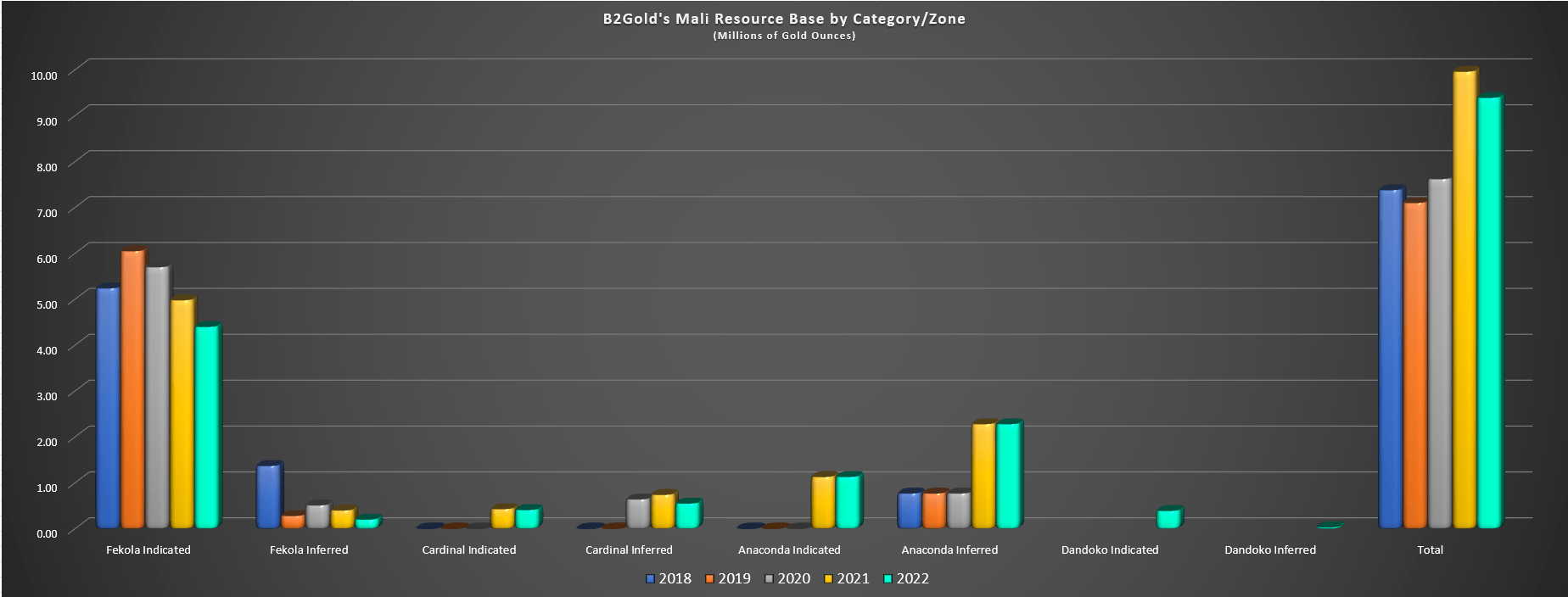

However, while reserves per share and total gold reserves have been declining since 2018, a couple of key developments will reverse this negative trend and also result in a higher quality reserve base. For starters, and as shown below, B2Gold's Malian resource base continues to grow, with total resources up from ~7.4 million ounces in 2018 to ~9.4 million ounces in 2022 despite a significant decline in ounces at Fekola Main (~2.0 million ounces). This is attributed to the declaration of mineral resources at the nearby Cardinal Zone (2022 resources: ~960,000 ounces), the addition of significant ounces at the Anaconda Area just north of Fekola (~3.41 million ounces), and the acquisition of new mid-grade ounces at Dandoko (~420,000 ounces). So, while Fekola Main might have a reserve base of barely 3.0 million ounces, the Fekola Complex is knocking on the door of a 10.0 million ounce resource base.

B2Gold's Malian Resource Base by Category/Zone (Company Filings, Author's Chart)

{kind=link}

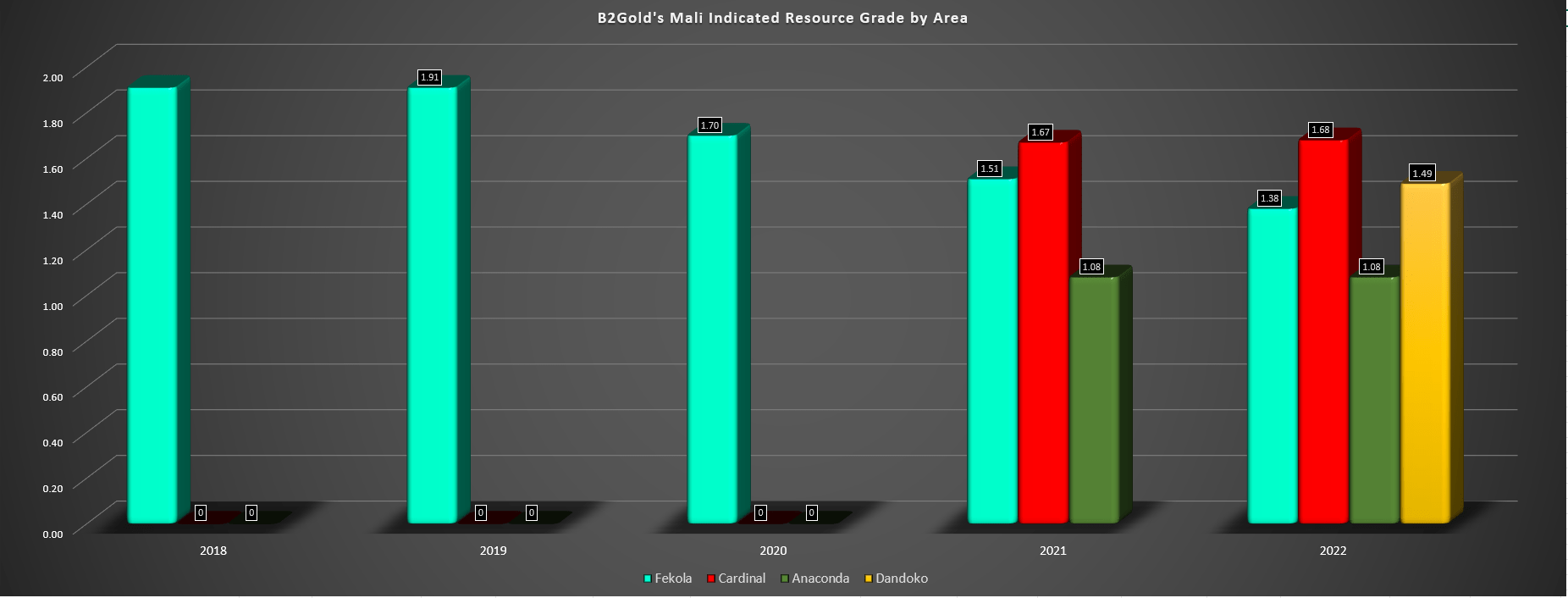

As the chart below highlights, the overall grades of these resources are quite respectable, with indicated resource grades of 1.68, 1.08, and 1.49 grams per tonne at Cardinal, Anaconda, and Dandoko, which is roughly in line with B2Gold's overall reserve grade of ~1.27 grams per tonne of gold if a portion of these resources can be converted to reserves in future years. So, while some companies have grown reserves through the addition of much lower grade resources which has diluted their overall reserve grade, this is not the case for B2Gold, which should be able to add reserves at similar grades at Anaconda, Dandoko, and Cardinal, and this will of course also benefit its reserve per share trend. However, the real driver of reserve growth will come from a new jurisdiction that B2Gold recently added with its acquisition of Sabina Gold & Silver.

B2Gold's Malian Indicated Resource Grade by Area (Company Filings, Author's Chart)

{kind=link}

As shown in the chart below, B2Gold's acquisition of Sabina will add ~3.60 million ounces of gold reserves at an average grade of ~6.0 grams per tonne of gold, which should result in a material increase in B2Gold's reserve grade to ~1.60 grams per tonne of gold. In addition, and even assuming ~400,000 ounces of depletion in 2023 from its current assets, this would push its total reserve base to ~8.5 million ounces of gold, translating to over 60% growth year-over-year in reserves. Finally, and arguably even more importantly from a valuation standpoint (potential for multiple expansion) is that a large portion of its reserve base (ounce standpoint, not tonnage standpoint) will come from a Tier-1 jurisdiction, which could allow the company to re-rate a little once Goose is in production vs. other solely Tier-3 jurisdiction producers that consistently trade at cash flow multiples below 7.0 and P/NAV multiples below 1.0 despite high quality assets.

{kind=link}

What's the result of the Sabina acquisition on total reserves and reserves per share?

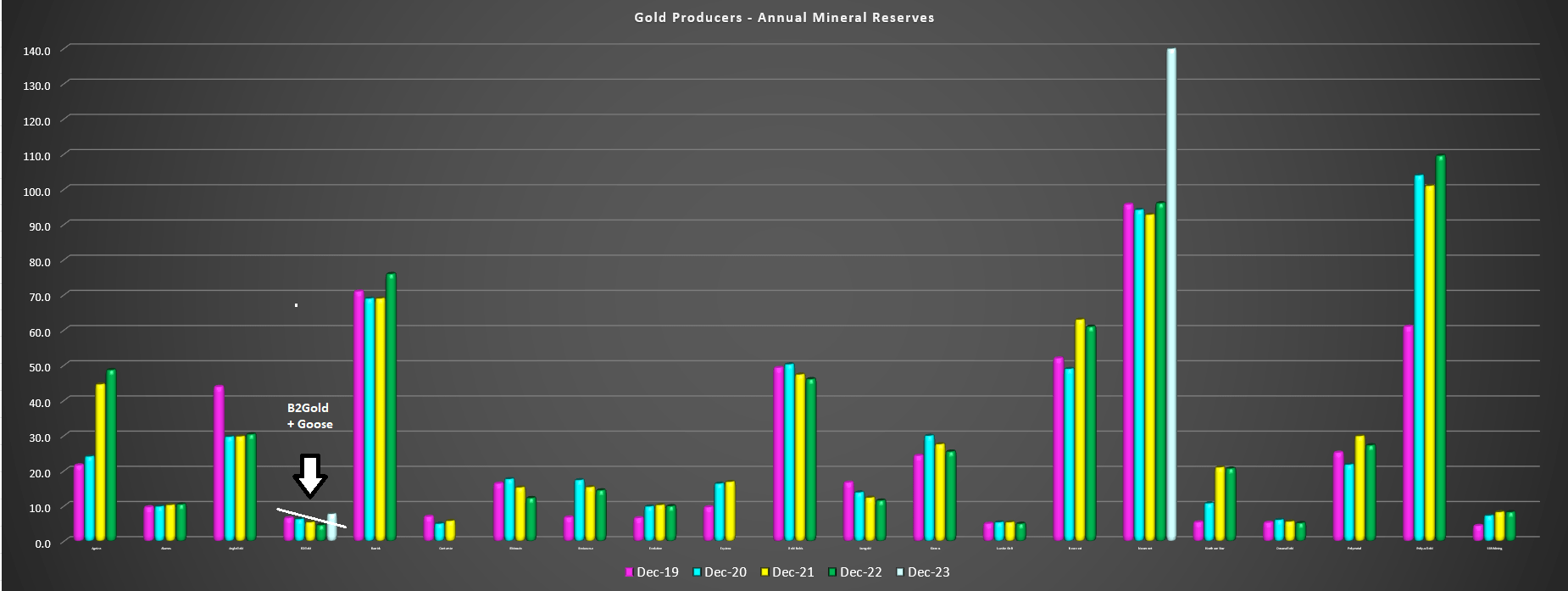

As shown below, B2Gold will reverse its trend of declining gold reserves (balanced by moderate share dilution), and it will see a major uptick in gold reserves per share even before any reserve growth from regional opportunities at the Fekola Complex. So, by B2Gold being opportunistic in its acquisition of Sabina and paying an attractive price after a blow-up in the stock, it will reverse several years of declines in reserves per share while increasing its reserve grade, adding considerable exploration upside with a massive land package in Nunavut, and also improving its overall margins given that Goose is a high-grade open-pit/underground asset. Therefore, I continue to see the Sabina deal as a brilliant move by the company, especially given the modest share dilution vs. other suitors that have paid a rich price to diversify, such as Fortuna Silver ( FSM ) and First Majestic ( AG ) in 2021.

Gold Producers - Attributable Annual Mineral Reserves vs. B2Gold with Goose (FY2023 Estimates) (Company Filings, Author's Chart & Estimates)

{kind=link}

B2Gold - Annual Mineral Reserves Per Share Held (Company Filings, Author's Chart & Estimates)

{kind=link}

Summary

While B2Gold has struggled to grow reserves per share over the past several years because of the difficulty in consistently replacing ~500,000 ounces per annum at Fekola Main, recent smaller acquisitions, exploration success on the northern end of the Fekola Complex and the larger acquisition of Sabina Gold & Silver should reverse this trend. And not only will this translate to a sharp reversal in its total reserve base that has slid 28% since year-end 2019, but we'll also see a reversal in the more important reserve per share metric. Plus, with a high probability of reserve growth outside of Fekola Main later this decade, this figure should continue to trend higher against a backdrop of minimal growth in its share count with major M&A out of the way. So, with a more diversified reserve base (addition of a Tier-1 jurisdiction in Nunavut), a higher reserve grade, and a return to reserve growth, B2Gold is finally catching up to million-ounce producer peers with larger reserve inventory.

{kind=link}

That said, and as highlighted in my previous update, the ideal time to buy B2Gold was below US$3.00 per share when I highlighted the stock as attractive in October, and while the stock is reasonably valued near US$3.70 and a market cap of ~$4.8 billion, I don't see enough margin of safety just yet. This is because the best time to buy B2Gold has been when it's traded below 5.5x cash flow, and it currently trades at ~6.0x cash flow, barely 10% below its 10-year average. Of course, the stock could head higher from here and waiting for lower prices could result in a missed opportunity, but I see the ideal buy zone for the stock coming in at US$3.27 or lower. So, while I see the upgrade to reserves and diversification as positive developments, I continue to focus on names trading at deeper discounts to fair value elsewhere in the market.

For further details see:

B2Gold: Sabina Deal To Materially Boost Reserve Inventory