BOLSY - B3 - Brasil Bolsa Balcao: A Good Defensive Stock Choice For The Long-Term

2023-07-16 00:37:15 ET

Summary

- B3, Brazil's stock exchange, has seen a rebound in shares due to anticipated interest rate cuts and decreasing inflation levels.

- The Brazilian company stands out with strong operational efficiency, profitability, and attractive dividend potential through share repurchases and payout guidance of about 125% this year.

- B3's valuation may not attract bargain seekers, but improving conditions and anticipated interest rate cuts indicate a positive medium to long-term outlook.

B3 S.A. - Brasil, Bolsa, Balcão ( OTCPK:BOLSY ) is Brazil's stock exchange that organizes and enables trading, post-trading, registration, and financing activities for vehicles and real estate. B3 is traded as an American Depositary Receipt (ADR), meaning its shares are traded in the United States through a depositary receipt issued by a U.S. depositary bank.

According to its business model, B3's revenues come mostly from trading fees charged on transactions carried out on the exchange and other fees for custody, listing, etc. Thus, B3's performance tends to have a very high correlation with the economy's growth and market temperature and is inversely correlated with Brazilian's basic interest rate (Selic).

Furthermore, the company demonstrates strong operational efficiency and has established itself as a monopoly in the Brazilian capital market. In recent years, it has consistently delivered high profitability and demonstrated a capacity for recurring returns by providing shareholders with attractive dividend payments.

However, the company's stock performance has suffered in the past couple of years due to high Brazilian interest rates and political uncertainties. This has resulted in a decline in the overall volume of initial public offerings (IPOs) and follow-on offerings.

Nevertheless, there is optimism as Brazil's anticipated interest rate cut and decreasing inflation levels have spurred a rapid rebound in B3 shares. The company has already capitalized on this favorable market movement, positioning itself for further growth.

Although a progressive slowdown in Brazilian interest rates in the coming years is imminent, is still a risk factor, but I believe the trend is likely to improve in the medium to long term. With that, I see good reasons for exposure in B3 as a defensive stock with the potential to pay good dividends in the long term.

Latest results

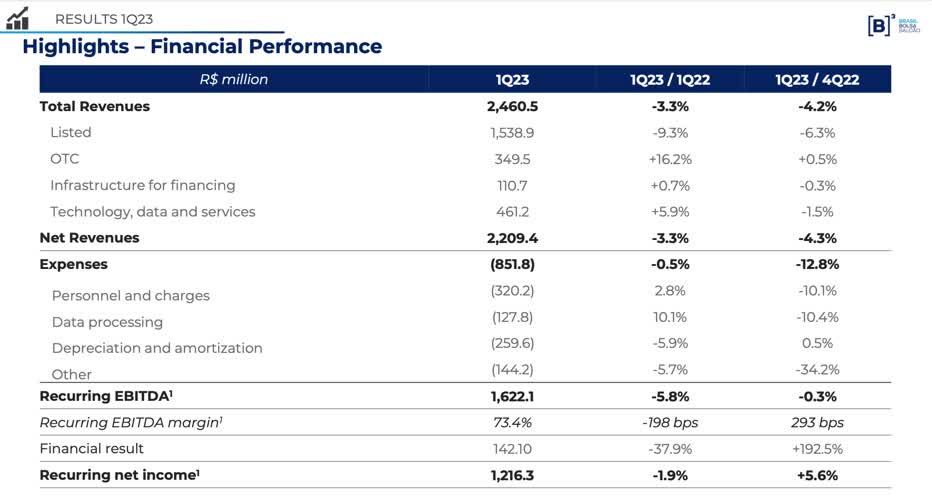

According to the most recent financial results , in the first quarter of 2023, B3 delivered unimpressive but predictable results considering the challenging macroeconomic scenario in Brazil.

The Brazilian company reported revenues of R$2.5 billion, representing an increase of 3.3% compared to last year. This result was mainly influenced by the decrease in revenue in the listed segment (equities and equities instruments), partially offset by the increase in revenue in the other segments.

{kind=link}

Breaking down the results by main segments:

- Listed Equities: The segment, which comprises 37% of B3's revenues, experienced an 18% YoY decline and a 14% QoQ decline due to lower trading volumes in the equities market.

- Listed Interest Rates, FX, and Commodities ((FICC)): Accounting for 25% of B3's revenues, this segment grew approximately 7% YoY and QoQ, totaling R$617 million in revenues. The growth was driven by positive performance in interest rates and FX derivatives.

- Technology Data and Services: The segment, representing around 19% of the company's revenues, experienced a 6% YoY growth but a 1% QoQ decline. The YoY increase can be attributed to adding clients and expanding the data and analytics line.

- Over-the-counter (OTC): This segment, accounting for 14% of B3's total revenues, reported a 16% YoY increase and a 1% QoQ increase, totaling R$350 million. The growth was driven by higher registrations of bank funding instruments, increased revenues from Treasury Direct, and a higher average inventory of corporate debt.

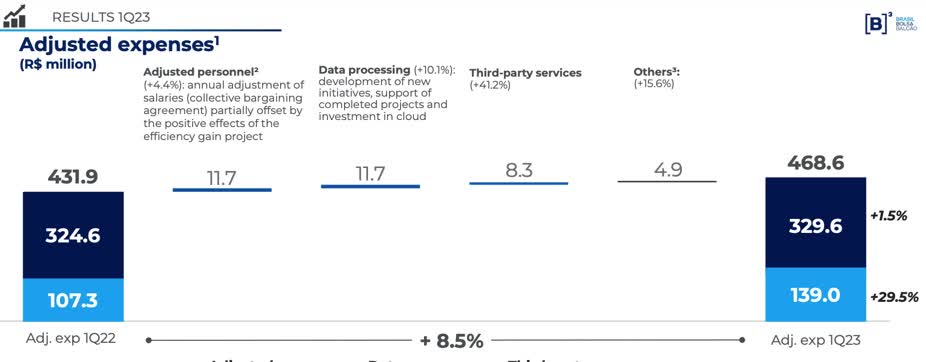

Analyzing the expenses, in the first quarter of 2023, they amounted to R$851.8 million, reflecting a 0.5% YoY decrease. Expenses related to personnel and charges increased by 2.8% due to wage increases, while data processing costs witnessed a 10.1% increase.

{kind=link}

B3, however, reported a positive financial result at R$142.1 million. However, there was a 37.9% drop compared to the same period of the previous year, mainly due to the increase in financial expenses caused by the higher CDI (Interbank Deposit Certificate) - commonly used as a benchmark for interest rates in Brazil, particularly for investments and loans.

The company's recurring EBITDA was R$1.6 billion, down 5.8%, and its EBITDA margin of 73.4% decreased 198 basis points. Net income for the first quarter of 2023 was R$1.1 billion, representing a decrease of 1.1% compared to the same period last year.

For second-quarter earnings, the company is expected to report more favorable results and increase its revenues by 8%. However, consensus forecasts EPS to fall by 10% for Q2, reflecting a more challenging environment affecting variable personnel and technology costs.

Dividends and buybacks

In my opinion, B3 represents a compelling opportunity as a potential income stock for the long run, given its diversified business model and strong operational efficiency. Despite boasting exceptionally high gross and net margins, currently at 87% and 40%, respectively, it is worth noting that the company's dividend distribution has not always followed a linear pattern in line with the cyclicality of the Brazilian macroeconomic scenario.

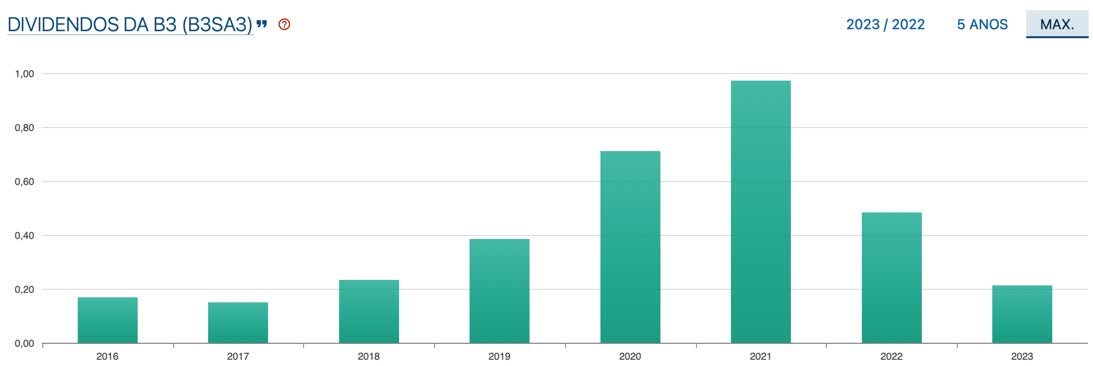

B3's dividend distribution. (Status Invest)

{kind=link}

However, B3 has consistently maintained a favorable historical payout ratio over the last ten years, averaging 86% and peaking at 134% in 2019. The company's guidance indicates an expected solid payout range of 110-140%.

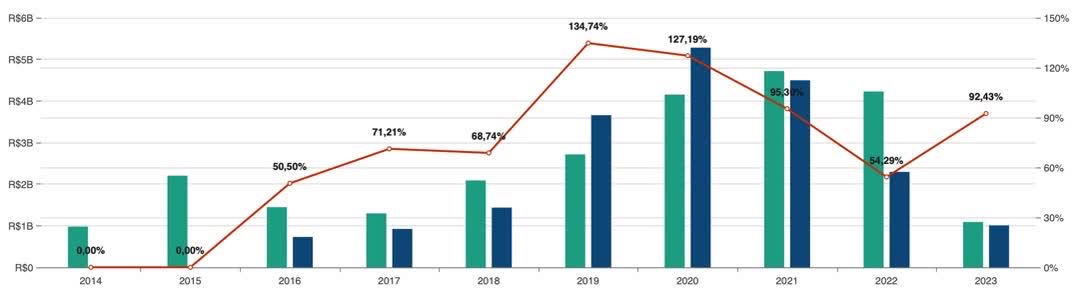

B3's payout (orange), net income (green), and dividends (blue). (Status Invest)

{kind=link}

In 2022, B3 generated about R$3.5 billion in cash and distributed R$2.28 billion in proceeds and about R$2.99 billion in buybacks related to last year's fiscal year. The trend continued in its first quarter of 2023 as it generated R$937 million in cash and distributed R$347 million in proceeds and $393 million in buybacks.

Despite the unimpressive dividend yield this year at an average of 3.7% and last year at 3.9%, this massive recent share buyback program by B3 should lead it to pay a higher yield.

B3 has reduced the total number of outstanding shares by buying its shares. Hence, the value of the total dividend distributed by the company remains relatively constant while the number of shares outstanding decreases. This increases the value of the dividend per share and, therefore, the dividend yield.

Consequently, it is expected that B3 will present a stronger dividend yield for 2023, remaining at approximately 4-5%. This yield may vary due to the number of share buybacks executed during the year. Furthermore, a progressive improvement is anticipated in the coming years as the downward trajectory of interest rates boosts B3's profitability. The consensus among analysts suggests a dividend yield in 2024 of around 6%.

Valuation and risks

From the start, it is essential to emphasize that B3's present valuation multiples are ill-suited for investors searching for discounted prices or bargain opportunities.

Currently, the company's shares trade at a price-to-earnings ratio of 22 times and a forward price-to-book ratio of 9 times, reflecting the market's high valuation of B3 due to its extensive competitive advantages. These advantages include the absence of competition in the Brazilian market and significant barriers to entry, particularly in terms of technology, operations, and regulatory compliance.

Since its share price approximately three months ago, B3 shares have experienced a remarkable rally of over 60%. This significant surge has resulted in a more stretched valuation, rendering it an even pricier stock. Consequently, there may be potential short to medium-term pressure for investors entering at current levels.

Considering the stretched current P/E multiple, a closer analysis of B3's earnings over the past five years reveals an intriguing correlation with Brazil's Real interest rates. These rates, which reflect the nominal interest rate minus the inflation rate, are inverse-correlated with the company's profitability growth trends in the past few years.

The prevailing basic interest rate in Brazil ( Selic ) at 13.75% since September of last year has had a detrimental effect on B3's trading volume. Moreover, the uncertainty stemming from the projection of prolonged high-interest rates brings unfavorable prospects for the Brazilian capital market, potentially impacting the company's operations with decreased IPO activity and reduced traded volumes.

The Brazilian Central Bank projects that the Selic rate will remain at 12.25% until the end of the year and at 9.5% in 2024, still considered high levels, especially when compared to the 2% Brazilian interest rate registered in 2020.

Therefore, B3's stretched valuations may be uncomfortable for bargain-hunters considering the macroeconomic risks affecting the company's earnings generation growth.

The bottom line

B3 emerges as an excellent choice for long-term investors seeking a defensive stock expected to grow over the years as the Brazilian capital market develops.

As Brazil's primary stock exchange, B3 holds a monopoly position and capitalizes on a diversified business model and strong operational efficiency. This combination results in substantial profitability and the potential for an attractive dividend yield, further bolstered by B3's capital allocation strategy of ongoing share repurchases and an anticipated average payout of 125%. B3's appeal is further enhanced.

While B3 has faced challenges stemming from high-interest slowing down its revenue growth, the upcoming prospects of interest rate cuts coupled with improving economic conditions suggest a more favorable outlook over the medium to long term. Although the current valuation of B3 after a massive rally may not present a bargaining opportunity, considering an investment in B3 looking for the long-term during a high-interest rate downturn could be opportune.

For further details see:

B3 - Brasil, Bolsa, Balcao: A Good Defensive Stock Choice For The Long-Term