AGNCP - Bad Time To Buy AGNC

2023-09-18 18:00:19 ET

Summary

- AGNC Investment Corp. has reached a high valuation as investors focus on the big dividend. They have forgotten how mortgage REITs work.

- Valuing a REIT based only on the dividend leads to poor choices, and investors should consider earnings and understand how they work.

- AGNC's high earnings yield on book value does not mean they are better at managing money compared to other companies in the sector. Not even close.

- Welcome to school. Class in session.

AGNC Investment Corp. ( AGNC ) has reached an exceptionally high valuation. It appears investors have forgotten how mortgage REITs work. They've become complacent as they focus on the big dividend. Let me be perfectly clear. This is the message:

The dividend rate is the amount the board of directors decides to declare as the dividend. It can change rapidly. It is not the right tool for fundamental valuation. Dividends are an important part of returns, but valuing a REIT based only on the dividend leads to terrible choices. If you want to consider earnings, you should know how they work.

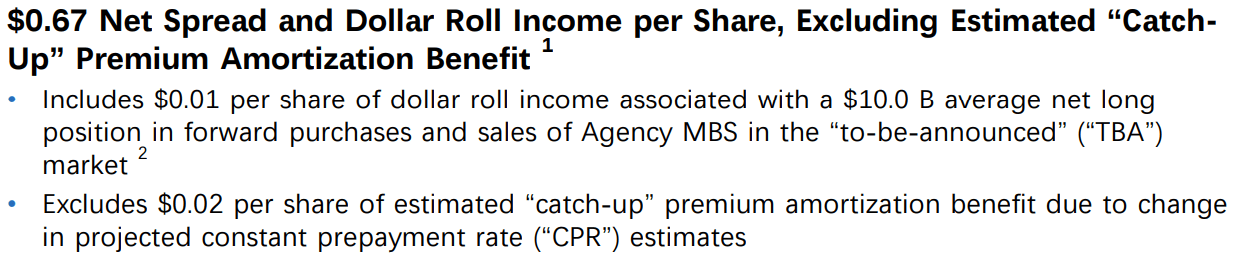

Net Spread and Dollar Roll Income

We typically talk about earnings for mortgage REITs as "Core EPS". That was the most common term for quite a while. AGNC uses a different term, but it refers to the same set of calculations:

{kind=link}

Seems great? Annualized that would be $2.68. That's amazing for a mortgage REIT that ended Q2 2023 with $9.39 in tangible book value per share.

Sorry. The text doesn't convey the tone all that well. Try reading it out loud and drag that "amazing" out for about seven seconds of sarcasm.

That annualized value of $2.68 implies a 28.5% earnings yield on trailing tangible book value per share. Is that something that can be sustained?

Meghan Trainer said it best:

No, no, no.

Don't blame me for bringing in some basic math. Remember when everyone was scared about the yield curve inverting? What happened? AGNC found a way to post extremely high earnings relative to the remaining book value.

Welcome to Elementary

This isn't just an elementary school deprived of funding, using old books, and claiming pizza should count as a vegetable. You're in my school now.

Remember when AGNC thought it was a good idea to issue more than 10 million shares at an average price below $10? AGNC remembers:

{kind=link}

Why would AGNC issue those shares? Because that's what they do when they trade at a premium (especially a big premium) to book value. Why? Because book value is the cornerstone of analysis.

Who thinks AGNC is vastly better at managing capital than Annaly Capital Management ( NLY ), Dynex Capital ( DX ), Rithm Capital Corp. ( RITM ), PennyMac Mortgage ( PMT ), and Ready Capital ( RC )?

People who haven't read my articles probably think AGNC's bigger earnings yield on book value proves they are better at managing money.

Open up your history books!

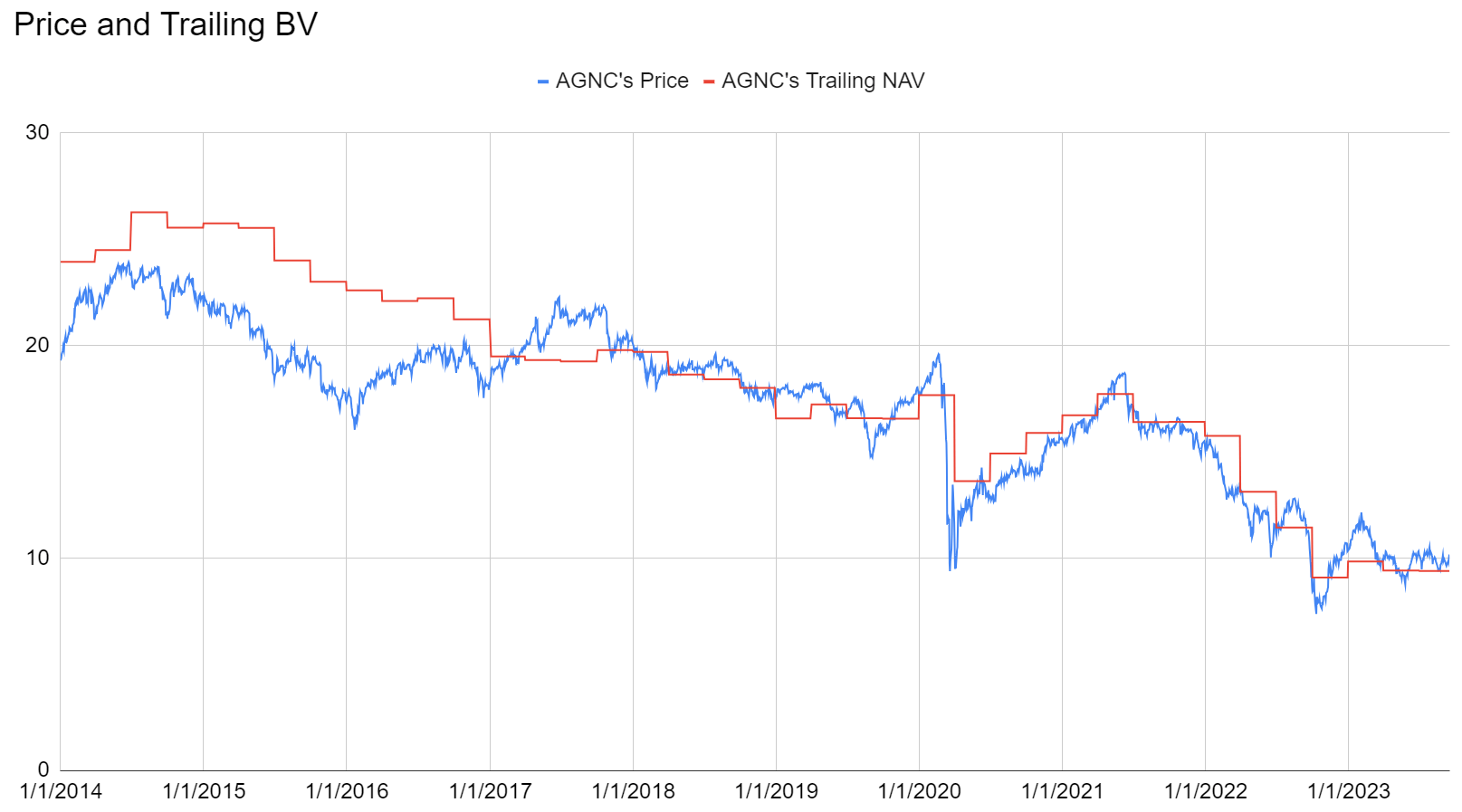

Here's AGNC's price history charted with trailing book value per share:

{kind=link}

How impressed are you right now?

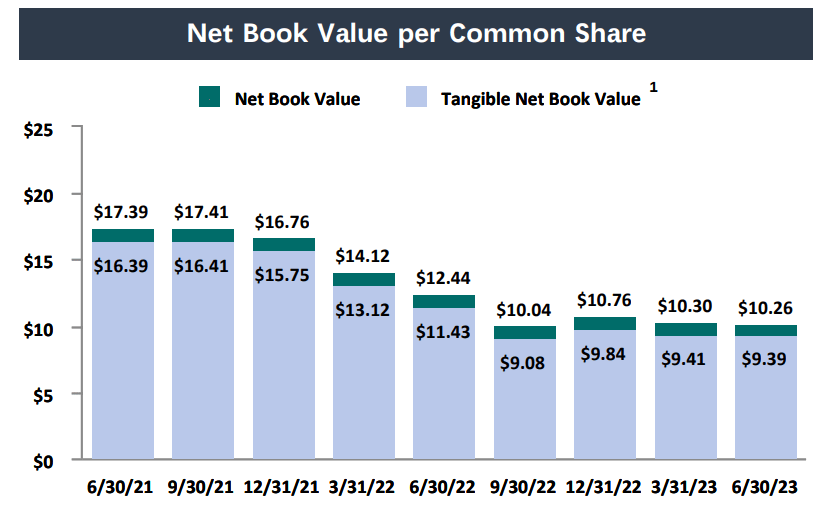

We run a series of articles covering projected book value per share and updated ratings most weeks. For this article, we're just using the official values from the end of the quarter, so it doesn't update between quarters.

Here's a chart from AGNC covering book value per share for part of the period:

{kind=link}

Cool.

How about another history lesson?

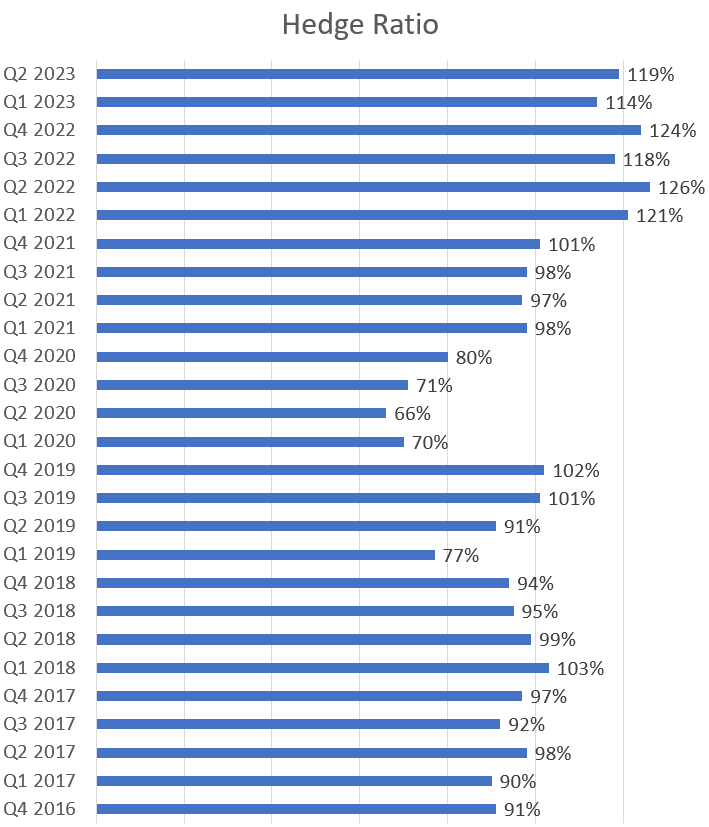

This is how AGNC's hedge ratio developed over the last several years:

Author's Chart, Data from AGNC presentations for Q2 2023, Q1 2021, and Q4 2018

{kind=link}

Notice how the hedge ratios are much higher now? What happened? The yield curve is inverted. Interest rate hedges are actually producing a material amount of net interest income today.

It's time for some math.

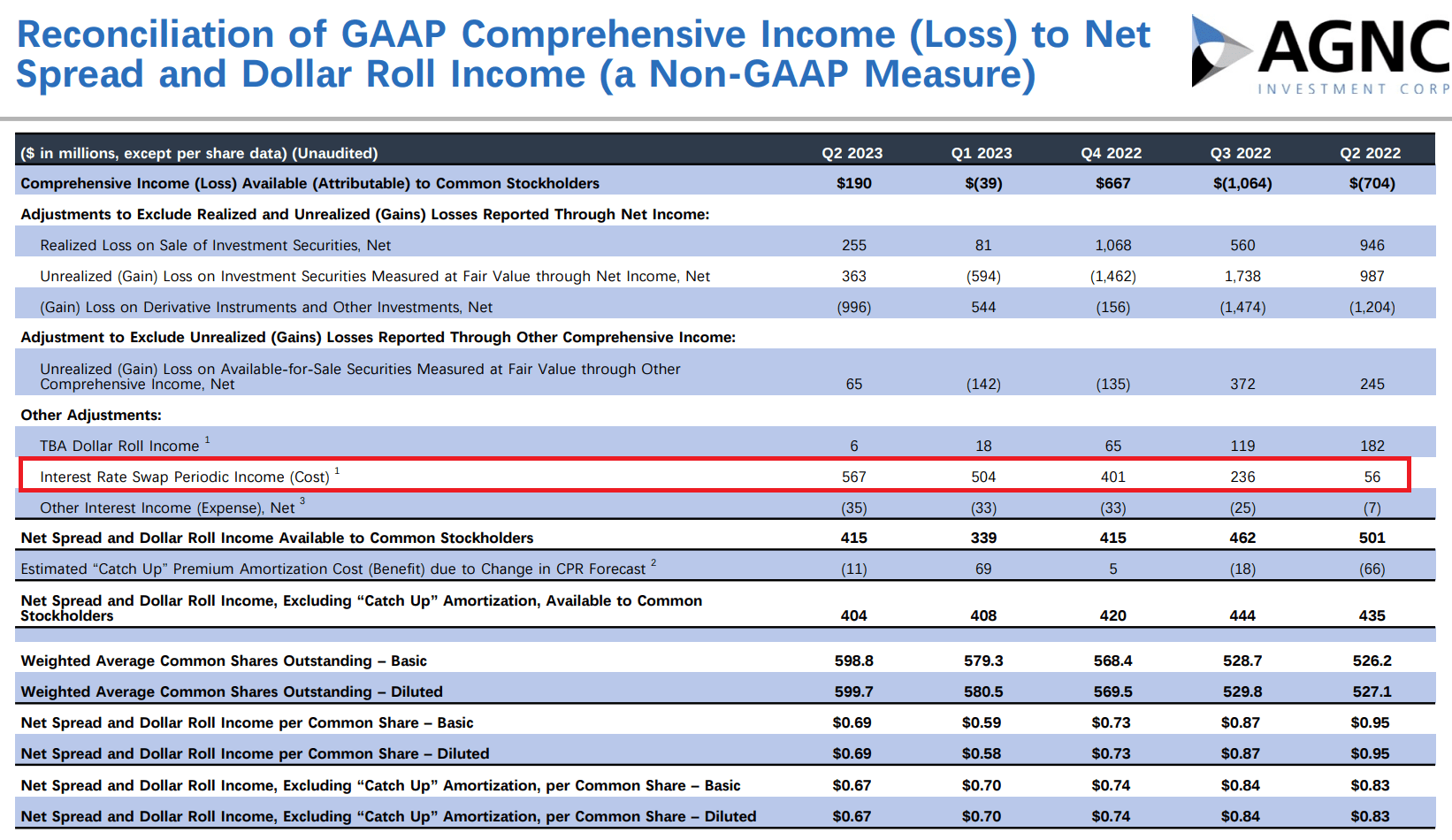

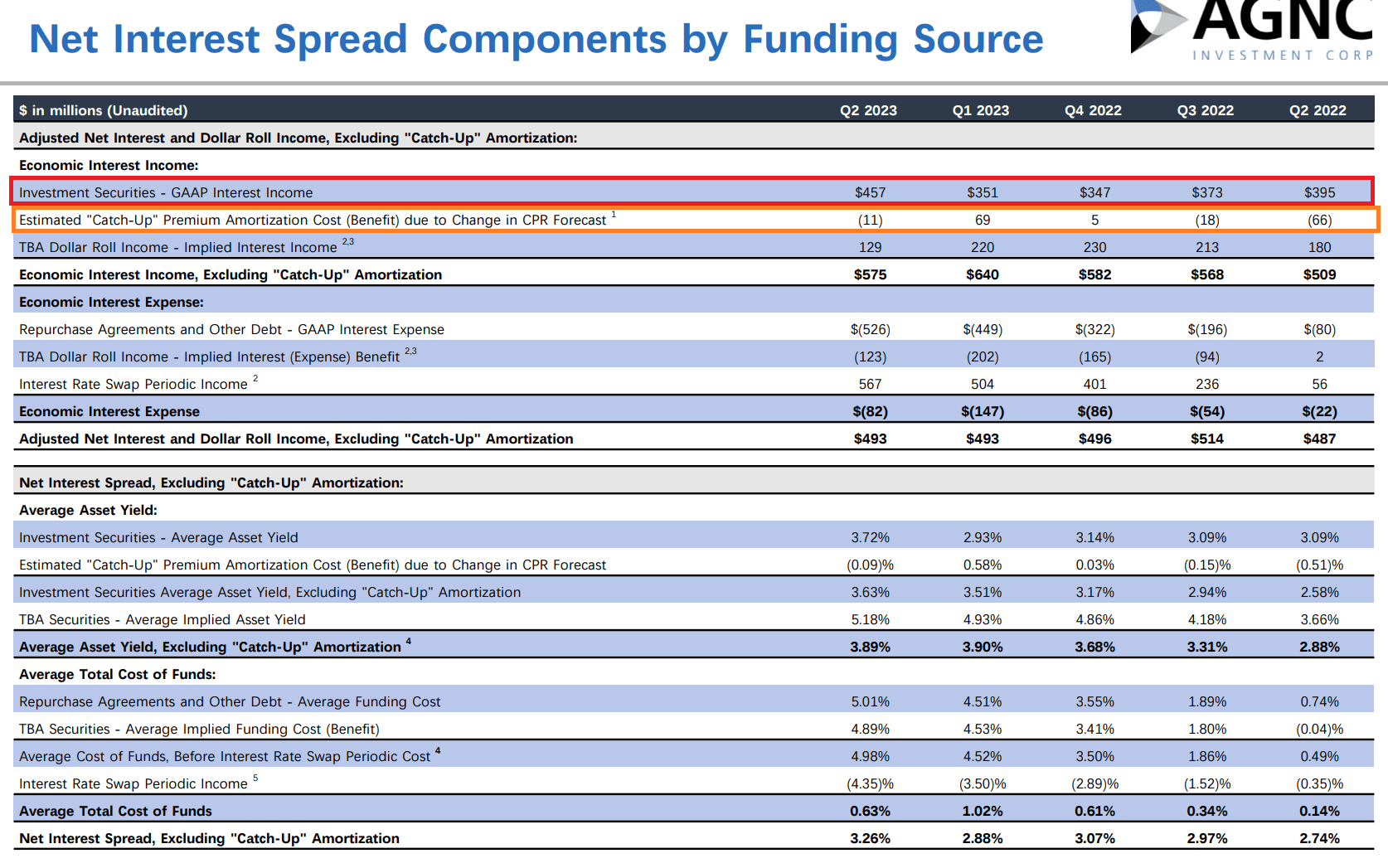

Take a look at the difference between the repo cost for AGNC and the cost of funds AGNC is including in their period interest expense:

AGNC

See how the average cost of 5.01% is vastly higher than the cost left after applying adjustments. The big factor here comes from interest rate swaps. AGNC is earning a very attractive amount of net interest income from their swaps. However, the net present value of all those cash flows is already included in the book value. It simply flows through the income statement each quarter as net interest income.

Want to see it? OK, this is where it goes:

{kind=link}

For reference, in the last three quarters the value for "Interest Rate Swap Periodic Income" has been greater than the total interest income under GAAP on their assets. Of course, GAAP figures for mortgage REITs can have some flaws. However, even if we adjust for premium amortization adjustments, the interest income from assets wouldn't match the interest income from swaps.

{kind=link}

Let me make this crystal clear. If AGNC sold some older MBS with a historical yield on cost of around 3% and closed out the repo financing (which is running about 5%), that would inflate their net interest income even further.

Congratulations. Now you know more about mortgage REIT accounting than many investors in the sector. Have a nice day.

Conclusion

There are some pretty good deals in the mortgage REIT sector. This is not one of them. Do I like anything about AGNC? Sure, I think preferred shares are pretty nice. I often have some of those in my portfolio, and I trade between them from time to time based on relative valuation. I expect to continue doing that.

I wouldn't want to buy AGNC common shares here. By our estimates, book value per share is down again in Q3 2023. I think the price-to-book ratio is materially too high. The one nice thing I will say is that Treasury to MBS spreads are quite high.

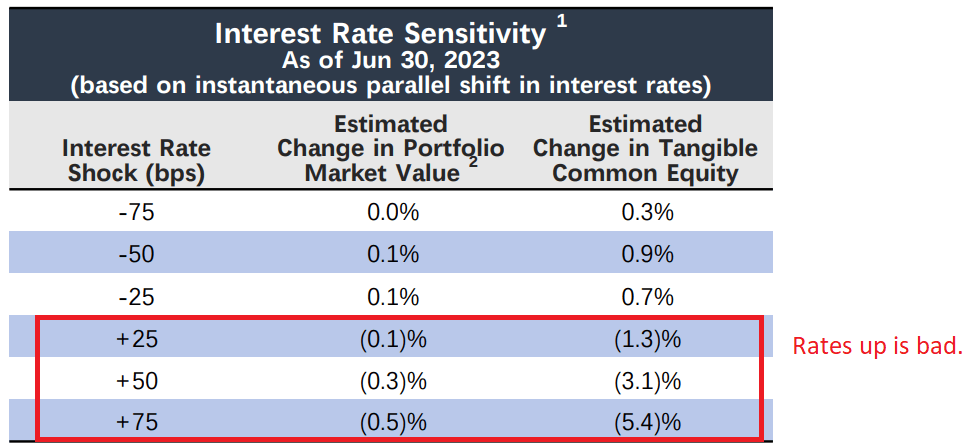

That's positive for total economic returns because it implies mortgages actually have pretty high yields compared to other securities. However, part of the higher yield is offsetting the negative convexity. When interest rates move significantly in either direction, that's generally bad for mortgage REITs. As of the end of Q2 2023, AGNC was positioned to hedge primarily against interest rates going down, not going up.

{kind=link}

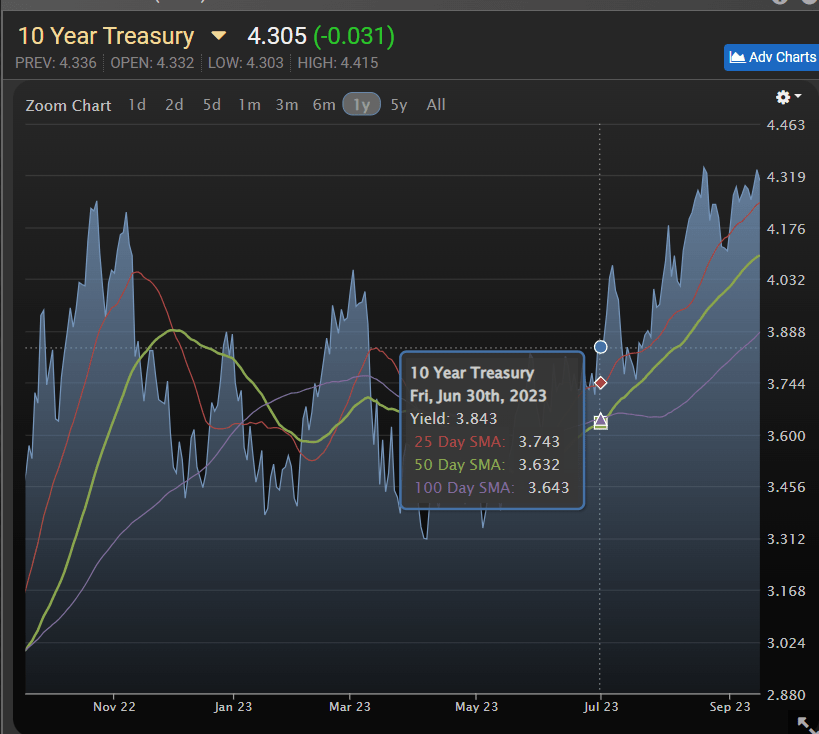

Do you think rates went down or up?

{kind=link}

Yeah, they went up. Not great. I expect investors to get better opportunities in the future.

For further details see:

Bad Time To Buy AGNC