BWSN - Babcock & Wilcox: Why This Old-Economy 'Falling Knife' Could Finally Turn Around

2023-12-11 12:43:42 ET

Summary

- Babcock & Wilcox has taken a heavy beating in the market over the past year.

- Management is taking action to reverse the situation.

- With management actions, a very depressed share price, and quantitative factors signaling a recovery, I'm rating BW a Buy.

Investment thesis

Babcock & Wilcox Enterprises, Inc. (BW) is down ~67 % in the past year as of writing this analysis. It's a historic enterprise that was instrumental in creating the first safe water-tube boiler for naval propulsion and other purposes. It produced boilers for the US Navy during World War II, and even supplied the Manhattan Project developing the first nuclear bomb of the US.

BW is an interesting stock as opinions on it vary quite a lot these days, as illustrated by the ratings on Seeking Alpha - with ratings ranging from Strong Buy to Strong Sell:

Seeking Alpha

In this analysis, I examine the reasons for BW's poor price performance, and I take a closer look at some quantitative factors that could suggest future outperformance. I also assess qualitative factors - mostly management actions - that could support the outperformance that the quantitative factors point to.

Based on my findings outlined below, I'm issuing a Buy rating for BW.

What caused the drop

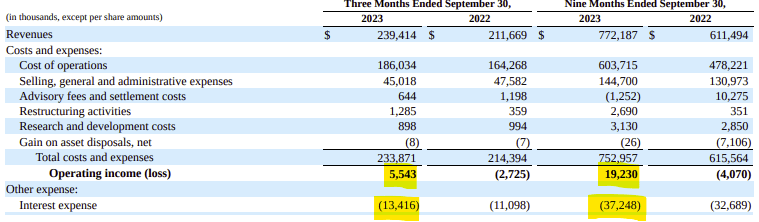

Much of BW's laggard price performance comes from a single-day drop of more than 50% in early November 2023, although the stock had been sliding for a while before then. The November drop came following BW's Q3 report in which it presented shareholders with a loss due to writedowns . The net loss in Q3 of ~$120 million is close to the size of the market capitalization of the entire company.

Before this recent drop, BW experienced a sharp decline in the fall of 2022, some of which is seemingly attributed to BW having lowered its EBITDA outlook amid macroeconomic headwinds . These headwinds included delayed accounting recognition of some of its projects, and issues pertaining to the war in Ukraine, including supply chain constraints.

Further, over the years, BW has transitioned its business to primarily focus on the clean energy transition. This change has also seen the company needing to re-focus its operations on the natural "structural damage" that can cause along the way.

Quantitative signals suggesting upcoming outperformance

BW trades at an enterprise value to revenue (EV/R) ratio of ~0.5. This ratio expresses the relationship between what a buyer for control would have to pay to have full control over the assets (enterprise value) and the revenue. Trading at less than a ratio of 1 is remarkably low. To me, this signals an opportunity.

Further, BW is a small cap company (market cap ~$150 million). On a statistical level, I believe small caps are more likely to trade at overly depressed levels, including at very low EV/R ratios like BW is.

As was reported on Seeking Alpha in November, BW's CFO, Louis Salamone, bought 50,000 shares of common stock in November. I always like to see insider buying as it points to undervaluation, and several studies have shown that as a group, stocks with insider buying tend to outperform.

Together, these signals - a low EV/R ratio coupled with small cap status and insider buying - point to a buying opportunity on a quantitative level in my view.

Qualitative actions taken by management

Management recently took steps toward realigning BW's business. Going forward, the company aims to focus on the higher margin aftermarket business. The aim of this is to achieve more steady cash flows and improve the balance sheet which has seen debt piling up in recent years.

Further, management has outlined a strategy to realize up to $30 million in annual cost cuts primarily through overhead cost reductions related to newbuild projects.

BW also intends to sell its solar business unit . This was the reason BW reported a substantial impairment charge against the earnings as it reported a $50 million+ loss, and also booked nearly $48 million in contract losses related to the solar business unit.

Risks

BW has a clear vision for the future: They want to help drive the renewable energy transition, and their service portfolio is aligned with that ambition.

BW has to navigate its ambition with a ton of debt, though. BW's long-term debt stands at ~$372 million. This compares to its cash on hand at ~$48 million and free cash flow for the TTM of -$28.5 million. The free cash flow of BW has been in the negative for several years, underpinning the leverage concerns.

Interest expenses are rising, and current interest expenses are high enough to turn an otherwise positive operating income into a loss when accounting for interest expenses (and other items):

Babcock & Wilcox most recent SEC filing

{kind=link}

It doesn't take a business or accounting course to see where this is going: BW needs to manage its debt stringently going forward and will need to eventually reverse the negative course of debt levels, interest expenses, and free cash flows. Otherwise, BW would probably need to restructure or liquidate more business units going forward.

Going forward, we'll have to see if management initiatives - including cost reductions and divestitures - will be sufficient to reverse the course.

Key takeaways

Babcock & Wilcox is an old-school industrial company that has played an important role in naval history, particularly that of the 20th century. In this century, however, innovations have seen the company's role shrink, and recent years in particular have been tough to navigate. BW has responded by transitioning its business to one focused on supporting renewable energy projects.

The challenges have seen BW perform very poorly on the stock exchange. Shares are down almost 70% in the past year.

Some quantitative factors point to future outperformance, though. I see these being mainly low valuations (including EV/R), its small cap status, and insider buying.

Qualitative factors supporting this thesis include a cost reduction program, divestitures, a focus on operations within clean energy, and a focus on stabilizing the balance sheet.

I see the main risks associated with buying BW being that of its debt. BW has managed to stabilize its operating performance with positive operating income for 2023 (9 months) as against a loss in 2022 (9 comparable months). But interest expenses take a toll on bottom line results, and impairments haven't made it any prettier. Companies don't go bankrupt from non-cash impairments. But the interest expenses are a real concern.

I think the risks involved with BW should be managed by owning BW not as an individual issue but as one in a portfolio of stocks like it: Shares with low valuations and recent substantial market price drops. I believe this portfolio should contain perhaps 20-30 such issues.

For further details see:

Babcock & Wilcox: Why This Old-Economy 'Falling Knife' Could Finally Turn Around