TSM - Back To The Future 5.0 Post-Earnings Review

2023-09-19 12:08:01 ET

Summary

- We end each quarter inspecting our work within both the semi and software/hardware spaces, dissecting our best calls and where we could’ve done better.

- This quarter marked a turning point for investor confidence in the A.I. boom; we’ve seen earnings under investor scrutiny this quarter regarding management comments on A.I. growth potential.

- China’s been a big theme this quarter, with the slower economic recovery weighing on the semi industry alongside some of its biggest customers, namely Apple.

- The current market is being driven more by macro data than fundamentals.

- We see a more volatile back end of the year, and as we operate in a forward-looking market, we hereon lay out our predictions for what’s to come.

This quarter kicked off with semi-cap earnings from ASML Holding N.V. (ASML), signaling stronger demand from Chinese customers for DUV tools but slower EUV growth - highlighting straight off the bat that the A.I. boom did not materialize into the near-term mega tailwinds investors had hoped for. Earnings results from Taiwan Semiconductor Manufacturing Company Limited ( TSM ) followed, confirming that the A.I.-related demand would not materially boost revenues while the industry still faces demand weakness in core end markets (smartphones, PCs, IoT, among others). To top it off, earnings from the software/hardware industry reflected a persisting cost-cautious environment weighing on revenues despite efforts across the board to integrate A.I. and paint it as a near-term growth catalyst.

The S&P 500 (SP500) rose 10% in June and July, celebrating an expectation of a bull market, an end of the Fed interest rate hikes, and easing inflation - of course, the celebration was misplaced. The bull market is not here yet, in our opinion - over the past month, the S&P 500 is up slightly by 2%, Nasdaq Inc. (COMP.IND) is down 2%, and the Dow Jones Industrial Average (DJI) is flat, not to mention the pullback across the semi industry. The following graph outlines key semi-stocks' performance over the past three months.

YCharts

We think this quarter signaled a turning point for investor confidence in the A.I. boom. While 1H23 exhibited an A.I.-driven rally across Nvidia (NVDA), Advanced Micro Devices (AMD), Marvell (MRVL), and Broadcom (AVGO), among others, this quarter's earnings results have been a stark comparison between what investors expected and the reality. We operate in the business of educated predictions; hence, looking forward, we see a more volatile back end of the year and think macro headwinds may spill into 1H24. Nevertheless, we see several names better positioned to outperform and through which investors can weather the macro backdrop: NVDA, Meta Platforms ( META ), Intel ( INTC ), and Uber ( UBER ), to name a few.

Special Takeaway From 3Q23

China was a bright spot at the beginning of the quarter, but this has quickly reversed to a negative spot. The semi-cap, ASML, Lam Research (LRCX), and Applied Materials ( AMAT) all highlighted stronger demand from Chinese customers this quarter. We argued early on that the demand was not a sign of true demand recovery but, instead, panic buying driven by fear over the Biden administration's export ban. At this month's investor conferences, we've seen management across the board confirm demand weakness from Chinese customers due to the slower economic recovery. We expect the semi-cap to see double-ordering triggered by panic buying into the next quarter.

Matters intensified further after Huawei launched its Mate 60 Pro smartphone with 7nm chips from SMIC; the 7nm Chinese smartphone demonstrated that even with the ban, China has the capabilities to manufacture advanced tech - the scale of which remains unclear. If the U.S. and Taiwan lose their share in domestic China, we think we'll see problems with production and a negative impact on the semis overall.

Best Calls - Review & Preview

Equally important to recognize where A.I. will drive material revenue growth is recognizing where or when it won't. Some of our best calls this quarter have been driven by this sentiment.

1. MRVL, AVGO & AMD

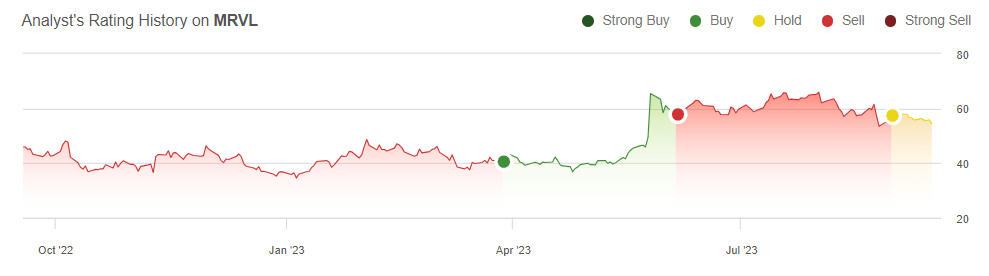

MRVL and AVGO were two of the best-performing semi stocks in 1H23 on the back of A.I. hype, as was AMD. This quarter, all three companies' A.I. growth "house of cards" narrative fell through. We upgraded MRVL to a hold from a sell in late August after July quarter earnings, and the October outlook confirmed our negative thesis of A.I.-related growth being unable to drive financial performance in the near-term. The following outlines our rating history on the stock.

{kind=link}

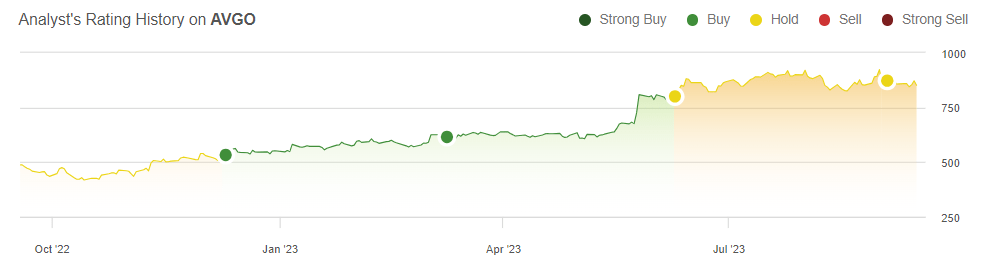

A similar situation played out with AVGO; we downgraded the stock to a hold in early June, expecting growth to moderate into 1H24 due to inventory correction cycles, weaker capex spending, and investor overconfidence in AVGO's A.I.-related revenue growth. Management predicted AI-related sales doubling this year and accounting for +25% of semiconductor revenue in FY24, feeding market noise into A.I. growth exposure. We saw our negative thesis confirmed by management at investor conferences this quarter; management is now talking about a soft landing in its business and guided conservatively for its October quarter. We think both AVGO and MRVL emphasize the unique risk investors face in 2023 by feeding into the attractive A.I. growth narrative without taking into account the demand weakness in other segments; in the case of AVGO, weaker demand for traditional cloud compute and enterprise and communications service providers' inventory correction, and in the case of MRVL continued demand weakness in enterprise and carrier markets. The following outlines our rating history on AVGO.

{kind=link}

AMD is at the heart of the A.I. discussion despite being a distant second place to NVDA in the A.I. accelerator market. We think the market has woken up to the reality that AMD won't be the next NVDA. We think the Wall Street expectations for AMD's A.I. revenue are too high and see outperformance moderating substantially in the second half of the year. AMD's AI GPU offerings lag behind NVDA in a material way. Additionally, we believe the market is overlooking the higher risk profile for AMD's data center CPU business as the industry spending shifts more wallet-share focus to A.I. over traditional compute under a limited cloud capex.

2. AAPL

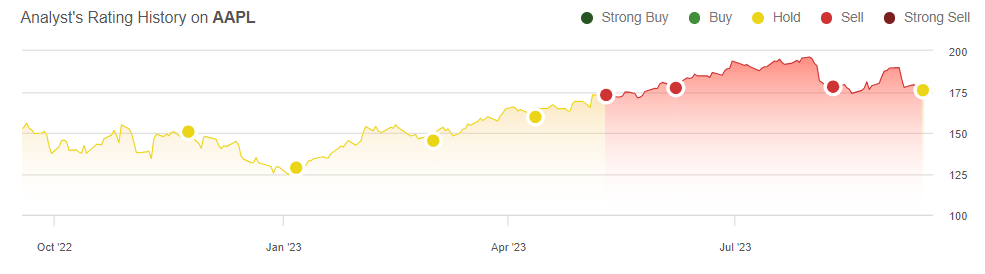

While we received a lot of backlash for our sell-rating on Apple ( AAPL ) from the hardcore Apple bulls, our negative thesis regarding iPhone sales growth suffering due to the worsening macro backdrop in China, the rest of Asia, the U.S. and Europe has played out; this quarter, Apple reported iPhone sales dropping QoQ and Y/Y. The 2023 smartphone total addressable market ("TAM") continues to contract Y/Y; since last quarter, we've revised our 2023 smartphone TAM to be -5-15% Y/Y revised, down from 0-5%. Additionally, this quarter has posed new risks to Apple, i.e., the Huawei Mate 60 Pro pressuring market share and rumors of China banning iPhone use among central government employees. We upgraded the stock to a hold in mid-September as we now believe the stock has priced in the current headwinds from China, but we continue to see the uncertain macro environment weighing on iPhone sales in spite of the iPhone 15 launch. The following graph outlines our rating history on Apple.

{kind=link}

Timing Is Everything; Where We Could've Gone Better

We operate in the business of calculated predictions and follow the motto of buy low, sell high . We've been expanding our coverage of the cybersecurity space this quarter - looking into Zscaler (ZS), CrowdStrike (CRWD), and Snowflake ( SNOW ), among others. While cybersecurity remains a top IT spending priority even during market downtrends, we think this quarter highlighted that the space is not immune to the cost-conscious environment. We continue to expect Palo Alto Networks ( PANW ) and CrowdStrike to be among the better-positioned names to outperform in 2H23, but we don't think this sentiment extends to Fortinet (FTNT). We think Fortinet was less resilient than expected due to macro headwinds tightening customer budgets.

What's Next In 4Q23?

We continue to see a more volatile market in 2H23, but we believe there remain outperformers in the software/hardware and semi mix in 2H23. We think the promises of A.I.-driven growth will materialize in the longer term but don't see companies aside from NVDA benefiting materially from the A.I. boom in the near-term. We think this quarter was proof to investors that the A.I. rally in 1H23 was driven by market noise rather than fundamentals, and expect to see a shift in sentiment into the next quarter. We still think investors are getting stuck in a chase to find the next NVDA, expecting NVDA's growth rate next year to be inferior to its current momentum; we're seeing investors cut down their position at current levels over the past month. We also think the semi space will be more increasingly volatile as geopolitical tensions between the U.S. and China increase and the latter's economic recovery slows. We now think the market is no longer attempting to wait out the worsening macro backdrop as stocks confront their A.I. promises and macro headwinds.

For further details see:

Back To The Future 5.0 Post-Earnings Review