BTG - B2Gold: The Market Has Yet To Be Convinced

2023-11-13 16:53:13 ET

Summary

- B2Gold's Q3 results showed underperformance at the Fekola mine in Mali.

- The Masbate mine in the Philippines performed well, exceeding gold production expectations.

- The company's focus on the Back River project in Nunavut presents high-risk, high-reward opportunities for investors.

B2Gold's ( BTG ) share price had been catching up with peers on the ground lost after Q2 earnings, and we were curious to see how the company would fare when it released Q3 results on November 8. And so we sat down and studied the latest data points contained in the company's filings, updated our charts, and listened to the earnings call.

The market shrugged, judging from the chart below, and continued to take a wait-and-see posture regarding this mid-tier gold miner with operating mines in Mali, the Philippines, and Namibia. We are taking a different view here, and see opportunity in the market's cautious approach, although not without risks.

Operations

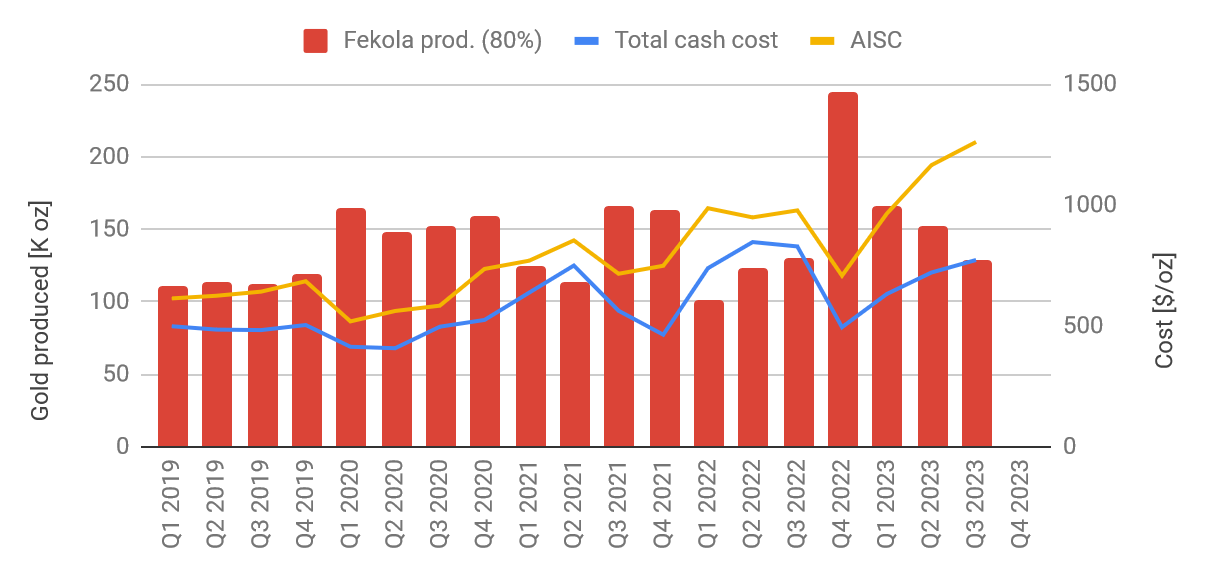

The Fekola mine in Mali under-performed (again) in Q3, and we submit this under-performance was most likely the cause for B2Gold's share price dipping after the earnings release. Quarterly production was reported 13,000 ounces short of budget thanks to the effects of a downpour that made the high-grade ore at the bottom of the Fekola pit inaccessible for some time during the quarter. Stockpiled ore was supplemented and the lower grade of this material has led to the disappointing data points for Q3 in the chart below. And as if this wasn't enough, the company also announced a delay in permitting the so-called Fekola regional ore sources as Mali transitions to a new mining code. The uncertainties surrounding this new permitting regime most likely added to market jitters regarding this flagship asset.

{kind=link}

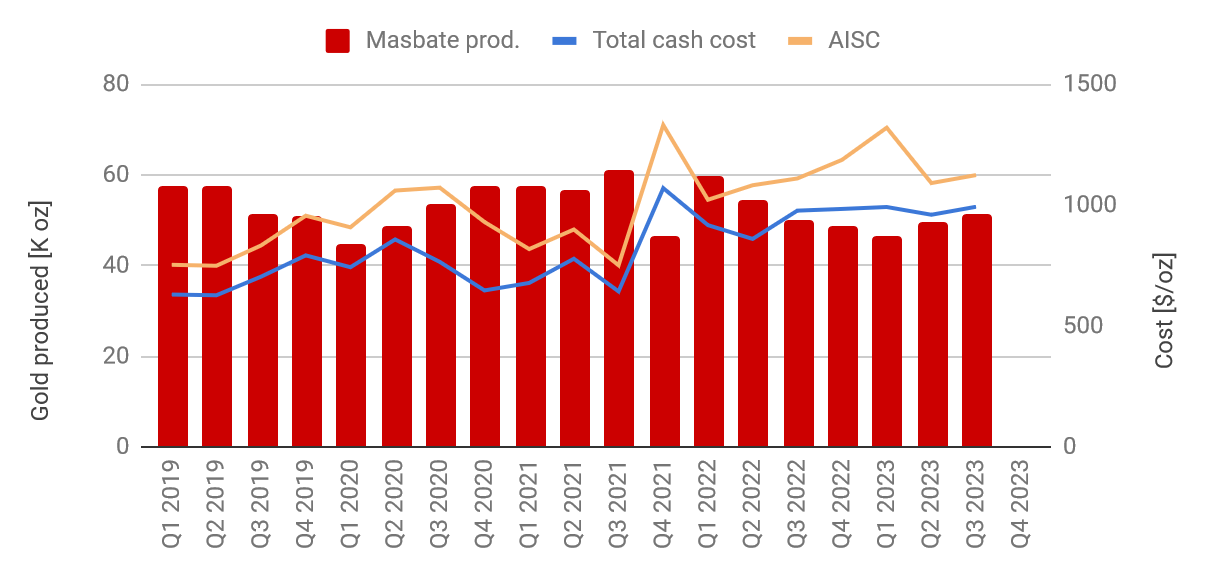

The Masbate mine in the Philippines turned in a strong Q3 showing, taking up some of the slack by logging gold production roughly 5,000 ounces ahead of budget. All-in sustaining costs seem to have stabilized at around $1,100/oz which we find quite remarkable for a low-grade low-recovery operation. B2Gold has managed the political risk better than other gold miners in the country, and the company seems ready to double down on its presence in the Philippines after establishing a new dedicated in-country exploration company.

{kind=link}

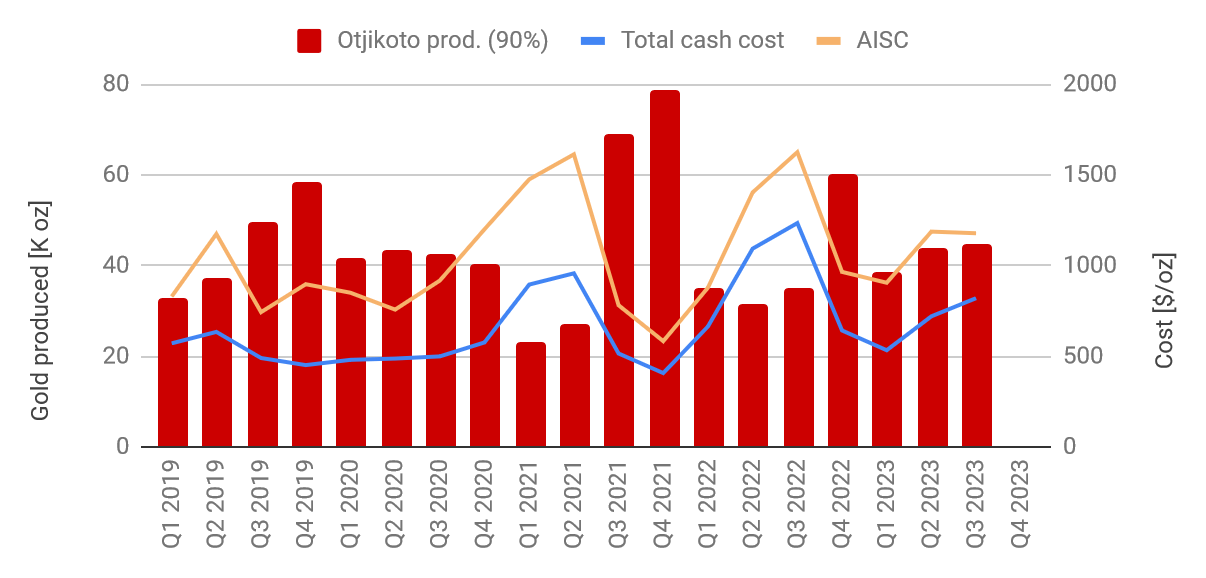

The Otjikoto mine delivered another robust quarter, thanks to ongoing contributions from the Wolfshag underground mine. This underground ore has a grade of 5.5g/t and represents a welcome boost to the much lower grades from the open pit. Operations in the pit are actually winding down and will terminate in 2025, followed by seven years of processing the lower-grade stockpiled ore. Wolfshag underground will remain in operation until 2026, or longer if exploration efforts bear fruit. The next couple of years will see additional costs from these transitions on the one hand, partially offset by the low handling cost of stockpile processing. We are looking forward to the upcoming guidance for some transparency on the future cost structure of this asset.

{kind=link}

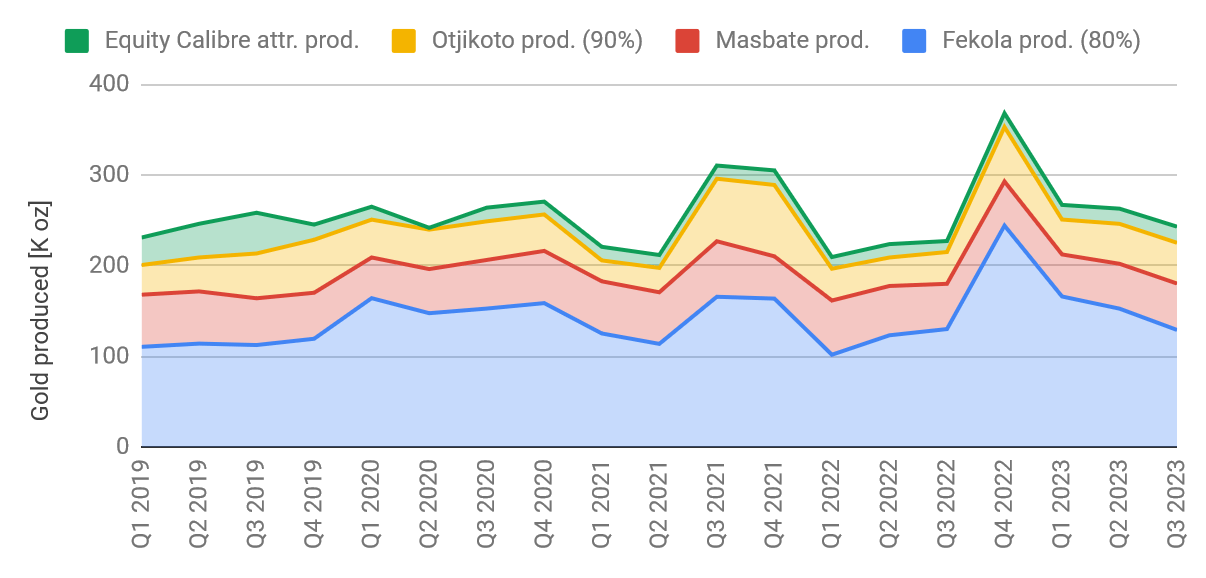

Consolidated gold production by mine is shown in the chart below, including the attributable production stemming from B2Gold's 24% equity stake in Calibre Mining ( CXBMF ). The dominant importance of the Fekola mine within this portfolio is obvious, and market jitters after a less-than-average quarter for the Malian asset are therefore understandable. B2Gold seems optimistic about achieving its production guidance for the year, which points to a very strong final quarter for the year.

Consolidated gold production (company's filings & author's work)

{kind=link}

Financial Results

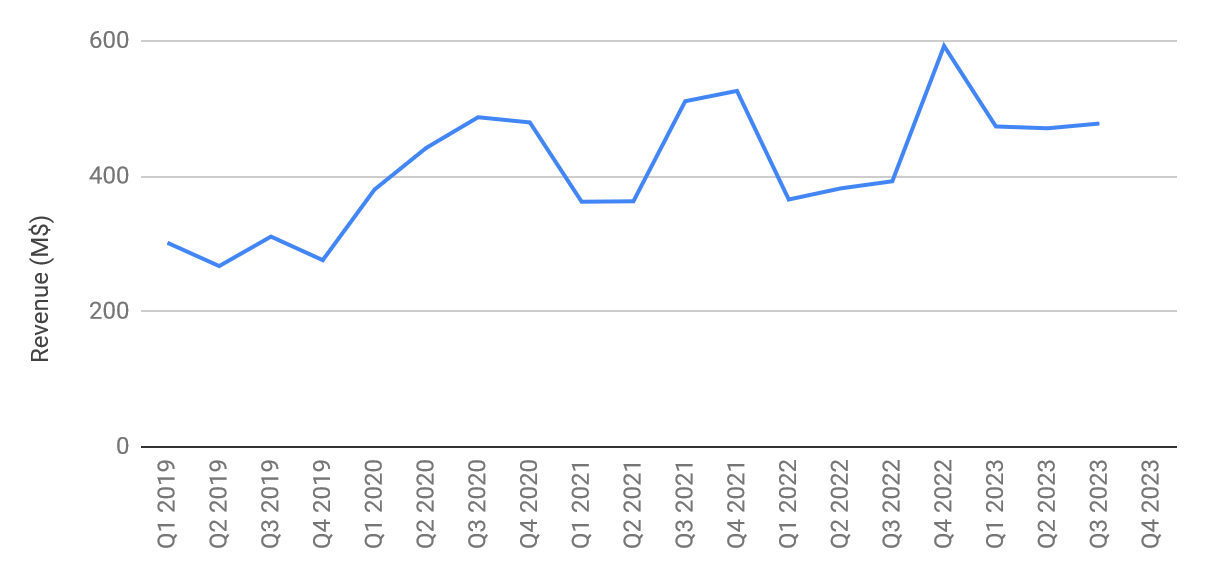

The strong gold price ensured a strong top-line result in Q3.

{kind=link}

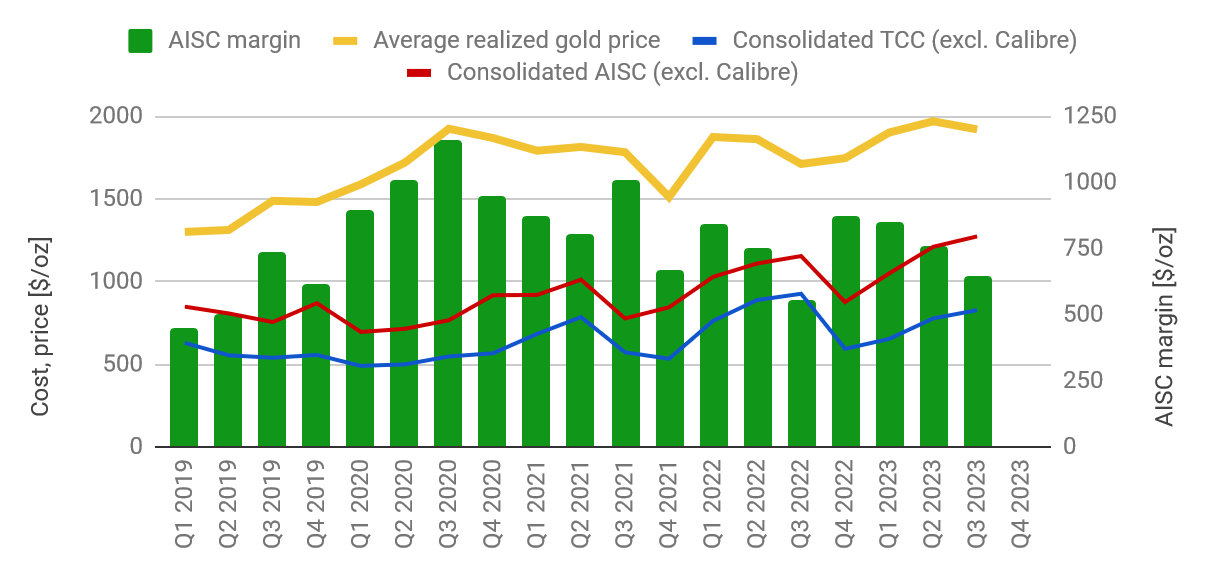

However, cost increases, especially at Fekola as discussed above, have continued to put pressure on margins for B2Gold (green bars in the chart below).

{kind=link}

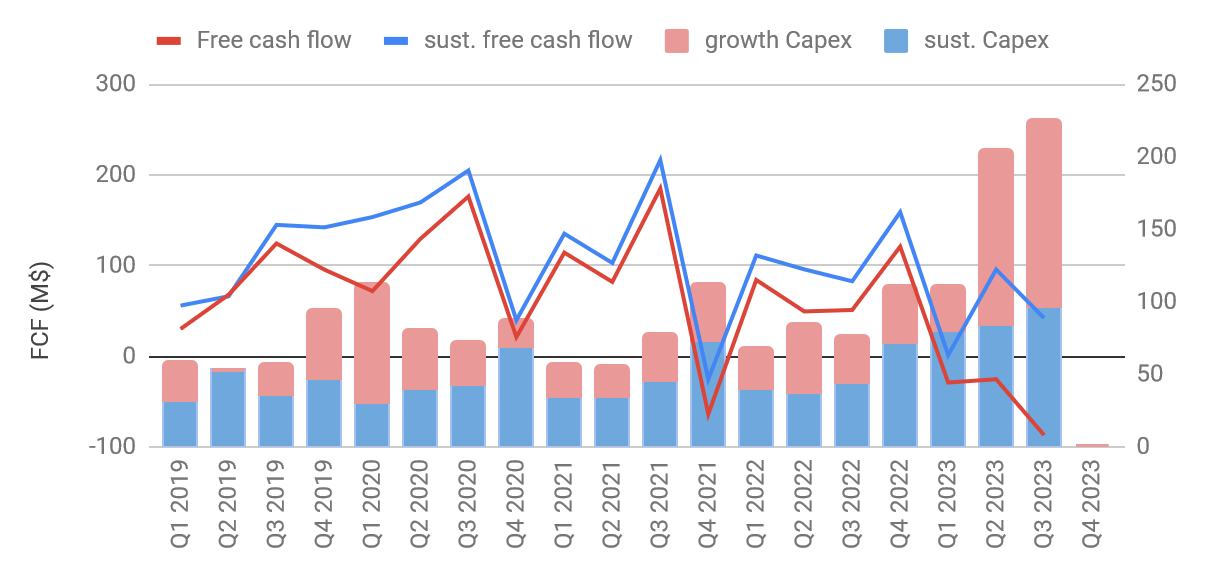

And shrinking margins, in combination with increased capital spending (sustaining capital as well as growth capital) has dented free cash flow generation. In Q3 free cash flow has turned negative, and sustaining free cash flow (after netting out growth capital) has only just remained in the black numbers. The bars in the chart below illustrate capex spending, and the lines show free cash flow generation (with and without growth capital consideration).

{kind=link}

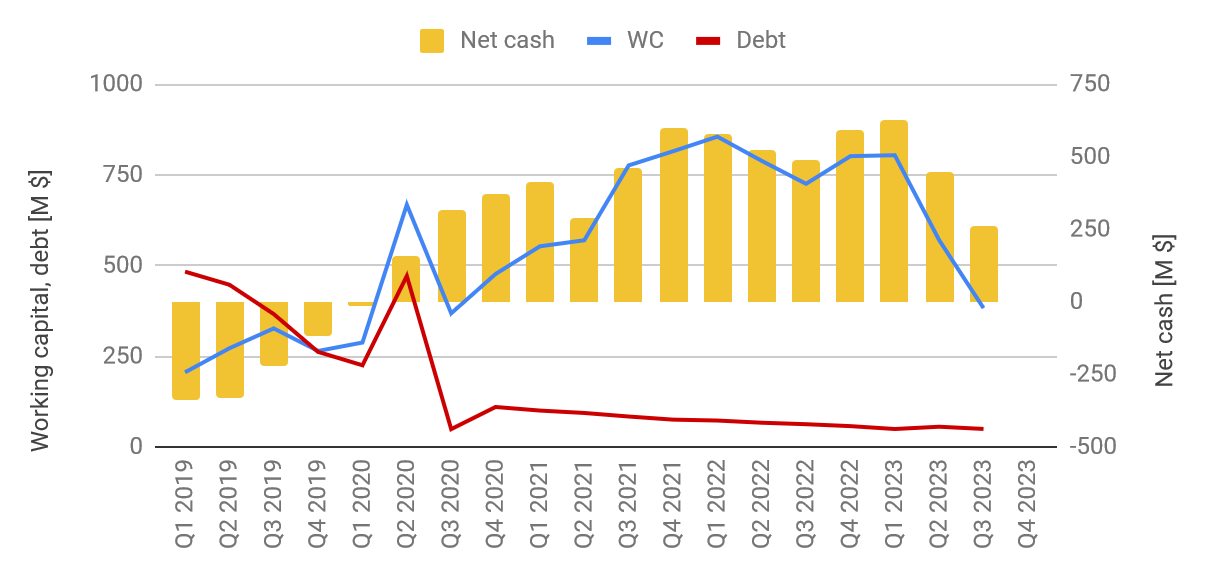

Fekola will see continued capital spending in coming quarters (provided that permitting for the regional ore sources can be completed), and spending at the Back River project in Nunavut will ramp up in 2024, so we are not expecting much free cash flow generation in 2024. B2Gold will leverage its strong balance sheet to fund these growth initiatives. This balance sheet carried negligible debt at the end of Q3; however, a first $50M draw post-quarter on the revolving facility was mentioned in the earnings call. This leaves $650M available on the company's debt facility -- sufficient fire power to see through B2Gold's capital projects barring unforeseen events.

{kind=link}

Back River Project

B2Gold is betting big on its newly acquired Back River project in Nunavut. The logistics of mine construction and material transport to the construction site were discussed at length and in great detail during the earnings call. This is a high-risk bet, and the TMAC Resources failure to bring the Hope Bay mine into sustainable production is still fresh in the minds of investors. So far, only Agnico Eagle ( AEM ) has succeeded to build and operate gold mines in the harsh and remote Nunavut environment, and this also came with a lengthy learning curve.

The B2Gold team has the advantage of experience with similar conditions from mines built in arctic Russia by its predecessor company. Nevertheless, building the Goose mine at the Back River project remains a daunting task. And when we mentioned a market stuck in a wait-and-see approach in our introduction, we had the capital project at the Back River project in mind first and foremost. Operations and cash flow are still important, but the company's valuation will be driven by success or failure in Nunavut for the foreseeable future.

Valuation & Investment Theory

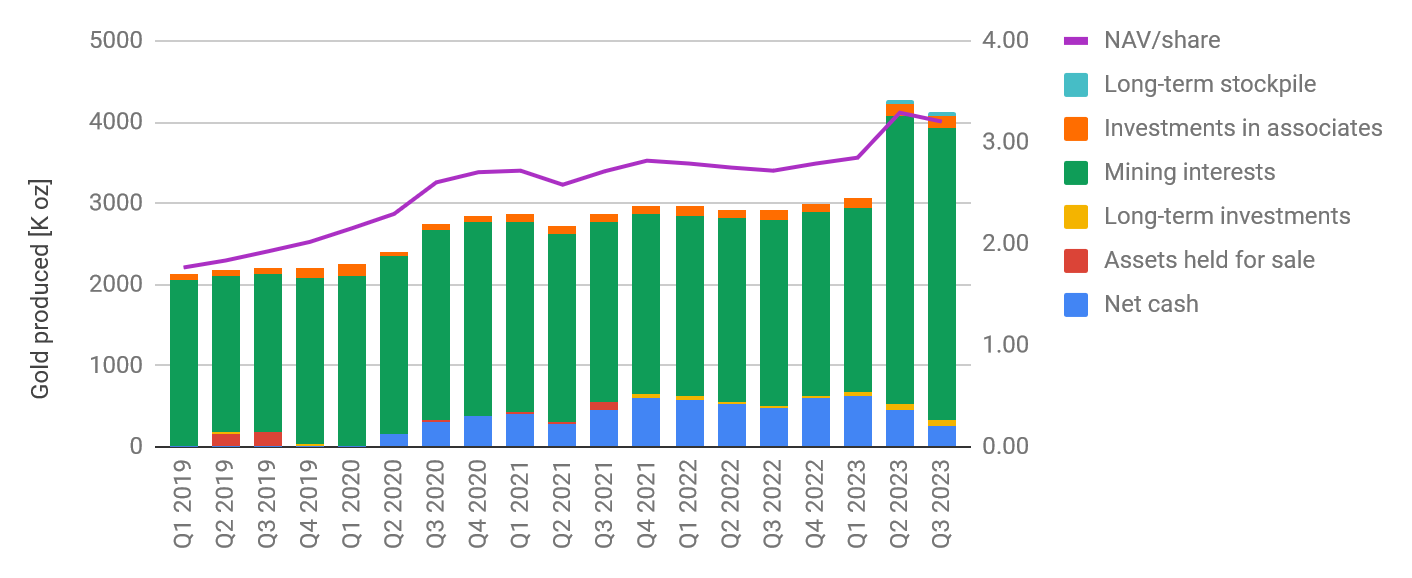

Consider the purple line in the chart below, illustrating Net Asset Value per share. The step up from Q1 to Q2 this year is caused by the addition of the Back River project, a highly accretive acquisition according to this chart.

{kind=link}

The market on the other hand seems to have focused on the risks associated with Back River and the share price has underperformed peers during the past 12 months.

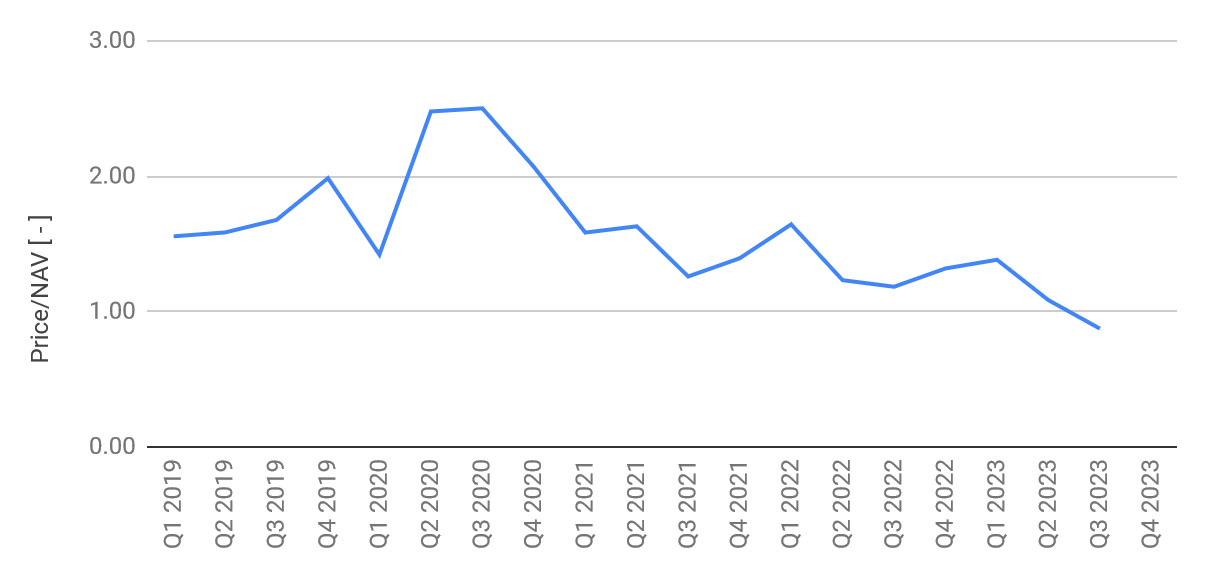

And this is where we see long-term opportunity, although as mentioned, not without risks. B2Gold used to trade consistently at NAV multiples of 1.3 or higher; but this multiple has shrunk to less than 0.9 as shown in the chart below. The market is clearly worried about risks mounting in B2Gold's portfolio: the development risks associated with the Back River mine build, but also the permitting risks at Fekola, and political risks in the Philippines. If these risks can be managed, and if the Back River mine can be brought into production by early 2025 as planned, then multiples should expand again. A return to the historic lower bound of 1.3 already offers a 50% upside from the current share price; and there is additional upside if we factor in the benefits of added production from the Back River project. A high risk/high reward opportunity in our view.

{kind=link}

B2Gold has been outstanding in managing the kind of risks that are currently mounting in the past. This is a management team that has successfully built several mines, has experience in arctic conditions, and has a convincing track record of dealing with country risk. Investors willing to trust B2Gold's continuing ability to manage these kind of risks should view the current situation as a buying opportunity; and investors with a low risk tolerance should probably look elsewhere.

For further details see:

B2Gold: The Market Has Yet To Be Convinced